What Is Seller’s Stamp Duty (SSD)?

Seller’s Stamp Duty (SSD) is a tax payable by the seller when disposing of certain residential and industrial properties in Singapore within a specified holding period. Unlike Additional Buyer’s Stamp Duty (ABSD), which the buyer pays, SSD is borne entirely by the property seller.

Introduced in February 2010, SSD was designed as a cooling measure to deter short-term property speculation and encourage longer-term property ownership. Over the past 16 years, the rates and holding periods have changed multiple times in response to market conditions and Government policy objectives.

For sellers, understanding SSD is critical: it can significantly erode capital gains or even create a loss when selling within the holding period. Many property investors overlook SSD in their calculations and are shocked by the tax bill at completion.

Current SSD Rates in 2026 (Critical Update)

Quick Answer: What Are Today’s SSD Rates?

Residential properties: Depends on purchase date.

- Purchased 11 March 2017 to 3 July 2025: 12% (Year 1) / 8% (Year 2) / 4% (Year 3) / 0% thereafter

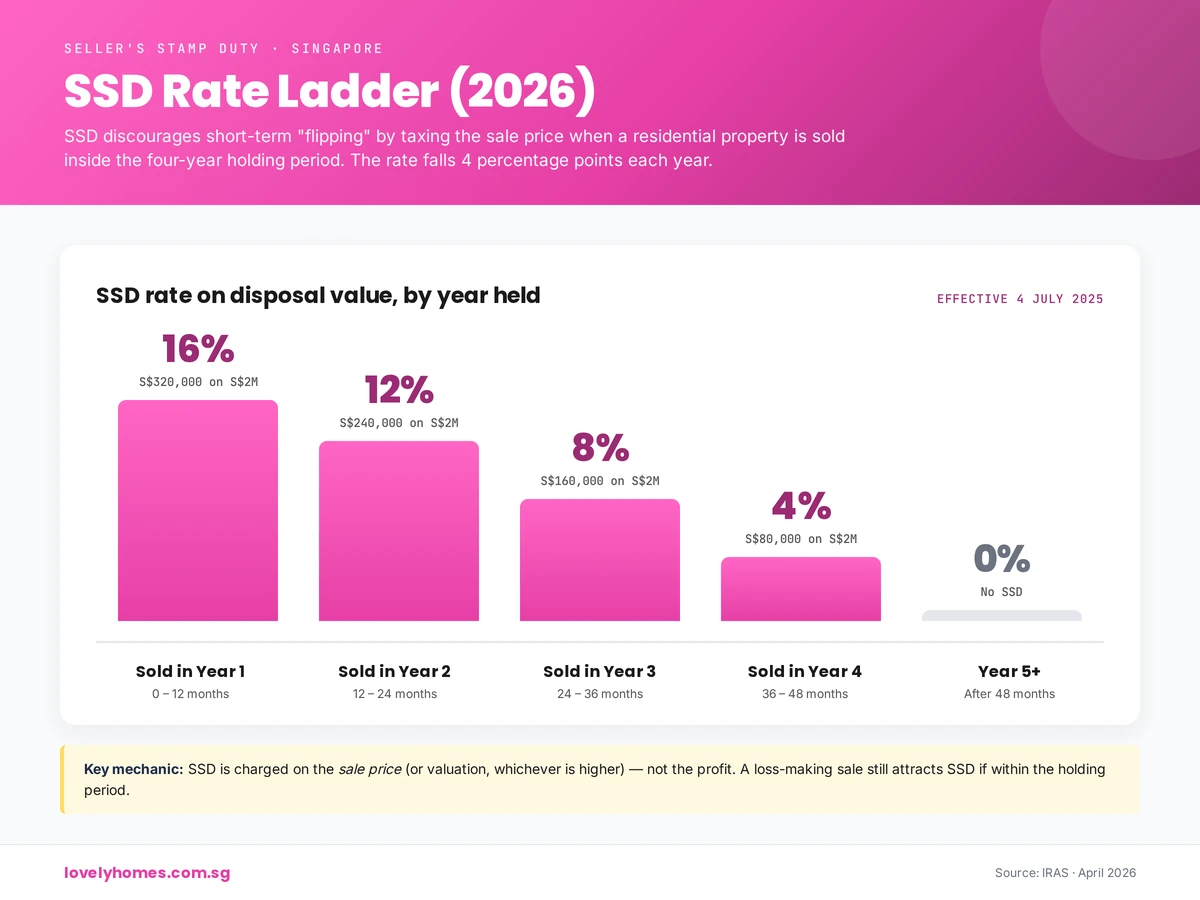

- Purchased on or after 4 July 2025: 16% (Year 1) / 12% (Year 2) / 8% (Year 3) / 4% (Year 4) / 0% thereafter

