Singapore Private Property Buying Guide 2026: Eligibility, ABSD, Financing and Step-by-Step Process

⚡ Quick Answer: Private Property in Singapore 2026

- Who can buy: Singapore Citizens (SC) and Permanent Residents (PR) may buy most non-landed private property freely; foreigners are restricted to non-landed condos and Sentosa Cove landed (with approval).

- ABSD: SC buying their first property pay 0% Additional Buyer’s Stamp Duty; a second property incurs 20%; foreigners pay 60% on any purchase.

- BSD: Buyer’s Stamp Duty applies to all buyers on a progressive rate schedule starting at 1% — see our full Stamp Duty Calculator Guide.

- Financing: Bank loans for private property are subject to a 55% Total Debt Servicing Ratio (TDSR); Loan-to-Value (LTV) limits apply (75% for 1st loan, 45% for 2nd).

- No MSR: The Mortgage Servicing Ratio does not apply to private property — only to HDB flats and Executive Condos.

- EC eligibility: Executive Condos (ECs) require both applicants to be SC and a household income of ≤ S$16,000 per month.

- Completion timeline: A typical private property purchase takes 10–16 weeks from Option to Purchase (OTP) to key collection.

- No HDB loan: Private property buyers must use a bank loan — HDB concessionary loans are available only for HDB flats.

What Is Private Property in Singapore?

Private property in Singapore refers to residential real estate that is not built or sold by the Housing & Development Board (HDB). It encompasses a broad range of property types — from compact studio condominiums in the Outside Central Region (OCR) to bungalows in Good Class Bungalow (GCB) areas and shophouses in the city core. Unlike HDB flats, private property is bought and sold on the open market, is not subject to the HDB Minimum Occupation Period (MOP), and can generally be rented out freely.

The Urban Redevelopment Authority (URA) regulates private residential development and maintains Singapore’s Master Plan, which governs land use and zoning. The Inland Revenue Authority of Singapore (IRAS) collects Buyer’s Stamp Duty (BSD), Additional Buyer’s Stamp Duty (ABSD), and annual property tax on private property. The Singapore Land Authority (SLA) maintains the land-title register and approves certain restricted purchases by Permanent Residents and foreigners.

Understanding the full picture of eligibility, costs, and process before committing to a purchase is essential — particularly given that stamp duties alone can add tens to hundreds of thousands of dollars to the acquisition cost depending on the buyer’s profile.

Types of Private Property in Singapore

Singapore’s private property market covers several distinct asset classes, each with its own eligibility rules, price range, and investment characteristics.

Non-Landed Condominiums and Apartments

Condominiums (condos) are the most widely traded form of private residential property in Singapore. A condominium development typically offers shared facilities — swimming pools, gyms, function rooms, and 24-hour security — and is governed by a management corporation (MCST). Any SC, PR, or foreigner may purchase a non-landed private residential unit without restriction, subject to applicable stamp duties. Apartments without condo facilities follow the same rules.

