Singapore stamp duty is not a single tax — it is a suite of four distinct levies that can collectively add hundreds of thousands of dollars to the cost of a property transaction. Understanding each one, when it applies, and how to calculate it is essential before you sign any Option to Purchase. This guide covers all four: Buyer’s Stamp Duty (BSD), Additional Buyer’s Stamp Duty (ABSD), Seller’s Stamp Duty (SSD), and Additional Conveyance Duty (ACD).

All figures are current as at 31 May 2026. For the authoritative position, always refer to the IRAS Stamp Duty page and consult a licensed conveyancing lawyer before transacting.

Quick Answer — Singapore Stamp Duty at a Glance

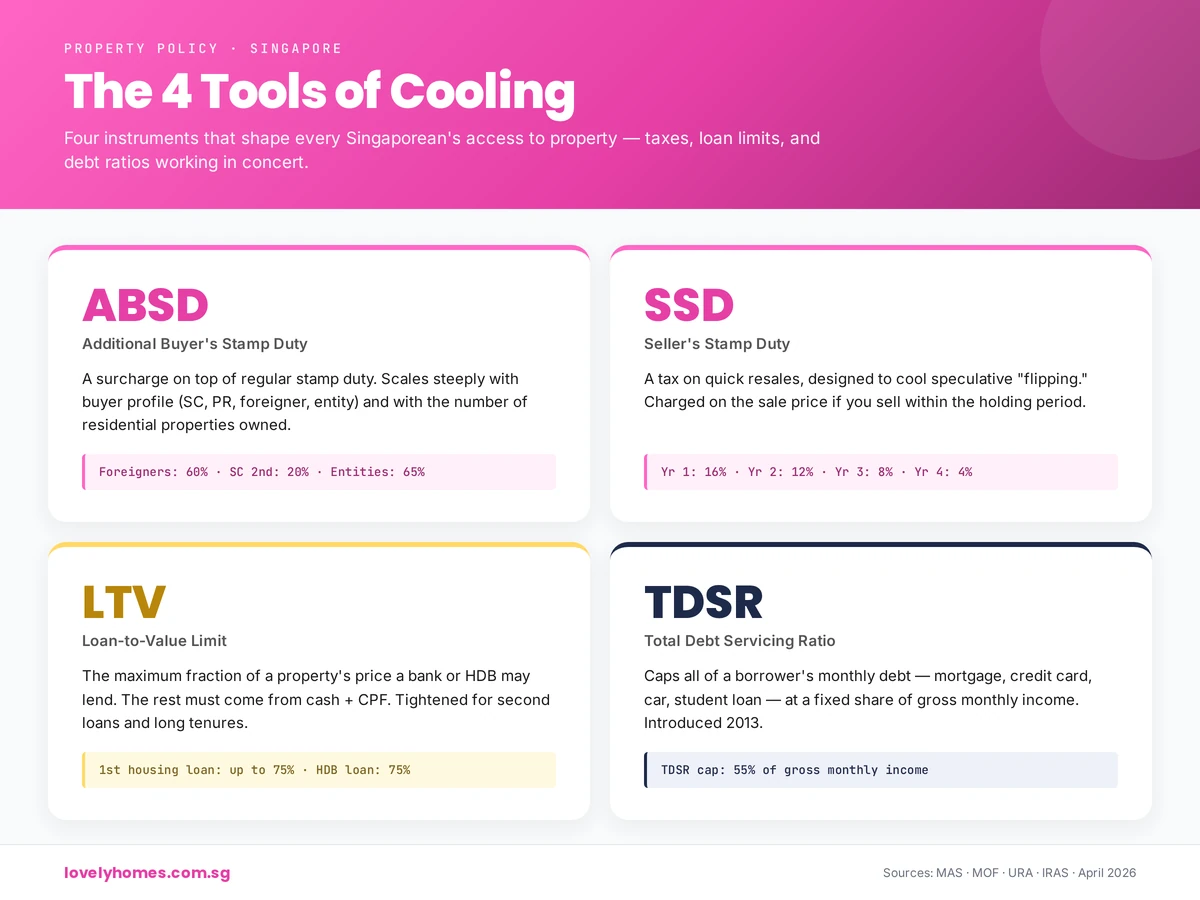

BSD — payable by EVERY buyer on every property purchase. Progressive rates 1%–6%.

ABSD — additional levy on top of BSD. Singapore Citizens pay 0% on their first property, 20% on their second, 30% on their third+. PRs pay 5%/30%/35%. Foreigners pay 60% on any residential property.

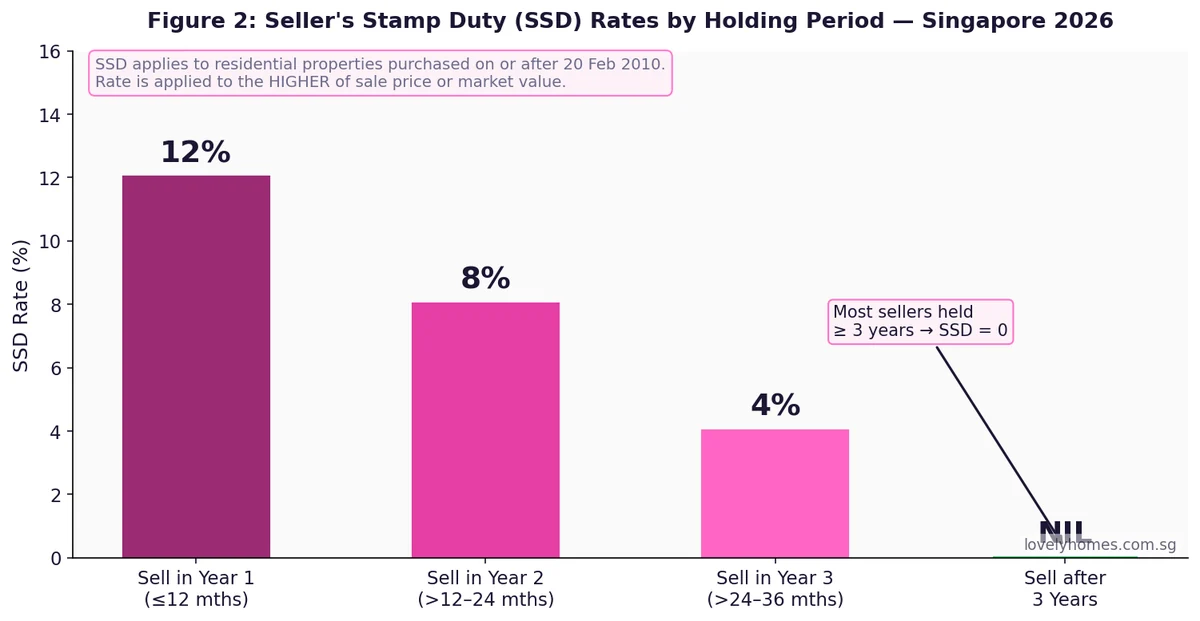

SSD — payable by the SELLER if the property is sold within 3 years of purchase. Rates: 12% (Year 1), 8% (Year 2), 4% (Year 3), nil thereafter.

ACD — applies when residential property is transferred indirectly through corporate equity. Flat 33% on the residential property value component.

BSD and ABSD are payable within 14 days of the Option to Purchase (OTP) or Sale & Purchase Agreement.

SSD is payable within 14 days of the sale contract.

CPF cannot be used to pay stamp duty at the point of purchase — you must pay in cash first, then apply for CPF reimbursement.

ABSD remission is available to Singapore Citizen couples replacing their matrimonial home — subject to conditions and strict timelines.

What Is Stamp Duty and Why Does Singapore Use It?

Stamp duty is a transaction tax levied on documents that effect the transfer of a property or shares in a property-holding entity. In Singapore, the Inland Revenue Authority of Singapore (IRAS) administers all stamp duties under the Stamp Duties Act (Cap. 312). The modern stamp duty regime serves two purposes: raising revenue, and acting as a macro-prudential tool to moderate speculative demand in the residential property market.

When you buy a residential property, you will encounter BSD and possibly ABSD. When you sell, SSD may apply if you sell too quickly. If a property changes hands through an equity transfer in a company, ACD enters the picture. Each levy has its own trigger, its own rate schedule, and its own payment deadline.

Buyer’s Stamp Duty (BSD) — the Baseline Tax Every Buyer Pays

BSD is the foundational property transaction tax. Every buyer — regardless of citizenship, residency status, or how many properties they already own — pays BSD on every property purchase. It is computed on the higher of the purchase price or the market value of the property at the time of acquisition.

The rates are progressive for residential property:

Purchase Price / Market Value

BSD Rate

Max BSD from This Tier

First S$180,000

1%

S$1,800

Next S$180,000

2%

S$3,600

Next S$640,000

3%

S$19,200

Next S$500,000

4%

S$20,000

Next S$1,500,000

5%

S$75,000

Above S$3,000,000

6%

No cap

A separate, flat-rate BSD schedule applies to non-residential property (commercial, industrial): 1% on the first S$180,000, 2% on the next S$180,000, and 3% on the remainder — capped at 3%. The progressive residential schedule shown above took effect for instruments executed on or after 15 February 2023, when the 5% and 6% tiers were introduced for high-value transactions.

Worked example (BSD only, S$1.5M residential condo):

First S$180,000 × 1% = S$1,800 Next S$180,000 × 2% = S$3,600 Next S$640,000 × 3% = S$19,200 Next S$500,000 × 4% = S$20,000 Total BSD = S$44,600

BSD is a fixed cost — there is no way to reduce it lawfully short of negotiating a lower purchase price. It is also not remissible (there are no BSD remission schemes for residential buyers equivalent to the ABSD remission).

Additional Buyer’s Stamp Duty (ABSD) — the Policy Lever

ABSD was introduced in December 2011 and has been raised five times since, most recently in April 2023. It is the single largest upfront cost for most second-property buyers and foreigners. ABSD is levied on top of BSD, at a flat rate on the entire purchase price.

Figure 1: Total stamp duty (BSD + ABSD) payable by buyer profile and property price — Singapore 2026. Source: IRAS.