Industrial properties: 15% (Year 1) / 10% (Year 2) / 5% (Year 3) / 0% thereafter (unchanged since January 2013)

Commercial properties: 0% (retail shops, offices, no SSD applies)

Important: On 4 July 2025, the Government announced a significant restructure of residential SSD, effective for all properties purchased on or after that date. The holding period extended from 3 years to 4 years, and rates increased by 4 percentage points across all tiers.

| Year of Disposal | Residential (Old: purchased ≤ 3 July 2025) | Residential (New: purchased ≥ 4 July 2025) | Industrial |

|---|---|---|---|

| Year 1 | 12% | 16% | 15% |

| Year 2 | 8% | 12% | 10% |

| Year 3 | 4% | 8% | 5% |

| Year 4 | N/A | 4% | N/A |

| Year 5+ | 0% | 0% | 0% |

A Brief History of SSD in Singapore

SSD rates have evolved significantly over the past 16 years, reflecting the Government’s shifting approach to cooling the property market:

- February 2010: SSD introduced at 1% (Year 1) / 2% (Year 2) / 3% (Year 3) for sales within 1 year of purchase.

- August 2010: SSD extended to cover sales within 3 years of purchase, maintaining the 1%/2%/3% rates.

- January 2011: Rates escalated dramatically to 16% (Year 1) / 12% (Year 2) / 8% (Year 3) / 4% (Year 4) over 4 years, coinciding with the Global Financial Crisis aftermath and rising property prices.

- January 2013: Industrial SSD introduced at 15%/10%/5% over 3 years, with no holding period extension thereafter.