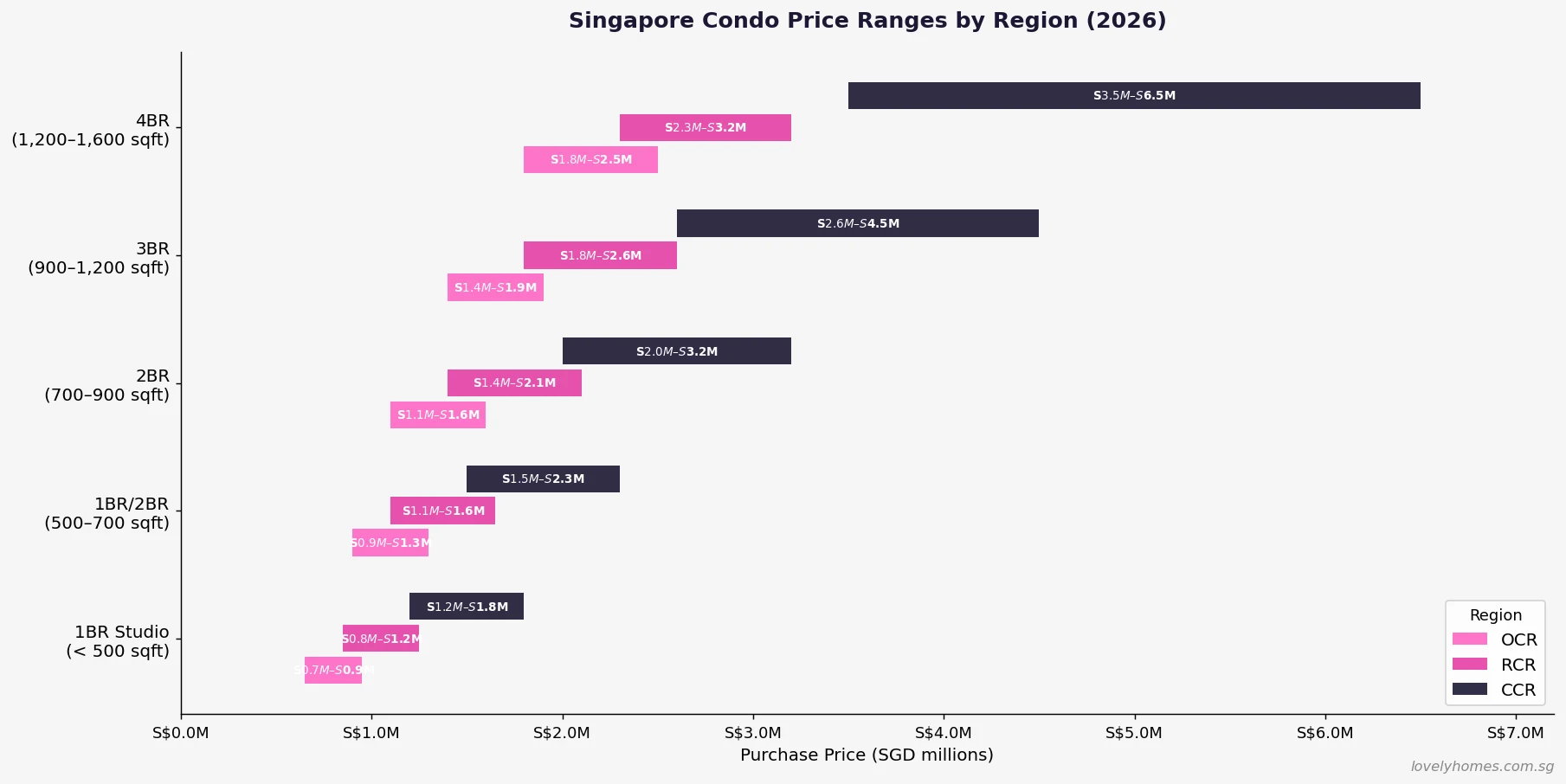

Prices range from roughly S$800,000 for a small studio in the OCR to well over S$10 million for a prime penthouse in the Core Central Region (CCR). As at mid-2026, OCR condos averaged around S$1,800–S$2,100 psf while CCR prime units commanded S$3,500–S$6,000 psf, according to URA transaction data.

Executive Condominiums (ECs)

ECs occupy a hybrid position between HDB and fully private housing. Developed by private developers on government land sold via the GLS (Government Land Sales) programme, ECs are HDB-subsidised at the point of sale to eligible buyers. They become fully privatised after 10 years, at which point they may be sold to foreigners.

To buy a new EC directly from a developer, both applicants must be SC and the combined household income must not exceed S$16,000 per month. A five-year MOP applies before the EC can be rented out or sold on the open market. After five years, it may be sold to SC or PR buyers; after 10 years, to any buyer including foreigners.

Landed Property

Landed homes — detached bungalows, semi-detached houses, and terrace houses — carry significant prestige in Singapore’s land-scarce market. SC may purchase any landed residential property without restriction. PRs, however, require approval from the SLA under the Residential Property Act, and approvals are rarely granted outside of the Sentosa Cove enclave. Foreigners are generally ineligible to purchase landed residential property, again with the exception of Sentosa Cove where Ministerial approval is required.

Entry prices for landed property start around S$2–3 million for a terrace in a non-mature estate and extend to S$20–50 million and beyond for a GCB in Districts 10, 11, or 21.

Shophouses and Commercial Properties

Conservation shophouses and commercial properties are not subject to ABSD — only BSD applies. This makes them attractive to investors who have already exhausted their residential ABSD concessions. Shophouses have been highly sought after as heritage assets, combining commercial ground-floor use with residential upper floors where permitted. Prices typically begin at S$3 million and can exceed S$20 million for prime Chinatown or Boat Quay conservation rows.

