The condo downpayment question — how much cash does a Singapore buyer actually need on day 1 — sounds simple, but it is where most first-time buyers underestimate by S$50,000 or more. The answer depends on three overlapping rules (LTV, minimum cash, and stamp duties), and it changes dramatically if this is your second or third property.

This 2026 guide walks through exactly what you need to write cheques for on the day you collect your condo keys, with worked tables for first-property Singaporean citizens, second-property buyers, and foreign buyers. For the regulator’s guidance, see MAS Notice 632 on residential LTV.

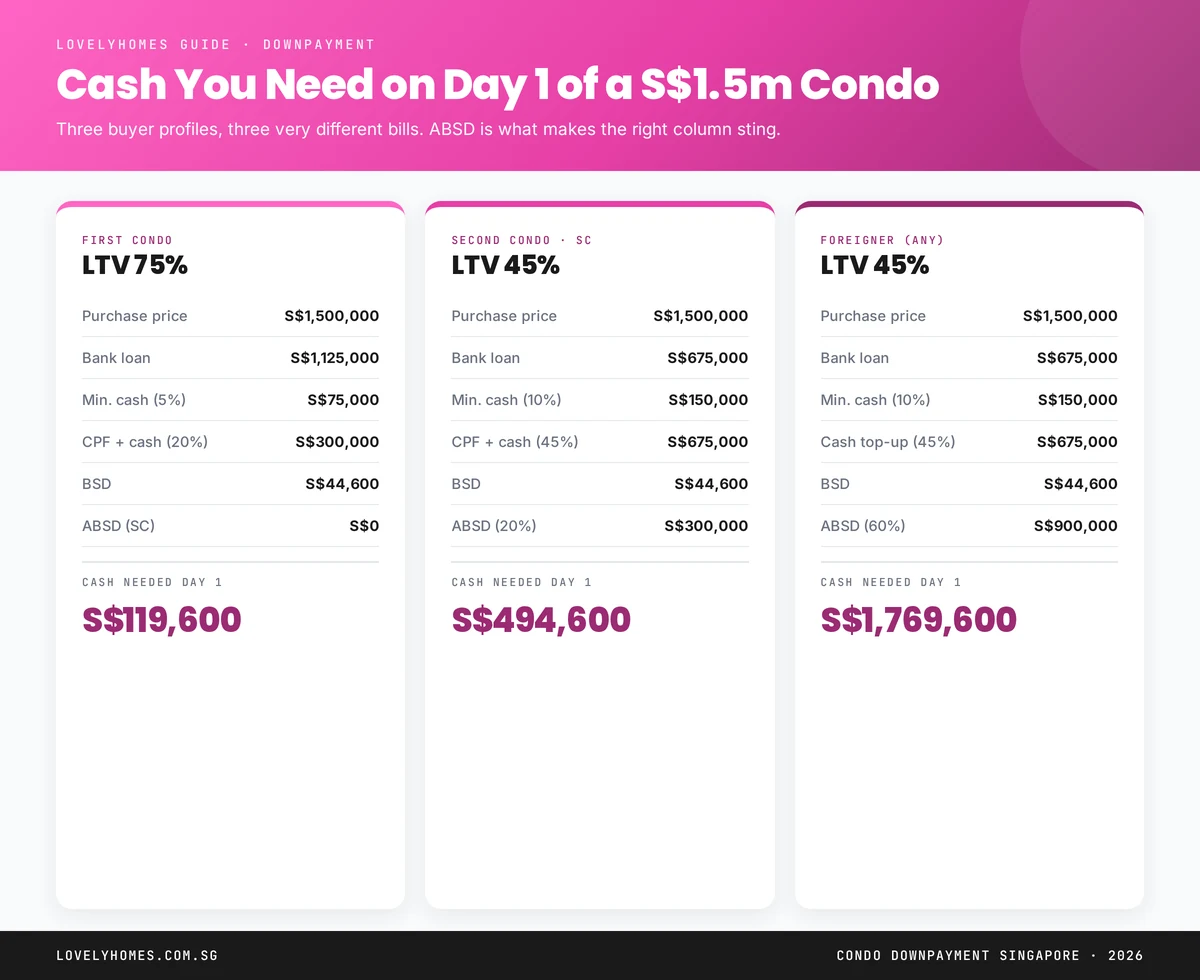

Quick Answer — Condo Downpayment on a S$1.5m Unit

- First condo, Singapore Citizen: ~S$119,600 cash + S$225,000 CPF/cash = S$344,600 total day-1 outlay (including BSD).

- Second condo, Singapore Citizen: ABSD alone adds S$300,000. Total day-1 outlay S$1,169,600.

- Foreigner buyer, any property: 60% ABSD on top of a 45% LTV. Total day-1 outlay S$1,769,600.

- Minimum cash: 5% of purchase price for 75% LTV; 10% for 45% or 35% LTV.

- BSD & ABSD: payable in cash within 14 days of OTP (reimbursable from CPF OA after).

The Three Rules That Set Your Downpayment

Three layers combine to set the cash and CPF you need:

- Loan-to-Value (LTV) ratio. MAS caps bank lending at 75% for a first housing loan, 45% for a second, and 35% for a third and beyond. The balance is your downpayment.

