ABSD Singapore — short for Additional Buyer’s Stamp Duty — is the single largest upfront cost most buyers face when purchasing a second (or third, or fourth) residential property in Singapore. If you are buying as a foreigner, ABSD can add 60% of the purchase price to your cost. If you are a Singapore Citizen buying your second property, that figure is 20%. Get this number wrong in your budgeting, and you can very quickly wipe out years of planning.

This guide walks you through exactly how ABSD works in 2026 — who pays, how much, how it is calculated, what remissions are available, and the legitimate strategies property buyers use to manage it. All figures reflect the Government’s 27 April 2023 cooling measures, which remain the applicable framework. For the latest rates, always check the IRAS Additional Buyer’s Stamp Duty page.

Quick Answer — ABSD at a glance

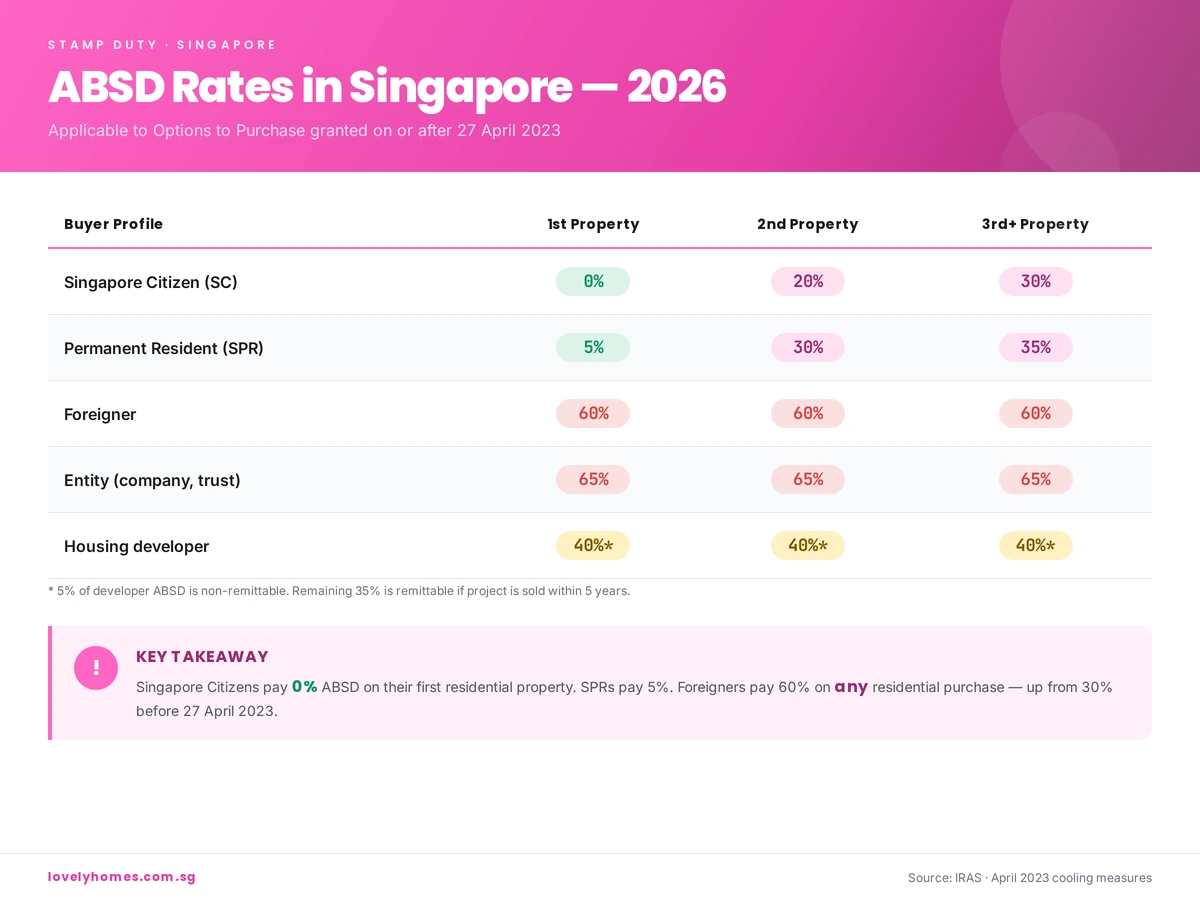

Singapore Citizens: 0% on 1st property, 20% on 2nd, 30% on 3rd+

Singapore PRs: 5% / 30% / 35%

Foreigners: 60% on any residential property

Companies, trusts and other entities: 65%

ABSD is payable within 14 days of signing the Option to Purchase (OTP) or Sale & Purchase Agreement.

What is ABSD and Why Does It Exist?

