Home loan refinancing in Singapore means replacing your existing mortgage with a new one — usually at a lower rate, sometimes with a new bank, occasionally with the same bank under a new package. In a market where SORA has been swinging between 2.8% and 3.6% for the past 24 months, refinancing at the right moment can save a typical buyer S$3,000–S$6,000 per year.

Mistime it, and the legal costs, valuation fees and lock-in penalties wipe out the saving. This 2026 guide walks through when refinancing actually pays, how to do the break-even maths, and the traps that catch most Singapore homeowners.

Quick Answer — Refinancing at a Glance

- Typical saving: 0.4–0.8% lower rate vs your legacy package, worth S$200–S$400 a month on a S$800k loan.

- Typical cost: ~S$3,000 in legal and valuation fees (often fully subsidised by the new bank on loans above S$500k).

- Break-even: 12–18 months on a typical S$800k loan.

- Lock-in penalty: Usually 1.5% of outstanding if you refinance during the original package’s lock-in.

- Best windows: 3 months before your existing package’s lock-in ends; when SORA 3M has moved by ≥0.5% in your favour.

What Refinancing Actually Is

When you refinance, your new bank pays off the old bank in full and a fresh loan is registered against your property. Your CPF usage, property title and outstanding principal transfer across. What changes is the interest rate structure, the lock-in period, and — if you switch bank — the lender.

Three flavours exist:

- Re-pricing (same bank, new package). No conveyancing required, no legal fees, but banks typically offer worse rates than they do to outsiders.

- Refinancing (new bank). Full switch with legal and valuation costs (~S$3,000), but meaningfully better rates.

- Refinancing from HDB loan to bank loan. A one-way door — you cannot switch back to an HDB concessionary loan afterwards.

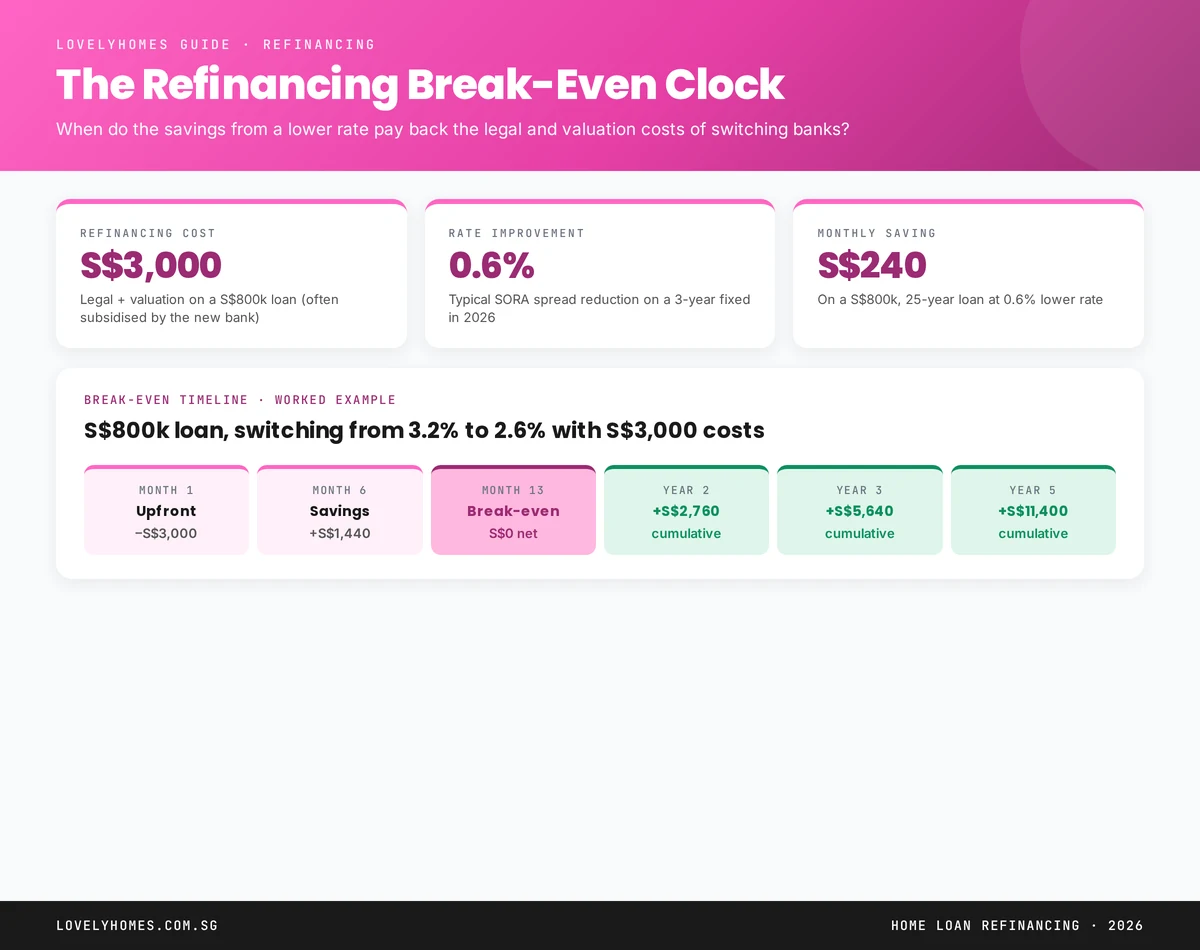

Break-Even: The Only Calculation That Matters

Break-even is simply: how many months of lower interest does it take to repay the switching costs?

