ABSD Singapore — short for Additional Buyer’s Stamp Duty — is the single largest upfront cost most buyers face when purchasing a second (or third, or fourth) residential property in Singapore. If you are buying as a foreigner, ABSD can add 60% of the purchase price to your cost. If you are a Singapore Citizen buying your second property, that figure is 20%. Get this number wrong in your budgeting, and you can very quickly wipe out years of planning.

This guide walks you through exactly how ABSD works in 2026 — who pays, how much, how it is calculated, what remissions are available, and the legitimate strategies property buyers use to manage it. All figures reflect the Government’s 27 April 2023 cooling measures, which remain the applicable framework. For the latest rates, always check the IRAS Additional Buyer’s Stamp Duty page.

Quick Answer — ABSD at a glance

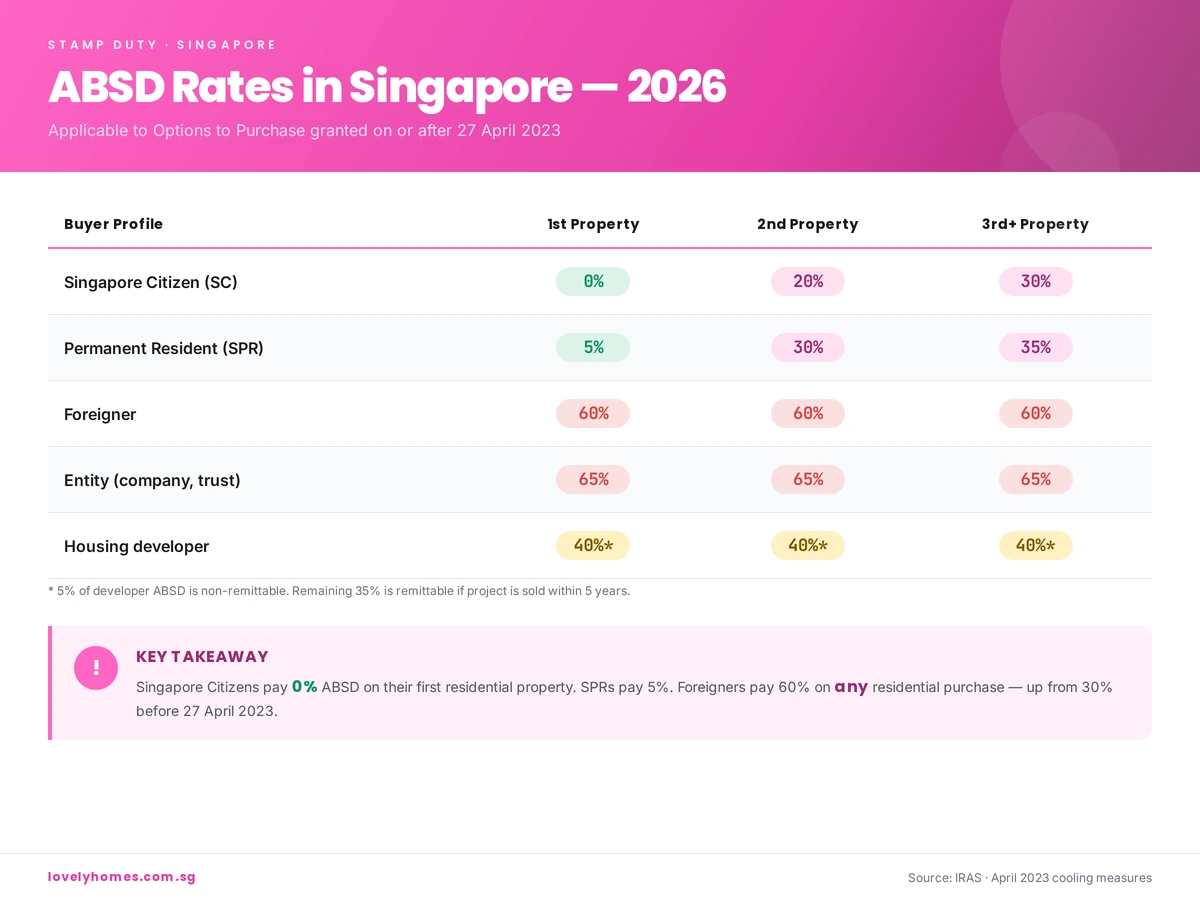

Singapore Citizens: 0% on 1st property, 20% on 2nd, 30% on 3rd+

Singapore PRs: 5% / 30% / 35%

Foreigners: 60% on any residential property

Companies, trusts and other entities: 65%

ABSD is payable within 14 days of signing the Option to Purchase (OTP) or Sale & Purchase Agreement.