ABSD is a transaction tax levied on the buyer when acquiring a residential property in Singapore. It sits on top of the regular Buyer’s Stamp Duty (BSD) that every buyer pays. Where BSD is progressive and maxes out at 6% for the portion of price above S$3 million, ABSD is a flat rate applied to the entire purchase price or market value (whichever is higher).

The tax was introduced in December 2011 as part of the Government’s suite of cooling measures — the tools Singapore uses to moderate speculative demand, manage affordability for owner-occupiers, and prevent the kind of runaway price inflation seen in other global cities. Because it targets second-and-subsequent-property buyers and non-citizens disproportionately, ABSD is the single most powerful lever in the cooling-measures toolbox. You can read more about the broader framework in our Property Cooling Measures section.

ABSD Rates in Singapore (2026)

The table below sets out the ABSD rates currently in force. Rates apply based on the profile of the buyer at the time the Option to Purchase (OTP) is granted.

ABSD rates by buyer profile — applicable to OTPs granted on or after 27 April 2023.

Buyer Profile

1st Residential Property

2nd Residential Property

3rd & Subsequent

Singapore Citizen (SC)

0%

20%

30%

Singapore Permanent Resident (SPR)

5%

30%

35%

Foreigner (non-PR individual)

60%

60%

60%

Entity (e.g. company, trustee for a trust)

65%

65%

65%

Housing developer

40%*

40%*

40%*

* 5% of a developer’s ABSD is non-remittable. The remaining 35% is remittable subject to conditions, including selling all units in a qualifying project within five years.

How ABSD is Calculated — A Worked Example

ABSD is applied to the higher of the purchase price or the market value of the property. It is not charged on a tiered basis — the full rate applies to the entire amount.

Example: A Singapore Citizen couple already owns their first home (a 4-room HDB flat). They decide to buy a S$2,000,000 resale condominium in District 15 as an upgrader investment. ABSD on the second property for a Singapore Citizen is 20%.

Purchase price: S$2,000,000

ABSD (20%): S$400,000

BSD (progressive, on S$2m): approximately S$64,600

Total stamp duty payable: S$464,600

That S$400,000 ABSD alone would consume most of the typical upgrader’s CPF and cash reserves. This is why many Singaporean couples take the ‘sell first, buy second’ upgrade route — selling the existing HDB or condo before buying the next home — which we cover later in this guide.

Who Pays ABSD? Exemptions and Special Cases

ABSD applies when you purchase an additional residential property. Commercial property, industrial property, and pure-land parcels are not within its scope. A property is counted toward your “property count” if:

You hold the title as a sole owner, joint tenant, or tenant-in-common;

You are a beneficial owner via a trust;

You are a beneficiary of an estate that holds residential property.

Properties not counted include: properties you merely reside in but do not own (e.g. as a tenant), inherited shares in a deceased estate within the administration period, and certain industrial/commercial units.

Executive Condominiums (ECs)

For new ECs bought directly from the developer during the minimum occupation period of the scheme, ABSD is not triggered because the buyer must commit to an owner-occupier arrangement. ABSD rules apply normally if an EC is purchased on the resale market after its 5-year MOP and 10-year privatisation milestones.

Free Trade Agreement (FTA) Nationals

Citizens and Permanent Residents of countries with which Singapore has an FTA extending National Treatment on stamp duty — namely Iceland, Liechtenstein, Norway, Switzerland, and United States citizens — are accorded the same ABSD treatment as Singapore Citizens. An eligible US citizen buying their first Singapore residential property therefore pays 0% ABSD, not 60%.

ABSD Remission Schemes — How to Get Some (or All) of It Back

Several remission schemes let qualifying buyers claim back part or all of the ABSD they initially pay. The big three to know are:

1. Married Couple Remission (Sale of First Residential Property)

If a Singapore Citizen (or mixed SC & SPR, SC & foreigner) couple buys a replacement home before selling their existing one, they can apply for ABSD remission provided they sell the first property within six months of the later of (a) the date of purchase of the replacement property, or (b) the TOP/CSC date if buying an uncompleted unit. This is effectively a “grace period” that allows upgraders to move without double-paying ABSD.

2. Mixed-Nationality Married Couples

An SC spouse married to a foreigner buying a matrimonial home jointly can enjoy SC rates (rather than foreigner rates) if the property will be used as their matrimonial home and conditions are met. Again, for a first joint home this means 0% ABSD.

3. Developer ABSD Remission

Licensed housing developers pay 40% ABSD upfront (5% non-remittable, 35% remittable) on land purchased for residential development. The 35% is remittable upon meeting development and sales conditions — typically completing the project and selling all units within 5 years.

Remissions must be applied for within strict timeframes (usually 14 days of the triggering event). We strongly recommend engaging a conveyancing lawyer who is experienced in stamp-duty remission applications before signing any OTP where remission will be relied upon.

