The Central Provident Fund (CPF) is Singapore’s mandatory social security savings scheme — and for most Singaporeans, it is also the single largest source of funds for buying a home. Yet CPF property rules are among the most commonly misunderstood in the entire home-buying process. How much can you actually withdraw? What happens when you sell? How does accrued interest quietly erode your cash proceeds? This guide answers every question, with worked examples, data tables, and real SGD figures.

Quick Answer — CPF for Property: 10 Key Points

- CPF Ordinary Account (OA) earns 2.5% p.a. interest — the same rate used to calculate accrued interest you must refund at sale.

- You may use CPF OA for down payment, stamp duties (BSD only, not ABSD), and monthly mortgage instalments.

- For HDB flats purchased with a HDB concessionary loan, there is no CPF Valuation Limit — you can use CPF OA without a cap (subject to the HDB loan quantum).

- For private property or HDB with a bank loan, the Valuation Limit (VL) = lower of purchase price or market valuation.

- You can use CPF beyond the VL up to 120% of VL only if you have set aside the Basic Retirement Sum (BRS) — applicable from age 55.

- Properties with a lease under 20 years remaining cannot use CPF at all.

- Short-lease properties (20–60 years) face a prorated withdrawal limit: remaining lease ÷ 95 × VL.

- When you sell, you must refund CPF principal plus accrued interest at 2.5% p.a. compounded — not just the principal withdrawn.

- After age 55, you must set aside the Full Retirement Sum (FRS) before using CPF for a new property purchase.

- CPF cannot be used to pay ABSD — only BSD on residential property qualifies.

What Is CPF OA and Why Does It Matter for Property?

The CPF Ordinary Account is the component of your CPF most directly relevant to housing. Contributions flow in automatically from both employee and employer — at 23% of wage for employees aged up to 35, tapering as one ages — and the OA earns a guaranteed 2.5% per annum interest rate, with a bonus 1% on the first S$60,000 of combined CPF balances. The OA balance can be deployed for HDB flat purchases, private residential property, CPF-Approved Mortgage Schemes, and certain insurance products.

The Central Provident Fund Board (CPF Board), a statutory board under the Ministry of Manpower, administers all CPF housing withdrawals. Its Public Housing Scheme (PHS) and Private Properties Scheme (PPS) govern how OA funds flow to property purchases. Every withdrawal is recorded in your CPF statement and a notional “accrued interest” clock starts ticking from the day each dollar is withdrawn.

CPF Withdrawal Limits by Property Type

The rules differ significantly depending on whether you are buying an HDB flat or a private property, and whether you finance through a HDB concessionary loan or a bank loan. The table below captures every scenario recognised by CPF Board as at May 2026.

The key distinctions are worth spelling out plainly. For an HDB flat purchased with the HDB concessionary loan (2.6% p.a. as at May 2026), you may direct CPF OA funds towards every dollar of the purchase — down payment, stamp duties, and each monthly instalment — without any ceiling tied to valuation, provided the remaining lease covers the youngest buyer to at least age 95, or is at least 20 years long at point of purchase. This reflects HDB’s policy intent: CPF should ease the burden of public housing acquisition.

For private residential property, or an HDB flat financed by a bank, the Valuation Limit discipline applies. CPF Board sets VL at the lower of the purchase price and the market valuation at the time of purchase — so if you overpay for a unit relative to its assessed market value, your CPF-eligible ceiling is capped at the lower number. This matters acutely in a competitive bidding environment where winning offers routinely exceed valuations.

The Accrued Interest Clock

This is the feature of CPF housing that surprises most first-time sellers. Every dollar you withdraw from CPF OA for property accrues notional interest at 2.5% per annum, compounded. This is not additional money leaving your pocket while you own the home — it is a deferred obligation that crystallises at the point of sale (or full loan repayment). When you sell, your conveyancing lawyer will receive from CPF Board a statement of the total refund amount: principal withdrawn plus all accrued interest since the first withdrawal date.