The current ABSD rate schedule (applicable to instruments executed on or after 27 April 2023) is:

Buyer Profile

1st Property

2nd Property

3rd & Subsequent

Singapore Citizen (SC)

0%

20%

30%

Singapore Permanent Resident (SPR)

5%

30%

35%

Foreigner (individual)

60%

60%

60%

Entity (company, trustee)

65%

65%

65%

Housing developer

40%*

40%*

40%*

* 5% of the developer ABSD is non-remittable. The remaining 35% is remittable upon completing the project and selling all units within 5 years.

FTA nationals — citizens of Iceland, Liechtenstein, Norway, Switzerland, and the United States — are accorded Singapore Citizen ABSD treatment under the respective Free Trade Agreements.

For a detailed breakdown of ABSD remission schemes (including the Married Couple Remission for upgraders), see our ABSD Complete Guide 2026.

Seller’s Stamp Duty (SSD) — the Anti-Flipping Tax

SSD was introduced in February 2010 to discourage short-term residential property speculation. It is paid by the seller (not the buyer) when a residential property is disposed of within three years of its acquisition. The rate depends on how quickly the seller flips the property:

Figure 2: SSD rates by holding period — residential property, Singapore 2026. Source: IRAS.

SSD is calculated on the higher of the sale price or the market value at the time of disposal. The holding period is measured from the date of purchase (execution of the Sale & Purchase Agreement) to the date of sale (execution of the disposal S&P). SSD does not apply to properties acquired before 20 February 2010, nor does it apply to commercial or industrial property.

Note: If you inherit a property and subsequently sell it, the SSD holding period runs from the original purchase date (the date the deceased acquired the property), not from the date of inheritance. This is a common source of confusion. If a parent bought a condo in 2024 and passed away in 2025, and the heir sells in early 2026, SSD at 8% could still apply.

The SSD is the reason most investor-buyers hold Singapore residential property for at least three years before selling. In practice, the combination of SSD and the time needed to recover transaction costs (BSD + ABSD + legal fees + agent commissions) means the effective minimum hold for a profitable flip is typically four to five years.

Additional Conveyance Duty (ACD) — the Entity Transfer Tax

ACD was introduced in May 2017 to close a loophole that allowed buyers to acquire residential property held in companies without paying ABSD — by buying shares in the company rather than the property directly. Under the ACD regime, a transfer of equity interests in a residential-property-holding entity is taxed as if it were a direct property acquisition.

ACD applies when:

The acquirer obtains a significant ownership interest (≥50%) in an entity (company, trust, or partnership);

That entity holds Singapore residential property as its primary asset; and

The residential property component exceeds a de minimis threshold.

The ACD rate is 33% on the residential property value component, levied on top of the existing stamp duty on the share transfer (which is normally 0.2%). For a $10 million residential property held in a company, an ACD transaction could trigger an additional $3.3 million in duty — making it broadly equivalent in cost to a direct ABSD transaction.

ACD is highly specialised and typically arises in commercial real estate transactions, family wealth restructuring, or en-bloc-related scenarios. Most individual residential buyers will never encounter it. If you are structuring a transaction that involves acquiring shares in a company that holds Singapore residential property, engage a tax adviser with stamp-duty expertise before proceeding.

Summary: All Four Singapore Stamp Duties at a Glance

Duty

Who Pays

When It Applies

Rate (Residential)

Deadline

BSD

Buyer

All property purchases

1%–6% progressive

14 days from OTP/S&P

ABSD

Buyer

2nd+ property / foreigner / entity

0%–65% flat on full price

14 days from OTP/S&P

SSD

Seller

Sold within 3 years of purchase

4%–12% flat on full price

14 days from disposal S&P

ACD

Acquirer of equity

≥50% stake in residential-property entity

33% on resi property value

14 days from share transfer

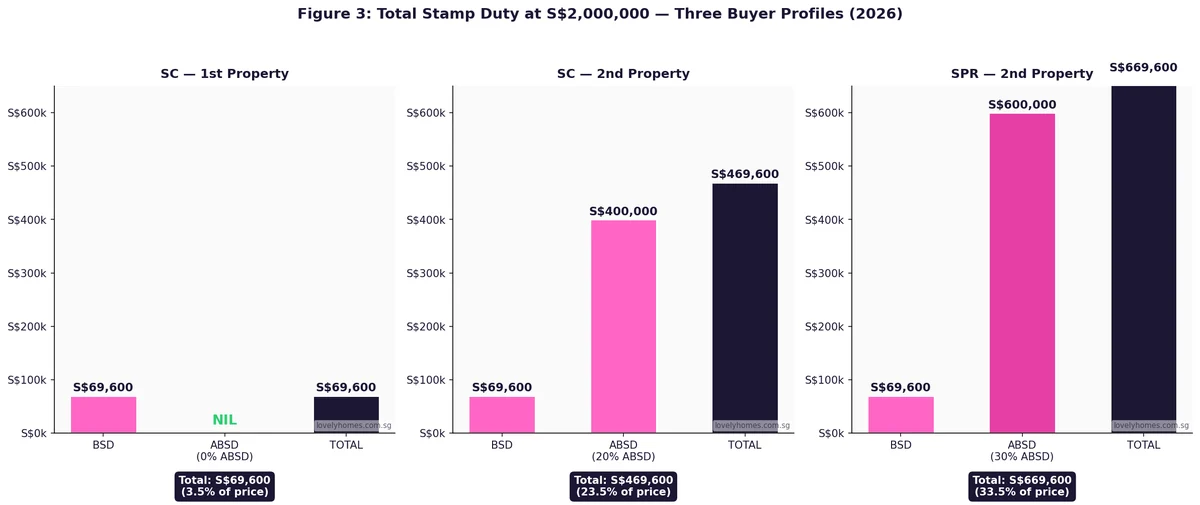

Comprehensive Worked Example: SC Couple Upgrading from HDB to Private Condo

Mr & Mrs Pang are Singapore Citizens. They own a Bishan 5-room HDB flat (purchased 2018, fully paid under CPF). They want to buy a S$2,000,000 2-bedroom freehold condo in District 10 and sell the HDB afterwards. Here is the full stamp duty picture:

Scenario A: Buy the condo BEFORE selling the HDB

Because they still own the HDB, the condo is their second residential property. ABSD at 20% is triggered.

BSD on S$2,000,000: S$64,600

ABSD (20%): S$400,000

Total stamp duty: S$464,600

However, they can apply for the ABSD Married Couple Remission — they get the S$400,000 back if they sell the HDB within 6 months of the later of (a) the condo’s purchase date or (b) its TOP date.

They must pay the ABSD upfront in cash and wait for the refund.

Scenario B: Sell the HDB FIRST, then buy the condo

After selling the HDB, they hold zero residential properties. The condo becomes their first residential property. Zero ABSD.

BSD on S$2,000,000: S$64,600

ABSD: S$0

Total stamp duty: S$64,600

Figure 3: Total stamp duty at S$2,000,000 — SC 1st property, SC 2nd property, and SPR 2nd property compared. Source: IRAS 2026.

Scenario B saves the Pangs S$400,000 and avoids the need for the remission application. The trade-off is the risk of not finding a new home before the HDB sale completes — and potentially needing temporary accommodation in the interim. Many upgrading couples use a bridging loan to manage this gap.

When Does Stamp Duty Really Matter? — Why These Numbers Are So Significant

Stamp duty in Singapore is, by international standards, among the highest in the world for non-citizen buyers. A foreign individual purchasing a S$3 million residential property in 2026 faces: BSD of approximately S$119,600 plus ABSD of S$1,800,000 — a total of S$1,919,600, or 64% of the purchase price. This is intentional: the Government has consistently stated that Singapore’s residential property market is primarily for Singaporeans to live in, and the ABSD is the mechanism that enforces that policy goal.

For Singapore Citizens, the numbers are far more manageable — but still significant. A first-time buyer at S$2 million pays S$64,600 in BSD alone. For an upgrader buying their second property at the same price, adding S$400,000 in ABSD transforms what might otherwise be a healthy financial decision into a transaction that requires either substantial cash reserves or careful sequencing via the remission route.

Stamp duty also has a secondary effect on the property market as a whole: it creates a minimum holding period incentive. Investors who pay BSD and ABSD on entry need their property to appreciate by at least those amounts — plus legal costs, agent commissions, and financing costs — before they break even on a sale. This structurally discourages short-term speculation and was a deliberate part of the policy design when rates were raised in 2021 and 2023.

What Might Change in 2026 and Beyond?

This section is speculative analysis, not official policy.

As at May 2026, there has been no signal from the Ministry of Finance or MAS of imminent changes to the stamp duty regime. Private residential prices rose 0.9% in Q1 2026 — a moderate pace that does not, on its own, suggest further tightening is imminent. The Government has traditionally intervened when quarterly price growth exceeds 2–3% or when transaction volumes indicate re-entry of speculative buyers.

Watch for the following triggers that could lead to a review: (1) sustained quarter-on-quarter private price growth above 2% for two or more consecutive quarters; (2) a significant rise in foreign buyer transactions as a proportion of total; (3) a global interest rate environment that makes Singapore dollar assets more attractive to offshore capital. Conversely, a sharp economic slowdown could prompt targeted relief — as was done in 2020 with the COVID-19 stamp-duty deferral scheme.

Frequently Asked Questions

Can I use my CPF to pay stamp duty?

No, not at the point of payment. BSD and ABSD (and SSD for sellers) must be paid in cash by the statutory deadline. After the duty has been stamped and paid, you may apply to withdraw from your CPF Ordinary Account to reimburse the cash outlay, provided the property qualifies under CPF Board rules and you have sufficient OA balance. The CPF withdrawal is a reimbursement step, not a direct payment channel.

Does SSD apply if I sell because of financial hardship?

There are no hardship exemptions to SSD built into the Stamp Duties Act. SSD is triggered automatically on any disposal within 3 years of purchase, regardless of the reason for sale. IRAS has no general discretion to waive SSD except in the specific circumstances defined in the Act (e.g. compulsory acquisition by the state). If you are facing distress and need to sell within the SSD window, factor the SSD cost into your net sale proceeds before deciding.

My spouse is a foreigner. Do we pay 60% ABSD on our first home together?

