Quick Answer: Singapore Private Property Buying Process at a Glance

- Total timeline: Typically 10–14 weeks from OTP to key collection for resale; new launches may take 2–4 years until TOP and key collection.

- OTP option period: 14 calendar days for private resale (standard); typically 3 weeks for new launch developer OTP.

- OTP fee: 1% of purchase price for resale; 5% for new launch (applied to purchase price on exercise).

- BSD: Buyer’s Stamp Duty must be paid within 14 days of OTP exercise. For a SGD 1.5M property, BSD is SGD 34,600.

- ABSD: Additional Buyer’s Stamp Duty (if applicable) is payable at the same time as BSD, must be paid in cash.

- Solicitor: Buyers must appoint their own conveyancing solicitor. Budget SGD 3,000–SGD 7,000 depending on property price.

- SLA caveat: Your solicitor lodges a caveat with the Singapore Land Authority to protect your interest after OTP exercise.

Overview: Buying Private Property in Singapore

Private residential property in Singapore — condominiums, apartments, landed houses, and executive condominiums after privatisation — is accessible to Singapore Citizens, Permanent Residents, and most foreigners (non-landed types only). The process is governed principally by the Conveyancing and Law of Property Act, the Residential Properties Act, and the Housing Developers (Control and Licensing) Act for new launches.

The private property buying process differs meaningfully from HDB. There is no central portal equivalent to HDB’s Resale Portal — private transactions proceed through solicitors and the URA/SLA framework. Stamp duties are higher for investors and upgraders, and the paperwork timeline is driven by solicitor and SLA processing rather than government approval queues. This guide walks through every stage in sequence, from pre-purchase preparation through to key collection, for both resale and new launch purchases in 2026.

Step 1: Pre-Purchase Financial Preparation

Get your finances in order before viewing properties

Check your CPF Ordinary Account balance, outstanding loan obligations, and credit bureau score. Determine how much cash you have available above the mandatory 5% (bank loan) or 0% (HDB loan for eligible buyers). Engage a mortgage broker or bank early — not after you have fallen in love with a property.

The first step is establishing your maximum budget. This requires knowing: (a) your gross monthly income for TDSR and MSR purposes, (b) all existing debt obligations including car loans, personal loans, and credit cards, (c) your CPF OA balance available for the down payment and BSD, and (d) your liquid cash position. The difference between what you can borrow (determined by TDSR at 55% of income) and what your cash and CPF can fund determines your maximum purchase price ceiling.

For most private property buyers, MAS’s stress-test floor of 4% per annum is the binding constraint. At 4%, 30 years, each SGD 1,000 per month of mortgage capacity supports approximately SGD 172,000 in loan quantum. A couple with SGD 12,000 combined income, no other debts, and a TDSR headroom of SGD 6,600 per month (55%) could theoretically borrow approximately SGD 1,134,000 — meaning at 75% LTV, the maximum purchase price before down payment considerations is approximately SGD 1.51 million.

Step 2: In-Principle Approval (IPA)

Obtain an In-Principle Approval letter before making offers

An IPA (sometimes called an Approval in Principle or AIP) is a conditional commitment from a bank confirming the maximum loan amount it is willing to lend, subject to the actual property passing its valuation and no material change to your financial circumstances.

IPAs are non-binding and typically valid for 30 days. They do not guarantee the final loan but give sellers and property agents confidence that you are a serious buyer. Most sellers in the current private market expect buyers to hold an IPA before granting an OTP. Applying for an IPA is free and requires payslips, CPF statements, NRIC or passport, and a credit bureau consent form.

Step 3: Property Search and Negotiation

Search, view, and negotiate — using URA transaction data to inform pricing

Singapore’s URA Realis database publishes every private residential transaction at postcode level. Use this to determine the reasonable market value range for your target property before making any offer.

For resale private property, prices are negotiable. The seller’s asking price is typically 3–8% above the URA transacted median for the development, with COV (cash-over-valuation) situations common in tighter submarkets. Industry figures show that the median transaction price for private non-landed property in the Outside Central Region reached approximately SGD 1,800 psf in Q1 2026, while the Core Central Region median was approximately SGD 2,900 psf.

For new launch developer sales, prices are set on a price list and are generally non-negotiable, though developers may offer early-bird discounts, absorption of stamp duty, or furniture vouchers depending on project stage and market conditions.

