Singapore Home Mortgage Guide 2026: Fixed vs Floating, SORA Rates and How to Choose

Quick Answer: Singapore Home Mortgage Guide 2026

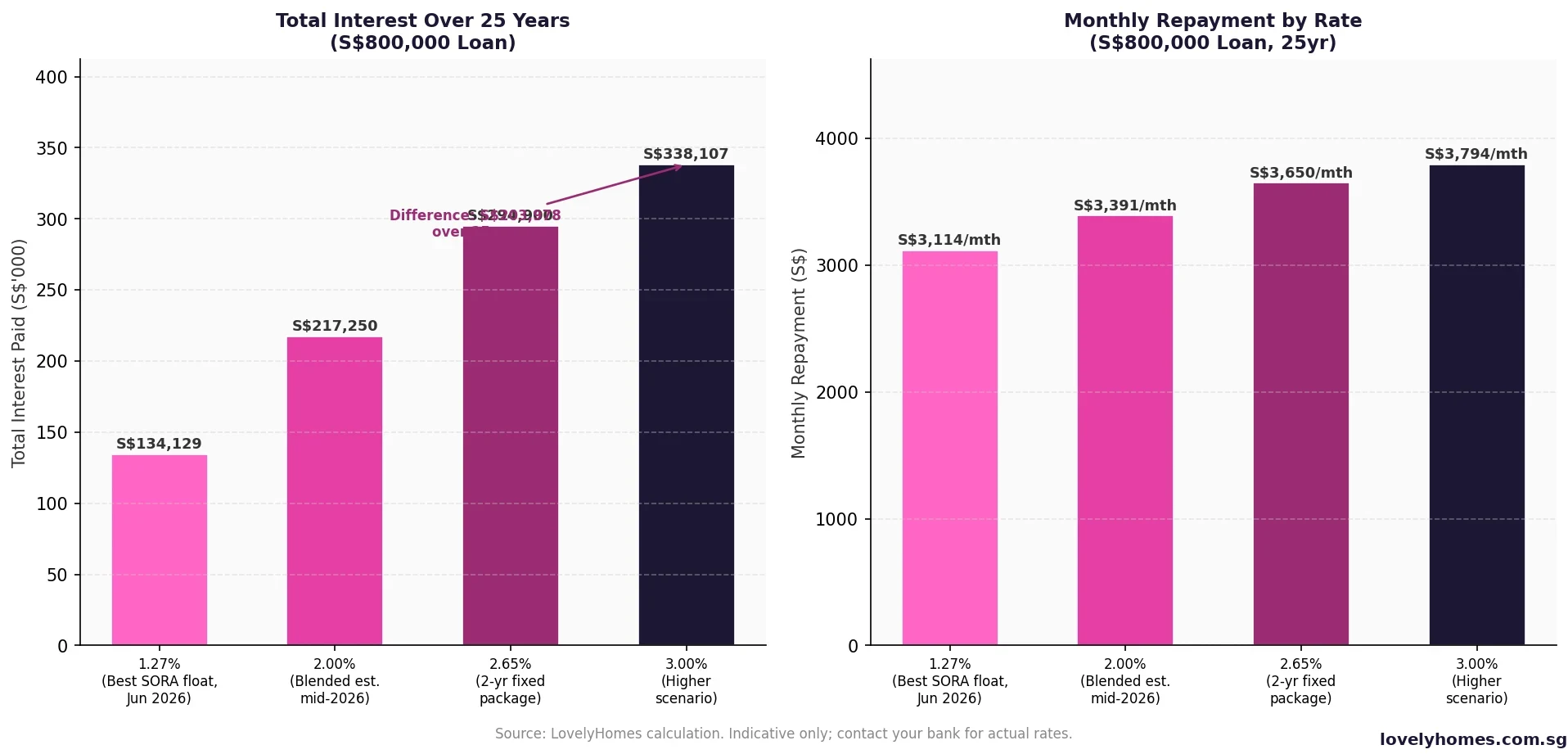

- Best SORA-linked floating rates start from 1.27% p.a. as of June 2026 — down from a peak of ~3.65% in mid-2023.

- Fixed rates (2-year) range from 2.45%–2.75% p.a. — offering payment certainty at a higher starting cost.

- The HDB concessionary loan rate stands at 2.6% p.a. — pegged to CPF OA rate + 0.1%, available for HDB flat purchases only.

- Bank loans allow LTV up to 75% on a first property; HDB loans allow up to 80% LTV.

- TDSR (Total Debt Servicing Ratio) cap is 55% of gross monthly income; MSR (Mortgage Servicing Ratio) cap of 30% applies additionally to HDB and EC loans.

