A bridging loan in Singapore is a short-term loan — typically 3 to 6 months — that covers the gap between buying your next home and receiving the sale proceeds from your current one. For upgraders who want to move into the new place before the buyer of the old one pays up, the bridge is often the single tool that makes the whole sequence possible without triggering a 20%+ ABSD bill.

This 2026 guide walks through how a bridging loan works, when it beats paying ABSD upfront, what it actually costs, and the scenarios where a bridge genuinely rescues an upgrade vs the ones where it quietly lights cash on fire.

Quick Answer — Bridging Loan at a Glance

- Tenure: typically 3–6 months, interest-only.

- Rate: typically 5%–6% p.a. (materially higher than a normal mortgage).

- Amount: bridges the downpayment of the new property, backed by expected sale proceeds of the current one.

- Purpose: lets you avoid holding two properties simultaneously (which triggers ABSD).

- Cost: S$5k–S$10k for a typical 3-month bridge — usually far less than the ABSD it avoids.

Why Bridging Loans Exist: The Upgrader’s Timing Problem

Singapore’s ABSD regime penalises buyers who hold two residential properties at the same time. A Singapore Citizen upgrading from an HDB flat to a condo pays 20% ABSD on the new property if they complete the purchase before the old HDB is sold. On a S$1.5m condo, that is S$300,000 in ABSD — potentially claimable back six months later under the married couple remission, but only if the old property sells on time.

The cleanest way to avoid that 20% outlay is the sell-first, buy-second route. But this creates a different problem: where do you live while waiting to complete your new home? Renting is expensive and disruptive, and the mechanics of moving a family twice in a year are brutal.

Bridging loans solve the cash-flow mismatch so you can effectively buy-first-sell-second without ever holding both properties at completion.

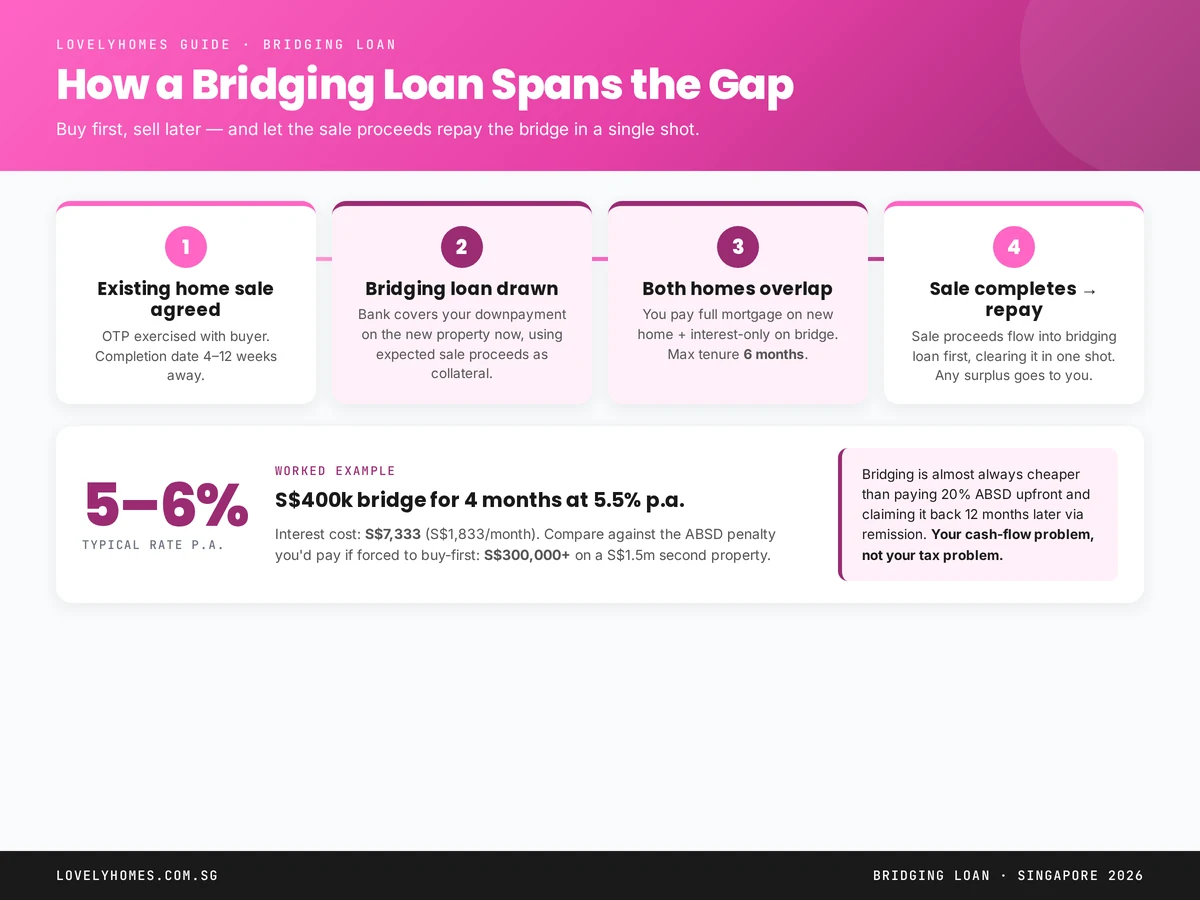

How a Bridging Loan Works, Step by Step

- You sell your existing home. OTP exercised, buyer’s 5% deposit received, completion date agreed (typically 10–14 weeks out).

- You buy your new home. OTP exercised on new property, downpayment due before your old sale completes.