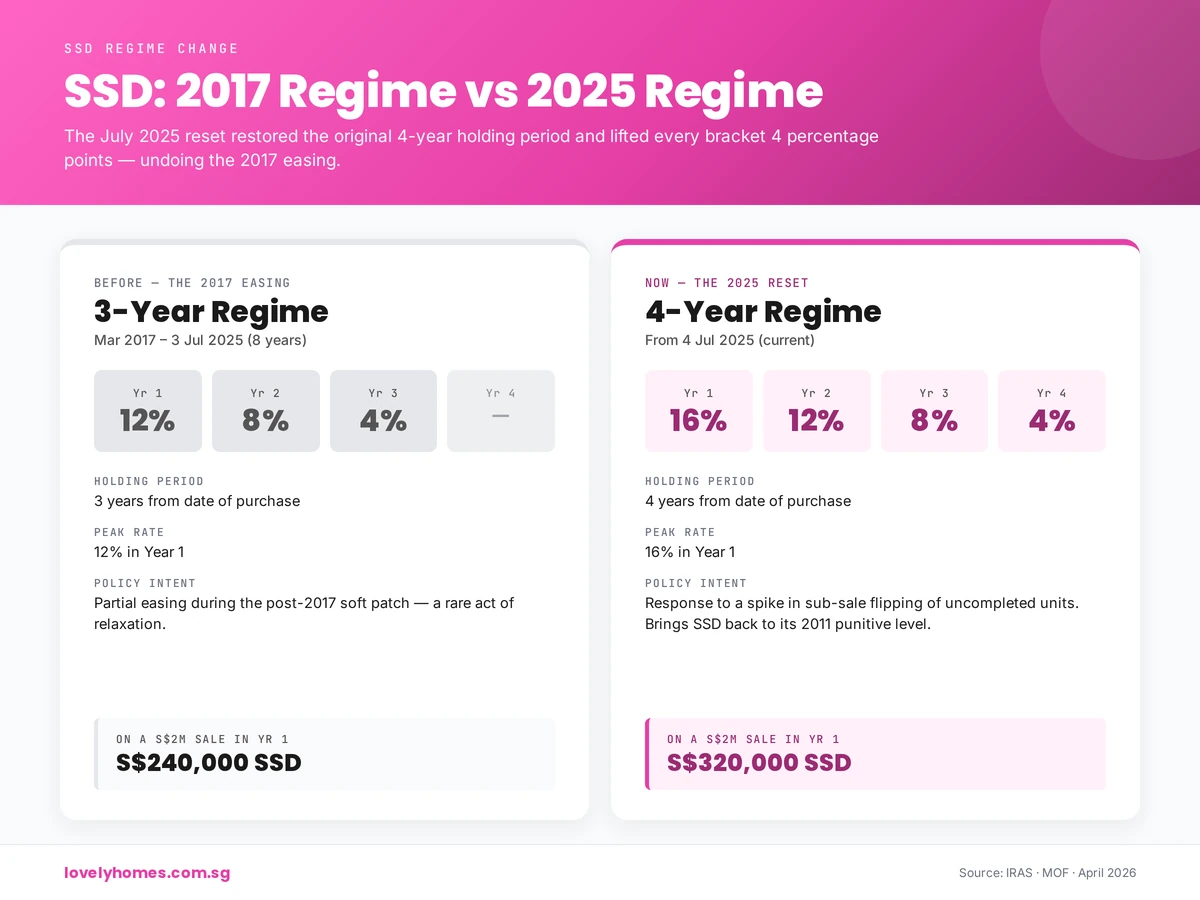

- 11 March 2017: Residential SSD rates eased back to 12% (Year 1) / 8% (Year 2) / 4% (Year 3), and the holding period shortened from 4 years to 3 years. This marked a significant market cooling.

- 4 July 2025: Latest restructure: SSD rates for residential properties increased to 16% (Year 1) / 12% (Year 2) / 8% (Year 3) / 4% (Year 4), and the holding period extended back to 4 years. This applies to all properties purchased on or after 4 July 2025. Properties purchased before this date remain under the 12%/8%/4% regime (3-year holding period).

When Does SSD Apply? Key Conditions

SSD applies when all of the following conditions are met:

- Property type: The property must be residential (private condo, terrace house, landed property) or industrial (factory, warehouse, B1/B2 zoned land). Commercial properties (retail shops, office units) are not subject to SSD.

- Holding period: The property must be sold or disposed of within the holding period (3 years for pre-July 2025 purchases, 4 years for post-July 2025 purchases).

- Disposal triggering event: The relevant date is when the Option to Purchase (OTP) is granted to the buyer or the Sale and Purchase Agreement (SPA) is signed, whichever is earlier. This date marks Day 1 of the holding period.

- Acquisition date: The holding period starts from the date the OTP was exercised or the SPA was signed when you purchased the property (the date you acquired it).

SSD applies to most property disposals: sales to third parties, transfers to family members (unless specifically remitted), gifts, and even transfers in lieu of insolvency. The key trigger is the disposal date relative to the acquisition date.

HDB and SSD

Whilst SSD technically applies to HDB flats purchased after the legislative date (February 2010), in practice, SSD rarely applies to HDB owners because HDB imposes a Minimum Occupation Period (MOP). Most HDB flats have a 5-year MOP, meaning you cannot sell before 5 years have passed. By the time you can sell, the SSD holding period (3 or 4 years) has expired, and you owe no SSD.

However, if you own an HDB flat purchased before the SSD regime and sell early (during a defined period when some flats had shorter MOPs), SSD could theoretically apply. Consult your legal conveyancer for your specific flat’s MOP rules.

Executive Condominiums (ECs) and SSD

Executive Condominiums are subject to SSD if disposed of within the holding period after the MOP expires (typically 5 years). Once the MOP is completed and the property is decoupled from HDB rules, it is treated as a private residential property for SSD purposes.

Worked Examples: How SSD Is Calculated

Example 1: Private Condo Purchased January 2025, Sold June 2026

Scenario: You purchased a private condo on 15 January 2025 for S$1,800,000. You sold it on 20 June 2026 for S$2,000,000. At the time of sale, the property’s market value was assessed at S$1,950,000.