ABSD vs BSD: What is the Difference?

Every property purchase in Singapore attracts Buyer’s Stamp Duty (BSD), which is a progressive tax on the purchase price:

1% on the first S$180,000

2% on the next S$180,000

3% on the next S$640,000

4% on the next S$500,000

5% on the next S$1,500,000

6% on the portion above S$3,000,000 (residential only)

BSD applies to every buyer; ABSD is the additional layer that may or may not apply depending on your citizenship status and property count. BSD and ABSD are payable together, within 14 days of signing the OTP.

The History of ABSD in Singapore (2011–2026)

Understanding how we arrived at today’s ABSD rates helps you anticipate where the Government may go next. The key milestones:

December 2011: ABSD introduced. Foreigners paid 10%; entities 10%; SPRs 3% on 2nd property; SCs 3% on 3rd+.

January 2013: First major hike. Foreigners to 15%, entities 15%, SPRs 5%/10%, SCs 7%/10% on 2nd/3rd.

July 2018: Rates raised again amid a reflating market. Foreigners to 20%, entities to 25%.

December 2021: Another round. Foreigners to 30%, entities to 35%, SPR 2nd property to 25%, SC 2nd to 17% / 3rd to 25%.

April 2023: The current regime. Foreigners doubled to 60%, entities to 65%, SPR 2nd to 30%, SC 2nd to 20%.

Each tightening has coincided with a period of accelerating private-residential price growth. For a full chronology including LTV, SSD and TDSR changes, see our comprehensive Property Cooling Measures archive.

How to Legally Minimise Your ABSD Bill

ABSD is not optional, but there are a handful of legitimate strategies buyers use to reduce the amount payable or to avoid triggering higher rates:

Sell first, then buy. For couples upgrading, timing the sale of your existing HDB or condo before the purchase of the next means you never hold two properties simultaneously and therefore pay 0% ABSD on the new first home (as an SC).

Use the matrimonial home remission. A mixed SC–foreigner couple buying their matrimonial home jointly enjoys SC rates if structured correctly.

Decouple responsibly. Where one spouse transfers their share of an existing property to the other, only the transferring spouse is freed to buy a second property as a “first” purchase. Decoupling has legal, CPF refund, and mortgage implications — always take specialist advice first.

Consider commercial or industrial property instead. Commercial and industrial properties do not attract ABSD. They have their own financing, GST, and tax considerations — but for investors focused on yield, they are worth analysing. See our Property Investment section for how commercial yields compare with residential.

Look offshore for second and third properties. Singaporeans investing in Malaysia (JB/Iskandar), Thailand, the UK, Australia, or Japan pay no ABSD to the Singapore Government for those purchases. Each destination has its own foreign-buyer regime, which we cover in our Foreign Property Investment guide.

Time your citizenship/PR application carefully. For families where PR or citizenship is in progress, the ABSD profile at the date the OTP is granted determines the rate. Moving the OTP date by a few weeks can, in edge cases, change the applicable rate by 15–25 percentage points.

Frequently Asked Questions

Is ABSD payable on the land value or the built-up value?

ABSD is calculated on the higher of the purchase price or the market value of the property at the time of acquisition. For new launches, this is typically the purchase price; for resale, IRAS may apply an independent market valuation.

When exactly is ABSD due?

Within 14 days from the date of the document triggering the duty — usually the signing of the Option to Purchase (for resale) or the Sale & Purchase Agreement (for new launches). Late payment attracts penalties.

Can CPF be used to pay ABSD?

No. ABSD (like BSD) cannot be paid from CPF directly at the point of purchase — it must be paid in cash. You can, however, apply for CPF reimbursement after the stamping is complete, drawing from your Ordinary Account against the purchase price.

Do I pay ABSD if I inherit a property?

No. A property acquired by way of inheritance is not a purchase and does not attract ABSD on the transfer itself. However, an inherited property does count toward your property count for future purchases.

I already own a commercial shophouse. Do I pay ABSD on my residential condo?

The residential-only count means commercial and industrial holdings are not included in your ABSD property count. If you are a Singapore Citizen buying your first residential property while owning commercial real estate, you still pay 0% ABSD.

How does ABSD affect an Executive Condominium purchase?

Buying a new EC from the developer under the EC scheme does not attract ABSD during the initial owner-occupation period. Once an EC is privatised (10 years after TOP) and traded on the open market, normal ABSD rules apply.

What to Do Next

ABSD changes how much house you can afford, how you time an upgrade, and sometimes whether a purchase makes sense at all. If you are weighing your options right now, we suggest three next steps:

If you are an upgrader, study our Upgrader Guide — the sequencing question (sell first vs buy first) is the single biggest lever for managing ABSD.