- The bridging loan is drawn. Your bank issues a loan of up to 80% of the expected sale proceeds to fund the new downpayment. Interest accrues monthly at ~5–6% p.a. (interest-only, no principal repayment).

- Sale of old home completes. Proceeds flow straight into the bridging loan, clearing principal and accrued interest in one tranche. Any surplus is yours.

- Normal mortgage on new home continues. The bridge is gone; you carry only the new home’s regular mortgage.

Costs and Rates

Singapore bridging loans typically charge 5%–6% per annum, payable monthly on the outstanding balance. Banks rarely charge formal setup fees, but valuation and legal costs can total S$1,500–S$2,500.

Worked example: S$400k bridge for 4 months

- Bridge amount: S$400,000

- Rate: 5.5% p.a.

- Interest per month: S$400,000 × 5.5% / 12 = S$1,833

- Total interest over 4 months: S$7,333

- Plus ~S$2,000 in legal/valuation

- All-in cost: ~S$9,333

Compare that to the alternative: pay 20% ABSD of S$300,000 upfront on the new property, tying up cash for 6+ months while waiting for the remission refund to arrive. A bridging loan is almost always cheaper.

Two Flavours of Bridging Loan

- Capitalised bridging loan (HDB-style): interest rolls into the loan and is paid off together with principal at sale completion. Simpler, slightly more expensive.

- Simultaneous repayment bridging loan: monthly interest paid from your cash-flow during the bridge period. Slightly cheaper in absolute terms but requires ongoing cash outlay.

Most banks offer both; ask for quotes on each.

When a Bridging Loan Makes Sense

- You have a firm buyer for your existing home. OTP exercised, 5% deposit received. Banks require this as proof of expected sale proceeds.

- You are buying within 3–6 months of the old sale completing. Longer gaps make the interest cost unpalatable.

- You cannot wait for the old sale to complete before buying. If the new property is a once-in-a-decade opportunity (unit you’ve been watching for years, developer early-bird), time-sensitivity justifies the cost.

- You would otherwise pay ABSD and claim refund. The bridging interest is almost always less than the opportunity cost of parking 20% of purchase price with IRAS for 6+ months.

When a Bridging Loan is a Trap

- Your existing home hasn’t sold. Without a firm OTP, no bank will issue a bridging loan. Some private lenders will, at 8%+ — almost never worth it.

- Your buyer falls through. If your buyer rescinds or fails to complete, your bridging loan converts into a permanent, high-cost second mortgage. Make sure your buyer is well-qualified.

- Your sale completion slips. Each month of delay costs another S$1,800–S$2,000 on a S$400k bridge. Build a realistic completion timeline, not a hopeful one.

- You are eligible for the married couple ABSD remission anyway. If you are an SC couple upgrading, you may pay ABSD upfront and claim it back within 6 months of the new property’s TOP. The bridging loan just moves the cash-flow friction; it does not eliminate stamp duty.

Bridging Loans vs. ABSD Remission: The Real Comparison

Most Singaporean upgraders have two viable paths for buying before selling:

- Path A: Pay ABSD, claim remission. Pay 20% ABSD (S$300,000 on a S$1.5m buy) up front. Sell old home within 6 months of new property’s completion (TOP). Claim full remission. Time value of money lost: ~S$7,500 at 2.5% p.a. for 6 months. No bridging interest.

- Path B: Take bridging loan. Sell old home first (complete before new buy), use bridge to fund new downpayment. Pay 0% ABSD on new property. Bridging interest cost: ~S$7,000–S$10,000.

Path B is usually cheaper in absolute terms. Path A is simpler (no sale-timing risk) and is the default if your existing home is in a slow-selling segment.

How to Apply

Every major Singapore bank offers bridging loans. The application flow is standard:

- Get an OTP on your new property and OTP-back on your existing home (from the buyer).

- Approach your intended bank for both the new-home mortgage and the bridge as a joint application.

- Submit the old-home OTP as proof of expected sale proceeds.

- Bank values both properties, confirms bridge quantum.

- Bridge is drawn at the new-home completion; settled at old-home completion.

Most banks insist you take the new mortgage from them too — bridging loans are effectively a loss-leader to capture the long-term mortgage customer.

Frequently Asked Questions

Can I get a bridging loan if my existing home has not yet received an OTP?

Not from a mainstream bank. Some private financing providers will consider it, at rates starting around 8% p.a. In almost every case, it is cheaper to delay the new purchase than to use private financing.

What happens if the sale of my existing home falls through?

The bridging loan becomes due at the original 6-month mark. Most banks will consider extending or converting to a term loan, but at materially higher rates. Always plan for this contingency by having a backup buyer or a Plan B.

Is the interest on a bridging loan tax-deductible?

Generally no for owner-occupied property. Investment property rules differ — consult a tax professional.

Can I use CPF to service the bridging loan?

No. Bridging loans must be serviced in cash. CPF can fund the underlying downpayment but not the bridge interest.

What is the maximum bridge amount?

Typically 80% of the expected net sale proceeds of the existing property, subject to the bank’s internal risk assessment.

What to Do Next

- ABSD Singapore 2026 Complete Guide — the tax the bridging loan helps you avoid.

- Condo Downpayment Singapore 2026 — what the bridging loan is actually funding.

- All Home Loans & Mortgages.

Disclaimer: This guide is general information, not financial advice. Bridging loan terms vary by bank and property profile. Always consult a licensed mortgage broker before committing to a bridge and upgrade sequence.

0 Comments