Analysis:

- Purchase date: 15 January 2025 (before 4 July 2025 → old regime applies)

- Sale date: 20 June 2026

- Holding period: Approximately 17 months = Year 2

- SSD rate: 8% (Year 2 rate under old regime)

- Disposal value for SSD: Higher of sale price (S$2,000,000) or market value (S$1,950,000) = S$2,000,000

- SSD payable: 8% × S$2,000,000 = S$160,000

Outcome: Despite a S$200,000 paper gain, you owe S$160,000 in SSD. Your actual net gain after SSD (and ignoring agent fees, legal costs, and ABSD if applicable to the buyer) would be only S$40,000—or entirely erased if other transaction costs are factored in.

Example 2: Private Condo Purchased March 2023, Sold April 2026

Scenario: You purchased a private condo on 10 March 2023 for S$1,600,000. You sold it on 5 April 2026 for S$1,750,000.

Analysis:

- Purchase date: 10 March 2023 (before 4 July 2025 → old regime applies)

- Sale date: 5 April 2026

- Holding period: Approximately 3 years 3 months = beyond Year 3

- SSD rate: 0% (holding period exceeded 3 years)

- SSD payable: S$0

Outcome: You have held the property beyond the 3-year holding period, so no SSD is due. Your entire S$150,000 gain (less transaction costs and ABSD if applicable) is yours to keep.

Example 3: Industrial Property Purchased January 2025, Sold March 2026

Scenario: You purchased an industrial property (warehouse) on 20 January 2025 for S$2,000,000. You sold it on 15 March 2026 for S$2,100,000.

Analysis:

- Property type: Industrial

- Purchase date: 20 January 2025

- Sale date: 15 March 2026

- Holding period: Approximately 14 months = Year 2

- SSD rate: 10% (Year 2 rate for industrial properties)

- Disposal value for SSD: Higher of sale price or market value = S$2,100,000

- SSD payable: 10% × S$2,100,000 = S$210,000

Outcome: Your S$100,000 paper gain is entirely wiped out by the S$210,000 SSD bill. You would need to pay S$110,000 from your own pocket to complete the sale. This illustrates why industrial property flippers face substantial tax penalties.

Example 4: New Regime – Residential Purchased July 2025, Sold November 2026

Scenario: You purchased a private condo on 10 July 2025 for S$1,500,000. You sold it on 15 November 2026 for S$1,650,000.

Analysis:

- Purchase date: 10 July 2025 (on or after 4 July 2025 → new regime applies)

- Sale date: 15 November 2026

- Holding period: Approximately 16 months = Year 2

- SSD rate: 12% (Year 2 rate under new regime)

- Disposal value for SSD: S$1,650,000

- SSD payable: 12% × S$1,650,000 = S$198,000

Outcome: Under the new, stricter regime, even a modest 10% appreciation is swallowed by a 12% SSD rate. The sale results in a net loss of approximately S$48,000 (before other transaction costs).

How SSD Is Calculated: Disposal Value

A critical point: SSD is calculated on the higher of the selling price or the market value of the property as at the date of sale.

If you sell below market value (e.g., to a family member at a discount, or in a distressed sale), the property’s assessed market value may still be used by IRAS to compute SSD. You cannot reduce your SSD bill by negotiating a lower sale price.

Market value is typically determined by a professional valuation, comparable sales data, or IRAS’s own assessment. If you believe IRAS’s valuation is incorrect, you can request a review, but the onus is on you to provide supporting evidence.

How to Legally Avoid or Minimise SSD

SSD is a significant liability for property sellers. Fortunately, several legitimate strategies exist:

1. Hold for the Full Period (3 or 4 Years)

The most straightforward approach: Hold your residential property for at least 3 years (if purchased before 4 July 2025) or 4 years (if purchased after) before selling. Once the holding period expires, SSD drops to 0%, and you keep your entire gain.

For industrial properties, hold for 3 years to eliminate SSD.

This strategy is ideal if you can afford to hold the property long-term. Many professional investors plan around these holding periods when structuring their portfolios.

2. Timing the OTP Carefully (Within Limits)

The key holding-period dates are:

- Start date: The date you exercised the OTP or signed the SPA when you purchased the property.

- End date: The date you granted the OTP to the buyer or signed the SPA when you sold the property.

If you purchased on 10 January 2025, the 3-year threshold is reached on 10 January 2028. If you can delay granting your buyer’s OTP until 10 January 2028 or later, SSD drops to 0%.