Step 4: Grant the Option to Purchase (OTP)

The OTP is the first legally binding step — read every clause before signing

The seller grants the OTP upon receipt of the option fee. For resale private property, the standard option fee is 1% of the agreed purchase price. You then have 14 calendar days — including weekends and public holidays — to exercise (complete) the OTP by paying an additional 4% exercise fee, bringing the total to 5%.

If you do not exercise the OTP within the option period, the option lapses and the 1% option fee is forfeited to the seller. For new launch OTPs, the developer’s standard form typically grants three weeks and requires 5% on exercise. The OTP is a standard Law Society form for resale transactions; developers use their own form for new launches, and buyers should have their solicitor review it before exercising.

Step 5: Appoint Your Conveyancing Solicitor

Appoint your own solicitor — the seller’s solicitor cannot act for you

Unlike some jurisdictions, Singapore law does not permit one solicitor to act for both buyer and seller in the same conveyancing transaction (except in very limited circumstances). You must appoint your own solicitor from a Singapore-registered firm.

The Law Society’s Conveyancing Practice Directions govern the process. Your solicitor will: check title at the Singapore Land Authority, verify that there are no outstanding caveats or encumbrances, handle stamp duty payment, draft and review the Sale and Purchase Agreement (S&P), liaise with CPF Board for any CPF withdrawal, liaise with your bank for loan drawdown, and lodge the instrument of transfer at SLA at completion.

Legal fees for private property conveyancing in 2026 typically range from SGD 3,000–SGD 4,500 for properties below SGD 1.5 million to SGD 5,000–SGD 7,000 for properties above SGD 2 million, plus disbursements (title searches, SLA lodgement fees, CPF board fees, etc.) of approximately SGD 700–SGD 1,200.

Step 6: Exercise the OTP and Pay Stamp Duties

Exercise the OTP by paying the 4% exercise fee, then settle BSD and ABSD within 14 days

BSD must be paid to IRAS within 14 days of exercising the OTP. ABSD, if applicable, is payable at the same time. Both are computed on the higher of the purchase price and the bank’s independent valuation.

BSD rates in 2026 (on the purchase price): 1% on the first SGD 180,000; 2% on the next SGD 180,000; 3% on the next SGD 640,000; 4% on the next SGD 500,000; 5% on amounts above SGD 1.5 million up to SGD 3 million; 6% above SGD 3 million. For a SGD 1.8 million property, BSD is SGD 44,600. CPF OA may be used to pay BSD on private property, subject to the CPF withdrawal limit for the property.

| Stamp Duty Type | Who Pays | Rate / Quantum | Deadline | Can CPF Pay? |

|---|---|---|---|---|

| BSD | Buyer | 1–6% tiered on purchase price | 14 days from OTP exercise | Yes (private property) |

| ABSD (SC 1st) | SC buyer | 0% | Same as BSD | N/A |

| ABSD (SC 2nd) | SC buyer | 20% | Same as BSD | No — cash only |

| ABSD (SC 3rd+) | SC buyer | 30% | Same as BSD | No — cash only |

| ABSD (SPR 1st) | SPR buyer | 5% | Same as BSD | No — cash only |

| ABSD (SPR 2nd+) | SPR buyer | 30% | Same as BSD | No — cash only |

| ABSD (Foreigner) | Foreign buyer | 60% | Same as BSD | No — cash only |

| SSD (if applicable) | Seller | 4–12% if sold within 3 yrs | 30 days from disposal | No |

Step 7: Bank Loan Drawdown and CPF Withdrawal

Your bank formally processes the loan; your solicitor coordinates CPF withdrawal simultaneously

Between OTP exercise and completion, your bank conducts its own independent valuation of the property. If valuation comes in below the purchase price, your loan quantum is reduced accordingly and you must fund the shortfall in cash.

The bank’s Letter of Offer (LO) is typically issued within 1–2 weeks of the bank receiving your full documentation package. You must accept the LO and return a signed copy. Your solicitor simultaneously requests CPF Board to prepare the CPF withdrawal documents. For progressive payment schemes (new launches), drawdown occurs stage by stage as construction milestones are reached — buyers pay only on each certified stage rather than a lump sum at completion.

Step 8: Title Search and Due Diligence

Your solicitor confirms title is clear — no outstanding caveats, mortgages, or charges

The SLA title register shows all encumbrances registered against the property. Your solicitor checks for: outstanding caveats from prior buyers, mortgages from the seller’s lender (to be discharged at completion), court orders, Strata Management Act compliance for condominiums, and compliance with URA development conditions.