For a jointly-owned first matrimonial home where one owner is a Singapore Citizen and the other is a foreigner, the couple can apply for ABSD remission to be taxed at the SC rate (0% on a first property). The remission is available for a property that will be used as the couple’s matrimonial home, and conditions must be met. The ABSD is still payable upfront at the foreigner rate; the remission is applied for thereafter. Engage a conveyancing lawyer well before the OTP is exercised to ensure the remission application is properly structured.

Is stamp duty payable on a property gift (transfer without payment)?

Yes. BSD (and ABSD where applicable) is computed on the market value of the property at the time of transfer, even if no money changes hands. A parent transferring a private condo to an adult child as a gift is treated as a purchase at market value for stamp duty purposes. The child is treated as the buyer and must pay BSD and ABSD based on their own buyer profile and existing property count.

How is stamp duty calculated for an uncompleted property (new launch)?

For an uncompleted unit bought directly from the developer, the stamp duty is computed on the purchase price stated in the Sale & Purchase Agreement (which is executed at the point of booking the unit). ABSD — where applicable — is payable within 14 days of the S&P execution, which means the full ABSD amount is due upfront even though the project may not complete for several years. The Married Couple Remission window (6 months to sell the existing property) runs from the later of the S&P date or the Temporary Occupation Permit (TOP) date.

Does stamp duty apply to HDB flat purchases?

Yes. BSD applies to all HDB flat purchases (new BTO and resale) at the same progressive rates as private residential property. For new BTO flats, BSD is computed on the selling price set by HDB; for resale, it is on the higher of the resale price or HDB’s valuation. ABSD also applies to HDB flat purchases under the same rules — although Singapore Citizen first-time buyers pay 0% ABSD, meaning only BSD is due. SPR first-time buyers face 5% ABSD even on an HDB flat purchase.

Disclaimer: This article is for general informational purposes only and does not constitute legal, tax, or financial advice. Stamp duty rates and remission rules may change. Always verify the current position with the IRAS Stamp Duty page and the Ministry of Finance. Consult a licensed conveyancing lawyer or tax specialist before transacting.

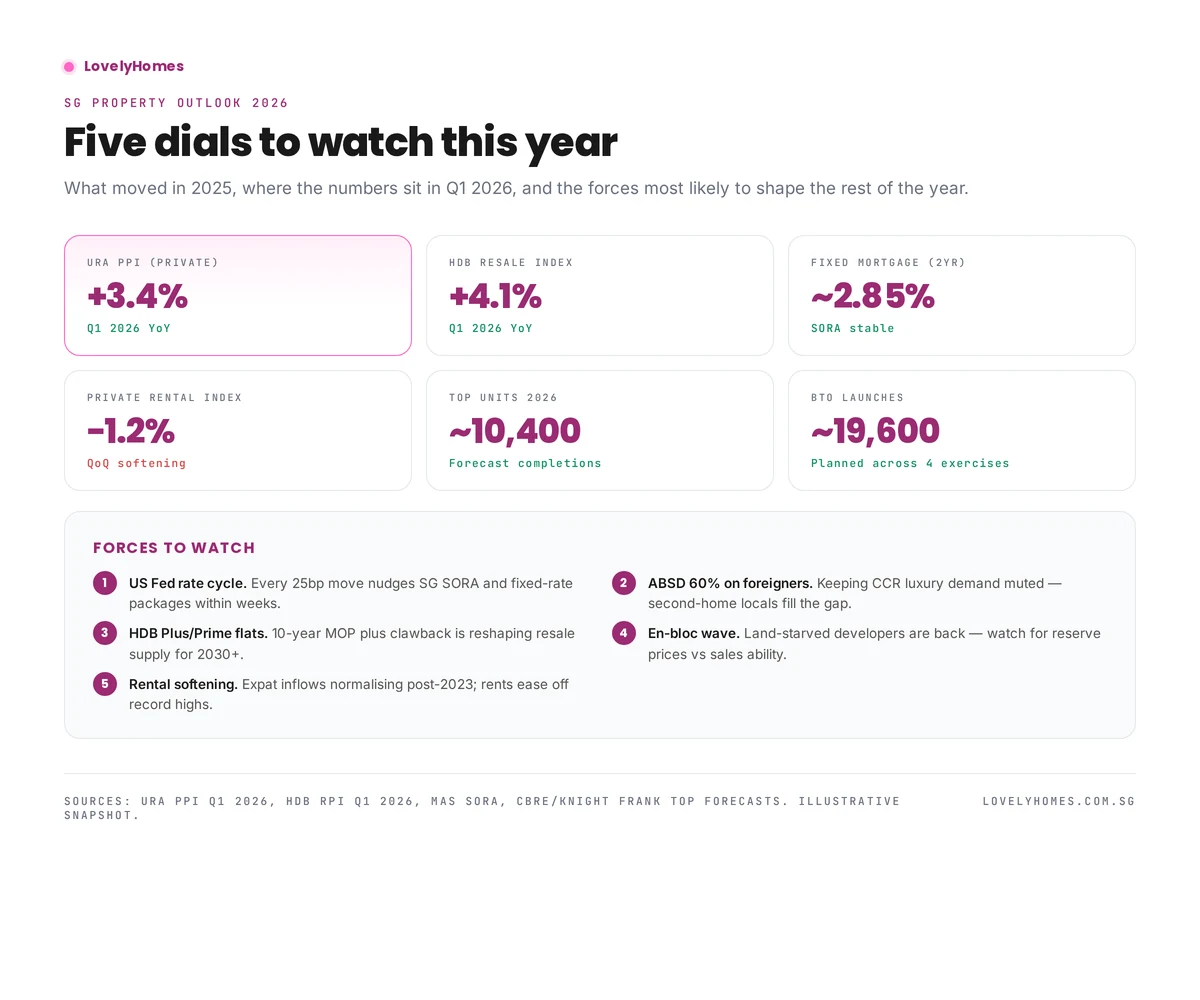

Singapore’s 2026 private residential market is entering the year with URA PPI up 3.4% YoY and HDB resale index up 4.1% YoY. Mortgage rates have stabilised in the mid-2% band. Private rents have softened 1–2% QoQ as expat-driven demand normalises. The five forces most likely to shape the rest of 2026 are: (1) US Fed rate path, (2) the 60% foreigner ABSD, (3) HDB Plus/Prime flat supply, (4) en-bloc activity, (5) rental yield compression from rising wages.

Every January, analysts publish a property outlook for the year ahead. Most read more like agent talking-points than analysis. This one tries to do the opposite — state the numbers as they stand at Q1 2026, name the forces that will move them, and flag where consensus is most likely to be wrong.

This is a general-market view, not a valuation of any specific district. For district-level granularity, watch our forthcoming Area Guide series. For the tax and cooling-measure context that underpins all of the below, start with our cooling measures timeline.

Q1 2026 snapshot of the five market dials that matter most.

Prices — private and public

URA Private Residential Price Index

URA PPI closed 2025 at record highs. The Q1 2026 flash estimate is +3.4% YoY, with the RCR (city fringe) band leading at roughly +4.6% and CCR lagging at +2.1%. OCR sits in between at +3.9%.

HDB Resale Price Index

HDB RPI is tracking +4.1% YoY — the eighth consecutive quarter of gains, but the pace has decelerated from the double-digit 2022 run. Million-dollar HDB transactions have broadened from central flats into Bishan, Bukit Merah, Queenstown and, increasingly, mature Bidadari and Kallang Whampoa.

Interest rates and financing

3-month compounded SORA has drifted into the 2.5–2.9% range. Fixed packages from local banks are quoting around 2.85% for two-year tenors. That is well below the 2023 peak (~4%) but still meaningfully higher than the 2020–2021 sub-2% era.

Two upshots:

Refinancing activity is picking up for loans originated at the 2023 peak. See our refinancing guide.

TDSR bites harder than it did pre-2022. Affordability constraints more than prices are now the dominant buying-decision driver. Our TDSR & MSR guide explains the maths.

Supply coming through

Segment

Units landing 2026

Impact

Private residential TOP

~10,400

Keeps rental supply refreshed

EC TOP

~3,800

HDB upgraders hand back resale flats

BTO launches (planned)

~19,600 flats

Large Plus/Prime share

Rental market

After the extraordinary 2022–2023 surge (+25% to +30% YoY at the peak), rents are normalising. Q4 2025 URA rental index was down 1.2% QoQ. Expect a sideways-to-softer 2026, especially for older non-integrated condos as expat renters rotate into newer stock.

Five forces shaping the rest of 2026

US Fed rate path. Every 25bp shift flows through SORA and fixed packages in weeks.

The 60% foreigner ABSD. Kept CCR luxury flat. Any softening would re-ignite CCR transaction volumes.

HDB Plus / Prime supply. 10-year MOP plus subsidy clawback is reshaping the 2030+ resale pool.

En-bloc cycle. Developers are land-starved; reserve prices that reflect cooling measures may finally clear.

Rental compression. Yields moderate as wages normalise; investor maths re-anchors on capital appreciation, not cash flow.

Frequently asked questions

Will prices fall in 2026?

Base case: no. Prices grind higher at low single digits. Downside case: if the Fed holds rates longer than expected and supply lands faster, a flattish 2H 2026 is plausible.

Is now a good time to buy?

Depends on your horizon and cash flow. Owner-occupier with stable income: time in market beats timing the market. Investor leveraging up: TDSR-constrained — stress-test your affordability at a 4% rate.

Which segment looks strongest?

City-fringe RCR continues to be the sweet spot for owner-occupiers. OCR near MRT interchanges wins on yield.

This guide is for general information only and is accurate as of April 2026. Singapore property rules, taxes and cooling measures change frequently — always verify current figures with URA, IRAS, HDB or a licensed professional before committing. LovelyHomes is not a financial, legal or tax advisor.

Wait-Out Period: Private property owners must wait 15 months before buying HDB resale without grant.