Break-even months = Switching costs ÷ Monthly interest saving

On a S$800,000 loan, dropping from 3.2% to 2.6% saves roughly S$4,800 of interest in year one (S$400/month). If the full legal + valuation cost is S$3,000 and the new bank subsidises S$2,000, net cost is S$1,000 — break-even at ~3 months. Even with zero subsidy and S$3,000 full cost, break-even is around month 13.

The Lock-In Trap

Every home loan package has a lock-in period — typically 2–3 years for fixed-rate packages, 1–2 years for floating. Refinancing during lock-in triggers a penalty of 1.5% of the outstanding principal. On a S$800k loan, that is S$12,000.

In almost every case, this penalty kills the business case for refinancing. The exception: if SORA has dropped so dramatically that even paying S$12,000 today is recouped within 2 years of lower rates. Rare, but it happens during rate-cut cycles.

The three-month rule

MAS banks require 3 months’ notice to refinance or to exit to a new lender. If your lock-in ends on 1 October, start engaging new banks by 1 July. Waiting until August leaves you paying the legacy rate for the full notice period.

When Refinancing Makes Sense in 2026

Three concrete triggers should make you look at your package:

- Your lock-in ends within 4 months. 90% of refinancing wins come from the reset window around the end of a 2-year or 3-year fixed package. Banks actively target this window with cashback subsidies.

- SORA 3M has moved ≥0.5% in your favour since you last locked. Tiny moves rarely pay for switching costs; 0.5%+ moves almost always do.

- Your bank’s published rack rate is ≥0.3% above a new competitor. If your legacy package has lapsed into an expensive floating-rate default, you are overpaying regardless of macro conditions.

Fixed vs Floating at Refinance Time

The decision framework at refinance is the same as at origination: certainty vs upside. See our dedicated Fixed vs Floating Home Loan Singapore 2026 guide for a full breakdown. The only nuance at refinance time: your new package will reset your lock-in clock, so a 3-year fixed refinance locks you in for a further 3 years regardless of what happens to rates.

The Refinancing Checklist

Once you have decided refinancing makes sense, execution is largely administrative:

- Request a fresh In-Principle Approval (IPA) from 2–3 competing banks. This is free and commits you to nothing.

- Compare: headline rate, lock-in period, subsidy on legal & valuation, any cashback, prepayment rules.

- Pick the package and accept the Letter of Offer. Instruct a conveyancing lawyer (the new bank typically has a panel).

- Serve 3 months’ notice to your existing bank (email or physical letter).

- Discharge of mortgage and registration of new mortgage happens on the redemption date, usually 8–10 weeks later.

- Direct Debit for the old GIRO is cancelled and replaced with the new one.

The process runs itself once you sign. Your only vigilance point: verify the new monthly instalment has kicked in and the old GIRO is stopped, to avoid paying both banks briefly.

Common Mistakes

- Focusing only on headline rate. A 2.35% loan with a 3-year lock-in and no subsidy is often worse than a 2.55% loan with 2-year lock-in and S$2,000 subsidy.

- Refinancing too early. Switching costs are real. Sub-0.3% rate improvements rarely justify the effort.

- Forgetting CPF accrued interest. Refinancing does not pause CPF accrued interest — if you want to reduce it, a voluntary housing refund is the separate tool.

- Ignoring partial prepayment options. Some packages let you prepay up to 25% of outstanding without penalty. If you have a windfall, a prepayment often beats a refinance.

Frequently Asked Questions

Does refinancing affect my credit score?

Minimally. A single credit inquiry when the new bank pulls your file is normal. Multiple simultaneous applications within a short window are usually scored as a single inquiry by the Credit Bureau.

Will I need to top up cash if the property has declined in value?

Possibly. New banks will value the property afresh; if the new LTV exceeds their internal limit, they may ask for a cash top-up to bring LTV back in line. This is the biggest technical obstacle to mid-cycle refinances.

Can I refinance with my existing bank?

Yes — this is “re-pricing”. No legal fees, but typically inferior rates. Always get two outside quotes first and then negotiate.

How does refinancing interact with TDSR?

For owner-occupied properties, TDSR is not applied to refinances. For investment properties, TDSR applies with a debt-reduction plan if you are above 55%.

Is the subsidy really “free”?

It is, in the sense that the bank absorbs the legal and valuation fees — but most subsidies come with a clawback clause: redeem the loan within 3 years and you repay the subsidy. Always read the clawback condition.

What to Do Next

- Fixed vs Floating Home Loan 2026 — the refinance decision simplified.

- HDB Loan vs Bank Loan — especially if you are considering leaving HDB financing.

- All Home Loans & Mortgages guides.

Disclaimer: This guide is for general information and not financial advice. Package rates and lock-in rules change frequently. Always verify current offers directly with banks or through a licensed mortgage broker.

0 Comments