- MAS stress-tests TDSR calculations at a floor of 4% regardless of the actual contractual rate.

- Refinancing can save S$8,000–S$20,000 over two years for a S$700,000-plus loan at current spreads.

- Lock-in periods of 2–3 years are standard; early full redemption penalty is typically 1.5% of outstanding loan.

What Is a Singapore Home Mortgage?

A home mortgage (or home loan) is a secured loan extended by a financial institution to help you finance the purchase of a residential property in Singapore. The property itself serves as collateral: if you default on repayments, the lender has the right to repossess and sell the property to recover the outstanding debt.

In Singapore, home mortgages are regulated by the Monetary Authority of Singapore (MAS), which sets the framework governing lending limits, stress tests, and debt servicing ratios for all licensed banks and finance companies. HDB separately administers its own concessionary loan programme for eligible flat buyers under different terms to bank loans. Every borrower in Singapore — whether buying an HDB flat, executive condominium, or private property — is subject to MAS’s property cooling measures, including the Loan-to-Value (LTV) limits and the Total Debt Servicing Ratio (TDSR) framework.

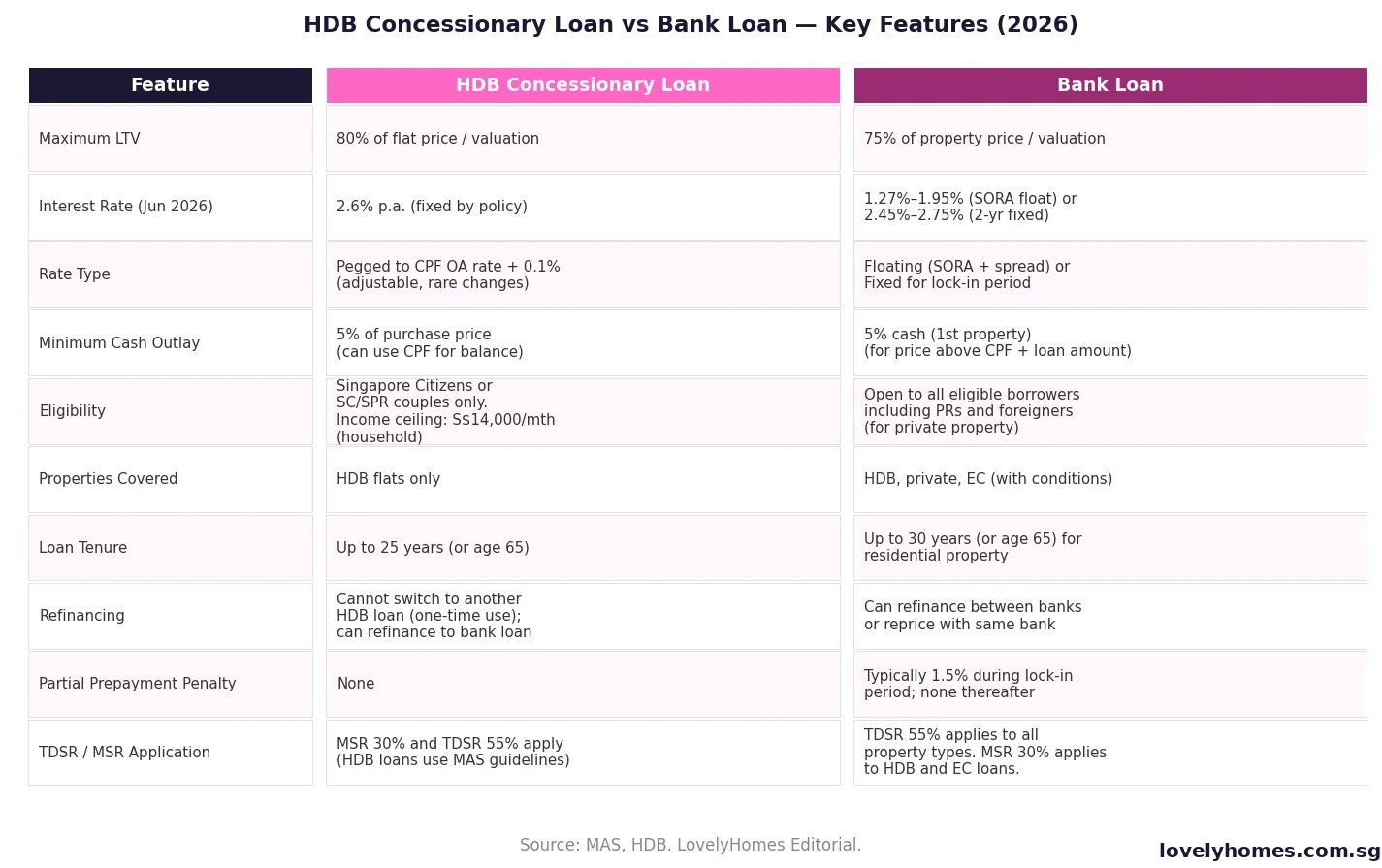

HDB Concessionary Loan vs Bank Loan: Which Should You Choose?