Step 9: Completion Appointment

Both parties attend completion — typically 8–12 weeks after OTP exercise for resale

At the completion appointment (held at SLA or through electronic lodgement), your solicitor and the seller’s solicitor exchange the balance purchase monies for the executed Instrument of Transfer. The bank releases the loan funds directly to the seller’s solicitor. CPF monies are credited simultaneously.

Immediately after completion, your solicitor lodges the Instrument of Transfer at SLA to register you as the new owner. SLA processing takes approximately 3–5 working days after submission. Upon lodgement, any prior caveats are cancelled and your ownership is registered on the land title.

Step 10: Key Collection

Keys are handed over at or immediately after completion for resale; at TOP for new launches

For resale properties, keys are exchanged at the completion appointment itself or on a pre-agreed handover date. For new launch properties, key collection occurs at TOP (Temporary Occupation Permit) — which may be 2–4 years after the OTP exercise date.

Before collecting keys, conduct a thorough pre-handover inspection. For resale, verify the condition matches the representations in the S&P and that fixtures and fittings listed in the agreement are present. For new launches, HDB or the developer provides a defects liability period (typically 12 months from TOP) during which defects must be rectified at no cost to the buyer.

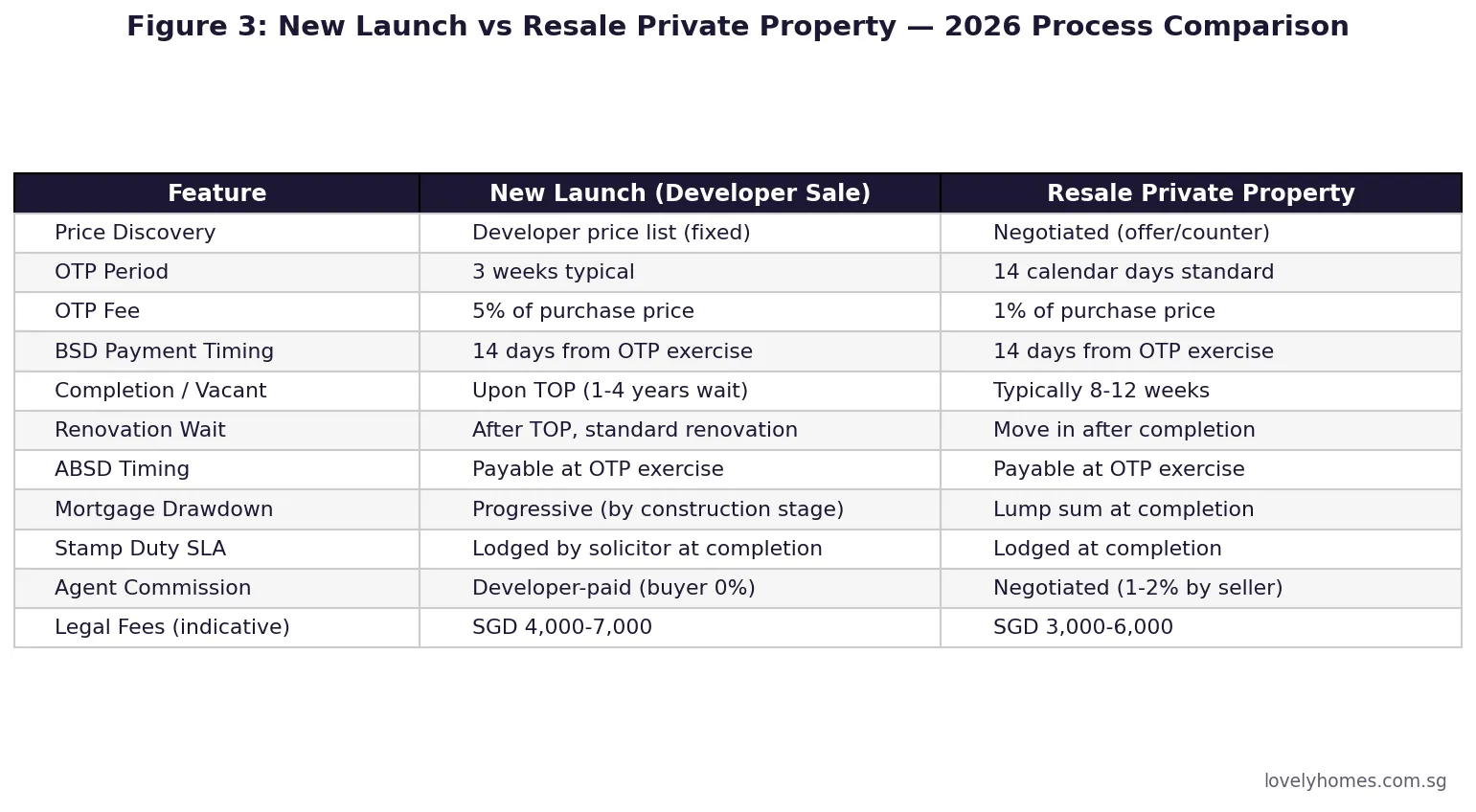

New Launch vs Resale: Key Differences

Choosing between a new launch and a resale private property is as much a lifestyle decision as a financial one. New launches offer modern specifications, deferred completion, and progressive payment schemes that reduce upfront cash pressure — but buyers wait years for occupation. Resale offers immediate entry, the ability to inspect exactly what you are buying, and neighbourhoods with established amenities.

Financially, new launches typically carry a price premium over resale in the same precinct — industry figures show new launch median PSFs in 2026 running approximately 15–25% above comparable resale units in the same district. Against this premium, progressive payment and potential capital appreciation from a lower launch price are the typical counterarguments. Resale buyers also benefit from the ability to use their CPF for stamp duty more immediately, rather than holding CPF balances idle during a lengthy construction period.