What is ABSD and Why Does It Exist?

ABSD is a transaction tax levied on the buyer when acquiring a residential property in Singapore. It sits on top of the regular Buyer’s Stamp Duty (BSD) that every buyer pays. Where BSD is progressive and maxes out at 6% for the portion of price above S$3 million, ABSD is a flat rate applied to the entire purchase price or market value (whichever is higher).

The tax was introduced in December 2011 as part of the Government’s suite of cooling measures — the tools Singapore uses to moderate speculative demand, manage affordability for owner-occupiers, and prevent the kind of runaway price inflation seen in other global cities. Because it targets second-and-subsequent-property buyers and non-citizens disproportionately, ABSD is the single most powerful lever in the cooling-measures toolbox. You can read more about the broader framework in our Property Cooling Measures section.

ABSD Rates in Singapore (2026)

The table below sets out the ABSD rates currently in force. Rates apply based on the profile of the buyer at the time the Option to Purchase (OTP) is granted.

ABSD rates by buyer profile — applicable to OTPs granted on or after 27 April 2023.

Buyer Profile

1st Residential Property

2nd Residential Property

3rd & Subsequent

Singapore Citizen (SC)

0%

20%

30%

Singapore Permanent Resident (SPR)

5%

30%

35%

Foreigner (non-PR individual)

60%

60%

60%

Entity (e.g. company, trustee for a trust)

65%

65%

65%

Housing developer

40%*

40%*

40%*

* 5% of a developer’s ABSD is non-remittable. The remaining 35% is remittable subject to conditions, including selling all units in a qualifying project within five years.

How ABSD is Calculated — A Worked Example

ABSD is applied to the higher of the purchase price or the market value of the property. It is not charged on a tiered basis — the full rate applies to the entire amount.

Example: A Singapore Citizen couple already owns their first home (a 4-room HDB flat). They decide to buy a S$2,000,000 resale condominium in District 15 as an upgrader investment. ABSD on the second property for a Singapore Citizen is 20%.

Purchase price: S$2,000,000

ABSD (20%): S$400,000

BSD (progressive, on S$2m): approximately S$64,600

Total stamp duty payable: S$464,600

That S$400,000 ABSD alone would consume most of the typical upgrader’s CPF and cash reserves. This is why many Singaporean couples take the ‘sell first, buy second’ upgrade route — selling the existing HDB or condo before buying the next home — which we cover later in this guide.

Who Pays ABSD? Exemptions and Special Cases

ABSD applies when you purchase an additional residential property. Commercial property, industrial property, and pure-land parcels are not within its scope. A property is counted toward your “property count” if:

You hold the title as a sole owner, joint tenant, or tenant-in-common;

You are a beneficial owner via a trust;

You are a beneficiary of an estate that holds residential property.

Properties not counted include: properties you merely reside in but do not own (e.g. as a tenant), inherited shares in a deceased estate within the administration period, and certain industrial/commercial units.

Executive Condominiums (ECs)

For new ECs bought directly from the developer during the minimum occupation period of the scheme, ABSD is not triggered because the buyer must commit to an owner-occupier arrangement. ABSD rules apply normally if an EC is purchased on the resale market after its 5-year MOP and 10-year privatisation milestones.

Free Trade Agreement (FTA) Nationals

Citizens and Permanent Residents of countries with which Singapore has an FTA extending National Treatment on stamp duty — namely Iceland, Liechtenstein, Norway, Switzerland, and United States citizens — are accorded the same ABSD treatment as Singapore Citizens. An eligible US citizen buying their first Singapore residential property therefore pays 0% ABSD, not 60%.

ABSD Remission Schemes — How to Get Some (or All) of It Back

Several remission schemes let qualifying buyers claim back part or all of the ABSD they initially pay. The big three to know are:

1. Married Couple Remission (Sale of First Residential Property)

If a Singapore Citizen (or mixed SC & SPR, SC & foreigner) couple buys a replacement home before selling their existing one, they can apply for ABSD remission provided they sell the first property within six months of the later of (a) the date of purchase of the replacement property, or (b) the TOP/CSC date if buying an uncompleted unit. This is effectively a “grace period” that allows upgraders to move without double-paying ABSD.