The first decision any Singapore property buyer faces is whether to finance through the HDB concessionary loan (available for eligible HDB flat buyers) or through a bank loan (available for both HDB and private property). The two options differ substantially on rate, eligibility, flexibility, and long-term cost.

The HDB concessionary loan charges interest at 2.6% p.a. — a rate pegged by policy to the CPF Ordinary Account (OA) interest rate of 2.5% plus 0.1%. This rate has remained unchanged since 1999 despite global interest rate cycles, though it can theoretically be revised if CPF OA rates change. Bank loans, by contrast, track market interest rates: as Singapore Overnight Rate Average (SORA) has fallen from 3.65% in late 2023 to 1.07% in June 2026, floating bank rates have fallen correspondingly to 1.27%–1.95% p.a., making them significantly cheaper than the HDB loan at current market conditions.

However, the HDB loan offers important advantages for risk-averse buyers: there is no lock-in period, no early redemption penalty, and the rate — while higher today — provides stability if global interest rates rise again. The HDB loan also allows a higher LTV of 80% (versus 75% for bank loans), reducing the upfront cash required.

One critical constraint: once you switch from an HDB loan to a bank loan, you cannot switch back. This makes the initial decision consequential.

Understanding SORA: Singapore’s Mortgage Benchmark Rate

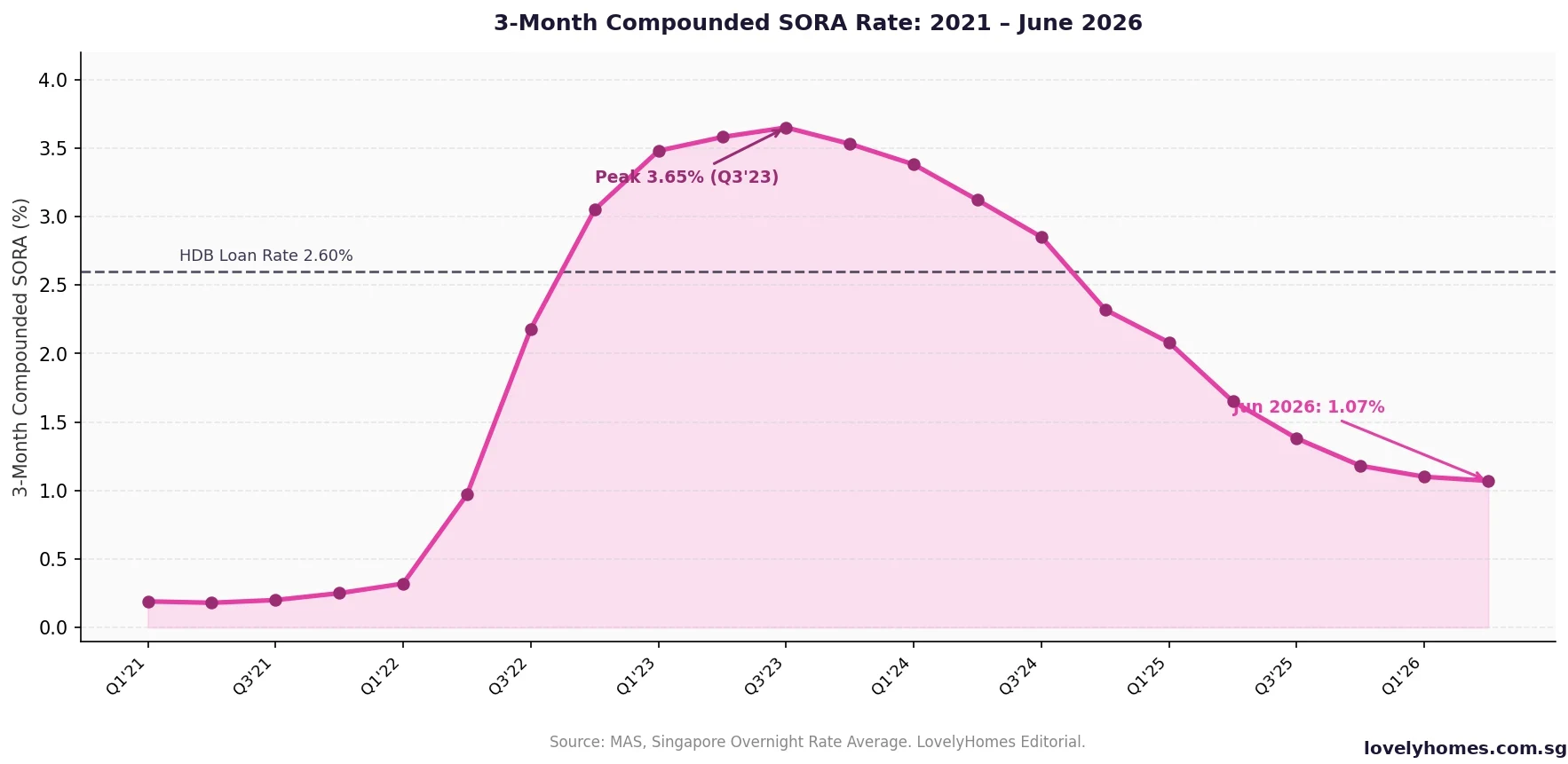

Since October 2021, Singapore banks have migrated their floating-rate home loans from the old SIBOR (Singapore Interbank Offered Rate) and SOR (Swap Offer Rate) benchmarks to SORA — the Singapore Overnight Rate Average administered by MAS. SORA is computed daily as the volume-weighted average rate of unsecured overnight interbank SGD transactions brokered in Singapore.

Home loans today are typically priced at a spread over the 3-Month Compounded SORA — for example, “3M SORA + 0.80% p.a.” A 3-Month Compounded SORA of 1.07% plus a 0.80% spread produces an effective rate of 1.87% p.a. The spread varies by bank, product, and loan size, but typically ranges from 0.20% to 0.90% p.a. for competitive packages in June 2026.

SORA fell sharply from its peak of approximately 3.65% in Q3 2023 as the US Federal Reserve paused and then cut rates, and as Singapore’s monetary policy stance eased. By June 2026, 3-Month Compounded SORA stands at approximately 1.07%, close to pre-2022 levels. Most analyst forecasts see SORA remaining between 0.7% and 1.5% through the second half of 2026, though any renewed global inflationary pressure could reverse this trajectory.