- Minimum cash portion. MAS requires at least 5% of the purchase price in cash for a first property, 10% for second and subsequent.

- Stamp duties. BSD and, where applicable, ABSD are paid in cash within 14 days of OTP. You can reimburse from CPF afterwards.

First Property: Singapore Citizen on a 75% LTV

The easiest case. On a S$1.5m condo, an SC buying their first home gets:

- Bank loan: up to S$1,125,000 (75% LTV, subject to TDSR).

- Downpayment: S$375,000 split as:

- Minimum 5% cash: S$75,000 — this is a hard floor, not a guideline.

- Remaining 20%: up to S$300,000 can come from CPF OA, cash, or a combination.

- BSD: ~S$44,600 (progressive on S$1.5m, capped at 5% at this level).

- ABSD: 0% (first residential property for a Singapore Citizen).

Total cash needed on day 1: S$75,000 (min. cash) + S$44,600 (BSD) = S$119,600. BSD can be reimbursed from CPF OA after stamping.

Second Property: Singapore Citizen on a 45% LTV

Two major shifts bite here. First, LTV drops to 45% — meaning you fund 55% of the purchase. Second, ABSD kicks in at 20%.

- Bank loan: S$675,000 maximum.

- Downpayment: S$825,000 split as:

- Minimum 10% cash: S$150,000.

- Remaining 45%: S$675,000 from CPF OA, cash, or combination.

- BSD: S$44,600.

- ABSD (20% SC 2nd): S$300,000.

Total cash needed day 1: S$150,000 + S$44,600 + S$300,000 = S$494,600. That is before the S$675,000 of CPF/cash needed to reach the loan ceiling.

This is why many Singaporean upgraders follow the sell-first-buy-second route — or take a bridging loan — to avoid holding two properties simultaneously.

Foreigner: 45% LTV + 60% ABSD

The most expensive profile. Foreign non-residents face LTV 45% (most banks drop to 40% for non-residents without local income), plus a flat 60% ABSD.

- Bank loan: S$675,000 maximum.

- Downpayment: S$825,000 in cash (no CPF access for foreigners).

- BSD: S$44,600.

- ABSD (60%): S$900,000.

Total cash needed day 1: S$1,769,600 against a S$1.5m purchase price. Many foreign buyers end up paying 100%+ cash when accounting for legal fees and renovation.

What About CPF OA?

CPF Ordinary Account can cover most of the non-minimum-cash portion of the downpayment, plus BSD/ABSD reimbursement after stamping. Critical caveats:

- CPF cannot cover the mandatory minimum cash portion (5% first, 10% subsequent).

- For private property, CPF usage caps at the Valuation Limit (purchase price or valuation, whichever lower) and the Withdrawal Limit of 120% of VL.

- Every dollar used compounds at 2.5% accrued interest — see our CPF for Property guide for the full maths.

New Launch vs Resale: Different Cash-Flow Timing

For a new launch (BUC — Building Under Construction), payments are staggered via the Progressive Payment Scheme. You typically need 25% at the Sale & Purchase Agreement (5% OTP deposit + 20% at S&PA), then 10% at foundation, 10% at reinforced concrete, etc. This reduces upfront cash strain dramatically.

For a resale, the entire downpayment hits at completion — typically 10–14 weeks after OTP. You need the full amount in cash and CPF by completion day.

TDSR Still Applies

The LTV numbers above are ceilings, not entitlements. Your actual bank loan may be smaller if your TDSR maxes out first — see our TDSR & MSR guide. A couple earning S$16,000 a month may qualify for a S$1.1m loan under TDSR even if LTV would allow S$1.125m on a S$1.5m purchase. In that case, the extra S$25,000 shortfall is yours to fund in cash or CPF.

Frequently Asked Questions

Can I put down more than 5%/10% in cash?

Yes. The minimums are floors, not ceilings. Some buyers put 20%+ cash to reduce their loan quantum and future interest.

Does option fee count as part of the downpayment?

Yes. The 1% Option Money and the 4% Option Exercise Fee together form the initial 5%, which is also the minimum cash portion for a first property.

Can I borrow more than 75% LTV?

Not from a MAS-regulated bank. Some private financing vehicles lend above 75% but at materially higher rates and with punitive terms — we do not recommend this route.

Does the 75% LTV apply to under-construction properties?

Yes, but payment is progressive — you do not need the full downpayment on day 1 for a new launch.

What if I am using an HDB loan for an HDB flat, not a bank loan for a condo?

HDB concessionary loans offer up to 75% LTV with 0% minimum cash. See our HDB Loan vs Bank Loan guide for the full difference.

What to Do Next

- ABSD Singapore 2026 Complete Guide — the biggest line in any upgrader’s cash-flow.

- BSD Singapore 2026 — full progressive rate ladder.

- TDSR & MSR 2026 — what your loan can actually be.

Disclaimer: This guide is general information, not financial advice. LTV and stamp-duty rules are subject to change. Verify current rules at mas.gov.sg and iras.gov.sg, and consult a licensed mortgage broker.

0 Comments