2. Mixed-Nationality Married Couples

An SC spouse married to a foreigner buying a matrimonial home jointly can enjoy SC rates (rather than foreigner rates) if the property will be used as their matrimonial home and conditions are met. Again, for a first joint home this means 0% ABSD.

3. Developer ABSD Remission

Licensed housing developers pay 40% ABSD upfront (5% non-remittable, 35% remittable) on land purchased for residential development. The 35% is remittable upon meeting development and sales conditions — typically completing the project and selling all units within 5 years.

Remissions must be applied for within strict timeframes (usually 14 days of the triggering event). We strongly recommend engaging a conveyancing lawyer who is experienced in stamp-duty remission applications before signing any OTP where remission will be relied upon.

ABSD vs BSD: What is the Difference?

Every property purchase in Singapore attracts Buyer’s Stamp Duty (BSD), which is a progressive tax on the purchase price:

1% on the first S$180,000

2% on the next S$180,000

3% on the next S$640,000

4% on the next S$500,000

5% on the next S$1,500,000

6% on the portion above S$3,000,000 (residential only)

BSD applies to every buyer; ABSD is the additional layer that may or may not apply depending on your citizenship status and property count. BSD and ABSD are payable together, within 14 days of signing the OTP.

The History of ABSD in Singapore (2011–2026)

Understanding how we arrived at today’s ABSD rates helps you anticipate where the Government may go next. The key milestones:

December 2011: ABSD introduced. Foreigners paid 10%; entities 10%; SPRs 3% on 2nd property; SCs 3% on 3rd+.

January 2013: First major hike. Foreigners to 15%, entities 15%, SPRs 5%/10%, SCs 7%/10% on 2nd/3rd.

July 2018: Rates raised again amid a reflating market. Foreigners to 20%, entities to 25%.

December 2021: Another round. Foreigners to 30%, entities to 35%, SPR 2nd property to 25%, SC 2nd to 17% / 3rd to 25%.

April 2023: The current regime. Foreigners doubled to 60%, entities to 65%, SPR 2nd to 30%, SC 2nd to 20%.

Each tightening has coincided with a period of accelerating private-residential price growth. For a full chronology including LTV, SSD and TDSR changes, see our comprehensive Property Cooling Measures archive.

How to Legally Minimise Your ABSD Bill

ABSD is not optional, but there are a handful of legitimate strategies buyers use to reduce the amount payable or to avoid triggering higher rates:

Sell first, then buy. For couples upgrading, timing the sale of your existing HDB or condo before the purchase of the next means you never hold two properties simultaneously and therefore pay 0% ABSD on the new first home (as an SC).

Use the matrimonial home remission. A mixed SC–foreigner couple buying their matrimonial home jointly enjoys SC rates if structured correctly.

Decouple responsibly. Where one spouse transfers their share of an existing property to the other, only the transferring spouse is freed to buy a second property as a “first” purchase. Decoupling has legal, CPF refund, and mortgage implications — always take specialist advice first.

Consider commercial or industrial property instead. Commercial and industrial properties do not attract ABSD. They have their own financing, GST, and tax considerations — but for investors focused on yield, they are worth analysing. See our Property Investment section for how commercial yields compare with residential.

Look offshore for second and third properties. Singaporeans investing in Malaysia (JB/Iskandar), Thailand, the UK, Australia, or Japan pay no ABSD to the Singapore Government for those purchases. Each destination has its own foreign-buyer regime, which we cover in our Foreign Property Investment guide.

Time your citizenship/PR application carefully. For families where PR or citizenship is in progress, the ABSD profile at the date the OTP is granted determines the rate. Moving the OTP date by a few weeks can, in edge cases, change the applicable rate by 15–25 percentage points.

Frequently Asked Questions

Is ABSD payable on the land value or the built-up value?

ABSD is calculated on the higher of the purchase price or the market value of the property at the time of acquisition. For new launches, this is typically the purchase price; for resale, IRAS may apply an independent market valuation.

When exactly is ABSD due?

Within 14 days from the date of the document triggering the duty — usually the signing of the Option to Purchase (for resale) or the Sale & Purchase Agreement (for new launches). Late payment attracts penalties.

Can CPF be used to pay ABSD?

No. ABSD (like BSD) cannot be paid from CPF directly at the point of purchase — it must be paid in cash. You can, however, apply for CPF reimbursement after the stamping is complete, drawing from your Ordinary Account against the purchase price.

Do I pay ABSD if I inherit a property?

