Choosing between a fixed vs floating home loan in Singapore is the single biggest interest-rate decision most Singaporeans ever make. Get it right, and you save S$200–S$500 a month on a typical condo mortgage. Get it wrong — lock in fixed just before a rate cut, or float into a rate-hike cycle — and the same decision costs you S$50,000+ over a loan term.

This 2026 guide cuts through the bank-marketing gloss. No one knows where SORA will be in two years, but the decision framework is knowable. Here it is.

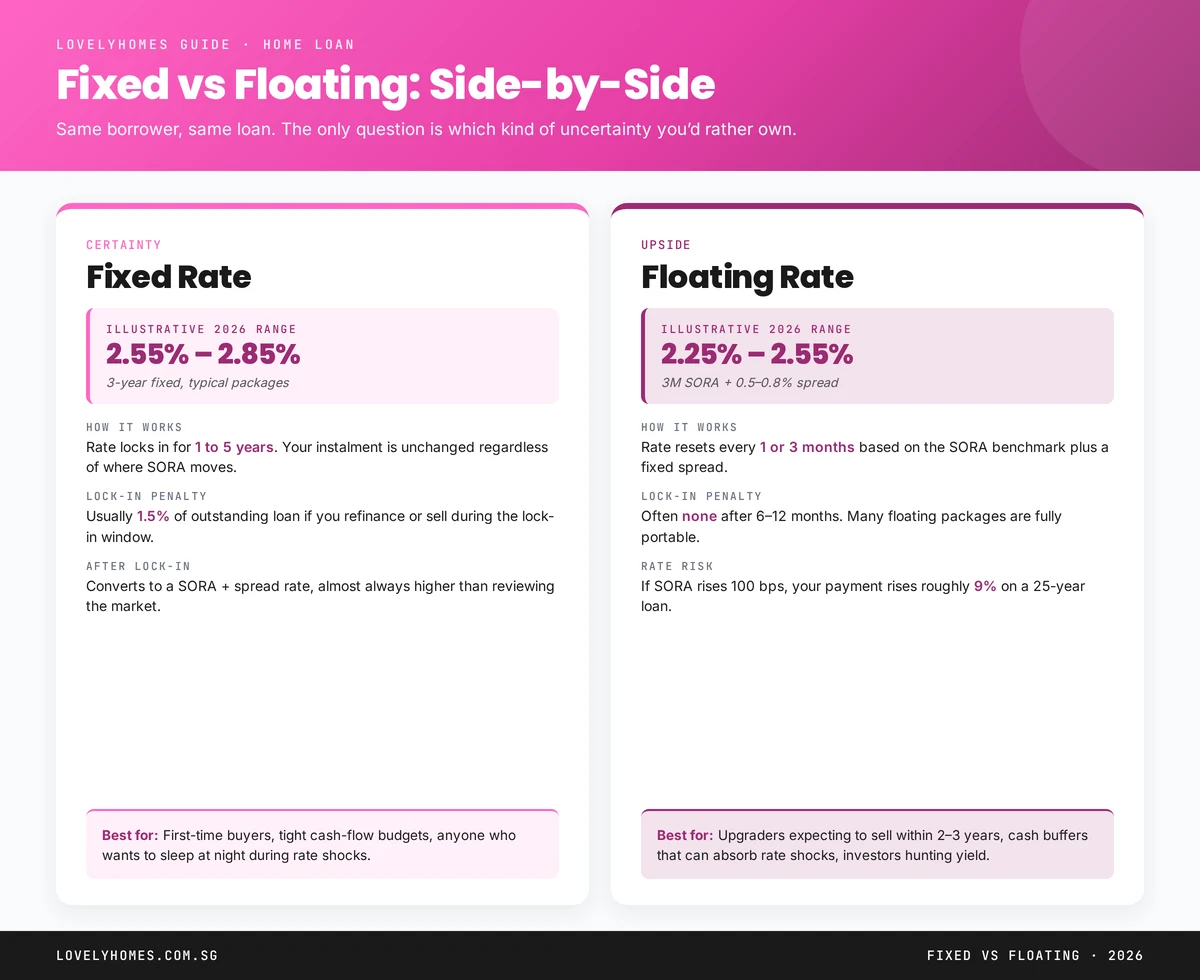

Quick Answer — Fixed vs Floating 2026

- Fixed: 2.55%–2.85% for 3-year packages; instalment locked; 1.5% penalty if you break lock-in.

- Floating (SORA): 2.25%–2.55% headline; resets every 1 or 3 months; usually no or light lock-in.

- Fixed wins when: you prioritise certainty, have tight cashflow, or expect rates to rise.

- Floating wins when: you have rate-shock buffer, are planning to sell within 2–3 years, or believe rates are peaking.

- Neither is strictly better — it depends on your time horizon and cash-flow tolerance.

What “Fixed” and “Floating” Actually Mean

A fixed-rate package contractually locks in your interest rate for a set term, typically 1, 2, 3, or 5 years. Your monthly instalment is flat; the bank bears the rate risk. At the end of the fixed term, the loan reverts to a floating rate (a “rollover” rate set by the bank) until you refinance or the loan matures.

A floating-rate package is priced as a benchmark plus a spread. In Singapore, the benchmark is almost always SORA 3M (the Singapore Overnight Rate Average, compounded over 3 months). A typical quote: “SORA 3M + 0.60% p.a., no lock-in”. Your rate resets every 1 or 3 months depending on the reset frequency.