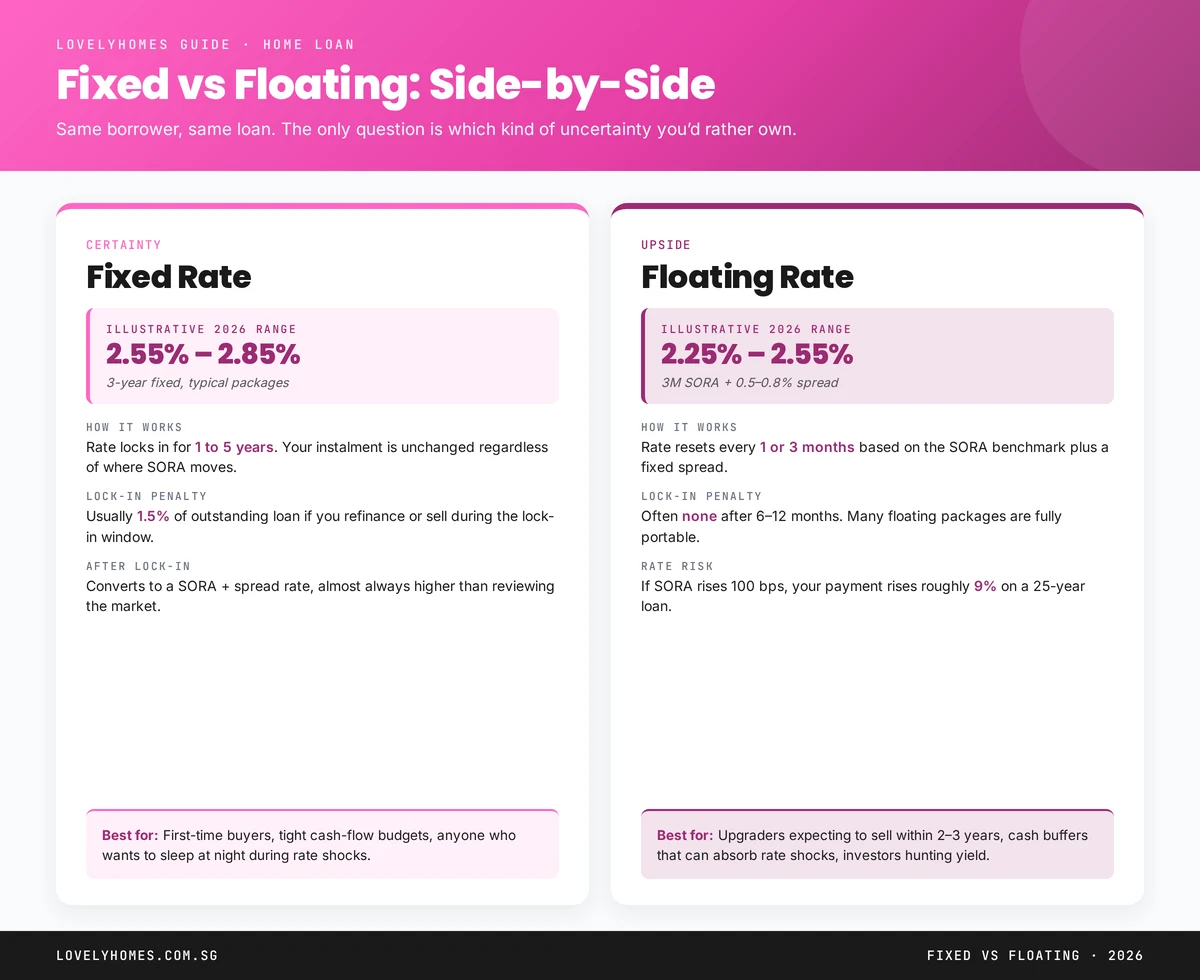

Fixed vs Floating Rate Mortgages in 2026

The choice between a fixed rate and a SORA-linked floating rate is the central strategic decision for most Singapore borrowers in 2026. Both options are currently available from major banks, and the decision hinges on your risk tolerance, cash flow needs, and view on where interest rates will move.

A floating SORA-linked rate adjusts with market conditions — if SORA falls further, your monthly instalment decreases; if it rises, it increases. In June 2026, best floating rates begin at 1.27% p.a., making them substantially cheaper than fixed alternatives. A fixed-rate package locks in a specified rate for 2–3 years, providing certainty on monthly payments regardless of what SORA does. June 2026 fixed rates range from 2.45% to 2.75% p.a. for 2-year fixed terms — a premium over floating rates, but offering protection against rate hikes.

Given that SORA is already low and forecasts suggest it will stay subdued through 2026, many financial advisers in Singapore currently favour floating packages for their immediate cost savings. However, borrowers should note: if MAS’s monetary policy stance tightens or if US rates rise unexpectedly, SORA could climb quickly. A hybrid approach — taking a shorter fixed term for certainty, then reassessing at repricing — is a common strategy for 2026.

Current Mortgage Rate Landscape in Singapore (June 2026)

As at June 2026, competition among banks for Singapore mortgage business remains intense, and indicative best rates are broadly as follows. Note that all packages require the borrower to meet eligibility criteria (income, property type, loan quantum), and rates are subject to change. Always obtain an In-Principle Approval (IPA) and compare offers from at least three banks before committing.