Review current market conditions in our Property News and Property Trends sections — if further cooling measures are telegraphed, timing your OTP becomes critical.

Looking at a specific development? Our detailed condo reviews — including One Marina Gardens, Arina East Residences, and our Aurea vs Chuan Park showdown — include the full ABSD-inclusive cost breakdown for various buyer profiles, so you can see the true entry cost before committing.

Disclaimer: This guide is for general information only and does not constitute legal, tax, or financial advice. ABSD rates and remission rules change over time. Always verify the current position on the IRAS Stamp Duty page and consult a licensed conveyancing lawyer or tax specialist before acting on any property transaction.

⚡ Quick Answer: Buying a Private Condo in Singapore 2026

Eligibility: Any Singapore Citizen, Permanent Resident or foreigner may buy private non-landed residential property — no income ceiling applies.

Minimum cash outlay: At least 5% of purchase price must be in cash; the remaining 20% of the 25% down payment may come from CPF Ordinary Account.

ABSD: Singapore Citizens pay 0% ABSD on their first property, 20% on the second, 30% on the third. Foreigners pay 65%. (Rates effective 27 April 2023.)

BSD: Buyer’s Stamp Duty is payable by all buyers — 1% on first S$180,000; 2% on next S$180,000; 3% on next S$640,000; 4% on remainder up to S$1.5M; 5% thereafter.

Loan-to-Value (LTV): Maximum 75% bank loan for a first property. TDSR cap is 55% of gross monthly income.

Timeline: From viewing to key collection typically takes 12–16 weeks for resale, or 3–5 years for a new launch off-plan purchase.

Key milestone: Option to Purchase (OTP) must be exercised within 21 days (developer) or 14 days (resale); stamp duty is payable within 14 days of acceptance.

No CPF for overseas property: CPF OA funds may only be used for Singapore residential property.

Buying a private condominium in Singapore is one of the most significant financial decisions a household will make. Unlike HDB flats — which are heavily regulated by income ceilings, nationality rules and a Minimum Occupation Period (MOP) before resale — private residential property is open to a broader pool of buyers, but comes with its own web of stamp duties, financing constraints and legal procedures.

This guide walks through every stage of the private condo buying process in Singapore as of 2026: from assessing your eligibility and finances, through exercising the Option to Purchase (OTP), paying Buyer’s Stamp Duty (BSD) and Additional Buyer’s Stamp Duty (ABSD), drawing down your bank loan and CPF, all the way to key collection and post-completion obligations. Data and regulations cited are current as at 15 May 2026.

Figure 1: The 10-step private condo buying process in Singapore 2026, from finance checks to post-completion. Source: URA, IRAS, CPF Board | lovelyhomes.com.sg

Step 1: Check Your Eligibility and Finances

Any buyer — Singapore Citizen (SC), Permanent Resident (PR) or foreigner — may purchase a private non-landed condominium. There is no HDB income ceiling for private property. However, financing is tightly regulated by the Monetary Authority of Singapore (MAS) through two key ratios:

Total Debt Servicing Ratio (TDSR): All monthly debt obligations — including the new mortgage — must not exceed 55% of gross monthly income. Banks typically stress-test the loan at a rate floor of 4% p.a. (MAS Notice 632 stress-test benchmark).

Loan-to-Value (LTV): The maximum bank loan is 75% of the lower of the purchase price or market valuation for a first residential property. This drops to 45% for a second property (if there is an outstanding housing loan) and 35% for a third or subsequent property.

Before viewing a single unit, calculate your maximum eligible loan amount and ensure your CPF Ordinary Account (OA) balance and cash savings can cover the 25% down payment, Buyer’s Stamp Duty, legal fees and renovation budget. A rough rule of thumb: budget an additional 4–5% of the purchase price on top of the down payment to cover all transaction costs.

Step 2: Obtain an In-Principle Approval (IPA)

An In-Principle Approval (IPA) — sometimes called an Approval in Principle (AIP) — is a conditional commitment from a bank that it is prepared to lend you up to a specified amount, subject to a satisfactory property valuation. Most major Singapore banks (DBS, OCBC, UOB, Standard Chartered, HSBC, Maybank) offer IPA letters valid for 30 days, renewable on request.

To obtain an IPA, the bank will assess your income documents (CPF contribution statements, IRAS Notice of Assessment, latest 3–12 months’ payslips for employed applicants), outstanding debt commitments, and credit bureau report. Processing typically takes 3–5 business days. Obtaining an IPA before you sign any OTP is strongly recommended — exercising an OTP without confirmed financing in place can result in a forfeited option fee if the loan falls through.

