Singapore Seller’s Stamp Duty (SSD) Guide 2026: Rates, History, Exemptions and How Much You’ll Pay

⚡ Quick Answer: Singapore SSD 2026 — Key Takeaways

- What is SSD? Seller’s Stamp Duty is a tax imposed by IRAS on the seller of a residential property sold within 3 years of purchase.

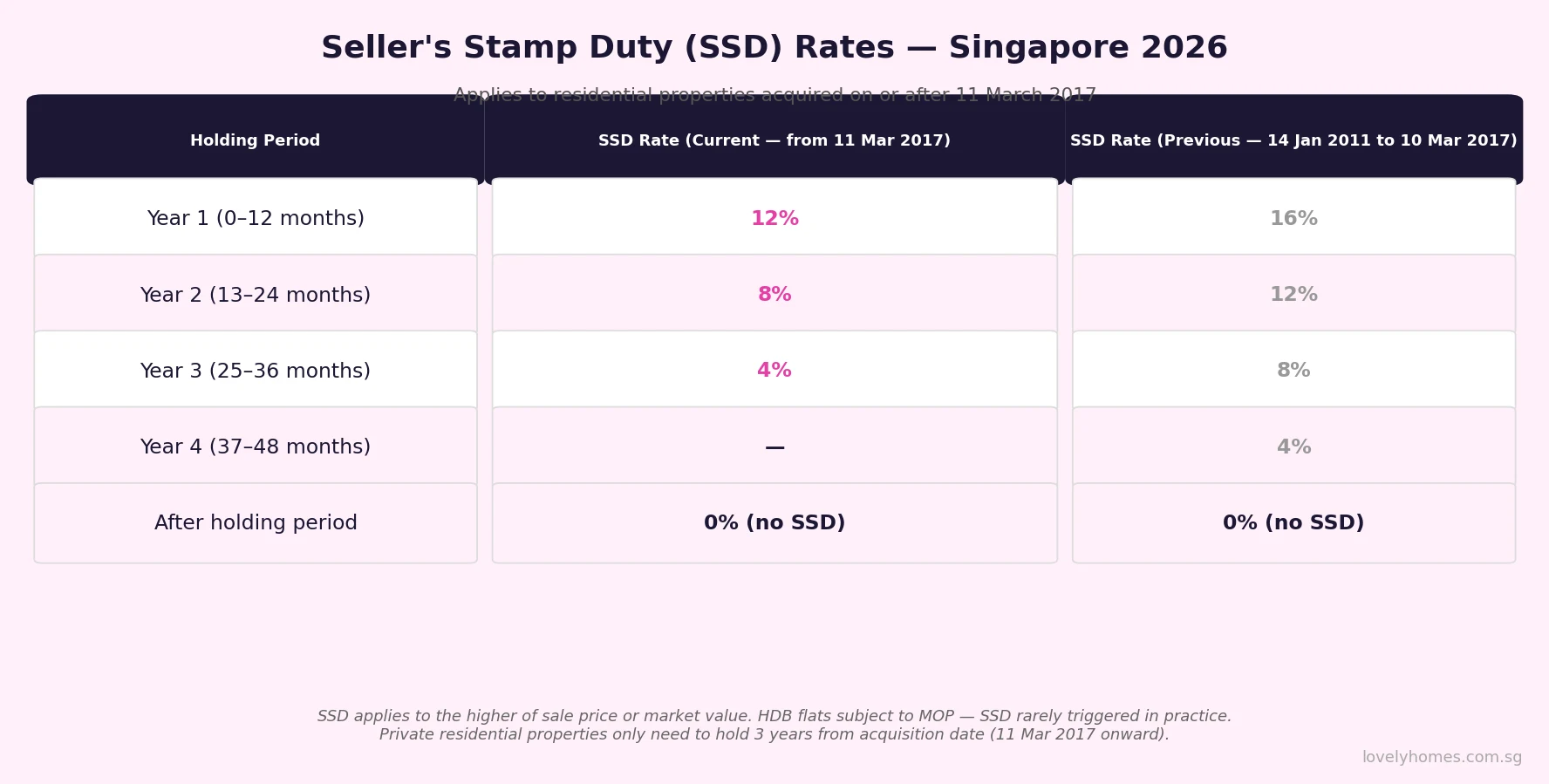

- Current rates (effective 11 March 2017): Year 1 = 12%, Year 2 = 8%, Year 3 = 4% of the sale price or market value, whichever is higher.