| Rate Type | Indicative Rate (Jun 2026) | Lock-in Period | Notes |

|---|---|---|---|

| SORA Floating (best) | ~1.27% p.a. (3M SORA + ~0.20%) | None / 1 year | Rates move quarterly with SORA resets |

| SORA Floating (typical) | ~1.50%–1.95% p.a. | 1–2 years | Spread 0.43%–0.88% over 3M SORA |

| 2-Year Fixed | ~2.45%–2.65% p.a. | 2 years | Converts to floating after lock-in |

| 3-Year Fixed | ~2.60%–2.75% p.a. | 3 years | Longer certainty; higher early exit penalty |

| HDB Concessionary Loan | 2.6% p.a. | No lock-in | HDB flat buyers only; SC/SC-PR eligible |

Key Mortgage Terms Decoded

Loan-to-Value (LTV) Ratio: The maximum percentage of the property’s purchase price or valuation (whichever is lower) that a lender will finance. Under MAS rules, a first bank loan allows up to 75% LTV for a 30-year term; a second outstanding loan reduces this to 45%, and third-or-subsequent loans to 35%.

Total Debt Servicing Ratio (TDSR): MAS caps the total monthly debt obligations (all loans, including car loans, personal loans, and the new mortgage) at 55% of gross monthly income. Banks stress-test the TDSR at 4% to ensure the loan remains serviceable if rates rise. If your TDSR exceeds 55% at the 4% floor rate, the bank will not approve the full loan amount requested.

Mortgage Servicing Ratio (MSR): An additional cap of 30% of gross monthly income that applies specifically to bank loans used to purchase HDB flats and executive condominiums. MSR is calculated on the actual loan rate.