No. A property acquired by way of inheritance is not a purchase and does not attract ABSD on the transfer itself. However, an inherited property does count toward your property count for future purchases.

I already own a commercial shophouse. Do I pay ABSD on my residential condo?

The residential-only count means commercial and industrial holdings are not included in your ABSD property count. If you are a Singapore Citizen buying your first residential property while owning commercial real estate, you still pay 0% ABSD.

How does ABSD affect an Executive Condominium purchase?

Buying a new EC from the developer under the EC scheme does not attract ABSD during the initial owner-occupation period. Once an EC is privatised (10 years after TOP) and traded on the open market, normal ABSD rules apply.

What to Do Next

ABSD changes how much house you can afford, how you time an upgrade, and sometimes whether a purchase makes sense at all. If you are weighing your options right now, we suggest three next steps:

If you are an upgrader, study our Upgrader Guide — the sequencing question (sell first vs buy first) is the single biggest lever for managing ABSD.

Review current market conditions in our Property News and Property Trends sections — if further cooling measures are telegraphed, timing your OTP becomes critical.

Looking at a specific development? Our detailed condo reviews — including One Marina Gardens, Arina East Residences, and our Aurea vs Chuan Park showdown — include the full ABSD-inclusive cost breakdown for various buyer profiles, so you can see the true entry cost before committing.

Disclaimer: This guide is for general information only and does not constitute legal, tax, or financial advice. ABSD rates and remission rules change over time. Always verify the current position on the IRAS Stamp Duty page and consult a licensed conveyancing lawyer or tax specialist before acting on any property transaction.

⚡ Quick Answer: Tampines at a Glance — 2026

Location: Planning Area in the East Region (District 18). Approximately 25 km from the CBD.

HDB resale prices: 4-room flats median around S$620,000–S$680,000; 5-room flats S$720,000–S$820,000 (Q1 2026).

Private condo PSF: OCR condos in Tampines trade at approximately S$1,300–S$1,500 psf (Q1 2026).

MRT: East-West Line (Tampines, Simei stations). Cross Island Line (CRL) Phase 2 extension to Tampines slated for completion around 2030.

Top schools: Poi Ching School, St Hilda’s Primary School, Tampines Primary, Ngee Ann Secondary, Anglican High School, Temasek Polytechnic.

Major malls: Tampines Mall, Century Square, Tampines 1, Tampines Hub (Our Tampines Hub — largest in Singapore), IKEA Tampines.

MOP wave: 2,133 Tampines HDB flats clearing MOP 2026–2028 — the third-largest district inflow after Punggol and Queenstown. This is expected to moderately increase resale supply.

Tampines — the largest HDB town in Singapore’s eastern heartland — has long punched above its weight as a residential destination. It is simultaneously a self-contained town (with multiple malls, a regional library, sports hub, hospital and polyclinic all within its borders) and a commuter-friendly node on the East-West MRT line, placing it within striking distance of both Changi Business Park and the CBD.

For property buyers and investors, Tampines in 2026 presents a nuanced picture: a large and stable HDB resale market absorbing a meaningful wave of MOP-cleared flats, a modest but growing private condo pipeline, and the longer-term catalyst of the Cross Island Line (CRL) extension due around 2030. This guide covers everything you need to know — from current property prices and investment returns to schools, amenities and planning outlook — as of 15 May 2026.