- Year 4+: Zero SSD. Selling after 3 years incurs no SSD regardless of profit.

- Who pays? The seller — not the buyer. SSD is on top of any Capital Gains (none in Singapore) and is not deductible against income tax.

- Applies to: All private residential properties (condos, landed, ECs post-TOP) and HDB flats.

- Exemptions: Compulsory acquisition, SERS, inherited property transferred by court order, and certain other statutory transfers.

- On a S$1.5M property sold in Year 1: SSD payable = S$180,000 cash — a major cost of early exit.

- Why does SSD exist? It is Singapore’s primary anti-speculation measure on the sell side, discouraging short-term flipping of residential property.

What is Seller’s Stamp Duty (SSD) in Singapore?

Seller’s Stamp Duty — commonly called SSD — is a stamp duty levied by the Inland Revenue Authority of Singapore (IRAS) on the sale of residential property within a specified holding period. Unlike the Additional Buyer’s Stamp Duty (ABSD), which targets the buyer, SSD falls entirely on the seller. Its design is deliberate: by making short-term resales expensive, the government discourages speculative flipping that can destabilise the residential market.

SSD was introduced in February 2010 as Singapore first began cooling an overheating residential market, and the rates and holding period have been adjusted several times since. As of 2026, the rules have remained unchanged from the March 2017 revision: sellers who dispose of a residential property within three years of acquisition pay a sliding rate of 12%, 8%, or 4% depending on how early they sell.

This guide covers every aspect of SSD — the rates, the history, who pays, what is exempt, how it interacts with other stamp duties, and exactly how much it costs in real Singapore dollar terms.

SSD Rates 2026: The Current Schedule

The current SSD schedule, introduced on 11 March 2017 and still in force as at 2026, is as follows:

| Year of Sale After Purchase | SSD Rate | Example: S$1.5M property | Example: S$2.5M property |

|---|---|---|---|

| Year 1 (within 1 year) | 12% | S$180,000 | S$300,000 |

| Year 2 (1–2 years) | 8% | S$120,000 | S$200,000 |

| Year 3 (2–3 years) | 4% | S$60,000 | S$100,000 |

| Year 4+ (beyond 3 years) | 0% | Nil | Nil |

Important technical points: SSD is calculated on the higher of the transacted sale price or the market value assessed by IRAS. This prevents sellers from artificially suppressing the declared price to reduce duty. SSD is payable to IRAS within 14 days of exercising the Option to Purchase (OTP) as seller, or within 30 days of the sale if no OTP is used.

The holding period begins on the date of purchase — typically the date the seller originally exercised the OTP to buy the property, or the date of transfer in the case of a CPF Housing Grant purchase or inherited top-up. For properties acquired before the relevant date of a policy change, the applicable SSD rates are those in force at the time of purchase, not the time of sale.