Buyer Profile

Max LTV

Min Cash Down

ABSD Rate (2026)

SC — 1st property

75%

5% cash

0%

SC — 2nd property

45%

25% cash

20%

SC — 3rd+ property

35%

25% cash

30%

SPR — 1st property

75%

5% cash

5%

SPR — 2nd+ property

45%

25% cash

30%

Foreigner (any)

75%

5% cash

65%

Entity / Company

75%

5% cash

65%

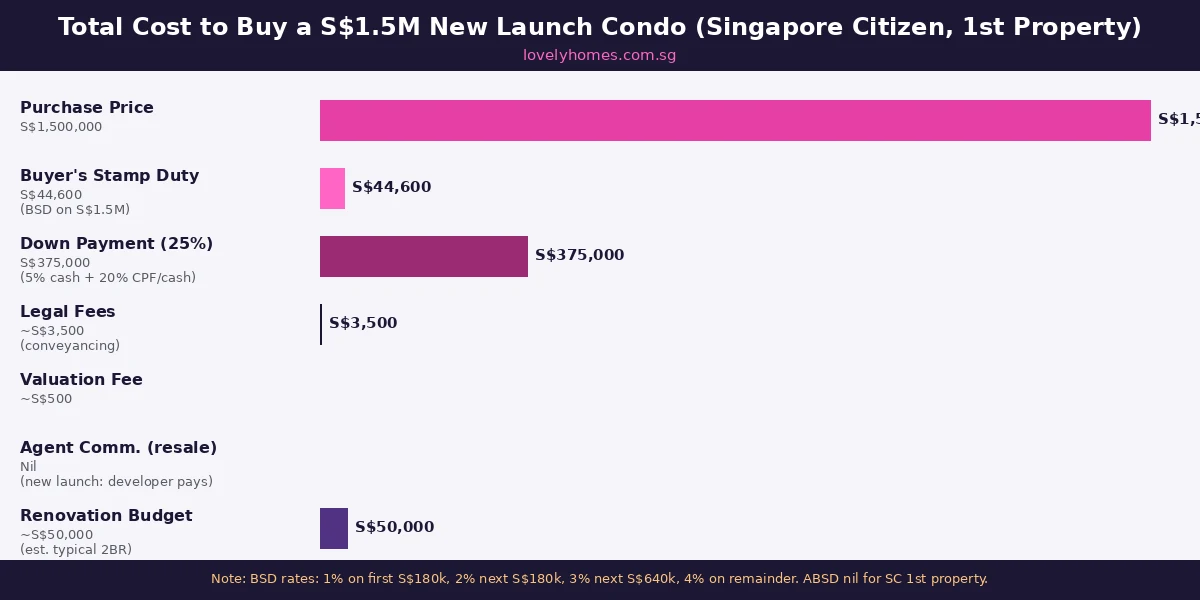

Figure 2: Full cost stack for a Singapore Citizen buying a S$1.5M new launch condo as their first property. Source: IRAS, CPF Board | lovelyhomes.com.sg

Step 3: Engage a Buyer’s Conveyancer

Unlike in some countries where a single solicitor can act for both buyer and seller (or buyer and bank), Singapore law requires separate solicitors for buyer and seller in most private property transactions. Your conveyancer — a law firm with real estate expertise — will review the Option to Purchase, the Sale and Purchase Agreement (S&P), lodge the CPF charge with the CPF Board, handle stamp duty payments and oversee the transfer of title. Engage your conveyancer before you grant or accept an OTP so they can review the documents promptly within the tight exercise windows.

Legal fees for a straightforward private condo purchase typically range from S$2,500 to S$4,500 for the buyer’s solicitor, plus the bank’s in-house or panel solicitor fees of S$800 to S$1,500 if you are taking a bank loan. Both are payable at completion.

Step 4: Search, Shortlist and View Properties

Singapore’s private residential market is segmented by location into three broad zones defined by URA: the Core Central Region (CCR — Districts 1, 2, 4, 6, 7, 9, 10, 11, and Sentosa), the Rest of Central Region (RCR — Districts 3, 5, 8, 12, 13, 14, 15, 20 and parts of others) and the Outside Central Region (OCR — all other districts). As of Q1 2026, URA data shows OCR non-landed prices led all segments with +2.2% quarter-on-quarter growth, reflecting sustained mass-market demand in towns like Tampines, Woodlands and Tengah.

For new launches, developer project websites and the URA New Sale caveat portal provide indicative price lists (PSF) before showflat visits. For resale units, URA’s Realis platform and HDB’s Resale Portal publish every caveat lodged within two weeks of an OTP being exercised. Use these sources to benchmark asking prices before negotiating.

Step 5: Grant and Exercise the Option to Purchase (OTP)

The Option to Purchase is the critical legal document that locks in the transaction. For new launches, the developer grants a 21-day OTP (extendable to a maximum of 42 days under the Housing Developers (Control and Licensing) Act). For resale, the seller grants a 14-day OTP, which may be extended by mutual agreement.