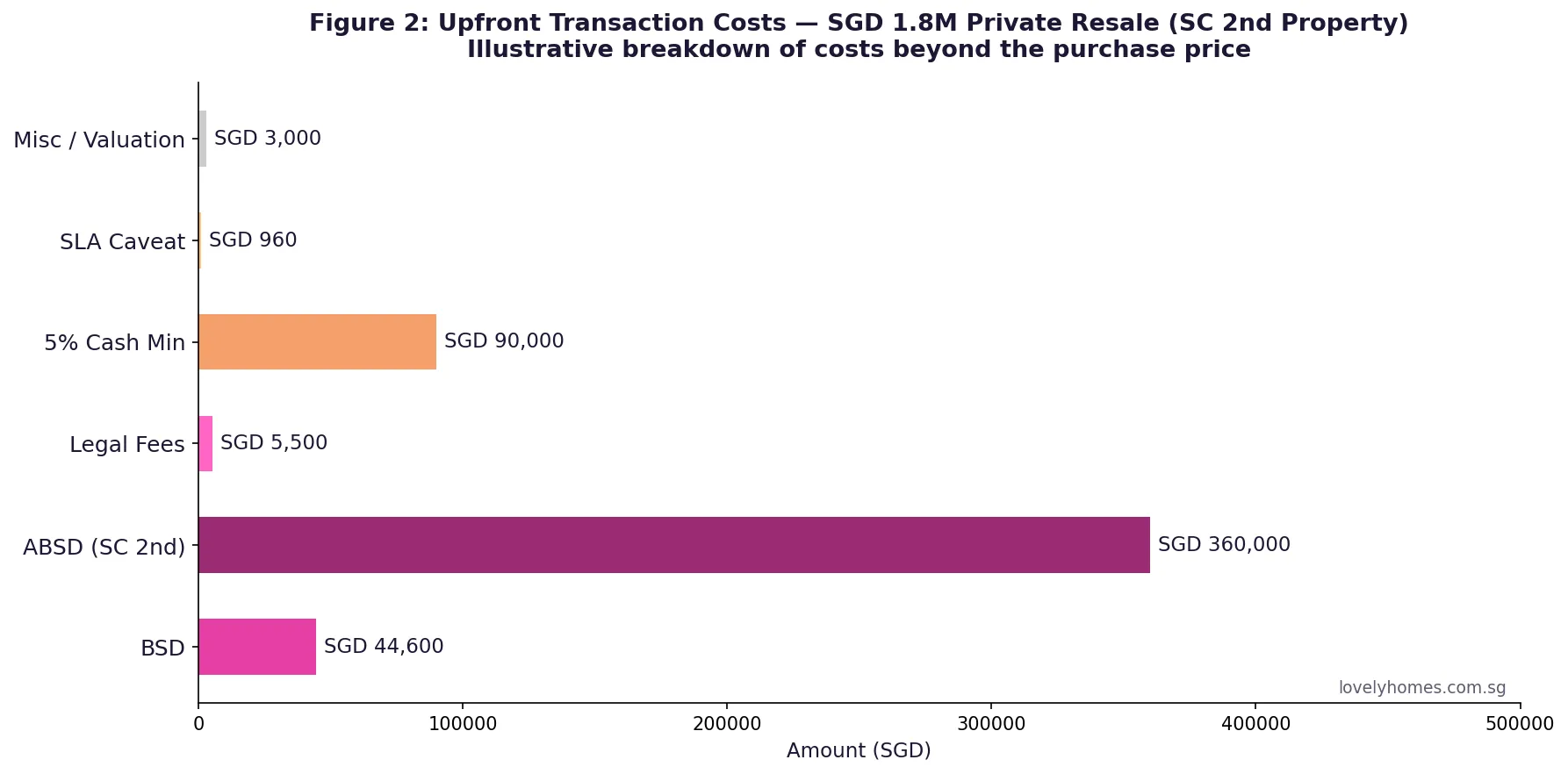

Worked Example: Chen Family — D15 Private Resale Condo SGD 1.8M (SC Second Property)

The Chen family are a Singapore Citizen couple. Mr Chen owns an HDB flat (not yet sold — MOP cleared in 2024). They are purchasing a D15 3-bedroom resale condo unit at SGD 1,800,000. Combined gross monthly income: SGD 14,000. No other loan obligations. CPF OA combined: SGD 200,000.

Stamp duties payable:

BSD (tiered on SGD 1.8M): 1% × SGD 180,000 + 2% × SGD 180,000 + 3% × SGD 640,000 + 4% × SGD 500,000 + 5% × SGD 300,000 = SGD 1,800 + SGD 3,600 + SGD 19,200 + SGD 20,000 = SGD 44,600.

ABSD (SC 2nd property, 20%): SGD 1,800,000 × 20% = SGD 360,000 — payable in cash (not CPF). Deadline: 14 days from OTP exercise.

BSD may be funded from CPF OA (SGD 44,600 from CPF OA).

Loan:

Bank loan (75% LTV on SGD 1.8M): SGD 1,350,000. Rate: 3.0% p.a. 2-yr fixed, then SORA-linked float. Tenure: 25 years (Mr Chen is 40).

Monthly repayment: approximately SGD 6,408/mth.

TDSR check: SGD 6,408 / SGD 14,000 = 45.8% — within 55% cap. Pass.

Cash requirement (non-CPF):

5% mandatory cash down: SGD 90,000

Remaining 20% balance: SGD 360,000 — from CPF OA (SGD 155,400 after BSD deduction) + additional cash (SGD 204,600)

ABSD: SGD 360,000 cash

Legal fees: approximately SGD 6,000 cash

Total cash needed before CPF: approximately SGD 660,600.

After CPF OA use (SGD 155,400 on 20% balance + SGD 44,600 BSD): Cash required is approximately SGD 660,600 − SGD 0 = SGD 660,600 (ABSD + 5% + legal + cash top-up for 20% balance).