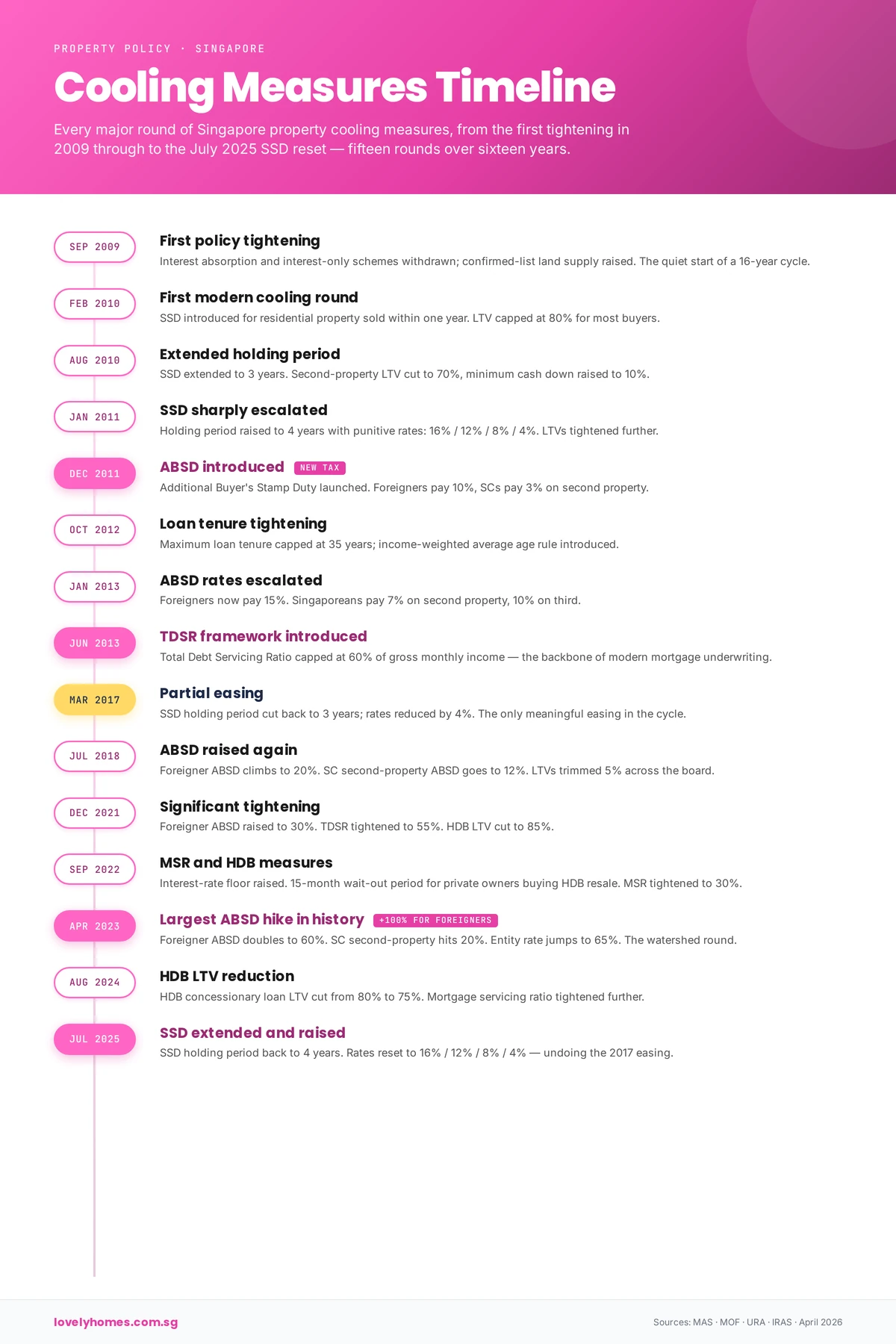

What are Singapore’s Property Cooling Measures?

Singapore’s property cooling measures are a suite of policy tools designed to moderate demand, curb speculation, and ensure housing remains affordable. They exist because rapid property price growth can outpace wage growth, lock first-time buyers out of the market, and create unsustainable bubbles. Four key agencies administer these measures: the Monetary Authority of Singapore (MAS), the Urban Redevelopment Authority (URA), the Inland Revenue Authority of Singapore (IRAS), and the Housing and Development Board (HDB). Together, they apply tools such as stamp duties, loan limits, affordability tests, and holding periods to regulate the market and protect both buyers and the broader economy.

Figure 1: The 15 major rounds of Singapore property cooling measures, 2009–2026.

September 2009: The First Policy Tightening

Before the modern cooling era, the government moved to restrict lending practices. In September 2009, the Monetary Authority of Singapore (MAS) disallowed two risky loan products: the Interest Absorption Scheme (IAS) and Interest-Only Housing Loans (IOL). These products had allowed borrowers to defer principal repayment during the early years of a mortgage, increasing default risk during rate rises. By banning them, the government signalled a preference for prudent, full-amortising loans and set the stage for the more comprehensive cooling measures that would follow.

February 2010: The First Modern Cooling Round

On 20 February 2010, Singapore introduced its first comprehensive cooling package, reflecting rapid price growth and surging demand. The government introduced two major tools:

Seller’s Stamp Duty (SSD): Properties sold within one year were hit with a 3% SSD. The intent was to discourage “flipping”—rapid resale for short-term gain.

Loan-to-Value (LTV) limit: Reduced from 90% to 80%, requiring buyers to put down at least 20%. This reduced lender exposure and made buyers more cautious.

These measures reflected a key insight: when buyers can leverage heavily and exit quickly, prices can spiral. By raising the entry cost and the holding cost, the government aimed to attract only genuine buyers.

August 2010: Extended Holding Period

By mid-2010, demand remained strong. On 19 August 2010, the government extended the SSD holding period from 1 year to 3 years, raising the cost of short-term resale. For those with existing loans, the LTV limit tightened further to 70%, and cash downpayment requirements rose, particularly hurting leveraged investors.

January 2011: Sharp SSD Escalation

Recognising that the market was still overheating, the government on 8 January 2011 escalated the SSD significantly. The new structure was:

Year 1: 16%

Year 2: 12%

Year 3: 8%

Year 4: 4%

The rationale was unmistakable: hold for less than a year and lose a sixth of your sale price. LTV limits were also tightened to 60% for those with existing loans, making it much harder for property investors to string together multiple mortgages.

December 2011: ABSD Introduced

On 8 December 2011, Singapore introduced the Additional Buyer’s Stamp Duty (ABSD), its most powerful tool. ABSD was a second layer of stamp duty on top of the normal Buyer’s Stamp Duty (BSD), calibrated to buyer type:

Singapore Citizens buying a 2nd+ property: 3%

Singapore Citizens buying a 3rd+ property: 3%

Permanent Residents buying a 2nd+ property: 3%

Foreigners: 10%

Corporate entities: 10%

ABSD was revolutionary because it directly attacked investment demand, particularly from overseas. It signalled that Singapore prioritised homeownership for citizens over investment returns for outsiders.

October 2012: Loan Tenure Tightening

The Monetary Authority of Singapore further tightened lending on 19 October 2012. The maximum loan tenure was capped at 35 years, with a penalty: if LTV remained above 60% after 30 years, the LTV would be capped at 40% in year 31 onwards. This forced borrowers to repay principal faster, reducing their borrowing power and making loans less attractive.

January 2013: ABSD Escalation

On 11 January 2013, the government raised ABSD across the board:

Singapore Citizens (2nd property): 7%

Singapore Citizens (3rd+ property): 10%

Permanent Residents (2nd+ property): 10%

Foreigners: 15%

Entities: 15%

The hike reflected continued demand, particularly from foreign investors and corporate buyers. Cash downpayment requirements also rose, targeting multiple-property owners and entities.

June 2013: TDSR Framework Introduced

On 28 June 2013, the Monetary Authority of Singapore introduced the Total Debt Servicing Ratio (TDSR) framework. TDSR capped total monthly debt repayments (mortgage, car loan, credit cards, personal loans, etc.) at 60% of gross monthly income. The intention was to prevent over-leverage: even if house prices were rising, a banker couldn’t lend to someone whose entire income was going to debt service.

This was a game-changer because it wasn’t about house prices directly—it was about borrower health. It also forced banks to stress-test loans, assuming interest rates would rise, to ensure borrowers could survive a shock.

March 2017: Partial Easing

By 2016–2017, prices had stabilised and growth had slowed. On 5 March 2017, the government eased some measures:

SSD holding period reduced from 4 years to 3 years, though rates remained steep (12%/8%/4% for years 1–3).

TDSR and ABSD eased slightly for refinancing.

This signalled a shift: the government was confident the market was no longer overheating and could afford marginal relief.

July 2018: ABSD Raised Again

By mid-2018, there were signs of renewed speculative interest, particularly from foreign and corporate buyers. On 6 July 2018, the government raised ABSD sharply:

LTV limits also tightened by 5 percentage points across all categories, making down payments larger and borrowing power lower.

December 2021: Significant Tightening

After years of near-zero interest rates post-COVID, demand surged again. On 16 December 2021, the government announced a comprehensive tightening:

ABSD raised again: foreigners to 30%; entities to 35%; PR 2nd property to 20%.

TDSR tightened from 60% to 55% of gross monthly income.

Interest-rate floor for TDSR/MSR calculations raised to 3.5% for private bank loans (previously 3%).

HDB LTV limits reduced across the board.

This was a significant hardening, reflecting real concern about affordability following three years of price growth.

September 2022: MSR and HDB Measures

On 30 September 2022, the government introduced new measures targeting the HDB resale market, where first-time buyers (and upgraders) primarily shop:

Mortgage Servicing Ratio (MSR) introduced: For HDB and Executive Condominium (EC) loans, monthly mortgage payments cannot exceed 30% of gross income—stricter than TDSR’s 55%.

15-month wait-out period: Private property owners must wait 15 months after selling before buying an HDB resale flat, curbing investor demand for subsidised public housing.

Interest-rate floor for TDSR/MSR raised from 3% to 3.5% for private loans; 3% for HDB loans.

These moves directly sheltered first-time HDB buyers from investor competition.