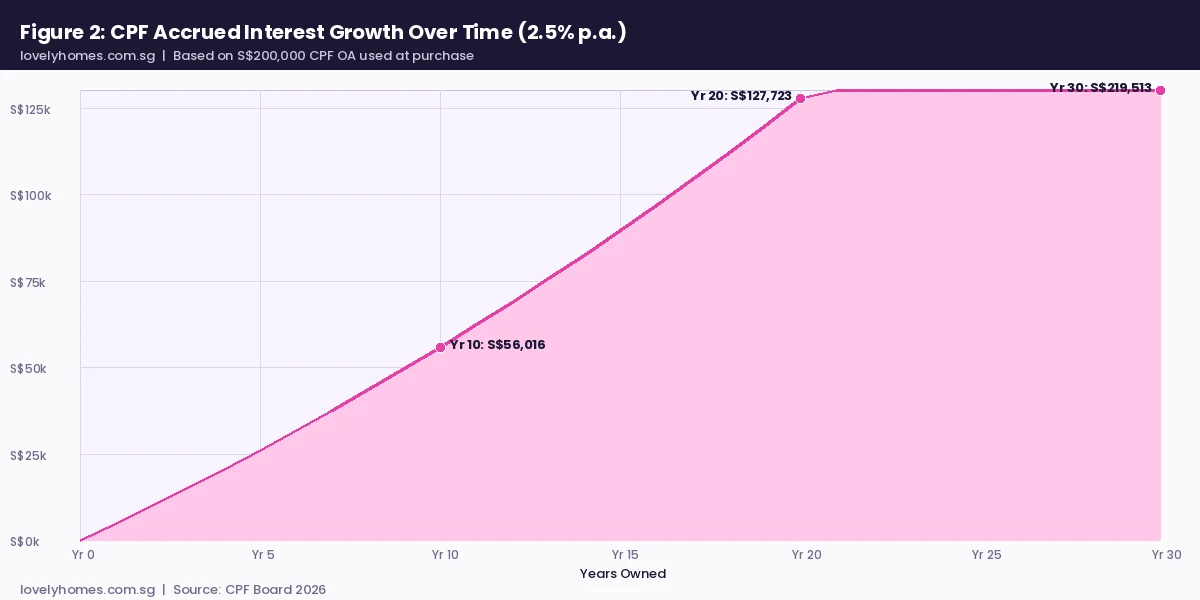

The chart below illustrates how dramatically accrued interest grows on a S$200,000 CPF OA withdrawal over a 30-year period.

At Year 10 the accrued interest on S$200,000 stands at roughly S$55,940. By Year 20 it reaches S$128,010. At Year 30 it totals S$228,370 — meaning your CPF refund obligation would be S$428,370 on a S$200,000 withdrawal, with no additional cash actually deployed. The implication for long-hold strategies is significant: if your property has not appreciated proportionally, the CPF refund eats deeply into net proceeds. The critical counter-point is that the same accrual rate (2.5%) applies to CPF savings sitting in the OA, so if the money were not in property, it would have grown in CPF anyway — this is why CPF Board frames accrued interest as “opportunity cost”, not a penalty.

What CPF Can and Cannot Be Used For

CPF OA can be applied to the following property-related payments: the initial deposit or down payment, Buyer’s Stamp Duty (BSD), HDB resale levy (where applicable), HDB or bank monthly loan instalments, and HDB or private conveyancing legal fees. Critically, CPF cannot be used for Additional Buyer’s Stamp Duty (ABSD), Seller’s Stamp Duty (SSD), renovation costs, or property tax. ABSD in particular must be paid in cash, which is why it represents such a significant liquidity hurdle for investors buying a second or third property.

CPF After Age 55 — the Retirement Sum Constraint

Once you turn 55, CPF rules introduce an additional layer. Your OA and Special Account savings are merged into a Retirement Account, and you are required to set aside either the Basic Retirement Sum (BRS) or the Full Retirement Sum (FRS) — the former if you pledge your property, the latter otherwise — before any CPF funds can be withdrawn for housing purposes. For 2026, CPF Board has set FRS at S$213,000 and BRS at S$106,500. If your CPF savings fall below the relevant sum after these deductions, no further CPF can be directed to housing. This is not an obscure rule for retirees: it increasingly affects buyers in their mid-to-late 50s who are upgrading or downsizing.

Short-Lease Properties and the Prorated Limit

Singapore’s leasehold property market includes many older HDB blocks and private developments whose remaining leases are declining. CPF Board applies a prorated Withdrawal Limit to these properties, calculated as: Remaining lease at drawdown end ÷ 95 × Valuation Limit. Properties with fewer than 20 years’ remaining lease at the point when the youngest buyer turns 95 cannot use CPF at all. This rule was tightened in 2019 and has significantly affected the resale liquidity of older leasehold stock — a buyer unable to use CPF faces a substantially all-cash transaction, compressing their buyer pool and, therefore, the eventual resale price.

