Joint Tenancy vs Tenancy in Common Singapore 2026: Which Is Right for You?

When two or more people purchase a property together in Singapore, they must choose between two legal ownership structures: Joint Tenancy (JT) or Tenancy in Common (TIC). This choice has significant consequences for estate planning, ABSD exposure, CPF usage, and how the property is inherited on the death of one owner. It is also at the centre of several controversial IRAS-flagged property structuring strategies, including the now-notorious “99-to-1” arrangement that attracted an anti-avoidance warning in April 2023. This guide explains each structure clearly, with worked ABSD scenarios and estate-planning implications for Singapore buyers in 2026.

Quick Answer — Key Takeaways

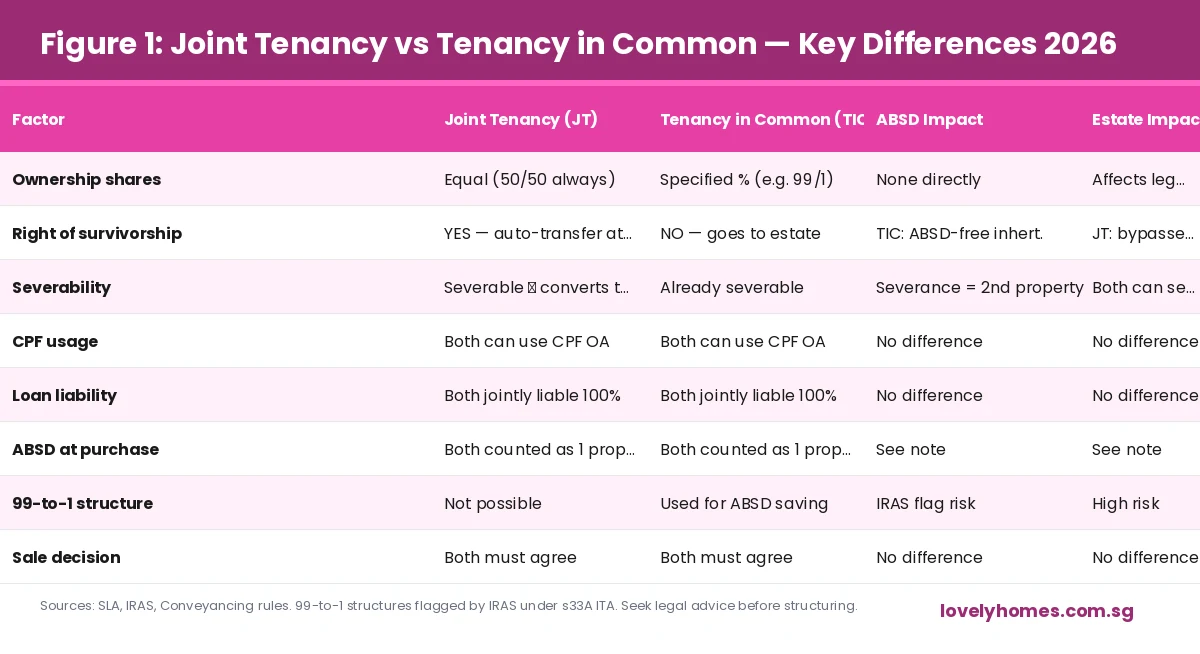

- Joint Tenancy (JT): Both owners hold equal undivided shares. On death, the surviving owner automatically inherits the deceased’s share by the right of survivorship — bypassing probate. Commonly used by married couples for matrimonial homes.

- Tenancy in Common (TIC): Owners hold specified percentage shares (e.g. 60/40, 99/1). Each owner’s share forms part of their estate on death and is distributed per their will or intestacy laws. More flexible but requires careful estate planning.

- ABSD risk for TIC: The IRAS has flagged TIC structures (especially 99/1 and 1/99) as potentially falling within the anti-avoidance provisions of Section 33A of the Income Tax Act if the primary purpose is ABSD avoidance. Seek legal advice before using TIC for tax-saving purposes.