Lock-in Period: A period during which you cannot fully repay or refinance the loan without incurring a penalty — typically 1.5% of the outstanding loan amount. Partial prepayments of up to a certain amount (often S$30,000–S$50,000 per year) may be allowed penalty-free even during lock-in, depending on the package.

Spread: The margin above SORA that the bank adds to arrive at the actual loan rate. For example, 3M SORA + 0.80% spread = effective rate. The spread is fixed for the life of the package (unlike the SORA component, which floats).

Repricing vs Refinancing: Repricing means switching to a different rate package offered by the same bank — usually possible at the end of a lock-in period, with a modest administrative fee (S$500–S$1,500). Refinancing means moving the entire loan to a different bank — typically saves more but involves legal fees (S$2,000–S$3,500), valuation fees, and a minimum loan quantum (usually S$200,000 or above).

Refinancing vs Repricing: When to Switch

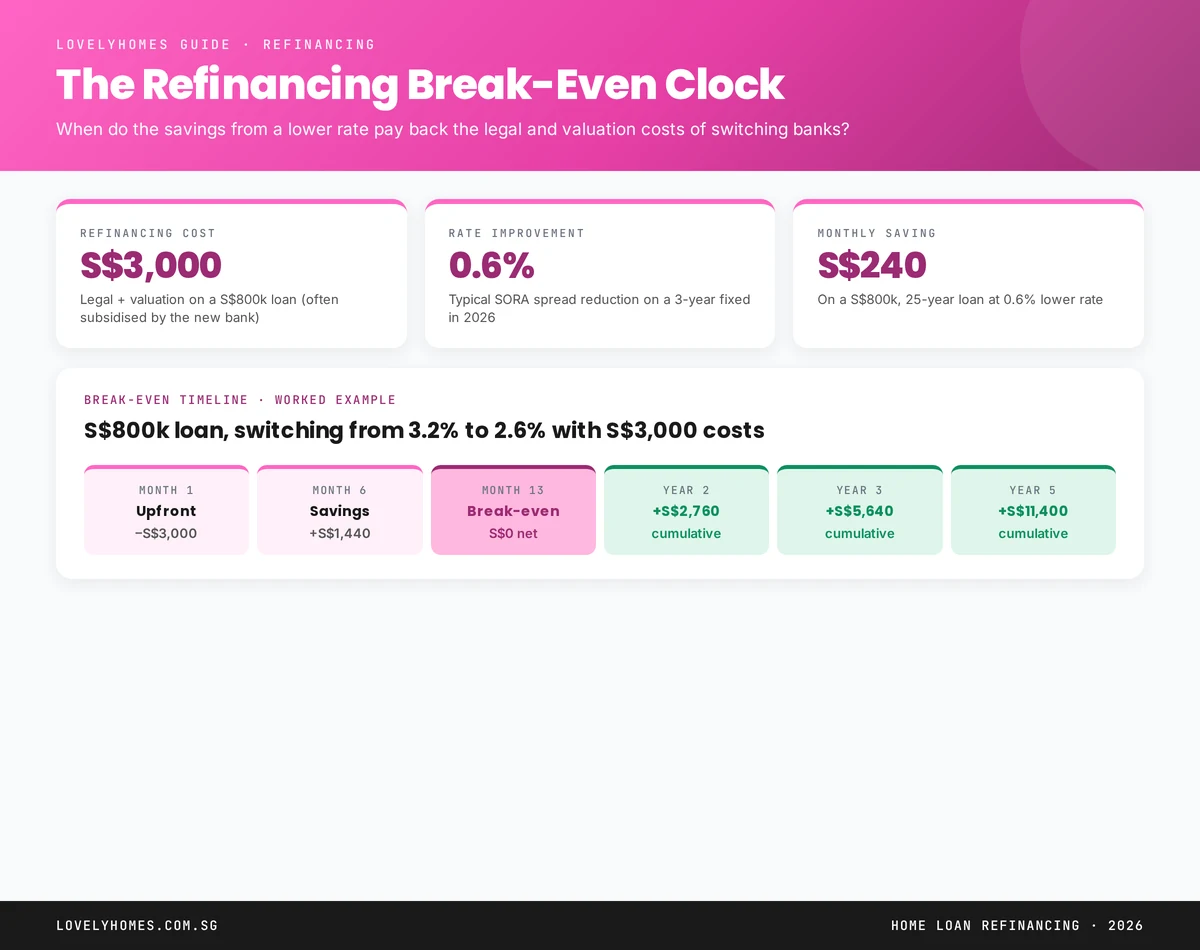

Refinancing — moving your mortgage from one bank to another — is one of the most effective ways Singapore property owners can reduce their borrowing costs over time. Most financial advisers recommend reviewing your home loan at least every 2–3 years, and particularly as your lock-in period expires.