Summary Table — CPF Usage at a Glance

| Scenario | Can Use CPF? | Limit | Notes |

|---|---|---|---|

| HDB (HDB loan) | Yes — no VL cap | Full purchase price + fees | Lease must cover buyer to 95 |

| HDB (bank loan) | Yes — up to VL | Lower of price or valuation | 120% VL if BRS set aside (age 55+) |

| Private condo | Yes — up to VL | Lower of price or valuation | BRS must be set aside at 55 |

| Short-lease (20–59 yr) | Yes — prorated | Lease ÷ 95 × VL | Both buyer and CPF Board must agree |

| Lease < 20 years | No | N/A | Cash-only transaction |

| ABSD payment | No | N/A | Must be paid in cash |

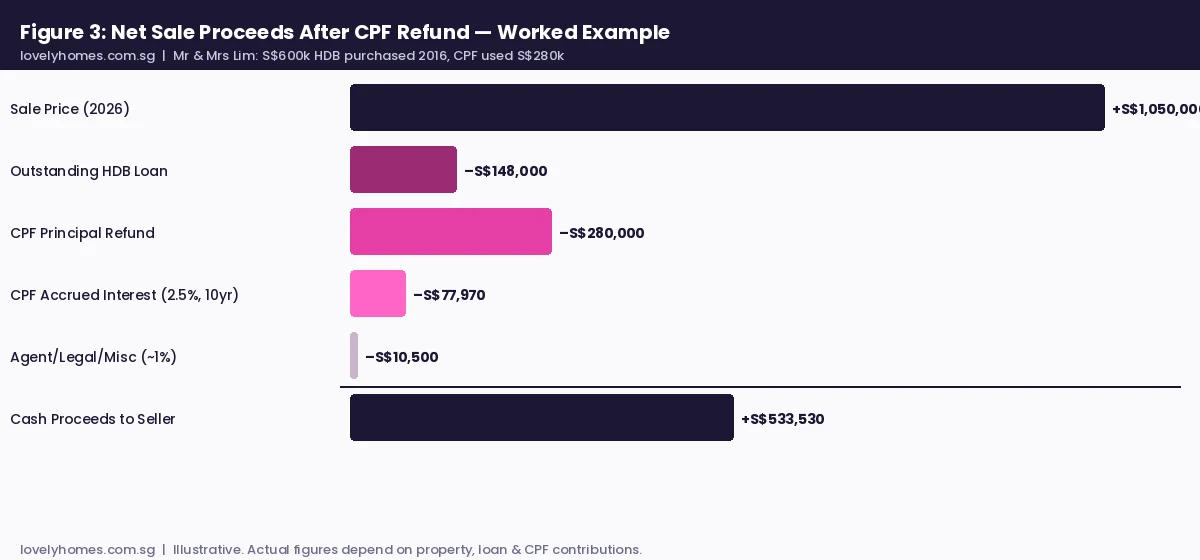

Worked Example: The Lim Family

Mr and Mrs Lim, both Singapore Citizens aged 42 and 40, purchased a four-room HDB flat in Ang Mo Kio in 2016 for S$600,000 using a HDB concessionary loan. Here is how their CPF story unfolds over a decade:

At purchase (2016): They paid a 10% down payment of S$60,000 from CPF OA. The HDB loan covered S$540,000. Over the subsequent 10 years they serviced monthly instalments of approximately S$1,850 on a 25-year loan. By 2026, cumulative CPF OA used totals approximately S$280,000 (including down payment and all monthly payments). Their outstanding loan balance has fallen to about S$148,000.

Accrued interest calculation: On S$280,000 withdrawn progressively over 10 years at 2.5% p.a. compounded, the accrued interest by 2026 is approximately S$77,970. This means the total CPF refund obligation at sale is S$357,970.

At sale (2026, S$1,050,000): After settling the outstanding loan (S$148,000), refunding CPF (S$357,970), and covering agent and legal fees (~S$10,500), the Lims receive approximately S$533,530 in cash. The CPF refund — S$357,970 — goes back into their individual CPF OA accounts, replenishing their CPF balances for the next home purchase. They do not lose the money; it returns to CPF rather than to their bank accounts. If they are upgrading to a private condo, they can immediately redeploy those OA funds towards the new purchase.