Lesson: ABSD at 20% (SGD 360,000) dominates the cash requirement for a second property purchase. The ABSD SC couple remission scheme (6-month window after buying to sell the first property) is relevant here — if the Chens sell their HDB flat within 6 months of the condo completion date, they may apply to IRAS for the SGD 360,000 ABSD refund. See our ABSD Remission Guide 2026 for full details on eligibility and the refund process.

Why This Matters: Private Property Ownership and Singapore’s Wealth Architecture

Private residential property is the dominant asset class in Singapore household balance sheets. MAS data shows that property accounts for approximately 43% of total household net worth. The private property buying process — its stamp duties, LTV constraints, and solicitor-mediated completion — is designed to ensure that each step is documented, verified, and legally sound. Unlike jurisdictions where informal agreements or verbal commitments carry weight, Singapore’s system gives primacy to registered instruments at SLA.

The 14-day BSD deadline, the mandatory caveat lodgement, and the SLA land title register together create a system where buyers’ interests are protected quickly after commitment. Understanding each step — particularly the BSD and ABSD cash requirements — prevents the scenario where a buyer commits to an OTP and then discovers they cannot fund the stamp duties within the statutory deadline.

Compared with Hong Kong (where stamp duty is similarly high but legal completion processes vary by tenure type), or Australia (where conveyancing timelines and cooling-off periods vary by state), Singapore’s process is more standardised and process-driven — reducing risk but also reducing flexibility.