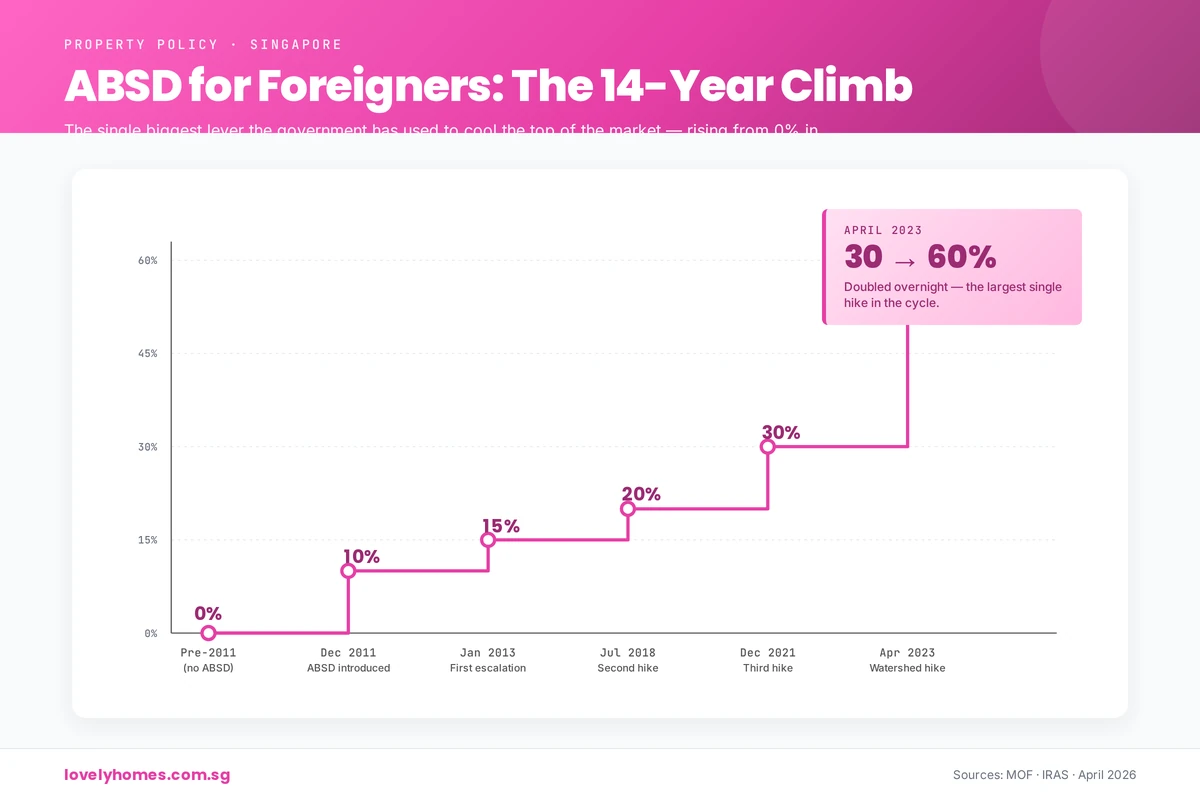

Figure 3: Foreigner ABSD climbed from 0% in 2011 to 60% in April 2023 — the largest single hike in the cycle.

April 2023: Largest ABSD Hike in History

On 27 April 2023, faced with renewed price acceleration in Q1 2023 (especially among owner-occupiers), the government announced its largest ABSD increase:

This was the most aggressive escalation since ABSD’s introduction, reflecting the government’s determination to prioritise homeownership for citizens and slow speculation. A foreign buyer purchasing a S$2 million condo now faced S$1.2 million in ABSD—an enormous barrier.

August 2024: HDB LTV Reduction

On 20 August 2024, the government reduced the Loan-to-Value (LTV) limit for HDB-granted housing loans from 80% to 75%. This meant HDB buyers now needed a 25% down payment instead of 20%, directly reducing borrowing power for this segment. Concurrently, higher CPF Housing Grants were introduced for first-time buyers to offset the impact, retaining affordability.

July 2025: SSD Extended and Raised

On 3 July 2025, the government responded to a spike in “flipping”—buyers purchasing uncompleted units (off-plan) and reselling before completion or soon after. The SSD holding period was extended from 3 years to 4 years, and rates were raised across the board by 4 percentage points:

Year 1: 20% (from 16%)

Year 2: 16% (from 12%)

Year 3: 12% (from 8%)

Year 4: 8% (from 4%)

This further discouraged short-term speculation while allowing long-term owners to exit penalty-free after four years.

Current Cooling Measures Framework (April 2026)

The current cooling-measures framework, established by the 27 April 2023 ABSD hike and subsequently adjusted by the 20 August 2024 HDB LTV reduction and the 4 July 2025 SSD restructure, remains in force as at April 2026. MAS, MND, URA and HDB jointly review the framework regularly and have repeatedly indicated they will recalibrate the measures — either tightening or easing — in response to market conditions.

Figure 2: The four core cooling tools — taxes (ABSD, SSD), loan limits (LTV) and debt ratios (TDSR) working in concert.

Let’s illustrate the impact with a hypothetical Singapore Citizen (SC) buying a second property valued at S$2 million:

Year

ABSD Rate

ABSD Cost (S$)

BSD + ABSD Total

2010 (Feb)

0%

S$0

~S$20,000 (BSD only)

2013 (Jan)

7%

S$140,000

~S$160,000

2018 (July)

7%

S$140,000

~S$160,000

2023 (April)

20%

S$400,000

~S$420,000

2026 (April)

20%

S$400,000

~S$420,000

Notice the leap from 2013 to 2023: the cost of buying a second home more than doubled in stamp duty alone, while the property value remained constant. This is the direct impact of cooling measures: they make property ownership more expensive, not by changing the property itself, but by raising friction and entry costs.

Why Have Cooling Measures Worked?

Singapore’s housing market has not crashed, despite aggressive cooling measures—a fact some cite as evidence of failure. But that misses the point. Cooling measures are designed to slow, not stop, price growth; to reduce speculation, not eliminate it; and to align prices with incomes, not freeze them.

Consider the evidence:

Slower growth: Private residential property annual price gains have typically stayed in the 2–5% range post-2013, compared to double-digit growth in the early 2010s. This moderation reflects a market rebalancing, where price appreciation has settled into a more sustainable trajectory aligned with economic fundamentals such as wage growth and rental yields.

Affordability preserved: First-time buyers, particularly HDB upgraders, have continued to buy; median house prices have not become so extreme relative to median incomes that the market has fractured. The price-to-income ratio in Singapore remains among the most manageable in developed Asia, allowing younger buyers to enter the market without undue hardship.

Comparison to global peers: Hong Kong, Vancouver, and Sydney have seen much steeper price-to-income ratios despite less stringent cooling measures. In Hong Kong, for example, a property may cost 20–30 times annual median household income; in Vancouver and Sydney, the ratio exceeds 12–15. Singapore’s pragmatic approach has kept the ratio at a more sustainable 8–10 times, making the market more accessible.

Investor activity moderated: The share of property transactions by investors (vs. owner-occupiers) has declined, indicating cooling measures are successfully crowding out speculative demand. This shift is crucial: when investors withdraw, price volatility typically decreases and stability improves.

Market resilience: The market has absorbed multiple rounds of tightening—seven major cooling packages since 2009—without experiencing a crash. This speaks to the underlying strength of Singapore’s economy and the government’s ability to calibrate policy precisely, neither so tight as to stifle the market nor so loose as to permit excess.

In short, cooling measures have succeeded in their core mission: managed, sustainable growth that preserves homeownership as an achievable goal for Singaporeans whilst safeguarding financial stability.

What Might Come Next?

Predicting future cooling measures is speculative, but several potential levers exist if the market overheats again. The government has shown it is willing to adjust policy swiftly when conditions warrant, and the following measures are within the realm of possibility:

Further LTV tightening: LTV could drop below 75% for HDB and 70% for private, forcing larger down payments. This would particularly affect HDB first-time buyers, though offsetting grants could mitigate the impact.

ABSD escalation on entities: Corporate and foreign entity purchases could face rates exceeding 70%, further discouraging institutional investors and offshore funds from treating Singapore residential property as an alternative asset class.

TDSR reduction: The 55% threshold could tighten to 50%, limiting borrowing power even further. This would reduce the quantum of debt banks could extend and force buyers to increase down payments or reduce property search prices.

Extended hold periods: SSD holding could extend beyond four years; MSR wait-out could lengthen beyond 15 months. A 5–7 year SSD period would effectively end short-to-medium-term flipping as an investment strategy.

Targeted HDB measures: Given HDB’s social mission, the government could ring-fence HDB buying further (e.g., longer wait-out periods for private owners, stricter owner-occupancy rules for upgrade purchases).

Differentiated ABSD by property type: Separate ABSD rates for landed (houses, land) vs. non-landed (condos, ECs) to focus cooling where prices are most extreme. Landed property prices have historically appreciated faster than condominiums, making them a natural target for stricter cooling.

Interest-rate floor adjustments: The MAS could raise the notional interest-rate floor used in TDSR/MSR calculations from the current 4% (private) to 4.5% or 5%, making loans seem more expensive during qualification, thereby reducing lending volumes.

These possibilities are illustrative, not predictions. The Government has consistently emphasised that cooling measures are reviewed against prevailing market conditions, and that any further recalibration — tightening or easing — will be driven by the data. Buyers and sellers should plan on the framework in force today and monitor MAS, URA, MND, IRAS and HDB announcements for updates.