Eligibility to Buy Private Property

Singapore Citizens (SC)

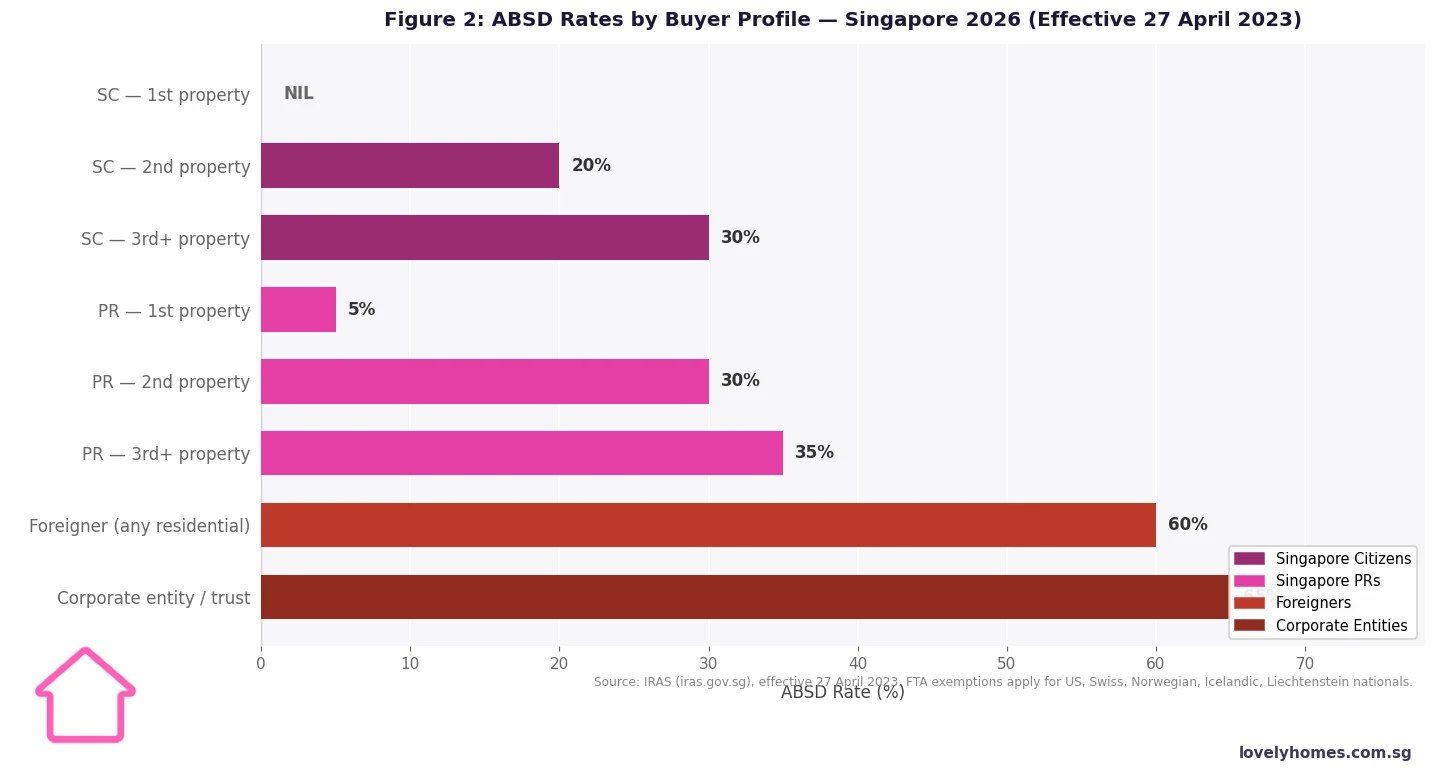

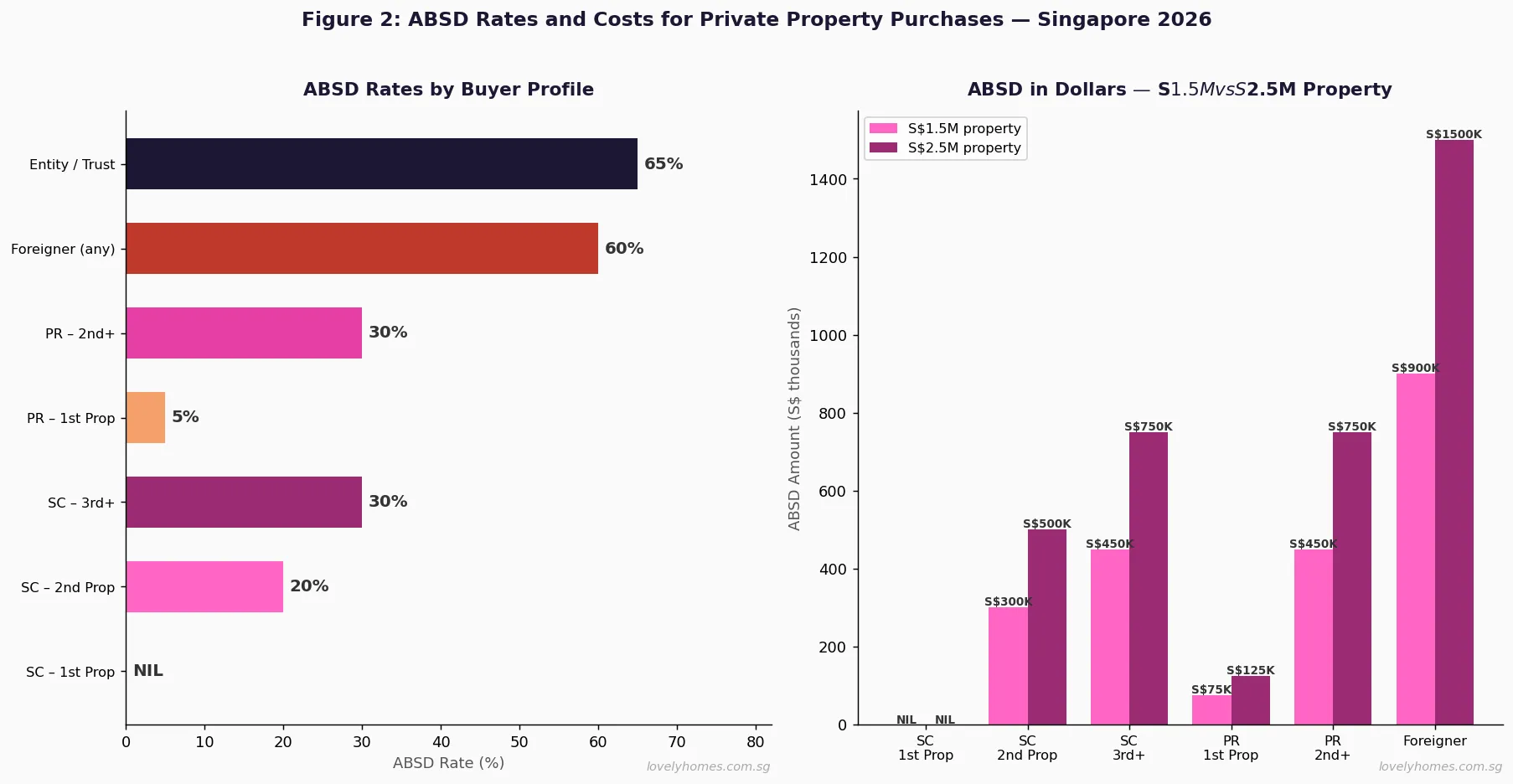

SC face no eligibility restrictions on any category of private residential property. They may purchase non-landed condos, ECs (subject to income ceiling and partner-SC requirement), and landed property freely. ABSD on a first property is 0%, making the first purchase the most cost-efficient for SC buyers. A second property attracts 20% ABSD; a third or subsequent property attracts 30%.

Singapore Permanent Residents (PR)

PRs are treated similarly to SC for non-landed private residential purchases — they may buy without restriction beyond ABSD. However, the ABSD rates differ: 5% on a first property and 30% on a second and subsequent property. PRs cannot purchase new EC units at launch but may buy EC units on the resale market once the five-year MOP has passed. Landed property requires SLA approval.

Foreigners

Foreigners — those who are neither SC nor PR — may purchase non-landed private residential property (condos, apartments) and, with Ministerial approval, Sentosa Cove landed units. They are ineligible for new EC purchases and resale ECs within the first 10 years. The ABSD rate for any foreigner purchasing any residential property is 60%, regardless of how many properties they hold.

Entities and Trusts

Companies and trusts that purchase residential property face the highest ABSD rate of 65%. This rate was introduced to prevent institutional investors from using corporate structures to avoid buyer-profile ABSD tiering. The only exceptions are certain housing developers who may remit ABSD against a development bond.