Why This Matters for Your Housing Plan

The CPF accrued interest mechanism has several practical implications that every property owner in Singapore should understand. First, the longer you hold a property, the larger the accrued interest obligation — but if the property price has grown proportionally, the proceeds still leave you ahead. The risk arises when appreciation is modest and the accrued interest consumes a disproportionate share of the gain. Second, because the CPF refund goes back into CPF rather than into your bank account, upgraders may find their cash shortfall for the next purchase is larger than they anticipated — even if their net wealth on paper is comfortable. Planning the cash component of any upgrade requires careful modelling of the refund, not just the headline sale price. Third, for investors buying second properties, the ABSD must be fully cash-funded, and the CPF cannot bridge this gap — meaning the true cash requirement for an investment purchase is substantially higher than for an owner-occupier purchase.

What Might Change

CPF housing rules are reviewed periodically by the Ministry of Manpower and CPF Board, typically in tandem with broader housing policy adjustments. The retirement sum thresholds — BRS and FRS — are raised each year in line with long-run wage growth, which will progressively constrain the CPF available for housing among those aged 55 and above. The government has also signalled ongoing review of lease-decay rules as an increasing share of Singapore’s HDB stock approaches the 40-to-60-year mark. Owners of older leasehold properties should monitor CPF Board announcements closely, as a further tightening of prorated limits could affect their resale marketability. For now, the core framework — OA for housing, accrued interest at 2.5%, Valuation Limit for private property — is expected to remain stable through 2027.

Frequently Asked Questions

Can I use CPF to pay ABSD on my second property?

No. Additional Buyer’s Stamp Duty must be paid entirely in cash. Only Buyer’s Stamp Duty (BSD) on residential property qualifies for CPF OA payment. Given that ABSD on a second property for Singapore Citizens is 20% of the purchase price, this represents a very substantial cash commitment — for example, S$280,000 in ABSD on a S$1.4 million condo.

What happens to my CPF if I sell my property at a loss?

The CPF refund obligation — principal plus accrued interest — must still be met in full, regardless of whether you sell at a profit or a loss. If the sale proceeds are insufficient to cover both the outstanding mortgage and the CPF refund, the shortfall must be made up from your other cash resources. You cannot partially refund CPF. This is a risk for properties that have depreciated or carry large mortgages, and it is one reason CPF Board and MAS recommend buyers not over-leverage.

Can I use my spouse’s CPF OA for our property?

Yes, provided both of you are listed as co-owners of the property. Both co-owners’ CPF OA balances can be used for the same property. Each co-owner’s CPF usage is tracked individually, and at sale, each person’s CPF refund (principal plus their accrued interest) is returned to their own CPF account respectively. This arrangement is common for joint HDB purchases and joint private property purchases.

I am 58 years old. Can I still use CPF for a new property?

Yes, but the retirement sum constraint applies. You must have set aside the Full Retirement Sum (FRS, S$213,000 for 2026) in your CPF Retirement Account, or the Basic Retirement Sum (BRS, S$106,500) if you pledge the property. Only OA savings above the applicable sum can be used for housing. Additionally, if you are buying a shorter-lease property, the prorated limit may further reduce how much CPF you can deploy.

Does the CPF refund go back into my OA immediately after I sell?

Yes. The CPF refund from a property sale — principal plus accrued interest — is credited back to your CPF OA (or Retirement Account if you are past 55) within a few business days of the completion of sale. This replenished OA balance can then be used for a subsequent property purchase without delay, which is why upgraders find that their CPF position resets effectively between transactions.

Can CPF be used to pay for renovation?

No. CPF OA funds cannot be used for renovation, furnishing, or fitting out — even though these costs can be substantial (S$40,000 to S$100,000 for a full HDB renovation, and more for private property). Renovation loans from banks are a separate product, and financing is typically at 3.5% to 5.5% p.a. with a 5-year tenor. Always factor renovation costs as a separate cash or loan component when planning your property budget.

Related Articles

- ABSD Singapore 2026 — Complete Guide to Additional Buyer’s Stamp Duty

- Stamp Duty Calculator Singapore 2026: BSD and ABSD for Every Buyer Type

- HDB Minimum Occupation Period (MOP) Singapore 2026: Standard, Plus and Prime Rules

- Singapore Property Checklist for First-Time Buyers 2026

- Private Condo Buying Process Singapore 2026: Complete Step-by-Step Guide

- Home Insurance Singapore 2026: Fire Insurance, Contents Cover and HPP Explained

Disclaimer: This article is for general informational purposes only and does not constitute financial, legal, or CPF advice. CPF withdrawal rules, retirement sum thresholds, and housing schemes are updated periodically by CPF Board and the Ministry of Manpower. Always verify current figures directly at cpf.gov.sg, consult your HDB Branch or bank mortgage specialist, and seek advice from a licensed financial adviser before making property financing decisions.

0 Comments