What Might Come Next

MAS and URA periodically review the private property buying framework. The 2023 cooling measures that raised ABSD to 60% for foreigners and 20% for SC second property buyers remain in effect as at mid-2026. Any market moderation or sustained price correction could prompt a recalibration, but MAS has historically maintained that cooling measures are removed only when there is sustained evidence that the property market is stable. The URA Q2 2026 flash estimates, expected in the first week of July 2026, will provide the next data point on whether the moderated price growth of Q1 2026 (+0.9% PPI) has continued into Q2.

Frequently Asked Questions

Can I back out after exercising the OTP?

Once you have exercised the OTP and paid the 5% option exercise fee, you are contractually bound to complete the purchase on the terms set out in the Option. Backing out at this stage means forfeiting the 5% (the 1% option fee and 4% exercise fee) and potentially exposing yourself to a claim by the seller for damages if the loss exceeds the forfeited amount. In practice, sellers in Singapore generally accept the forfeiture as full settlement and re-list the property, but this is not guaranteed and depends on market conditions at the time.

What is the difference between the OTP option fee and the option exercise fee?

The OTP option fee (1% for resale, 5% for new launch) is paid when the seller grants the OTP — it buys you the right, but not the obligation, to purchase the property during the option period. The option exercise fee is the additional amount paid when you choose to exercise (activate) the OTP and commit to the purchase. For resale properties, the standard split is 1% on grant and 4% on exercise, totalling 5%. For new launches, developers typically require the full 5% at exercise. Both amounts are applied toward the purchase price at completion — they are not fees lost to an intermediary.

Do I need a property agent to buy private property in Singapore?

You are not legally required to use a property agent (registered with CEA) when purchasing private property in Singapore. Buyers may transact directly without an agent. In practice, most buyers use an agent, particularly for resale where searching inventory, arranging viewings, and negotiating price requires market knowledge and access to the co-broking network. For new launch developer sales, developers typically have their own salespeople and do not charge the buyer agent commission — the buyer’s agent is paid by the developer from the sales proceeds. If you choose to transact without an agent, ensure you engage a solicitor early to review the OTP and S&P.

How long does SLA take to register the title after completion?

SLA processes lodgements of instruments of transfer (completing the change of ownership on the land title register) within approximately 3–5 working days of receipt from the solicitor. Electronic lodgement through SLA’s electronic lodgement system has significantly reduced turnaround times from the historical weeks. You will receive a new Certificate of Title (or updated digital record) showing you as the registered owner. In the interim, the lodged instrument constitutes constructive notice of your ownership.

Can a Singapore PR buy any type of private property?

Singapore Permanent Residents may purchase non-landed private residential property (condominiums, apartments, executive condominiums after privatisation) freely. PRs require Land Dealings Approval Unit (LDAU) approval to buy restricted residential property — which includes landed property (terrace houses, semi-detached, bungalows, and Good Class Bungalows) on Singapore Island. This approval is rarely granted. PRs may buy strata-titled landed housing (strata landed, such as cluster houses or townhouses on strata lots) without LDAU approval. PR buyers are subject to the 5% ABSD on a first property and 30% ABSD on a second.

What is a progressive payment scheme and how does it work for new launches?

The progressive payment scheme (PPS) is the standard payment structure for new launch developer sales. Under PPS, the purchase price is paid in stages as specific construction milestones are completed and certified by a qualified person under the Housing Developers Rules. Key stages include foundation, reinforced concrete frame, partition walls, roofing, windows/doors, car park/roads, and TOP. The loan drawdown and CPF withdrawals are similarly staggered. This means a buyer purchasing a new launch in 2026 may not draw down their full loan until 2028 or 2029, reducing early interest payments but extending the financial commitment period.

What inspections should I do before signing the OTP on a resale property?

At a minimum: (1) structural inspection — check for cracks, water seepage, and signs of settlement; (2) plumbing and drainage — run all taps, flush toilets, check for leaks under sinks; (3) electrical — test switches, sockets, air-conditioning units; (4) windows and doors — check for warping, sealing, and opening mechanism; (5) confirm all fixtures and fittings agreed in the OTP are present. For older properties (more than 20 years), engage a qualified independent building inspector. The cost of a professional inspection (SGD 300–SGD 600) is minimal relative to the purchase price and the remediation cost of uncovering issues post-completion.

0 Comments