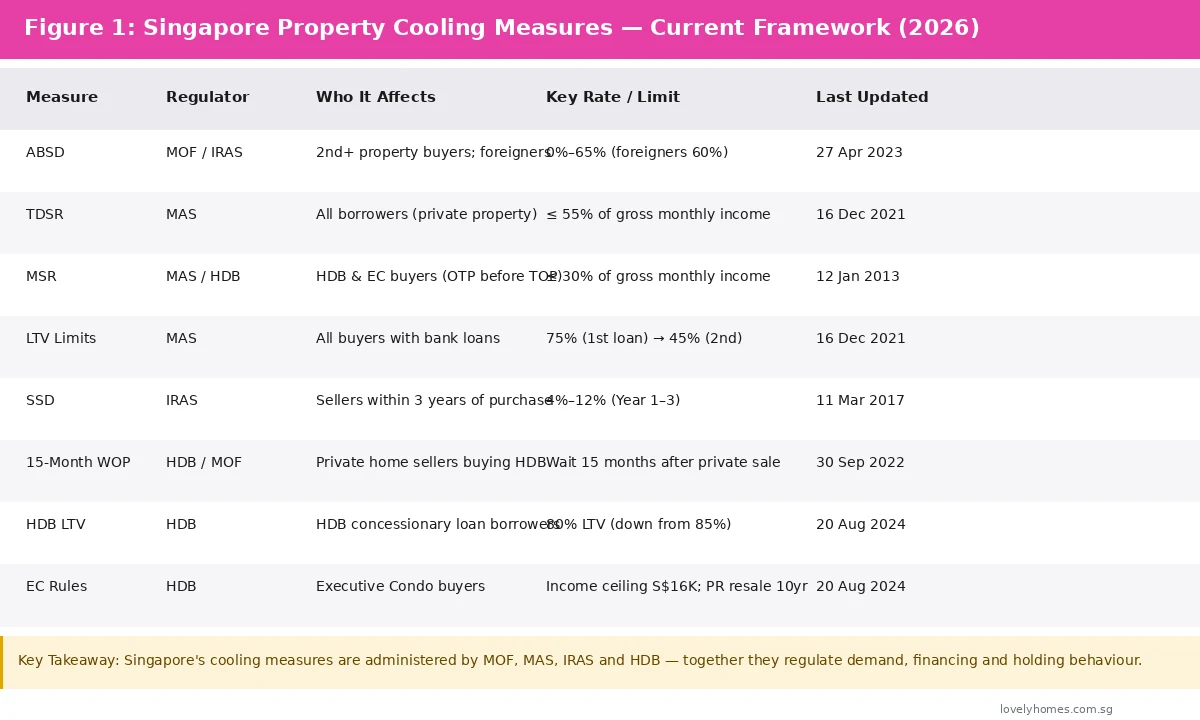

How SSD Interacts with Other Stamp Duties

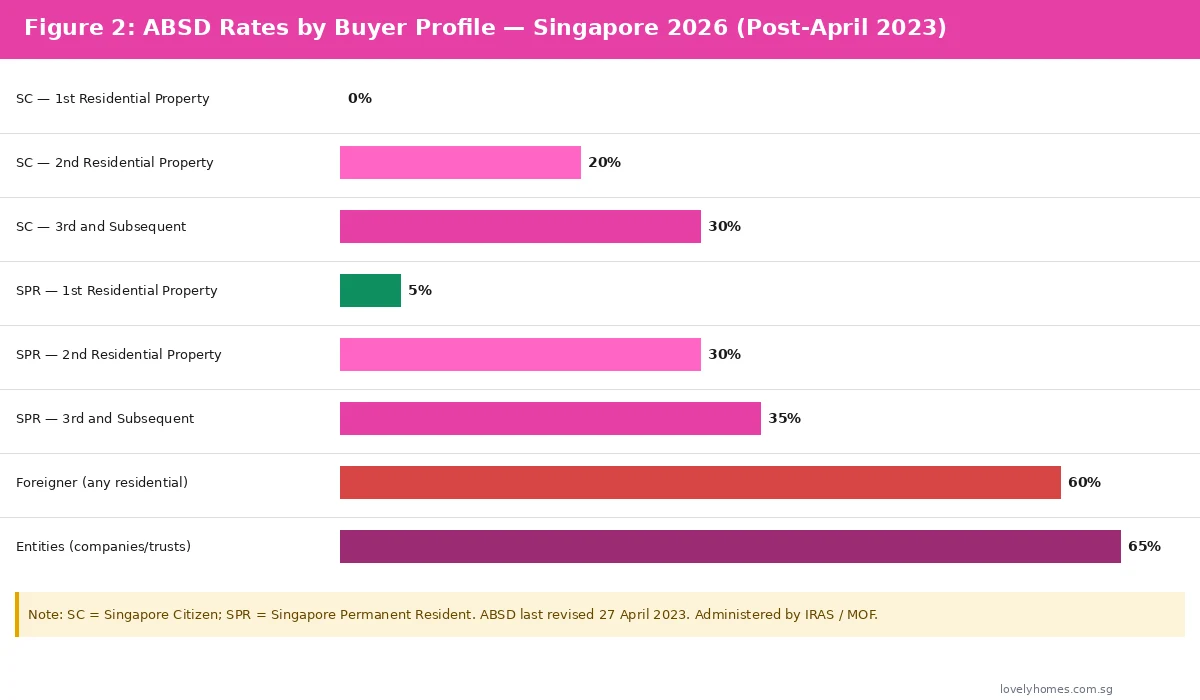

Singapore’s stamp duty framework has three main instruments: Buyer’s Stamp Duty (BSD), payable by the buyer on acquisition; Additional Buyer’s Stamp Duty (ABSD), also payable by the buyer and calibrated by citizenship status and property count; and Seller’s Stamp Duty (SSD), payable by the seller on disposal within three years. These are not mutually exclusive — in any given transaction, the buyer pays BSD plus any applicable ABSD, while the seller simultaneously pays SSD if selling within the holding period.

This creates a compounding effect for short-term investors. A Singaporean citizen who buys a S$1.5M condo as a second property pays 20% ABSD (S$300,000) on purchase. If they then sell within Year 1, the new seller pays 12% SSD (S$180,000) on the same property. The combined stamp duty burden across both sides of the transaction is S$480,000 — more than 32% of the purchase price. This architecture is intentional: it makes rapid cycling of residential property financially punishing.

Who Pays SSD — and What Is Exempt?

SSD is the legal obligation of the seller of a residential property. The buyer has no liability for SSD — they pay BSD and ABSD on their side of the transaction. In practice, SSD payments are coordinated by the conveyancing solicitors at the point of completion, funded from the sale proceeds before they are released to the seller. If the proceeds are insufficient (for example, if the property is sold at a loss and the outstanding mortgage is large), the seller must top up the SSD from their own funds.

Properties subject to SSD include:

- Private residential properties — condominiums, apartments, townhouses, bungalows, semi-detached and terrace houses

- Executive Condominiums (ECs) that have received Temporary Occupation Permit (TOP), when sold within three years of purchase

- HDB flats — including resale flats bought from the open market

- Mixed-use properties where the residential component is the predominant use

Properties and transactions NOT subject to SSD:

- Commercial and industrial properties — shophouses (commercial use), office units, factory/warehouse units, and retail strata units. SSD does not apply to non-residential real estate.

- Compulsory acquisition — where the Singapore Land Authority (SLA) or a statutory body acquires the property compulsorily under the Land Acquisition Act, no SSD is triggered.

- SERS (Selective En Bloc Redevelopment Scheme) — HDB flat owners displaced under SERS are not subject to SSD.

- Inheritance — property transferred to a beneficiary pursuant to the deceased’s estate is not subject to SSD, as there is no sale consideration.

- Court order transfers — transfers of matrimonial property pursuant to a court order in divorce proceedings are exempt, subject to IRAS conditions.

- Gift transfers — there is no sale, though other stamp duties may apply.