The buyer pays a 1% option fee (new launch: typically 5–10% option exercise fee as the booking fee) to receive the OTP. If the buyer decides not to proceed, the seller may forfeit the option fee. If the buyer exercises the option (by signing and returning it with the additional exercise money — typically a further 4% for resale, bringing total to 5%), the transaction is legally binding. The buyer must then pay BSD within 14 days of acceptance and sign the S&P or proceed with the developer’s standard agreement within 8 weeks (new launch) or 12 weeks (resale).

BSD is payable by every buyer on every purchase, regardless of nationality or property count. The current rates, administered by the Inland Revenue Authority of Singapore (IRAS), are progressive:

1% on the first S$180,000 of the purchase price

2% on the next S$180,000 (S$180,001 to S$360,000)

3% on the next S$640,000 (S$360,001 to S$1,000,000)

4% on the next S$500,000 (S$1,000,001 to S$1,500,000)

5% on the next S$1,500,000 (S$1,500,001 to S$3,000,000)

6% on the remainder above S$3,000,000

For a S$1.5M condo, BSD = S$1,800 + S$3,600 + S$19,200 + S$20,000 = S$44,600. ABSD is payable in addition to BSD — it must be stamped within 14 days of exercising the OTP. ABSD is not payable on a Singapore Citizen’s first property. On a S$1.5M second property for an SC, ABSD = 20% × S$1,500,000 = S$300,000. This is a material sum that must be factored into your budget before signing any OTP.

Worked Example: Mr and Mrs Tan Buy a S$1.5M Condo in Tampines (First Property)

Mr and Mrs Tan are both Singapore Citizens with a combined gross monthly income of S$14,000. They wish to purchase a new launch 3-bedroom condo in Tampines priced at S$1,500,000 as their first and only property (their HDB flat was sold to clear MOP).

BSD: S$44,600 (calculated above)

ABSD: S$0 (SC first property)

Down payment (25%): S$375,000 — at least S$75,000 (5%) must be cash; remaining S$300,000 may be CPF OA

Bank loan (75%): S$1,125,000 at 1.80% fixed for 2 years, 25-year tenure → monthly instalment ≈ S$4,634

TDSR check: S$4,634 ÷ S$14,000 = 33.1% — well within the 55% cap

Total cash needed at completion: S$75,000 (cash downpayment) + S$44,600 (BSD) + S$4,700 (legal) ≈ S$124,300 cash, plus S$300,000 from CPF OA

The Tans need to ensure their CPF OA balances (combined) are at least S$300,000 and that they have at least S$125,000 in cash savings before exercising the OTP.

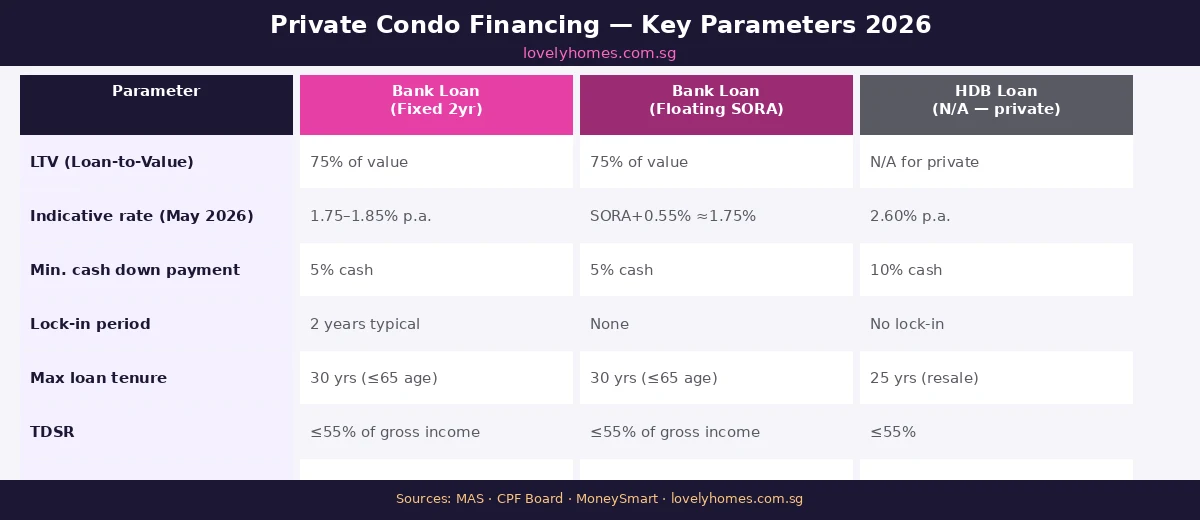

Figure 3: Key financing parameters for private condos in Singapore 2026 — fixed-rate vs floating SORA bank loans. Source: MAS, CPF Board | lovelyhomes.com.sg

Step 7: Sign the Sale and Purchase Agreement and Loan Documents

The Sale and Purchase Agreement (S&P) is the legally binding contract between buyer and seller. For new launches, the developer is required by law (Housing Developers Rules) to use a standard-form S&P that specifies progressive payment milestones tied to construction stages. For resale, the S&P is drafted by the seller’s solicitor and reviewed by the buyer’s solicitor for any unusual conditions or encumbrances on the title.