Frequently Asked Questions

1. What’s the difference between ABSD and SSD?

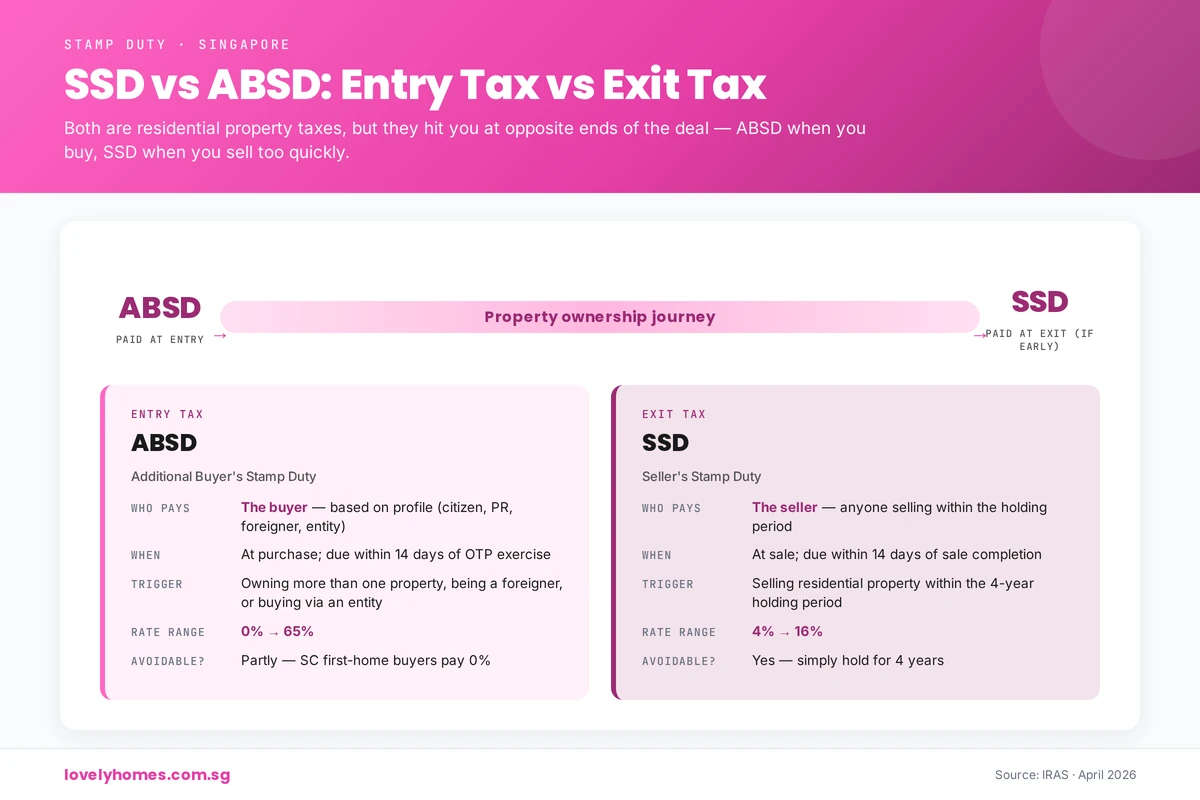

ABSD (Additional Buyer’s Stamp Duty) is a tax paid by the buyer when purchasing a property (typically 2nd or 3rd+). It’s calibrated by buyer type (citizen, PR, foreigner, entity) and aims to dampen investment demand. SSD (Seller’s Stamp Duty) is a tax paid by the seller when selling within a holding period; it discourages flipping. Both reduce demand, but ABSD targets entry; SSD targets exit.

2. Are cooling measures permanent?

No. All cooling measures are policy tools, not constitutional laws. They can be eased or tightened depending on market conditions. For example, SSD was partially eased in March 2017, and TDSR has been adjusted twice (60% → 55%). The Government reviews the framework regularly against market conditions.

3. Can you appeal a cooling-measure penalty (e.g., SSD)?

No. Cooling measures are statutory levies applied uniformly. Once a property is sold within the SSD holding period, the duty is automatically calculated and due. There is no appeal mechanism, though you can seek professional tax advice if you believe your classification is incorrect. Early repayment of SSD (before expiry) is not available.

4. How do cooling measures affect HDB owners?

Cooling measures affect HDB owners primarily when upgrading (selling to buy private) or downgrading (selling private to buy HDB resale). HDB owners upgrading to private face ABSD. Private owners downgrading to HDB resale face a 15-month wait-out period and stricter MSR limits (30% vs. TDSR 55%). Cooling measures have also reduced HDB LTV to 75%, requiring larger down payments.

5. Do foreigners face the toughest measures?

Yes, unambiguously. Foreigners pay 60% ABSD (vs. 20% for SC 2nd property), and are excluded from some HDB categories altogether. The government’s policy framework explicitly prioritises owner-occupation for citizens and PRs over foreign investment. A foreigner buying a S$2M property pays S$1.2M in ABSD alone, making foreign residential investment significantly less attractive.

6. Will the government remove cooling measures if the market drops?

Possibly, but history suggests a “last in, first out” approach. When prices fell during COVID-19, cooling measures were retained (some were even tightened). The government views cooling measures as structural policy, not cyclical. However, if prices fell sharply and sustained (e.g., 15% decline year-on-year), measures like ABSD could be eased to stimulate demand. The government’s current stance (April 2026) is that stabilisation is preferable to rollback, unless emergency conditions warrant it.

This guide is for general information only and does not constitute legal, tax, or financial advice. Cooling measures are subject to change at any time by the relevant authorities (MAS, URA, IRAS, HDB). Interest rates, property values, and policy frameworks are subject to modification. Before entering into any property transaction, verify the current ABSD rates, SSD holding periods, LTV limits, TDSR/MSR thresholds, and any other applicable cooling measures with the Inland Revenue Authority of Singapore (IRAS), the Housing and Development Board (HDB), or the Monetary Authority of Singapore (MAS). Consult a licensed conveyancing lawyer and a qualified mortgage specialist or financial adviser to assess your personal circumstances and borrowing capacity. LovelyHomes.com.sg takes no responsibility for losses or liabilities arising from reliance on this article.

Seller’s Stamp Duty (SSD) is a tax payable by the seller when disposing of certain residential and industrial properties in Singapore within a specified holding period. Unlike Additional Buyer’s Stamp Duty (ABSD), which the buyer pays, SSD is borne entirely by the property seller.

Introduced in February 2010, SSD was designed as a cooling measure to deter short-term property speculation and encourage longer-term property ownership. Over the past 16 years, the rates and holding periods have changed multiple times in response to market conditions and Government policy objectives.

For sellers, understanding SSD is critical: it can significantly erode capital gains or even create a loss when selling within the holding period. Many property investors overlook SSD in their calculations and are shocked by the tax bill at completion.

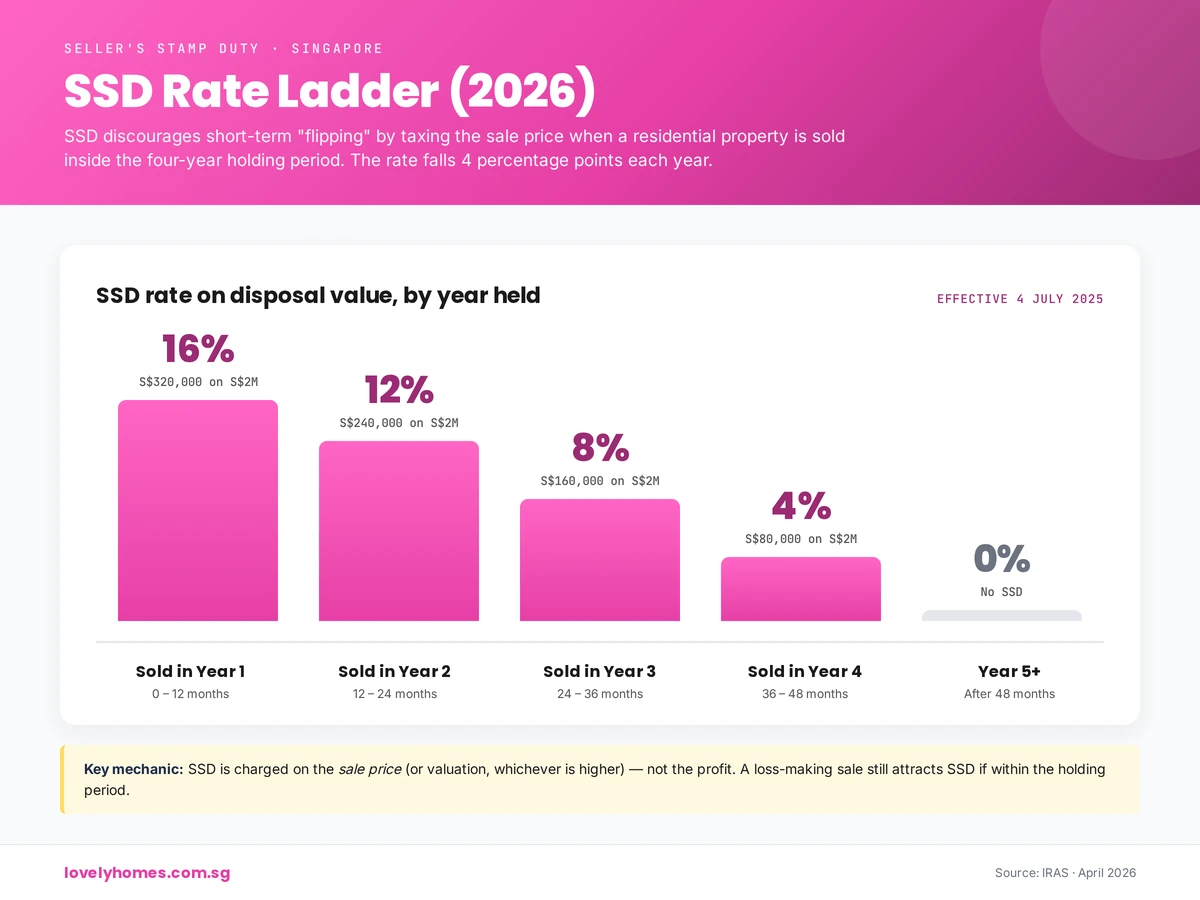

Figure 1: The current four-year SSD ladder — 16%/12%/8%/4% on disposal value (IRAS, 2026).

Current SSD Rates in 2026 (Critical Update)

Quick Answer: What Are Today’s SSD Rates?

Residential properties: Depends on purchase date.

Purchased 11 March 2017 to 3 July 2025: 12% (Year 1) / 8% (Year 2) / 4% (Year 3) / 0% thereafter

Purchased on or after 4 July 2025: 16% (Year 1) / 12% (Year 2) / 8% (Year 3) / 4% (Year 4) / 0% thereafter

Industrial properties: 15% (Year 1) / 10% (Year 2) / 5% (Year 3) / 0% thereafter (unchanged since January 2013)

Commercial properties: 0% (retail shops, offices, no SSD applies)

Important: On 4 July 2025, the Government announced a significant restructure of residential SSD, effective for all properties purchased on or after that date. The holding period extended from 3 years to 4 years, and rates increased by 4 percentage points across all tiers.