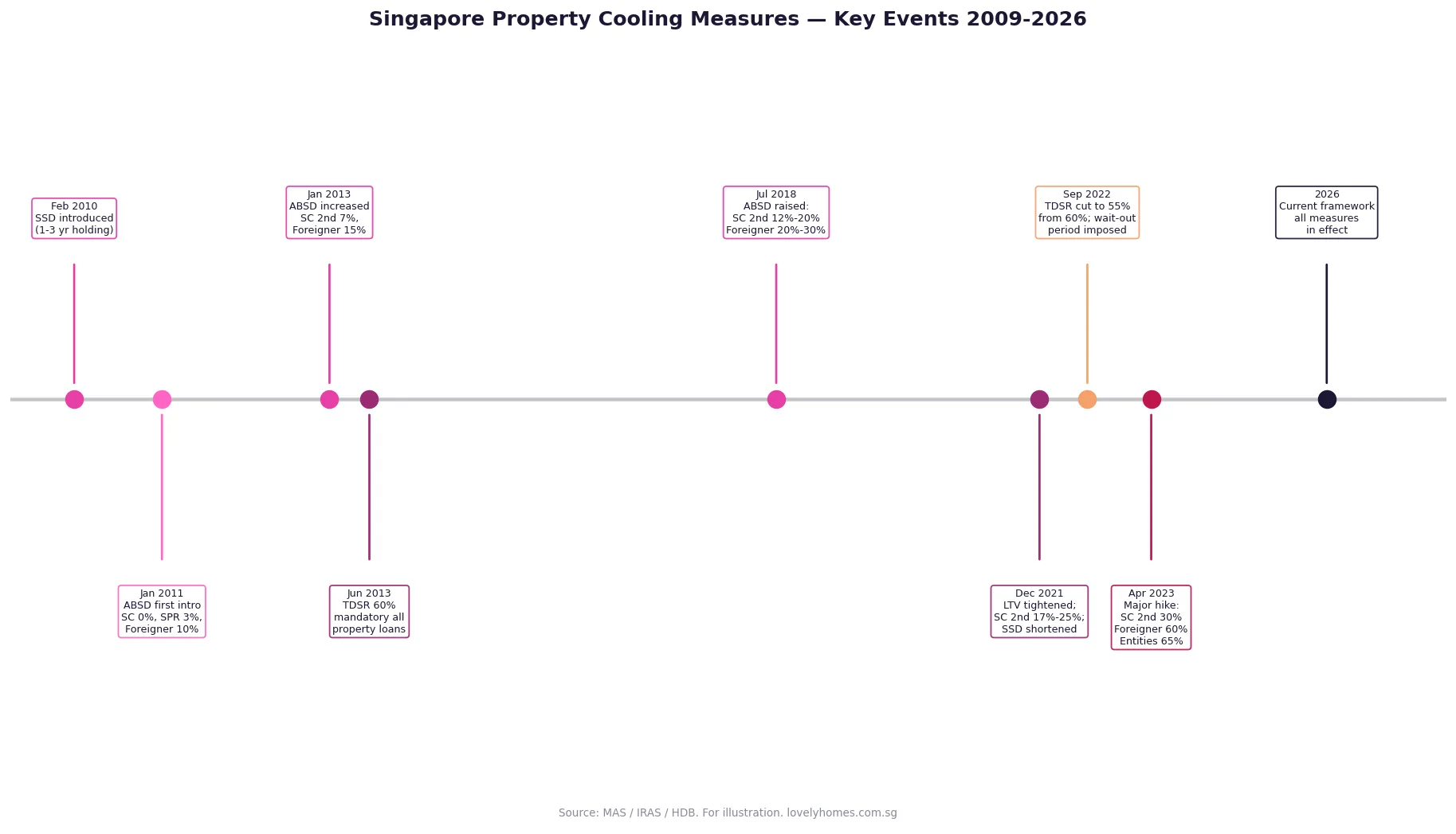

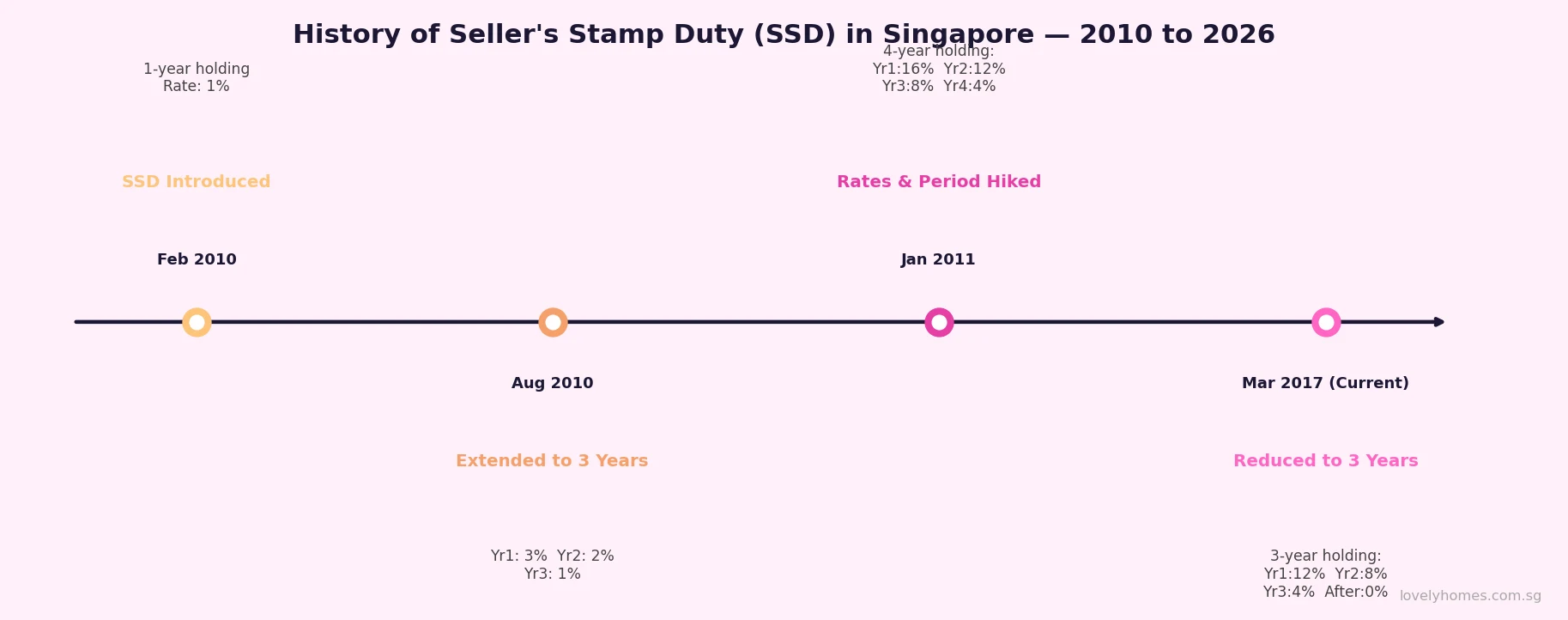

SSD Policy History: From 2010 to 2026

SSD has been adjusted five times since its introduction, reflecting the government’s ongoing calibration of the residential property market. Understanding this history is useful for buyers and sellers assessing whether further changes may be forthcoming.

In February 2010, SSD was introduced for properties sold within one year, at a nominal 1% rate — primarily a signalling measure in an overheating post-global-financial-crisis market. By August 2010, the scope expanded to three years (1%, 0.67%, 0.33%), still modest in dollar terms.

The big shift came in January 2011, when the government extended the holding period to four years and dramatically raised rates to 16%, 12%, 8%, and 4% respectively. This reflected the government’s alarm at the pace of speculation during 2010. In January 2013, with the market showing signs of more stable behaviour, the holding period was trimmed back to three years while rates were retained.

The most recent change — and the one still in force — came on 11 March 2017. As part of a broader easing of property cooling measures (which also saw ABSD rates for Singaporeans reduced and TDSR concessions introduced), SSD rates were reduced by four percentage points at each tier: from 16/12/8% to the current 12/8/4%. This reduction signalled the government’s view that the market had stabilised sufficiently to ease — but not fully remove — the sell-side deterrent.