The typical break-even calculation for refinancing involves comparing the projected interest savings over the next 2 years against the one-time costs: legal fees (S$2,000–S$3,500), valuation fees (S$300–S$500), and any cashback that was received from the existing bank and may need to be returned on early exit. As a rule of thumb, refinancing makes economic sense when the annual interest saving exceeds S$3,000–S$4,000 — typically achievable on loans of S$500,000 and above where the rate differential is 0.3% or more.

Repricing with the same bank is lower-cost and requires no legal or valuation work, making it attractive for smaller loan balances or where the new rate from your existing bank is competitive. Some banks now offer online repricing portals that complete the process in days without the need to submit income documents again.

Worked Example: The Choo Family — Choosing a Mortgage Package for an S$1.35M Condo

Marcus and Lin Choo are a Singapore Citizen couple with a combined gross monthly income of S$12,000, purchasing their first property — a 3-bedroom resale condominium in the OCR at S$1,350,000. This is their only residential property (no ABSD payable as first-purchase SC couple).

BSD calculation: 1% on first S$180,000 = S$1,800 + 2% on next S$180,000 = S$3,600 + 3% on next S$640,000 = S$19,200 + 4% on remaining S$350,000 = S$14,000. Total BSD = S$38,600 (payable from CPF OA).

Bank loan at 75% LTV: S$1,350,000 × 75% = S$1,012,500. Cash/CPF down payment required: S$337,500.

Option A — SORA floating at 1.27% p.a.: Monthly instalment ≈ S$3,940 (25yr, 300 months). TDSR: S$3,940 / S$12,000 = 32.8% — PASS (well within 55%). MAS stress test at 4%: monthly ≈ S$5,338; TDSR 44.5% — PASS.

Option B — 2-year fixed at 2.65% p.a.: Monthly instalment ≈ S$4,616 (25yr). TDSR: 38.5% — PASS. Monthly difference vs Option A: S$676/mth (S$16,224 over 2 years at current rates).

Decision: The Choos chose Option A (SORA floating) for the immediate S$676/mth saving. They note that if SORA rises to 2.5% (making their rate ~3.3%), the monthly payment would increase to approximately S$5,103/mth (TDSR 42.5% — still within limits). They set aside S$800/mth as a rate-rise buffer in a high-yield savings account.

Refinancing plan: At month 24, the Choos will review rates and consider refinancing to whichever bank offers the best package. Estimated legal fees if they refinance: S$2,500; break-even requires saving more than S$1,250/yr in interest — achievable if any bank offers a rate more than 0.13% lower than their renewal rate.

What This Means for Singapore Borrowers in 2026

The current rate environment represents a meaningful turning point for Singapore’s property financing landscape. After three years of elevated SORA rates that squeezed buyer affordability and contributed to a slowdown in the mid-price condo market, SORA at 1.07% marks a return to conditions last seen before the 2022 global rate-tightening cycle. For existing variable-rate borrowers, monthly instalments have already fallen materially from their 2023–2024 peaks — providing direct cash-flow relief and improving property investment yields.

For new buyers, low SORA rates increase the maximum loan quantum that passes the TDSR stress test, effectively expanding the pool of properties buyers can afford. The concern, however, is that easier financing conditions could feed further price growth — particularly in the OCR segment where demand remains robust and new supply is limited outside of GLS launches.

International peer comparison: SORA’s current 1.07% level is low by historical standards but is not out of line with broader Asia-Pacific trends. Australia’s RBA cash rate remains elevated at ~3.85%, while Hong Kong’s HIBOR has also eased but remains above Singapore levels. Singapore borrowers currently enjoy some of the most competitive mortgage rates in Asia.

What Might Come Next

Most analysts expect SORA to remain in the 0.7%–1.5% range through the remainder of 2026, supported by continued easing from the US Federal Reserve and MAS’s own exchange-rate-based monetary policy stance. A key risk is renewed US inflation — if the Fed pauses or reverses cuts, SORA could drift upwards. However, Singapore’s property market cooling measures (ABSD, TDSR, LTV limits) are designed to prevent mortgage stress even in rising-rate scenarios.

On the lending side, banks are actively competing for mortgage originations, and rate packages may become even more attractive in the second half of 2026 as lenders fight for market share. Borrowers who are out of lock-in — or approaching the end of their lock-in periods — should actively benchmark their current rates against the market before auto-repricing kicks in, as default repricing rates are typically less competitive than the best new-customer packages.