Simultaneously, you will sign the bank’s Letter of Offer (loan agreement), which sets out the interest rate, tenure, prepayment conditions, lock-in penalties and any repricing rights. Under the MAS Notice on Mortgage Servicing Ratio (MSR) — which caps HDB-related loans at 30% of gross monthly income — private property loans have no MSR cap, only TDSR. Banks have typically been offering 2-year fixed rates of 1.75–1.85% p.a. as of May 2026 (SORA 3M at approximately 1.20% + spread of 0.55%).

Step 8: Pre-Completion Checks, Snagging and Handover

For new launches, Temporary Occupation Permit (TOP) is issued when construction is substantially complete. Buyers are invited to conduct a snagging inspection before key collection — a thorough walkthrough to identify and log defects (water seepage, scratched flooring, misaligned doors, non-functioning fixtures) in the developer’s Defects Rectification Form. Developers are obligated under the Building and Construction Authority (BCA) guidelines to rectify defects within 12 months of TOP. Do not waive your right to a snagging inspection; defects are far cheaper to fix before handing over deposit-linked remedies.

For resale units, arrange for an independent building inspector to inspect the unit before exercising the OTP. A structural defect discovered after signing the S&P may be difficult and expensive to resolve.

Step 9: Completion and Key Collection

Legal completion typically occurs 8–12 weeks after the S&P is signed (resale) or upon TOP for new launches. At completion, the balance of the purchase price (minus your deposit already paid and minus the loan drawn down by the bank) is transferred from your solicitor’s client account. Your CPF OA charge is lodged, the bank’s mortgage is registered, and the Transfer of Title is stamped and lodged with the Singapore Land Authority (SLA). You collect the keys (and for new launches, the developer issues your Electronic Certificate of Statutory Completion / Certificate of Fitness).

Step 10: Post-Completion Obligations

After key collection, several post-completion obligations apply. First, notify IRAS within 15 days of the change in ownership — your solicitor will typically handle this. Second, if you sold your HDB flat to fund this purchase, ensure all CPF refunds (principal + accrued interest) have been credited back to your CPF OA. Third, review your fire insurance and home contents insurance. If your unit is in a strata development, the MCST’s master fire insurance policy covers the building structure but not your contents or renovation works. Finally, if you plan to rent out the unit, notify IRAS as rental income is taxable — declare it in your annual personal income tax return.

Why the Process Matters: OCR’s S$2.2% Q1 2026 Surge and What It Signals

URA’s Q1 2026 final private residential data (released 24 April 2026) showed private property prices rising 0.9% quarter-on-quarter overall, with the OCR — the mass-market segment covering Tampines, Woodlands, Tengah and similar suburbs — surging 2.2%. This is the highest OCR quarterly gain since Q2 2024. Against this backdrop, buyers who understand every cost component of the transaction — particularly the BSD and ABSD exposure on second properties — are better positioned to make rational bid-versus-walk decisions.

The large supply pipeline ahead — URA reports approximately 55,800 private units and ECs expected to complete over the next several years, plus 4,575 units from the 1H 2026 GLS confirmed list — suggests that buyers who over-commit on today’s prices without stress-testing against a possible price correction do so at their own risk. The MAS stress-test rate of 4% p.a. is deliberately conservative for this reason.

What Might Come Next: Cooling Measure Adjustments and ABSD Calibration

Singapore’s property cooling measures have been calibrated in multiple rounds since 2009. The most recent significant revision was the April 2023 ABSD increase (foreigners to 65%, SC second property to 20%). As of May 2026, there are no confirmed further ABSD adjustments on the horizon. However, the ongoing strength of OCR prices and the record-breaking new launch weekend sales in April 2026 (Tengah Garden Residences and Vela Bay together sold over 1,200 units in 48 hours) may prompt the Ministry of National Development to revisit cooling measures should the market overheat. Buyers considering a second private property — particularly the decoupling strategy to lower ABSD exposure — should seek legal and financial advice before committing.

Frequently Asked Questions

Can I use CPF to buy a private condo in Singapore?