However, there are strict limits: You cannot artificially delay the OTP grant date if you have already agreed to sell. Doing so could constitute a breach of contract or fraud. The dates must reflect genuine transaction timings.

3. Properties Exempt or Remitted from SSD

Certain disposals qualify for full SSD remission or exemption:

- Compulsory Acquisition (CA) by the Government: If your property is acquired under the Land Acquisition Act (e.g., for public housing, roads, or infrastructure), SSD is fully remitted.

- Developer Repurchase: If a property developer repurchases a unit within a stipulated period (e.g., within 5 years of the original sale for some EC schemes), SSD may be remitted under the scheme’s terms.

- Matrimonial Property Transfer: Transfers of residential property between spouses or ex-spouses as part of matrimonial or ancillary relief proceedings may qualify for remission if executed pursuant to a Court Order. However, this is a narrow exemption—consult a legal advisor.

- HDB Repurchase by HDB: If HDB repurchases a flat from you (e.g., under right of first refusal schemes), SSD is typically remitted.

- Bankruptcy or Insolvency: In certain insolvency situations, SSD may be remitted if the property is disposed of by a trustee or official receiver under court order.

These exemptions are narrow and require specific conditions. If you believe you qualify, consult a licensed conveyancing lawyer or contact IRAS directly for a ruling.

4. Decoupling Strategy (With Caution)

If you are married and own property as joint tenants, decoupling (transferring one spouse’s share to the other spouse) creates a new acquisition date for the transferred share. This means the holding period for that share restarts.

Example: You and your spouse bought a property jointly on 1 January 2025. On 1 July 2026, you transfer your spouse’s share to yourself. Your spouse’s share now has a new acquisition date (1 July 2026), so its holding period restarts. If you then sell the entire property on 1 January 2027, your share is subject to Year 2 SSD, but your spouse’s share (which was only held from July 2026 to January 2027 = 6 months = Year 1) would trigger Year 1 SSD on that portion.

This strategy is complex, has significant stamp duty and ABSD implications, and may not be worthwhile. Do not attempt without guidance from a tax professional and conveyancer.

5. Beware: Legitimate Avoidance vs. Tax Evasion

There is a clear legal line between legitimate tax planning and tax evasion:

- Legitimate: Holding the property longer, timing transactions around the 3-year mark, claiming available exemptions.

- Illegal: Falsifying transaction dates, under-declaring the sale price, splitting the sale into multiple transactions to circumvent SSD, or using straw buyers.

IRAS actively audits property transactions and has recovered substantial SSD arrears from taxpayers who attempted to evade the tax. The penalties (including interest and potential prosecution) far exceed any tax saved.