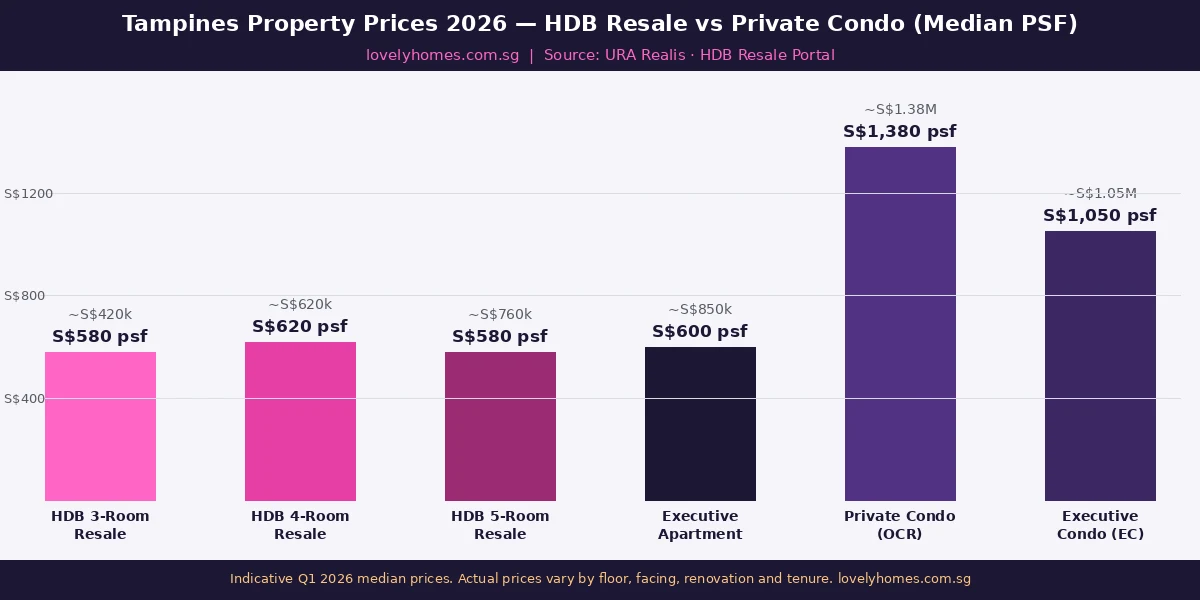

Figure 1: Median transacted PSF and indicative total price for different property types in Tampines, Q1 2026. Source: URA Realis, HDB Resale Portal | lovelyhomes.com.sg

Property Overview: HDB, Executive Condos and Private Residential

Tampines is overwhelmingly an HDB town — roughly 82,000 HDB flats across 12 residential zones house the bulk of its approximately 260,000 residents. The HDB resale market here is liquid, with a steady stream of transactions throughout the year. As of Q1 2026, URA and HDB transaction data indicate the following median price benchmarks:

Property Type

Approx. Median PSF

Approx. Median Price (Q1 2026)

Notes

HDB 3-Room Resale

~S$580 psf

~S$400k–S$450k

Strong demand from singles & couples

HDB 4-Room Resale

~S$620 psf

~S$620k–S$680k

Most liquid segment

HDB 5-Room Resale

~S$580 psf

~S$720k–S$820k

Upgrader-driven demand

Executive Apartment (EA)

~S$600 psf

~S$800k–S$950k

Limited supply; premium over 5-room

EC (e.g. Tampines GreenGems)

~S$1,050 psf

~S$1.0M–S$1.2M

EC rules: income cap S$16k/mth

Private Condo (OCR)

~S$1,380 psf

~S$1.2M–S$1.6M (2BR–3BR)

Small pool of projects; CRL upside

The MOP Wave: 2,133 Tampines Flats Clearing MOP by 2028

One of the most consequential supply-side developments for Tampines’s property market in the near term is the incoming Minimum Occupation Period (MOP) wave. HDB data published in Q1 2026 shows that 2,133 Tampines HDB flats are expected to complete their 5-year MOP between 2026 and 2028 — making Tampines the third-largest contributor to the national MOP wave of 53,816 units, behind Punggol (3,222) and Queenstown (2,405). Flats clearing MOP become available for resale or as platforms for upgrading to private property; a concentrated wave in a single town typically softens short-term resale price appreciation as supply enters the market simultaneously. Buyers looking at Tampines HDB resale should factor this modestly increased supply into their price negotiations over the 2026–2028 window.