- You can convert: A JT can be severed (converted to TIC) by any one owner’s unilateral act of severance. Conversely, TIC owners can merge their interests into a JT by mutual agreement.

- CPF usage: Both JT and TIC allow CPF OA usage for the property purchase, subject to the CPF Withdrawal Limit. CPF accrued interest is charged on the amount withdrawn and must be refunded on sale.

- Decoupling: TIC is the starting structure for a decoupling exercise, where one co-owner sells their share to the other — but this has ABSD and legal risks. See our decoupling guide for the full analysis.

What Is Joint Tenancy in Singapore?

Joint Tenancy (JT) is an ownership structure in which two or more co-owners hold a property collectively without any specified individual share. Each joint tenant holds an undivided interest in the entire property — not a 50% slice, but a whole-of-property interest held simultaneously with the other joint tenants. The four unities of Joint Tenancy must be present: unity of time (same time of acquisition), unity of title (same instrument of transfer), unity of interest (equal shares), and unity of possession (equal right to possess the whole property).

The defining feature of Joint Tenancy is the right of survivorship (jus accrescendi). On the death of one joint tenant, their interest in the property automatically passes to the surviving joint tenant(s) — regardless of what the deceased’s will says. The property does not form part of the deceased’s estate and does not go through probate. This makes JT the preferred structure for married couples who want a simple, automatic estate outcome without the complexity and delay of probate proceedings.

What Is Tenancy in Common in Singapore?

Tenancy in Common (TIC) is an ownership structure in which co-owners hold specified, separate shares of the property. Unlike JT, TIC owners do not hold the property collectively — each holds a defined percentage (e.g. 70% / 30%, or 99% / 1%) that can be independently dealt with, mortgaged, or bequeathed. Only unity of possession is required — TIC owners need not have acquired the property at the same time or under the same instrument.

On the death of a TIC owner, their share does not pass automatically to the other co-owner(s). Instead, it becomes part of the deceased’s estate and is distributed according to their will (or under the Intestate Succession Act if there is no will). This means TIC ownership requires more deliberate estate planning — but it also provides greater flexibility for owners with different estate objectives, different financial contributions to the purchase, or different intended inheritance outcomes.