Yes. CPF Ordinary Account (OA) funds may be used for the down payment (above the mandatory 5% cash) and for servicing the monthly mortgage instalments, subject to the Valuation Limit (VL) and Withdrawal Limit (WL) rules. The VL is set at the lower of the purchase price or valuation at the time of purchase. You can use CPF up to the VL, and beyond that up to 120% of the VL (the WL), provided you retain the prevailing Basic Retirement Sum (BRS) in your CPF. Once the WL is reached, no further CPF can be used for that property. Note: CPF may not be used for overseas property under any circumstances.

Can foreigners buy private condos in Singapore?

Yes. Foreigners (non-Singapore Citizens, non-PRs) may purchase private non-landed residential property — including condominiums, apartments and strata-titled units — without any government approval. However, they may not purchase HDB flats, executive condominiums within the first 10 years of MOP, landed properties (detached houses, semi-detached, terrace houses) except in specific cases approved by the Singapore Land Authority, or residential properties on Sentosa Cove below a specified threshold without prior SLA approval. Foreigners pay ABSD of 65% on any Singapore residential property purchase.

What happens if I cannot exercise the OTP within the 14-day window?

If you fail to exercise the OTP within the specified period (14 days for resale, 21 days for new launches), the option lapses. The seller may forfeit the 1% option fee — it does not need to be returned to you. For new launches, the developer’s standard form typically allows forfeiture of 25% of the booking fee (which is usually 5% of the purchase price) if the buyer does not exercise. This means on a S$1.5M new launch, failure to exercise could cost you S$75,000 × 25% = S$18,750 in forfeitures. Ensure your financing is confirmed before you sign the OTP receipt.

Do I need to sell my HDB flat before buying a private condo?

No, but there are significant financial consequences if you do not. If you own an HDB flat and purchase a private condo without selling the HDB first, you will be counted as owning two residential properties — triggering ABSD of 20% on the private property (for a Singapore Citizen). To avoid ABSD on the private purchase, you would need to sell your HDB flat before or simultaneously with completing the condo purchase. If you buy first and then sell the HDB within 6 months of the condo’s completion (or TOP for new launch), there is a remission mechanism for the ABSD paid — you may apply to IRAS for a refund if you meet all the conditions (including the property being jointly or solely owned by a married SC couple buying their second residential property and they have sold the first within the 6-month window). See IRAS’s stamp duty remission guidelines.

What is the difference between a new launch and a resale private condo?

A new launch condo is sold directly by the developer from an uncompleted or newly completed project, typically at a showflat. Prices are set by the developer (in PSF terms), there are no agents on the buyer’s side (the developer pays the selling commission), and the progressive payment scheme means you pay in tranches tied to construction milestones. The wait from booking to key collection is typically 3–5 years. A resale condo is an existing completed unit being sold by a private individual or investor. You can inspect the actual unit, the condition of the development and the management corporation (MCST). Transaction timelines are much shorter (8–12 weeks to completion) but you may need to factor in renovation costs and the condition of existing fixtures. Resale condo prices are also subject to market negotiation.

How long does the private condo buying process take in Singapore?

For a resale private condo, the process from OTP issuance to legal completion typically takes 10–14 weeks. You have 14 days to exercise the OTP, then 8–12 weeks for completion. The full process from first viewing to key collection, including time to arrange financing, is typically 2–4 months. For a new launch condo purchased off-plan, the process is very different: you book a unit at the showflat (same-day for popular launches), sign the OTP and formal S&P within 3 weeks, pay progressively over the construction period of 3–5 years, and collect keys at TOP.

Can a Singapore Permanent Resident (PR) buy a private condo?

Yes, PRs may purchase private non-landed residential property. A PR buying their first residential property pays ABSD of 5% and can access up to 75% LTV. However, PRs may not use their CPF Ordinary Account to purchase property until they have been a PR for 1 year. PRs also cannot purchase HDB resale flats unless the entire purchasing household is PR-only and they meet a minimum 3-year PR residency requirement; they cannot purchase new HDB BTO flats. For a second property, the ABSD rate for PRs rises to 30%, the same as Singapore Citizens buying a third property.

Disclaimer: This article is for general informational purposes only and does not constitute legal, financial or investment advice. Stamp duty rates, ABSD rates, LTV limits, CPF rules and MAS regulatory requirements are as published by IRAS, MAS and CPF Board and are subject to change by the Singapore government at any time. Readers should verify all figures directly with IRAS (iras.gov.sg), MAS (mas.gov.sg), CPF Board (cpf.gov.sg) and URA (ura.gov.sg), and consult a licensed solicitor, a MAS-licensed financial adviser or a registered mortgage broker before making any property transaction decision. LovelyHomes is not affiliated with any property agency and does not provide brokerage services.

0 Comments