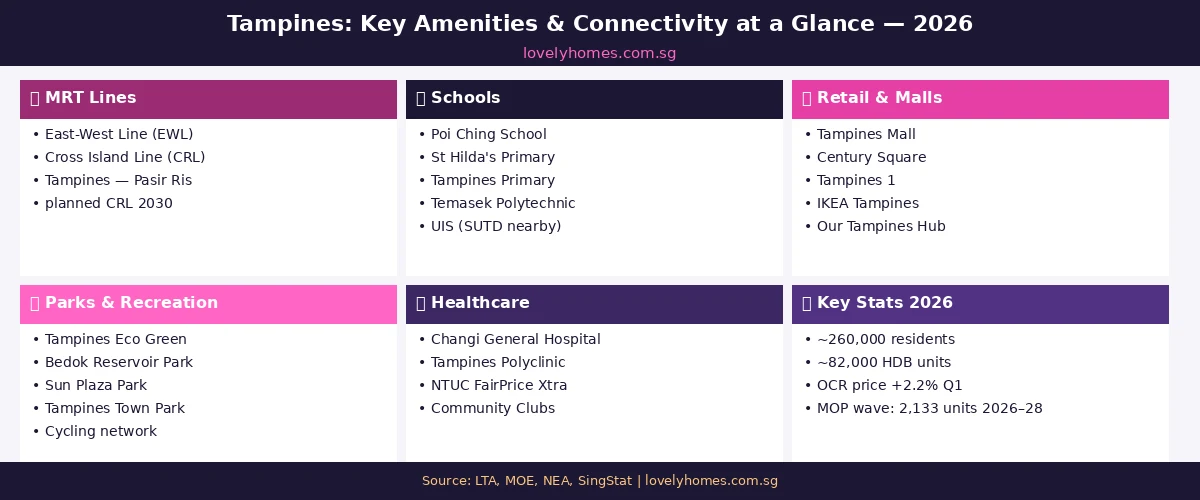

Figure 2: Tampines 2026 — key amenities, transport connectivity, schools, retail and healthcare at a glance. Source: LTA, MOE, NEA | lovelyhomes.com.sg

Transport Connectivity: EWL Today, CRL Tomorrow

Tampines currently has four MRT stations on the East-West Line (EWL): Simei (EW3), Tampines (EW2), Tampines West (DT31, Downtown Line, which serves the western fringe of the estate) and Tampines East (DT32). The EWL provides direct access to Changi Airport (two stops from Tampines EWL), the Changi Business Park cluster, and the CBD via Raffles Place. Typical journey time from Tampines to the City Hall area is 35–40 minutes on the MRT.

The transformative catalyst for Tampines is the Cross Island Line (CRL). The CRL Phase 2 extension — which the Land Transport Authority (LTA) has confirmed will include a Tampines North station — is scheduled for completion around 2030. When operational, this will provide Tampines residents with a second cross-island route connecting them to Punggol, Ang Mo Kio, Buona Vista and eventually West Coast, without requiring a change at Jurong East or Raffles Place. Property-market analysis consistently shows that proximity to new MRT lines generates a measurable premium (typically 5–15% above otherwise comparable units) as the completion date approaches.

Schools: Primary, Secondary and Tertiary

Tampines is well-served by educational institutions at every level, making it a perennial favourite for young families. At the primary level, Poi Ching School and St Hilda’s Primary School are consistently over-subscribed due to strong parent networks and community ties. Tampines Primary and White Sands Primary offer additional places for residents within 1–2 km. For secondary school, Anglican High School, Ngee Ann Secondary and Tampines Secondary serve the estate. At the post-secondary level, Temasek Polytechnic — one of Singapore’s five polytechnics — sits within the Tampines planning area, and the Singapore University of Technology and Design (SUTD) is located in the adjacent Changi area.

For HDB buyers, proximity to a primary school is a priority consideration: within 1 km of an oversubscribed primary school, flats command a premium of up to S$30,000–S$80,000 relative to units further away, according to industry analysis of transaction caveats.

Retail, Recreation and Community Amenities

Tampines has one of the densest concentrations of retail infrastructure of any OCR town. Tampines Mall, Century Square and Tampines 1 — three large malls clustered around the Tampines MRT station — together provide over 400 retail and food-and-beverage tenants. IKEA Tampines (one of only two IKEA outlets in Singapore) and Courts Megastore provide large-format retail. Our Tampines Hub (OTH) — opened in 2017 as Singapore’s largest integrated community and lifestyle hub — includes a hawker centre, library, swimming complex, indoor sports hall and community club all under one roof. Tampines Eco Green, a 36-hectare nature park, provides green space adjacent to the town’s residential estates.

Rental Market: Who Rents in Tampines?