ABSD and Ownership Structure — The Critical Interaction

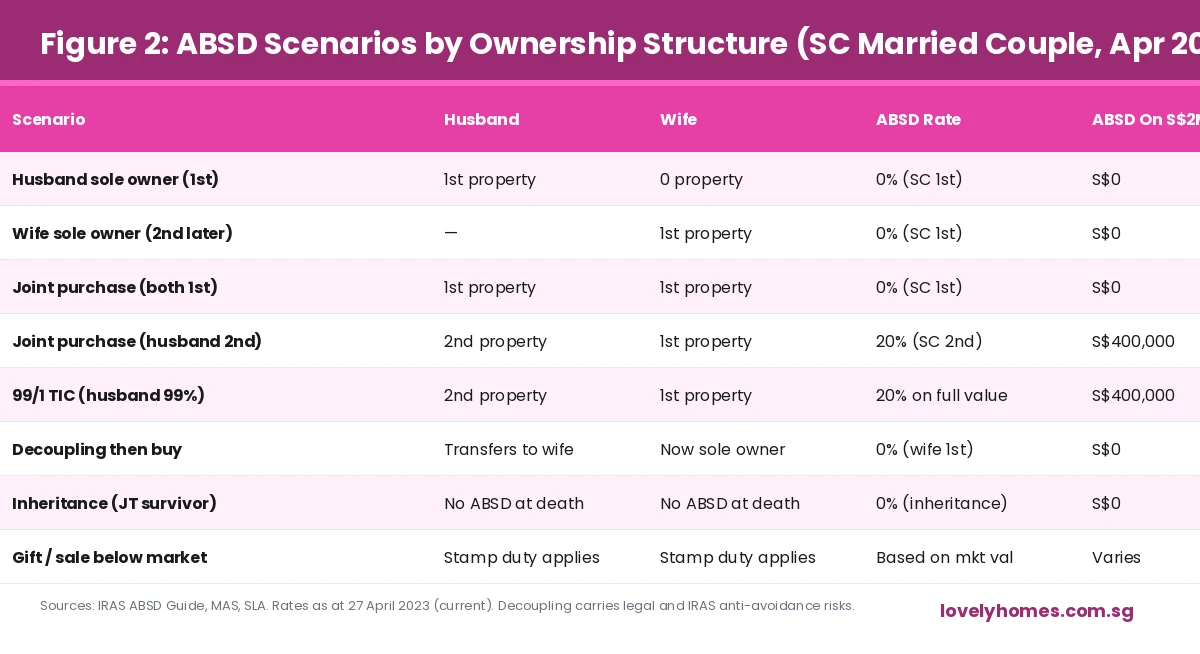

The most important practical difference between JT and TIC for Singapore property buyers in 2026 is how each structure interacts with Additional Buyer’s Stamp Duty (ABSD). ABSD is calculated based on the higher of the two co-buyers’ property count. If a Singapore Citizen (SC) husband who already owns a property buys with his SC wife who has no property, the purchase is treated as a “second property” for ABSD purposes — attracting 20% ABSD on the full purchase price — regardless of whether they use JT or TIC.

The ABSD rules were deliberately designed to prevent ownership structuring from being used as an ABSD avoidance mechanism. A 99/1 TIC arrangement — where the husband holds 1% and the wife holds 99%, ostensibly making the wife the “primary” owner — does not reduce the ABSD payable. IRAS applies ABSD based on each buyer’s property count. If the husband (with existing property) is on the title at all, the purchase is assessed at his higher ABSD rate on the full market value. The IRAS also has Section 33A anti-avoidance powers that can be invoked where an arrangement’s primary purpose is ABSD avoidance — potentially leading to reassessment, penalties, and interest.

Summary: Key Differences at a Glance

| Dimension | Joint Tenancy | Tenancy in Common |

|---|---|---|

| Individual share specified? | No — equal undivided interest | Yes — e.g. 70/30, 99/1 |

| Right of survivorship? | Yes — auto-passes on death | No — goes to estate |

| Can be bequeathed in will? | No (survivorship overrides will) | Yes |

| Probate required on death? | No | Yes (for the deceased’s share) |

| ABSD treatment | Higher count of any co-owner applies | Higher count of any co-owner applies |

| Convertible to the other? | Yes — by severance (any 1 owner) | Yes — by agreement (all owners) |

| Typical use | Matrimonial home, equal-share investment | Unequal contributions, estate planning |

| Decoupling suitability | Must sever to TIC first | Directly usable (with risks) |

Worked Example: Estate Planning with TIC vs JT

Scenario: Mr Tan (60%) and Mrs Tan (40%) own a S$3M condo in TIC

How to Convert Between Joint Tenancy and Tenancy in Common

Converting from Joint Tenancy to Tenancy in Common (severance) can be done unilaterally by any one joint tenant — it does not require the consent of the other co-owner(s). A joint tenant serves written notice of severance on the other co-owner(s), and a declaration is registered with the Singapore Land Authority (SLA). Upon registration, the JT converts to a TIC in equal shares (e.g. 50/50 for two former joint tenants). If the severing party wants unequal shares, they must transfer the relevant portion of their interest to the other co-owner — which may attract stamp duty and ABSD if the recipient thereby “acquires” an additional property interest.

Converting from Tenancy in Common back to Joint Tenancy requires the agreement of all co-owners and the re-execution of a transfer instrument, registered with SLA. The four unities must be re-established. This is less common but may be appropriate when co-owners who originally split their shares for estate planning purposes later want to consolidate for simplicity.