Frequently Asked Questions: Singapore Home Mortgage Guide 2026

Can I use CPF Ordinary Account funds to pay my monthly mortgage instalment?

Yes. CPF OA savings can be used to service monthly mortgage instalments on both HDB flats and private properties, subject to property-specific limits. For HDB flats, you can use CPF OA up to the Valuation Limit (the lower of the purchase price or the HDB valuation). For private properties, CPF OA usage is subject to the Valuation Limit and the Withdrawal Limit (typically 120% of the Valuation Limit for properties with remaining lease of at least 60 years). Note that CPF funds used incur accrued interest at 2.5% p.a., which must be refunded to your CPF account on the sale of the property.

What is the difference between an IPA and an AIP?

An In-Principle Approval (IPA), sometimes called an Approval-in-Principle (AIP), is a conditional commitment from a bank indicating how much they are willing to lend you based on a preliminary assessment of your income, credit history, and existing obligations. An IPA is not a formal loan offer and does not guarantee final loan approval (which is subject to a satisfactory property valuation and final income verification). Nevertheless, having an IPA before making an offer to purchase gives you confidence in your borrowing power and demonstrates seriousness to sellers. Most banks issue IPAs within 1–3 working days, and they are typically valid for 30–90 days.

What happens if my bank’s valuation comes in below the purchase price I agreed to pay?

If the bank’s valuation is lower than the agreed purchase price, your loan quantum is based on the lower valuation figure — not the price you agreed to pay. The shortfall (often called a “Cash-over-Valuation” or COV for HDB, or a valuation gap for private property) must be paid in cash and cannot be financed by the bank or from CPF. For example, if you agree to pay S$1.5M but the bank values the property at S$1.45M, the 75% LTV bank loan is S$1,087,500 (75% of S$1.45M), and you must fund the S$50,000 valuation gap in cash, plus your down payment. This is why checking property valuation before exercising the OTP is an important part of the buying process.

Can I take a home loan if I am a Singapore Permanent Resident or foreigner?

Singapore Permanent Residents (PRs) can take bank home loans for private properties and, under certain conditions, for HDB resale flats (subject to eligibility and the 5% deposit requirement). PRs are not eligible for the HDB concessionary loan. Foreign nationals (non-PRs) can take bank loans for approved private residential properties but are subject to significantly higher ABSD rates (60% as at June 2026) that effectively price most foreigners out of residential property investment. All borrowers — including PRs and foreigners — are subject to MAS’s TDSR framework and LTV limits for any property financing in Singapore.

What is the penalty for selling or refinancing during the lock-in period?

Early full redemption during a lock-in period typically attracts a penalty of 1.5% of the outstanding loan amount at the time of redemption. On a S$900,000 outstanding balance, this equates to S$13,500. Some packages allow partial prepayments of up to S$30,000–S$50,000 per year without penalty during lock-in. Banks sometimes also claw back any cashback or legal fee subsidies they paid at the time of the original loan. Before refinancing, always calculate the total cost of exit (penalty + clawback + new legal fees) against the projected savings from the new rate to determine the true break-even period.

Is the HDB concessionary loan better than a bank loan in 2026?

At current SORA levels (1.07% as of June 2026), bank floating rates of 1.27%–1.95% are materially below the HDB concessionary loan rate of 2.6% p.a., making bank loans financially more attractive in the short term. Over a S$500,000 loan at 25 years, the interest saving from a 1.5% bank rate versus 2.6% (HDB) is approximately S$67,000–S$80,000 in total interest. However, the HDB loan offers rate certainty, no lock-in, and a higher LTV (80% vs 75%), and is the only option if you cannot meet the bank’s income documentation requirements or if the interest rate environment changes materially. Risk-averse buyers — particularly first-timers with tight cash flows — may still prefer the simplicity and stability of the HDB loan despite the current rate disadvantage.

How does the TDSR stress test at 4% affect how much I can borrow?

MAS requires banks to compute your TDSR using a minimum rate of 4% (or the actual contractual rate if higher) when assessing whether your total monthly debt obligations stay within 55% of gross monthly income. This means even if your actual loan rate is 1.5%, the bank calculates affordability as if you were paying at 4%. On a S$1,000,000 loan at 25 years and 4%, the theoretical monthly instalment is approximately S$5,278. If your gross monthly income is S$10,000 and you have no other debts, your maximum monthly instalment under TDSR is S$5,500 (55% × S$10,000) — which barely passes. This stress test prevents borrowers from over-leveraging at low rates only to face distress if rates normalise upwards.

Click anywhere outside to close