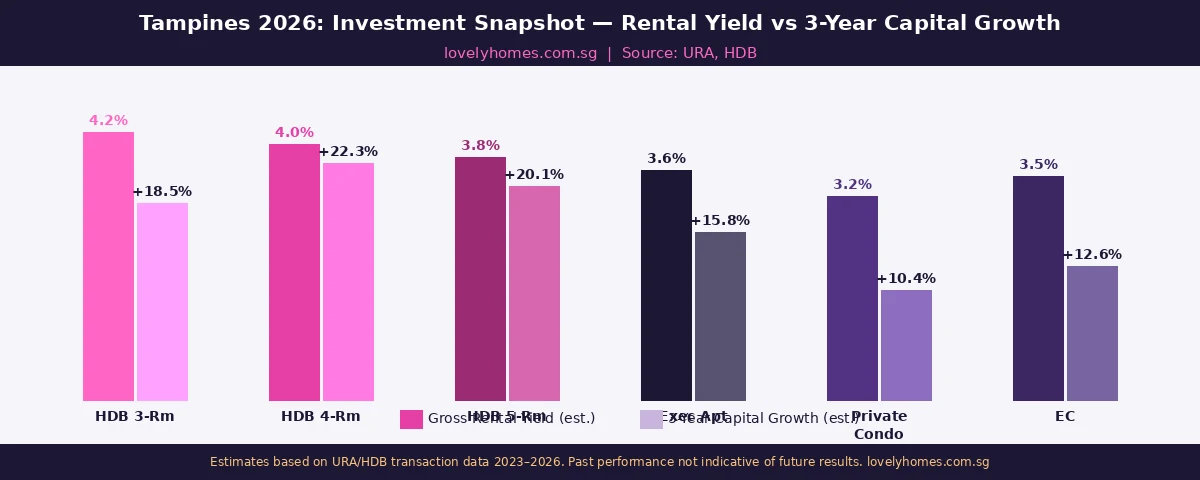

The rental market in Tampines is driven primarily by: (1) expatriate families priced out of CCR/RCR who need proximity to Changi Business Park or Singapore Expo; (2) domestic tenants occupying HDB rooms or whole flats while waiting for BTO completion; and (3) investors holding private condo units between sales. Indicative whole-unit HDB rental rates in Q1 2026 range from approximately S$2,200–S$2,600 per month for a 4-room flat to S$2,600–S$3,200 for a 5-room flat. Private condo 2-bedroom units in Tampines transact at approximately S$3,200–S$4,000 per month. Gross rental yields for HDB units are estimated at 3.8–4.2%, compared to 3.0–3.5% for private condos, reflecting the difference in purchase prices relative to achievable rents.

Figure 3: Tampines — estimated gross rental yield vs 3-year capital growth (2023–2026) by property type. Source: URA, HDB | lovelyhomes.com.sg

Worked Example: HDB Upgrader Buying Tampines Private Condo

Mr and Mrs Wong are Singapore Citizens who purchased a 5-room Tampines HDB flat in 2019 for S$550,000. Their MOP completed in October 2024. By Q1 2026, their HDB flat has appreciated to approximately S$760,000. They wish to sell the HDB and purchase a 3-bedroom private condo in Tampines priced at S$1,400,000.

BSD on new condo: S$1,800 + S$3,600 + S$19,200 + S$16,000 = S$40,600

ABSD: S$0 (SC first property, having sold HDB before purchase)

Down payment (25%): S$350,000 (5% cash S$70,000 + CPF OA S$280,000 — after CPF refund from HDB)

Bank loan (75%): S$1,050,000 at 1.80% for 2 years, 25-year tenure → ~S$4,326/month

Combined gross income needed: S$4,326 ÷ 55% (TDSR) = minimum ~S$7,866/month, leaving ample headroom for the Wongs on a combined S$12,500 income.

What Might Come Next: CRL Uplift and Bayshore Connectivity

The two most significant medium-term catalysts for Tampines property values are the CRL Phase 2 completion (estimated 2030) and the broader development of the Bayshore/East Coast masterplan by URA. The Bayshore GLS site — a mixed-use tender with a tender close date of 15 July 2026 — will unlock a major new residential and commercial node adjacent to the East Coast, which URA envisions as a sea-facing precinct with good walking access to future MRT and park connector links. While Bayshore is not in Tampines per se, the development of the eastern corridor broadly supports demand for Tampines residential property from spillover buyers seeking relative value.

Conversely, the incoming MOP supply wave (2,133 flats by 2028) and the large pipeline of new BTO launches in nearby Tampines (the February 2026 BTO exercise included Tampines North flats) mean that resale HDB price growth in Tampines is likely to moderate compared to the strong gains seen in 2021–2024. Buyers should approach the market with realistic price expectations and longer holding horizons of at least 5–8 years to capture the full CRL uplift.

Frequently Asked Questions

Is Tampines a good area to buy property in Singapore?