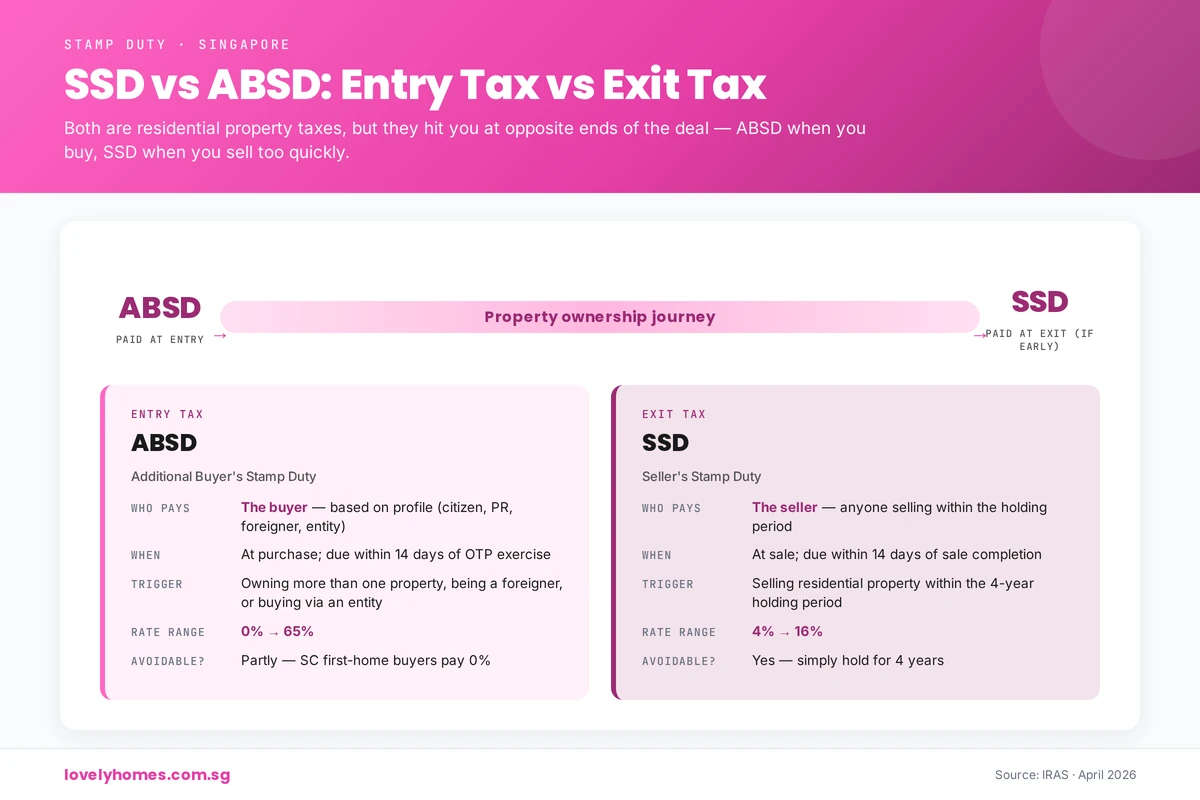

SSD vs. ABSD: What’s the Difference?

Many property sellers confuse SSD (Seller’s Stamp Duty) with ABSD (Additional Buyer’s Stamp Duty). They are separate taxes and can both apply to a single transaction:

| Aspect | SSD (Seller’s Stamp Duty) | ABSD (Additional Buyer’s Stamp Duty) |

|---|---|---|

| Payable By | Seller | Buyer |

| When | At sale, if property sold within holding period (3 or 4 years) | At purchase, if buyer is foreigner, company, trust, or owns other properties |

| Applies To | Residential & industrial properties only | Residential properties only (no ABSD on industrial) |

| Purpose | Deter short-term speculation by sellers | Deter foreign ownership & multiple property purchases by buyers |

| Example Rate | 12% (Year 1, old regime) or 16% (Year 1, new regime) | 30% (if foreigner buying 1st residential property) |

Key Point: Both SSD and ABSD can apply to a single transaction. If a Singaporean citizen (owner) sells a residential property within 3 years to a foreign buyer (or to another Singaporean who already owns 1+ properties), the seller pays SSD and the buyer pays ABSD. Each is computed on the transaction price and borne by the respective party.

Frequently Asked Questions (FAQ)

Q1: Who decides what the “disposal value” is for SSD calculation?

A: The disposal value is the higher of the actual selling price or the property’s market value as at the date of sale. If you sell at S$2M but IRAS assesses the market value at S$2.2M, SSD is computed on S$2.2M. You can appeal IRAS’s valuation, but the burden is on you to prove the value with evidence (comparables, professional appraisals). In most cases, the selling price is the disposal value, unless it is significantly below market (a rare event).

Q2: Can I use my CPF to pay SSD?

A: No. SSD is a seller’s cost and must be paid from the sale proceeds or your own funds. CPF can only be used to purchase residential property and to pay the conveyance duty (stamp duty) on the purchase itself, not on the sale or SSD. SSD is withheld from your sale proceeds at completion.

Q3: Does SSD apply if I gift my property to a family member?

A: Yes, in principle, SSD applies to gifts unless a specific remission is granted. The “disposal value” for a gift is the property’s market value (since there is no actual sale price), and SSD is computed on that value. However, if the gift is part of a matrimonial order or compulsory acquisition, remission may apply. For most family gifts without legal exemption, SSD is payable by the donor (gift-giver). Consult a lawyer before gifting property if within the holding period.

Q4: Does SSD apply if I inherited the property?