Year of Disposal

Residential (Old: purchased ≤ 3 July 2025)

Residential (New: purchased ≥ 4 July 2025)

Industrial

Year 1

12%

16%

15%

Year 2

8%

12%

10%

Year 3

4%

8%

5%

Year 4

N/A

4%

N/A

Year 5+

0%

0%

0%

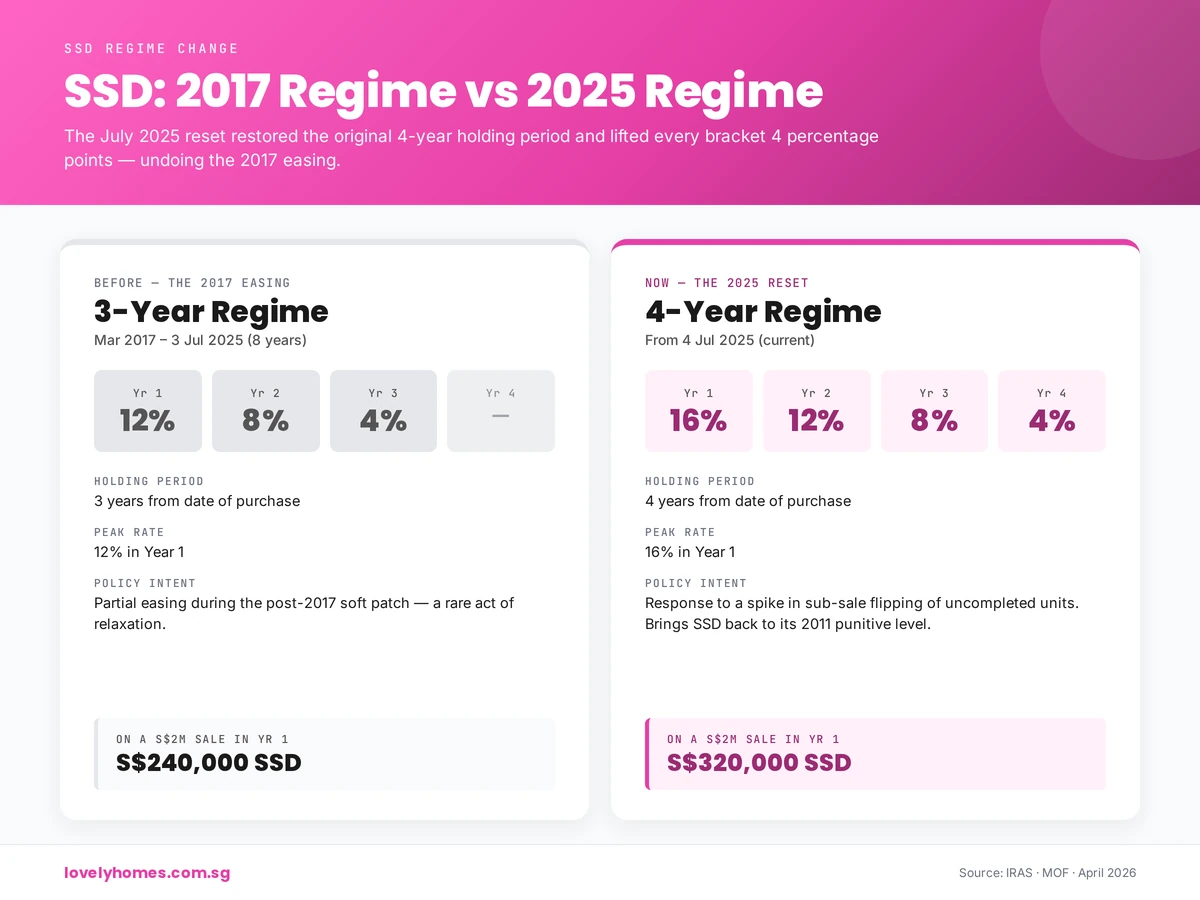

Figure 2: The July 2025 reset undid the 2017 easing — back to four years, up 4 percentage points per bracket.

A Brief History of SSD in Singapore

SSD rates have evolved significantly over the past 16 years, reflecting the Government’s shifting approach to cooling the property market:

February 2010: SSD introduced at 1% (Year 1) / 2% (Year 2) / 3% (Year 3) for sales within 1 year of purchase.

August 2010: SSD extended to cover sales within 3 years of purchase, maintaining the 1%/2%/3% rates.

January 2011: Rates escalated dramatically to 16% (Year 1) / 12% (Year 2) / 8% (Year 3) / 4% (Year 4) over 4 years, coinciding with the Global Financial Crisis aftermath and rising property prices.

January 2013: Industrial SSD introduced at 15%/10%/5% over 3 years, with no holding period extension thereafter.

11 March 2017: Residential SSD rates eased back to 12% (Year 1) / 8% (Year 2) / 4% (Year 3), and the holding period shortened from 4 years to 3 years. This marked a significant market cooling.

4 July 2025:Latest restructure: SSD rates for residential properties increased to 16% (Year 1) / 12% (Year 2) / 8% (Year 3) / 4% (Year 4), and the holding period extended back to 4 years. This applies to all properties purchased on or after 4 July 2025. Properties purchased before this date remain under the 12%/8%/4% regime (3-year holding period).

When Does SSD Apply? Key Conditions

SSD applies when all of the following conditions are met:

Property type: The property must be residential (private condo, terrace house, landed property) or industrial (factory, warehouse, B1/B2 zoned land). Commercial properties (retail shops, office units) are not subject to SSD.

Holding period: The property must be sold or disposed of within the holding period (3 years for pre-July 2025 purchases, 4 years for post-July 2025 purchases).

Disposal triggering event: The relevant date is when the Option to Purchase (OTP) is granted to the buyer or the Sale and Purchase Agreement (SPA) is signed, whichever is earlier. This date marks Day 1 of the holding period.

Acquisition date: The holding period starts from the date the OTP was exercised or the SPA was signed when you purchased the property (the date you acquired it).

SSD applies to most property disposals: sales to third parties, transfers to family members (unless specifically remitted), gifts, and even transfers in lieu of insolvency. The key trigger is the disposal date relative to the acquisition date.

HDB and SSD

Whilst SSD technically applies to HDB flats purchased after the legislative date (February 2010), in practice, SSD rarely applies to HDB owners because HDB imposes a Minimum Occupation Period (MOP). Most HDB flats have a 5-year MOP, meaning you cannot sell before 5 years have passed. By the time you can sell, the SSD holding period (3 or 4 years) has expired, and you owe no SSD.

However, if you own an HDB flat purchased before the SSD regime and sell early (during a defined period when some flats had shorter MOPs), SSD could theoretically apply. Consult your legal conveyancer for your specific flat’s MOP rules.

Executive Condominiums (ECs) and SSD

Executive Condominiums are subject to SSD if disposed of within the holding period after the MOP expires (typically 5 years). Once the MOP is completed and the property is decoupled from HDB rules, it is treated as a private residential property for SSD purposes.

Worked Examples: How SSD Is Calculated

Example 1: Private Condo Purchased January 2025, Sold June 2026

Scenario: You purchased a private condo on 15 January 2025 for S$1,800,000. You sold it on 20 June 2026 for S$2,000,000. At the time of sale, the property’s market value was assessed at S$1,950,000.

Analysis:

Purchase date: 15 January 2025 (before 4 July 2025 → old regime applies)

Sale date: 20 June 2026

Holding period: Approximately 17 months = Year 2

SSD rate: 8% (Year 2 rate under old regime)

Disposal value for SSD: Higher of sale price (S$2,000,000) or market value (S$1,950,000) = S$2,000,000

SSD payable: 8% × S$2,000,000 = S$160,000

Outcome: Despite a S$200,000 paper gain, you owe S$160,000 in SSD. Your actual net gain after SSD (and ignoring agent fees, legal costs, and ABSD if applicable to the buyer) would be only S$40,000—or entirely erased if other transaction costs are factored in.

Example 2: Private Condo Purchased March 2023, Sold April 2026

Scenario: You purchased a private condo on 10 March 2023 for S$1,600,000. You sold it on 5 April 2026 for S$1,750,000.

Analysis:

Purchase date: 10 March 2023 (before 4 July 2025 → old regime applies)

Sale date: 5 April 2026

Holding period: Approximately 3 years 3 months = beyond Year 3

SSD rate: 0% (holding period exceeded 3 years)

SSD payable: S$0

Outcome: You have held the property beyond the 3-year holding period, so no SSD is due. Your entire S$150,000 gain (less transaction costs and ABSD if applicable) is yours to keep.

Example 3: Industrial Property Purchased January 2025, Sold March 2026

Scenario: You purchased an industrial property (warehouse) on 20 January 2025 for S$2,000,000. You sold it on 15 March 2026 for S$2,100,000.

Analysis:

Property type: Industrial

Purchase date: 20 January 2025

Sale date: 15 March 2026

Holding period: Approximately 14 months = Year 2

SSD rate: 10% (Year 2 rate for industrial properties)

Disposal value for SSD: Higher of sale price or market value = S$2,100,000

SSD payable: 10% × S$2,100,000 = S$210,000

Outcome: Your S$100,000 paper gain is entirely wiped out by the S$210,000 SSD bill. You would need to pay S$110,000 from your own pocket to complete the sale. This illustrates why industrial property flippers face substantial tax penalties.

Example 4: New Regime – Residential Purchased July 2025, Sold November 2026

Scenario: You purchased a private condo on 10 July 2025 for S$1,500,000. You sold it on 15 November 2026 for S$1,650,000.

Analysis:

Purchase date: 10 July 2025 (on or after 4 July 2025 → new regime applies)

Sale date: 15 November 2026

Holding period: Approximately 16 months = Year 2

SSD rate: 12% (Year 2 rate under new regime)

Disposal value for SSD: S$1,650,000

SSD payable: 12% × S$1,650,000 = S$198,000

Outcome: Under the new, stricter regime, even a modest 10% appreciation is swallowed by a 12% SSD rate. The sale results in a net loss of approximately S$48,000 (before other transaction costs).