Tampines offers strong fundamentals for both owner-occupiers and investors. Its self-contained town infrastructure — multiple malls, good schools, Changi General Hospital, Temasek Polytechnic and extensive recreational facilities — makes it consistently attractive for families. For investors, rental demand from the Changi Business Park and Singapore Expo clusters supports stable occupancy. The CRL Phase 2 extension, expected around 2030, is the single largest near-term price catalyst. However, the incoming MOP wave (2,133 flats clearing by 2028) means short-term HDB resale price growth is likely to be more measured than in the 2021–2023 peak. Private condos in Tampines currently offer better capital appreciation prospects due to limited supply and the CRL premium.

Which MRT stations serve Tampines?

Tampines is currently served by three East-West Line (EWL) stations — Simei (EW3), Tampines (EW2), and the upcoming Tampines East and Tampines West stations on the Downtown Line (DTL). The Cross Island Line (CRL) Phase 2 will add a Tampines North station, providing the estate with a direct diagonal cross-island route to Ang Mo Kio, Jurong and West Coast. LTA has confirmed the CRL Phase 2 alignment; the target completion is approximately 2030. The addition of a second MRT line is historically associated with meaningful property price premiums in Singapore — buyers near the Tampines North CRL station area should monitor land parcel activity and showflat prices in that sub-zone.

What are the best primary schools in Tampines?

The most sought-after primary schools in Tampines, based on past Phase 2C vacancy ballot history, are Poi Ching School (strong CCA and PSLE track record) and St Hilda’s Primary School (historically over-subscribed, alumni-linked admission priority). Within 1 km of these schools, HDB resale flats typically command a meaningful premium. Other well-regarded primary schools in the area include Tampines Primary School, White Sands Primary and Park View Primary. Families who prioritise school proximity should identify units within 1 km of their preferred school and check distance eligibility on the MOE Primary One Registration portal before purchasing.

What is the price difference between Tampines HDB and private condos?

As of Q1 2026, there is a significant price gap between HDB resale flats and private condos in Tampines. A 4-room HDB resale flat trades at approximately S$620,000–S$680,000 (around S$620 psf), while a 2-bedroom private condo trades at approximately S$1.2M–S$1.4M (around S$1,300–S$1,400 psf). This price-per-square-foot premium reflects the private condo’s freehold or 99-year strata title, no income eligibility restrictions, no MOP before resale, private facilities (pool, gym) and the ability to be rented to any nationality. For Singapore Citizens buying a first property, the private condo requires no ABSD but involves a significantly larger financial commitment — especially the 5% mandatory cash down payment (S$60,000–S$70,000 on a S$1.2M–S$1.4M purchase) versus an HDB purchase where no mandatory cash component beyond the option fee is required if using an HDB loan.

How does Tampines compare to Pasir Ris or Bedok for property investment?

Each eastern OCR town has a distinct risk/return profile. Tampines offers the highest liquidity (most transactions per year) and the most comprehensive retail/lifestyle amenities, but the incoming MOP wave will add near-term resale supply. Pasir Ris benefits from the Pasir Ris 8 integrated development (which opened in 2023 adjacent to the new Pasir Ris MRT interchange on the Cross Island Line) and a newer HDB stock profile, giving it stronger near-term price momentum. Bedok is the most mature of the three, with limited new supply and higher PSF for HDB resale (reflecting age-adjusted desirability and proximity to both the EWL and the upcoming Thomson-East Coast Line), but also the smallest pipeline of new private projects. Investors prioritising rental yield may prefer Tampines for its Changi-cluster employment demand; those prioritising capital appreciation may find Pasir Ris’s CRL interchange premium more compelling.

Are there upcoming HDB BTO launches in Tampines?

Yes. Tampines North was included in HDB’s February 2026 BTO exercise with Standard-type flats. HDB has confirmed it will launch approximately 19,600 BTO flats across three exercises in 2026 (February, June and October). Future Tampines BTO projects may include Plus-type classifications under HDB’s new flat classification framework (Standard, Plus, Prime), which affect resale restrictions and subsidy recovery conditions. Buyers considering a BTO in Tampines North (which has proximity to the future CRL Tampines North station) should monitor HDB’s official launch announcements via HDB InfoWEB and the Flat Portal.

Disclaimer: Property prices, rental rates, school enrolment criteria and planning information cited in this article are indicative figures based on publicly available URA, HDB, MOE and LTA data as at May 2026, and are subject to change. This article is for general informational purposes only and does not constitute investment, financial or legal advice. Prospective buyers should conduct their own due diligence, consult a MAS-licensed financial adviser and verify all transaction data on URA Realis, HDB Flat Portal and IRAS before making any property purchase decision. LovelyHomes does not provide brokerage services.

0 Comments