A: No, SSD does not apply to inherited properties. Inheritance is not a “disposal” triggering SSD; it is a transmission of title by operation of law upon death. Your holding period for SSD purposes starts from the date the original buyer (the deceased) purchased the property. If the deceased held it for more than 3 years before dying, there is no SSD when you (the heir) subsequently sell. If the deceased had held it less than 3 years and you sell shortly after, you may owe SSD, but the holding period is measured from the original purchase date, not your inheritance date.

Q5: Does SSD apply to HDB flats?

A: Technically, yes—SSD applies to HDB flats purchased after February 2010. However, in practice, SSD rarely triggers for HDB owners because HDB imposes a Minimum Occupation Period (typically 5 years). Once you can sell (after MOP), the SSD holding period has usually expired. If you own an older HDB flat or one with a shorter MOP and sell within the holding period, SSD would apply. Check your flat’s MOP with HDB before selling early.

Q6: Can I get SSD back if the buyer backs out?

A: SSD is paid at completion of the sale (when the sale is finalised and transferred to the buyer). If the buyer backs out before completion, the sale does not complete, and SSD is not triggered or payable. If the sale completes and you have paid SSD, but the buyer later defaults or the sale is reversed (rare), you would need to seek legal remedy or negotiate a refund directly with the buyer. IRAS does not refund SSD unless the underlying transaction is formally set aside by Court order.

Q7: How is SSD calculated on an incomplete property (Build-to-Completion, BUC)?

A: For a property sold before completion of construction (i.e., before the Completion Certificate is issued), SSD is calculated on the contract price (as stated in the SPA or OTP), not the actual completion value. The holding period is measured from the date the OTP was exercised on the original purchase. If you resale a BUC unit within the holding period, SSD is due on the resale price. This is an area where many investors get caught—ensure you understand the SSD implications before flipping an off-plan property.

Q8: What happens if I sell a property that is jointly owned with my spouse?

A: If you and your spouse own a property as joint tenants or tenants-in-common, the sale price is shared (usually 50/50 unless another ratio is agreed). SSD is calculated on the full sale price, but it is paid from the joint sale proceeds. The holding period is the same for both owners (it starts from the date the property was first acquired). No special relief applies merely because of joint ownership; both spouses are treated as single sellers of a single property. If you decouple (transfer one spouse’s share to the other), the transferred share gets a new acquisition date, which can complicate SSD calculations.

Q9: Can I defer or spread SSD payments over time?

A: No, SSD must be paid in full at the point of completion (when the sale is finalised). There is no option to spread the payment or defer it. Your conveyancer will calculate the SSD owed and ensure it is deducted from the sale proceeds before you receive your net amount. If you cannot afford the SSD, the sale cannot complete, and you remain the owner.

Q10: Are there any SSD changes coming in 2026/2027?

A: As of April 2026, no further changes to SSD have been announced. The most recent restructure took effect on 4 July 2025 (16%/12%/8%/4% over 4 years for properties purchased on or after that date). Keep monitoring IRAS’s official website and Government budget announcements for any future changes. However, do not assume changes; rely only on official announcements from IRAS and the Ministry of Finance (MOF).

Related Articles & Resources

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty Rates

- Stamp Duties & Taxes Category: All Articles on Property Taxes in Singapore

- Property Cooling Measures: Comprehensive Coverage of SSD, ABSD, MSR & More

- Property Investment Guide: Strategies for Singapore Real Estate Investors

- Buyer’s Guide: Navigate Singapore Property Purchase Process

- Laws, Regulations & Policies: Property Rules & Government Announcements

Important Disclaimer

This guide is provided for general informational purposes only and does not constitute legal, tax, financial, or investment advice. SSD rates, holding periods, and exemptions are subject to change at the discretion of the Government of Singapore and the Inland Revenue Authority of Singapore (IRAS).

Before making any property transaction, you must:

- Verify the current SSD rates on the official IRAS website: IRAS Seller’s Stamp Duty for Residential Property

- Consult a licensed conveyancing lawyer to understand your specific SSD liability based on your property’s purchase and sale dates.

- Obtain a professional valuation if you believe the market value of your property may differ significantly from the sale price.

- Contact IRAS directly for clarification on any specific scenarios or exemptions that may apply to your situation.

Property laws change, and individual circumstances vary widely. LovelyHomes.com.sg and its authors assume no liability for actions taken based on this guide. Always seek independent professional advice before committing to a property transaction.

0 Comments