How SSD Is Calculated: Disposal Value

A critical point: SSD is calculated on the higher of the selling price or the market value of the property as at the date of sale.

If you sell below market value (e.g., to a family member at a discount, or in a distressed sale), the property’s assessed market value may still be used by IRAS to compute SSD. You cannot reduce your SSD bill by negotiating a lower sale price.

Market value is typically determined by a professional valuation, comparable sales data, or IRAS’s own assessment. If you believe IRAS’s valuation is incorrect, you can request a review, but the onus is on you to provide supporting evidence.

How to Legally Avoid or Minimise SSD

SSD is a significant liability for property sellers. Fortunately, several legitimate strategies exist:

1. Hold for the Full Period (3 or 4 Years)

The most straightforward approach: Hold your residential property for at least 3 years (if purchased before 4 July 2025) or 4 years (if purchased after) before selling. Once the holding period expires, SSD drops to 0%, and you keep your entire gain.

For industrial properties, hold for 3 years to eliminate SSD.

This strategy is ideal if you can afford to hold the property long-term. Many professional investors plan around these holding periods when structuring their portfolios.

2. Timing the OTP Carefully (Within Limits)

The key holding-period dates are:

Start date: The date you exercised the OTP or signed the SPA when you purchased the property.

End date: The date you granted the OTP to the buyer or signed the SPA when you sold the property.

If you purchased on 10 January 2025, the 3-year threshold is reached on 10 January 2028. If you can delay granting your buyer’s OTP until 10 January 2028 or later, SSD drops to 0%.

However, there are strict limits: You cannot artificially delay the OTP grant date if you have already agreed to sell. Doing so could constitute a breach of contract or fraud. The dates must reflect genuine transaction timings.

3. Properties Exempt or Remitted from SSD

Certain disposals qualify for full SSD remission or exemption:

Compulsory Acquisition (CA) by the Government: If your property is acquired under the Land Acquisition Act (e.g., for public housing, roads, or infrastructure), SSD is fully remitted.

Developer Repurchase: If a property developer repurchases a unit within a stipulated period (e.g., within 5 years of the original sale for some EC schemes), SSD may be remitted under the scheme’s terms.

Matrimonial Property Transfer: Transfers of residential property between spouses or ex-spouses as part of matrimonial or ancillary relief proceedings may qualify for remission if executed pursuant to a Court Order. However, this is a narrow exemption—consult a legal advisor.

HDB Repurchase by HDB: If HDB repurchases a flat from you (e.g., under right of first refusal schemes), SSD is typically remitted.

Bankruptcy or Insolvency: In certain insolvency situations, SSD may be remitted if the property is disposed of by a trustee or official receiver under court order.

These exemptions are narrow and require specific conditions. If you believe you qualify, consult a licensed conveyancing lawyer or contact IRAS directly for a ruling.

4. Decoupling Strategy (With Caution)

If you are married and own property as joint tenants, decoupling (transferring one spouse’s share to the other spouse) creates a new acquisition date for the transferred share. This means the holding period for that share restarts.

Example: You and your spouse bought a property jointly on 1 January 2025. On 1 July 2026, you transfer your spouse’s share to yourself. Your spouse’s share now has a new acquisition date (1 July 2026), so its holding period restarts. If you then sell the entire property on 1 January 2027, your share is subject to Year 2 SSD, but your spouse’s share (which was only held from July 2026 to January 2027 = 6 months = Year 1) would trigger Year 1 SSD on that portion.

This strategy is complex, has significant stamp duty and ABSD implications, and may not be worthwhile. Do not attempt without guidance from a tax professional and conveyancer.

5. Beware: Legitimate Avoidance vs. Tax Evasion

There is a clear legal line between legitimate tax planning and tax evasion:

Legitimate: Holding the property longer, timing transactions around the 3-year mark, claiming available exemptions.

Illegal: Falsifying transaction dates, under-declaring the sale price, splitting the sale into multiple transactions to circumvent SSD, or using straw buyers.

IRAS actively audits property transactions and has recovered substantial SSD arrears from taxpayers who attempted to evade the tax. The penalties (including interest and potential prosecution) far exceed any tax saved.

Figure 3: ABSD is charged when you buy; SSD is charged only if you sell within the holding period.

SSD vs. ABSD: What’s the Difference?

Many property sellers confuse SSD (Seller’s Stamp Duty) with ABSD (Additional Buyer’s Stamp Duty). They are separate taxes and can both apply to a single transaction:

Aspect

SSD (Seller’s Stamp Duty)

ABSD (Additional Buyer’s Stamp Duty)

Payable By

Seller

Buyer

When

At sale, if property sold within holding period (3 or 4 years)

At purchase, if buyer is foreigner, company, trust, or owns other properties

Applies To

Residential & industrial properties only

Residential properties only (no ABSD on industrial)

Purpose

Deter short-term speculation by sellers

Deter foreign ownership & multiple property purchases by buyers

Example Rate

12% (Year 1, old regime) or 16% (Year 1, new regime)

Key Point: Both SSD and ABSD can apply to a single transaction. If a Singaporean citizen (owner) sells a residential property within 3 years to a foreign buyer (or to another Singaporean who already owns 1+ properties), the seller pays SSD and the buyer pays ABSD. Each is computed on the transaction price and borne by the respective party.

Frequently Asked Questions (FAQ)

Q1: Who decides what the “disposal value” is for SSD calculation?

A: The disposal value is the higher of the actual selling price or the property’s market value as at the date of sale. If you sell at S$2M but IRAS assesses the market value at S$2.2M, SSD is computed on S$2.2M. You can appeal IRAS’s valuation, but the burden is on you to prove the value with evidence (comparables, professional appraisals). In most cases, the selling price is the disposal value, unless it is significantly below market (a rare event).

Q2: Can I use my CPF to pay SSD?

A: No. SSD is a seller’s cost and must be paid from the sale proceeds or your own funds. CPF can only be used to purchase residential property and to pay the conveyance duty (stamp duty) on the purchase itself, not on the sale or SSD. SSD is withheld from your sale proceeds at completion.

Q3: Does SSD apply if I gift my property to a family member?

A: Yes, in principle, SSD applies to gifts unless a specific remission is granted. The “disposal value” for a gift is the property’s market value (since there is no actual sale price), and SSD is computed on that value. However, if the gift is part of a matrimonial order or compulsory acquisition, remission may apply. For most family gifts without legal exemption, SSD is payable by the donor (gift-giver). Consult a lawyer before gifting property if within the holding period.

Q4: Does SSD apply if I inherited the property?

A: No, SSD does not apply to inherited properties. Inheritance is not a “disposal” triggering SSD; it is a transmission of title by operation of law upon death. Your holding period for SSD purposes starts from the date the original buyer (the deceased) purchased the property. If the deceased held it for more than 3 years before dying, there is no SSD when you (the heir) subsequently sell. If the deceased had held it less than 3 years and you sell shortly after, you may owe SSD, but the holding period is measured from the original purchase date, not your inheritance date.

Q5: Does SSD apply to HDB flats?

A: Technically, yes—SSD applies to HDB flats purchased after February 2010. However, in practice, SSD rarely triggers for HDB owners because HDB imposes a Minimum Occupation Period (typically 5 years). Once you can sell (after MOP), the SSD holding period has usually expired. If you own an older HDB flat or one with a shorter MOP and sell within the holding period, SSD would apply. Check your flat’s MOP with HDB before selling early.

Q6: Can I get SSD back if the buyer backs out?

A: SSD is paid at completion of the sale (when the sale is finalised and transferred to the buyer). If the buyer backs out before completion, the sale does not complete, and SSD is not triggered or payable. If the sale completes and you have paid SSD, but the buyer later defaults or the sale is reversed (rare), you would need to seek legal remedy or negotiate a refund directly with the buyer. IRAS does not refund SSD unless the underlying transaction is formally set aside by Court order.

Q7: How is SSD calculated on an incomplete property (Build-to-Completion, BUC)?

A: For a property sold before completion of construction (i.e., before the Completion Certificate is issued), SSD is calculated on the contract price (as stated in the SPA or OTP), not the actual completion value. The holding period is measured from the date the OTP was exercised on the original purchase. If you resale a BUC unit within the holding period, SSD is due on the resale price. This is an area where many investors get caught—ensure you understand the SSD implications before flipping an off-plan property.

Q8: What happens if I sell a property that is jointly owned with my spouse?

A: If you and your spouse own a property as joint tenants or tenants-in-common, the sale price is shared (usually 50/50 unless another ratio is agreed). SSD is calculated on the full sale price, but it is paid from the joint sale proceeds. The holding period is the same for both owners (it starts from the date the property was first acquired). No special relief applies merely because of joint ownership; both spouses are treated as single sellers of a single property. If you decouple (transfer one spouse’s share to the other), the transferred share gets a new acquisition date, which can complicate SSD calculations.

Q9: Can I defer or spread SSD payments over time?

A: No, SSD must be paid in full at the point of completion (when the sale is finalised). There is no option to spread the payment or defer it. Your conveyancer will calculate the SSD owed and ensure it is deducted from the sale proceeds before you receive your net amount. If you cannot afford the SSD, the sale cannot complete, and you remain the owner.

Q10: Are there any SSD changes coming in 2026/2027?

A: As of April 2026, no further changes to SSD have been announced. The most recent restructure took effect on 4 July 2025 (16%/12%/8%/4% over 4 years for properties purchased on or after that date). Keep monitoring IRAS’s official website and Government budget announcements for any future changes. However, do not assume changes; rely only on official announcements from IRAS and the Ministry of Finance (MOF).

This guide is provided for general informational purposes only and does not constitute legal, tax, financial, or investment advice. SSD rates, holding periods, and exemptions are subject to change at the discretion of the Government of Singapore and the Inland Revenue Authority of Singapore (IRAS).

Consult a licensed conveyancing lawyer to understand your specific SSD liability based on your property’s purchase and sale dates.

Obtain a professional valuation if you believe the market value of your property may differ significantly from the sale price.

Contact IRAS directly for clarification on any specific scenarios or exemptions that may apply to your situation.

Property laws change, and individual circumstances vary widely. LovelyHomes.com.sg and its authors assume no liability for actions taken based on this guide. Always seek independent professional advice before committing to a property transaction.