The 2026 Rate Environment

SORA 3M is currently sitting around 2.3% after peaking at 3.9% in late 2023. Market consensus for 2026–2027 is a gradual drift to 2.0%–2.5%, with the Fed’s trajectory dominating.

In this environment, fixed rates and floating rates are pricing close: 3-year fixed packages quote around 2.55%–2.85%, and floating SORA+spread packages quote 2.25%–2.55%. The floating edge is roughly 30 bps.

Banks price this way because they are hedging a forward rate view. If banks thought rates would fall sharply, fixed rates would be materially cheaper than floating (banks want to lock in the highest rate they can). If they thought rates would rise, fixed would be materially more expensive.

When Fixed Wins

Fixed is the right call if any of the following apply:

- Tight monthly cash-flow. If a 100-bps rate rise would make your monthly instalment uncomfortable, pay the small fixed-rate premium for certainty.

- First-time buyer. First-time buyers often have the least cash buffer; predictability outweighs marginal rate savings.

- Property bought for the long haul. If you intend to hold 10+ years, locking in 3 years of certainty through the next rate cycle is worth it.

- Macro view: rising rates. If you believe the Fed or MAS will hike, fixed hedges you. The bank is taking the other side of that bet at a market-cleared price, but if your macro read is strong, that is the trade.

When Floating Wins

Floating is right when:

- You plan to sell or upgrade within 2–3 years. Floating packages typically have no lock-in past month 6–12. Fixed packages impose a 1.5% penalty that can cost S$12,000+ on an S$800k loan.

- You have substantial cash reserves. A 6-month emergency fund means you can ride out a 100-bps hike without distress.

- Macro view: falling or flat rates. Floating captures every cut as it happens; fixed locks you out of savings.

- You’re a property investor. Investors typically prioritise net yield and use cash buffers to manage rate risk; floating usually wins over an investment holding period.

The Hybrid Options

Two hybrid structures are popular in 2026:

- Fixed-then-floating (“step-up”). 2-year fixed at 2.65%, converts to SORA+spread thereafter. Gives you short-term certainty with upside later.

- Partial split. Some banks let you split the loan — e.g. 50% fixed, 50% floating. Effective blended rate halfway between the two packages, and you diversify rate risk.

The hybrid approaches are rarely dominated by a pure fixed or floating choice — they usually emerge as “middle” options when banks want to compete on flexibility.

Lock-In: The Real Cost Driver

Lock-in is more important than headline rate for most borrowers. A 2.85% 3-year fixed with a 3-year lock-in effectively bets you do not need to refinance or sell before month 36. If rates fall 50 bps and you want to switch, you pay 1.5% of outstanding — often S$10,000–S$15,000 — to break the lock-in.

Floating packages typically waive the lock-in after 6–12 months. This portability is why floating wins for anyone who might move, upgrade, or refinance mid-term.

SORA Reset Frequency: 1M vs 3M

Most floating packages now price against 3M SORA (the 3-month compounded average). The 1M version resets faster — you capture rate cuts sooner but also eat rate hikes sooner. In 2026’s low-volatility environment, 3M is slightly cheaper on spread but marginally less reactive.

The replacement of SIBOR and SOR with SORA was completed in mid-2024; any legacy SIBOR/SOR loans have been migrated or are on run-off.

Worked Comparison: S$800k Loan Over 25 Years

Consider two competing packages today for an identical loan:

- Package A — 3Y Fixed at 2.75%: monthly S$3,691, lock-in 3Y, 1.5% break penalty (S$12,000).

- Package B — SORA 3M + 0.55% (~2.30% effective): monthly S$3,516, lock-in 6M, no break penalty after.

If rates stay flat, Package B saves S$175 × 36 = S$6,300 over the first 3 years, with no lock-in risk. If SORA rises 100 bps, Package B payment rises to ~S$4,015 — S$324 more than A after the rise. Package B bet loses S$7,500 over 2 years of hikes.

The cross-over point is roughly a 60 bps sustained rise. Your view on that probability decides the trade.

Frequently Asked Questions

Can I switch from floating to fixed mid-term?

Yes, by refinancing or re-pricing with your existing bank. Re-pricing usually has no cost; refinancing has switching costs. Both are subject to whatever lock-in remains.

What if I want to prepay part of the loan?

Most packages allow partial prepayment of up to 25% of outstanding per year without penalty. Check the specific prepayment clause — some fixed packages are stricter.

Do I need MRTA (mortgage reducing term assurance)?

Not technically required for bank loans on private property, but most buyers take it. HDB loans with CPF require the HPS (see our CPF for Property guide).

Is there still SIBOR or SOR in 2026?

No. Both benchmarks were retired in mid-2024 and replaced with SORA. Any remaining SIBOR/SOR references in older documentation should be treated as historical.

Should I time the refinance to Fed meetings?

Marginally useful. Fed rate decisions move SORA, but banks lag Fed moves by weeks. The more reliable signal is your own lock-in expiry date — see our refinancing guide.

What to Do Next

- Home Loan Refinancing 2026 — the same decision, applied at your package reset.

- HDB Loan vs Bank Loan — fixed vs floating only applies to bank loans.

- All Home Loans & Mortgages.

Disclaimer: This guide is general information, not financial advice. Rate levels quoted are illustrative of 2026 packages and change frequently. Always obtain a current IPA and package terms directly from banks or a licensed mortgage broker before deciding.

0 Comments