Worked Example: How Much SSD Will You Pay?

📚 Case Study: Mr & Mrs Phua — Forced Early Sale of OCR Condo

Background: Mr and Mrs Phua (Singapore Citizens) purchase a 3-bedroom condominium in the Outside Central Region (OCR) at S$1,600,000. The Option to Purchase is exercised on 10 February 2025, which becomes the date of purchase for SSD purposes.

Scenario: In late 2025, Mr Phua is posted overseas by his employer. The family decides they cannot maintain the property and must sell. They accept an offer and exercise the OTP as sellers on 1 December 2025 — approximately 9 months and 21 days after purchase.

SSD calculation:

- Date of purchase: 10 February 2025

- Date of sale (OTP exercised): 1 December 2025

- Holding period: <12 months → Year 1 rate applies: 12%

- Sale price: S$1,600,000 (assume at or above market value)

- SSD payable: 12% × S$1,600,000 = S$192,000

Impact on net proceeds:

- Sale price: S$1,600,000

- Less: SSD (12%): −S$192,000

- Less: Legal fees (selling): ~−S$3,500

- Less: Agent commission (1%): −S$16,000

- Less: Outstanding mortgage balance (approx): −S$1,100,000

- Less: CPF housing refund (principal + accrued interest): −S$210,000

- Net cash proceeds: ~S$78,500

Key lesson: Had the Phuas waited until after 10 February 2027 (Year 3 passes), the SSD would fall to 4% (S$64,000) — a saving of S$128,000. Had they waited until 10 February 2028 (beyond Year 3), SSD would be zero. The trade-off between the rental income from the property, the cost of holding, and the SSD saving must be carefully modelled.