The 99-to-1 Structure and IRAS Anti-Avoidance

The “99-to-1” or “1-to-99” TIC structure gained notoriety in Singapore around 2021–2022 as a mechanism purportedly used by married couples to reduce ABSD. The arrangement involves one spouse (who already owns a property) purchasing just 1% of a new property, while the other spouse (who owns nothing) purchases 99%. The intended logic was that the 99% owner — being a “first-time buyer” — would attract 0% ABSD on their 99% share, with only 1% of the value attracting the higher ABSD rate.

IRAS expressly addressed this in April 2023, clarifying that ABSD applies to the full value of the property for each buyer, based on the buyer’s property count — not proportionate to their ownership share. A husband who buys even 1% of a property where he already owns another property is treated as a “second property” buyer on the full purchase price. Additionally, IRAS warned that 99-to-1 arrangements could be subject to the general anti-avoidance provision in Section 33A of the Income Tax Act, which empowers IRAS to disregard or reconstruct transactions that are not entered into for bona fide commercial reasons, or that are primarily for the purpose of obtaining a tax advantage. Buyers who have entered into such arrangements are advised to seek a legal opinion on their exposure.

What This Means for You in 2026

For most married couples buying their first home together, Joint Tenancy remains the simpler and more appropriate structure. The right of survivorship provides automatic estate protection without the cost or complexity of probate, and the equal share assumption aligns with the typical matrimonial home context. For investors, business partners, or co-owners with meaningfully different financial contributions or different estate objectives, Tenancy in Common with a clearly drafted will is the more appropriate structure — but it requires professional legal advice to ensure the intended outcome.

The ABSD landscape of 2026 has made property ownership structuring significantly more fraught. The 60% ABSD on foreign purchases, the 20% on SC second properties, and IRAS’s active anti-avoidance posture mean that creative structuring carries real legal risk. The safest path is to engage a conveyancing solicitor and a property tax advisor before executing any co-ownership arrangement, particularly where one of the buyers already holds a residential property.

What Might Come Next

There is ongoing industry discussion about whether Singapore’s ABSD regime will be relaxed for specific categories — particularly the 60% foreign-buyer rate, which has significantly reduced CCR transaction volumes since 2023. Any reduction in foreign ABSD could trigger a wave of CCR resale activity, changing the dynamics for TIC investors who hold CCR properties jointly with foreign spouses. On the estate-planning side, Singapore does not currently impose inheritance tax or estate duty (abolished in 2008) — meaning TIC inheritance of property is tax-free. Should Singapore ever reintroduce estate duty as part of a broader fiscal package, TIC structures with careful will-drafting could become even more strategically important.

Related Articles

Frequently Asked Questions

Can a husband and wife hold a property in different ownership structures for different properties?

Does Tenancy in Common affect the CPF usage rules?

Can a foreigner co-own a Singapore private condo as a Tenancy in Common co-owner?

What happens to a joint tenancy when the parties divorce?

Is there stamp duty payable when converting from Joint Tenancy to Tenancy in Common?

Can I leave my Tenancy in Common share to anyone I choose in my will?

DISCLAIMER: All information in this article is for general informational and educational purposes only and does not constitute legal, tax, or financial advice. Ownership structuring decisions have significant stamp duty, estate, and legal implications. The IRAS anti-avoidance provisions under Section 33A of the Income Tax Act can apply to arrangements entered into for the purpose of obtaining a tax advantage. Readers should consult a qualified conveyancing solicitor and a property tax advisor before making any ownership structuring decisions. LovelyHomes.com.sg is an independent editorial platform. Refer to official sources: IRAS (iras.gov.sg), SLA (sla.gov.sg), CPF Board (cpf.gov.sg), Ministry of Law (mlaw.gov.sg).

0 Comments