Alternative: If the Phuas had rented out the property during the overseas posting and returned to sell after three years, they would have avoided SSD entirely — potentially saving S$64,000–S$192,000 depending on the year of eventual sale, while generating rental income in the interim.

Why SSD Exists — The Policy Rationale

Singapore’s residential property market is one of the most tightly regulated in Asia. The government’s consistent objective since 2009 has been to maintain a stable and sustainable market — one where prices reflect genuine occupier demand rather than speculative momentum. SSD is the sell-side component of this framework, designed to extend the effective investment horizon of property buyers.

By making early exit expensive, SSD discourages the “hot money” short-term flipping that can amplify boom-bust cycles. A property investor who knows they will face 12% SSD in Year 1 is effectively underwriting that cost into their required return. At S$1.5M, that is S$180,000 in SSD alone — equivalent to roughly four years of gross rental income on many Singapore condominiums. This creates a strong structural incentive to hold rather than flip.

Peer comparison: Hong Kong’s equivalent measure (Seller’s Stamp Duty) was revised in November 2023, reducing its holding period from three years to two years and cutting rates. Australia does not have SSD; its anti-speculation measures operate primarily through capital gains tax (CGT) discounting rules. Singapore’s SSD is widely regarded by international investors as a relatively blunt but effective tool that has contributed to lower price volatility than comparable markets.

SSD and the Singapore Property Investment Calculus

For legitimate long-term investors — those holding for four or more years — SSD is a non-issue. The practical implication is simple: plan your exit timeline. If you are buying a condo as an investment, build in a minimum four-year holding period before any planned disposal. This eliminates SSD liability entirely and also typically allows sufficient time for capital appreciation to absorb transaction costs.

For owner-occupiers facing an unexpected need to sell within three years — job relocation, family emergency, financial hardship — SSD is an unavoidable cost. IRAS does not grant SSD remissions on personal hardship grounds (unlike ABSD remissions, which exist for certain co-ownership scenarios). The practical mitigation is to consider renting out the property during the forced absence period, if circumstances and HDB/condominium rules permit.

What Might Come Next for Singapore SSD?

As of mid-2026, the SSD schedule has been unchanged for more than nine years. The government has signalled — most recently through the Deputy Prime Minister’s public statements in early 2026 — that it remains watchful of the residential market, particularly in the wake of the URA’s Q2 2026 flash estimate showing a modest +0.5% overall price increase alongside continued CCR strength.

Speculation (appropriately labelled as such) about SSD changes falls into two camps. One camp argues that the market has been sufficiently stable since 2017 to warrant a further relaxation — perhaps reducing the holding period to two years or cutting Year 1 rates. The other camp notes that foreign demand has remained elevated (particularly in the CCR, where ABSD does not fully deter affluent foreign buyers) and that SSD remains one of the few friction costs that applies symmetrically regardless of buyer nationality.

LovelyHomes’ view: absent a significant deterioration in macroeconomic conditions or a sharp acceleration in price growth, the government is unlikely to change SSD rates in the near term. The 2017 rates represent a considered equilibrium, and any further easing would require clear evidence that the market has moved to a structurally lower risk of speculation — which the current data does not unambiguously show.

FAQ: Singapore SSD 2026

Does SSD apply if I sell my HDB flat within 3 years?

Yes. SSD applies to HDB flats as well as private residential properties. If you sell your HDB flat within three years of purchasing it (whether from HDB directly in a BTO exercise or as a resale flat from the open market), you are liable for SSD at 12%, 8%, or 4% depending on the year of sale. This is in addition to the HDB Minimum Occupation Period (MOP) rules, which separately prohibit the sale of most HDB flats within the first 5 years. In practice, MOP restrictions mean most HDB sellers are not exposed to SSD — you cannot legally sell a standard HDB flat within 5 years, but the 5-year MOP means the 3-year SSD window has long passed by the time you are eligible to sell. The main HDB exception is resale flats purchased without a direct HDB grant that are nonetheless subject to a 3-year holding period — in that narrow scenario, SSD may overlap with early-sale plans.

Can I use CPF to pay SSD?

No. CPF Ordinary Account (OA) funds cannot be used to pay Seller’s Stamp Duty. SSD must be settled in cash. This is consistent with IRAS’s treatment of all stamp duties — BSD and ABSD payable by buyers may be paid from CPF OA in limited circumstances (for the purchase of a property that is also being financed with CPF), but SSD is a seller-side obligation with no CPF payment route. The SSD amount will be deducted from your sale proceeds (or topped up from your own cash) before the net proceeds are released to you and transferred back to your CPF account (to repay the CPF principal and accrued interest used in the purchase).

Is SSD the same as capital gains tax?

No. SSD is a stamp duty — a transaction tax based on the sale price, not the profit. Singapore does not impose capital gains tax (CGT) on the sale of property. Even if you sell a property at a significant profit, there is no CGT in Singapore. SSD is entirely separate: it is payable based on the timing of the sale (within 3 years) and the sale price, regardless of whether you made a gain or a loss. If you sell at a loss, you still pay SSD. IRAS does not adjust SSD for acquisition costs, renovation costs, or any other expenses. The only figure that matters is the sale price (or market value if higher) multiplied by the applicable rate.

What happens if I gift or transfer the property instead of selling it?

A gift (gratuitous transfer) of a residential property does not involve a sale price, so SSD is technically not triggered in the same way as a sale. However, IRAS treats a gift as a deemed sale at the market value of the property at the time of the gift, for stamp duty purposes. This means that if you “gift” a property to a family member within three years of purchase, IRAS will assess SSD on the market value as though a sale occurred at market price. This prevents the use of gifts as an SSD avoidance mechanism. There are limited exemptions — transfers between spouses and certain court-ordered transfers in divorce — but these are narrow and require IRAS confirmation.

Does SSD apply to EC (Executive Condominium) units?

Yes, with a timing caveat. SSD applies to EC units sold after the EC has received its Temporary Occupation Permit (TOP). The EC must also have passed its 5-year Minimum Occupation Period before the unit can be sold on the open market. In most cases, the MOP ends well after the 3-year SSD window. However, SSD can become relevant for EC owners who acquired their unit through a sub-sale or on the secondary market after TOP but before privatisation (the 10-year mark). In those scenarios, if the EC is sold within 3 years of the sub-sale or secondary-market acquisition, SSD applies. Always check the date of your most recent acquisition — that is the starting date for SSD purposes.

Is there any way to reduce or waive SSD?

IRAS does not offer SSD remissions for financial hardship, relocation, or other personal circumstances. The only genuine way to avoid or reduce SSD is to hold the property beyond the applicable year threshold — 3 years for zero SSD. Partial strategies include: structuring the sale to complete just after the start of a new holding-period year (e.g. selling in Year 2 rather than Year 1 saves 4 percentage points); renting out the property during the holding period to offset costs; or, in extreme cases, exploring whether the property qualifies for one of the statutory exemptions (compulsory acquisition, SERS, inheritance). IRAS administers these strictly and grants remissions only where the statutory criteria are met — there is no discretionary waiver process for ordinary sellers.

How do I pay SSD — and what is the deadline?

SSD is payable to IRAS and is handled by your conveyancing solicitors as part of the sale completion process. If you granted the buyer an Option to Purchase (OTP), SSD must be stamped within 14 days of the date you (as seller) exercised the OTP by accepting the buyer’s notice of exercise. If no OTP was used (e.g. in a direct sale via a Sale and Purchase Agreement), SSD must be paid within 30 days of the date of the SPA. Late payment attracts a penalty of up to S$10 per day or 10 times the duty, whichever is greater, plus interest. Your solicitors will typically handle this automatically through the IRAS e-Stamping system.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Property Tax Guide 2026: IRAS Annual Value, Owner-Occupied Rates and How to Pay

- Singapore CPF for Property Guide 2026: How to Use Your OA, Valuation Limits and Accrued Interest Explained

- Singapore Private Property Buying Guide 2026: Eligibility, ABSD, Financing and Step-by-Step Process

- Singapore Property Cooling Measures Timeline 2009–2026

- En Bloc Sale Singapore 2026: Complete Guide to Collective Sales, 80% Consent and Owner Rights

- Singapore Housing Loan Guide 2026: HDB Loan, Bank Loan, TDSR, MSR and Fixed vs Floating Rates