Financing a Private Property Purchase

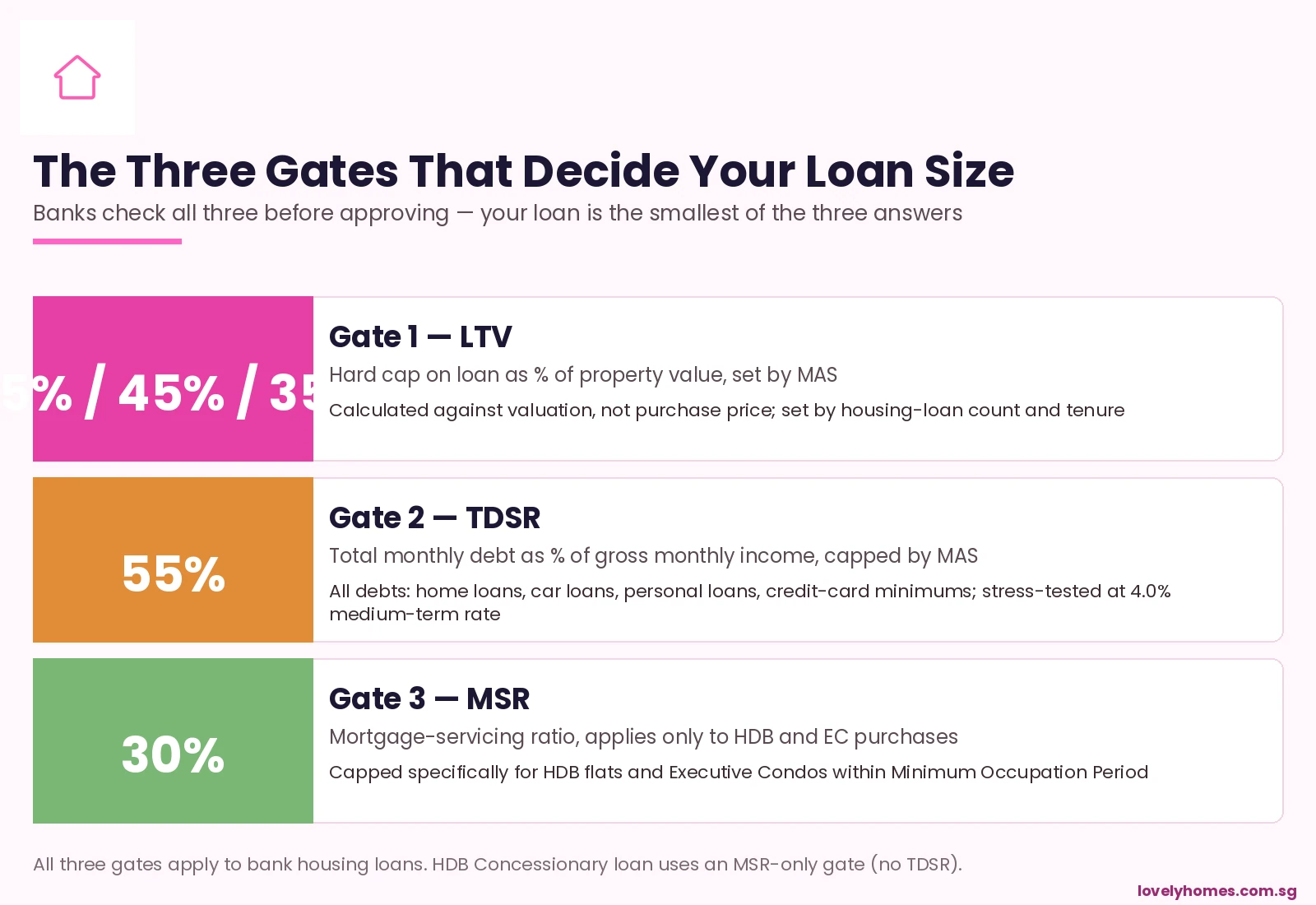

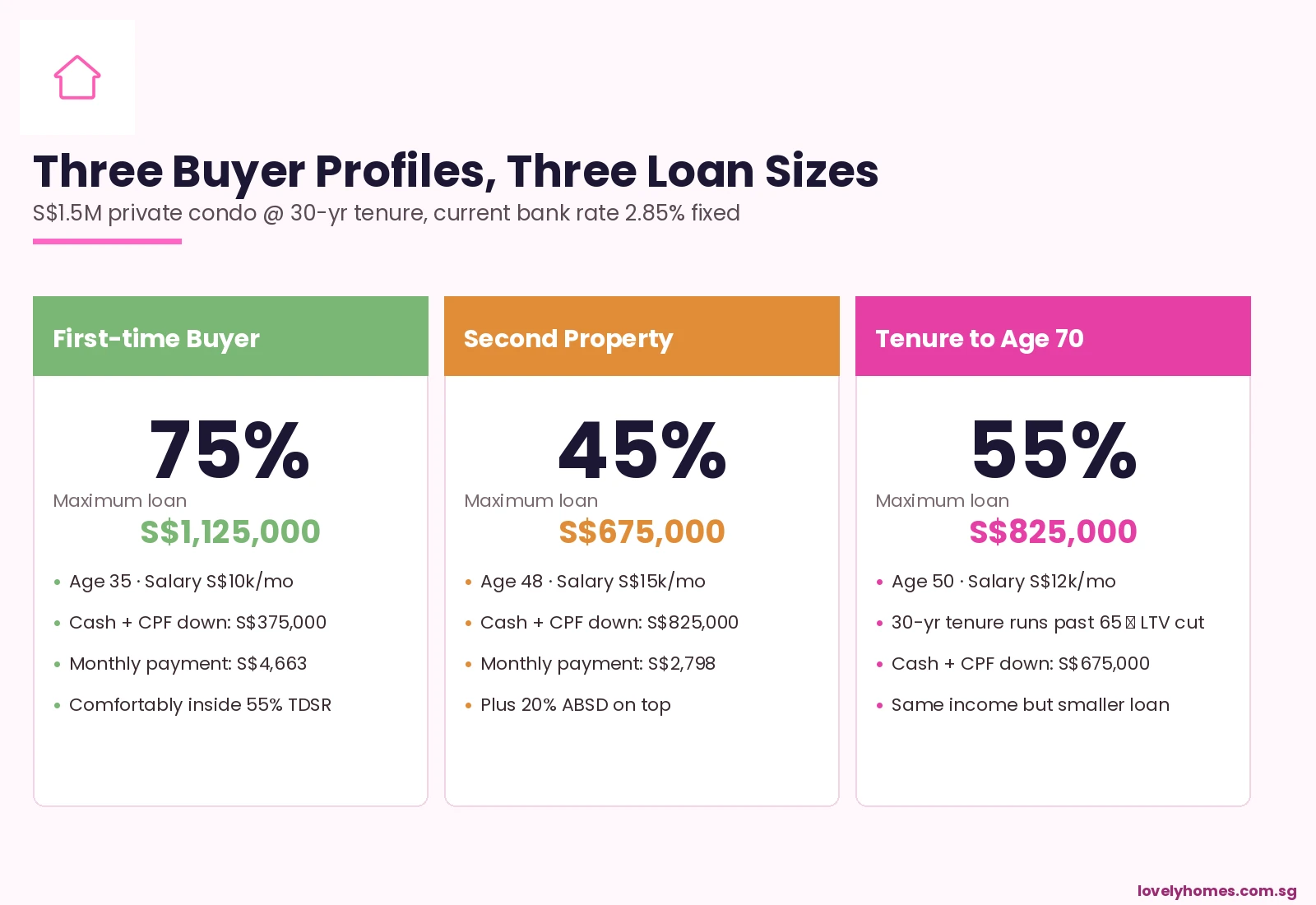

Loan-to-Value (LTV) Limits

The LTV ratio caps how much a bank can lend against the property’s value. For a borrower with no outstanding housing loans, the maximum LTV is 75%, meaning a minimum 25% downpayment is required — of which at least 5% must be cash (the remaining 20% may come from CPF Ordinary Account savings). A borrower with one existing housing loan sees the LTV cap fall to 45%, with at least 25% in cash. Two or more existing housing loans reduce the LTV to 35%.

Total Debt Servicing Ratio (TDSR)

The TDSR framework, administered by the Monetary Authority of Singapore (MAS), limits a borrower’s total monthly debt obligations to 55% of gross monthly income. All existing loan repayments — car loans, student loans, credit card minimum payments, and any other housing loans — are factored into the calculation alongside the new mortgage. For investment properties, rental income may be partially used to offset TDSR (typically 30% of declared rental income).

Unlike HDB purchases, private property purchases are not subject to the Mortgage Servicing Ratio (MSR). The MSR — which caps repayments at 30% of gross monthly income — applies exclusively to HDB and EC loans.

Interest Rates and Loan Tenure

Bank loans for private property in Singapore are typically priced at SORA (Singapore Overnight Rate Average) plus a spread, or offered as fixed-rate packages for 2–3 years. As at mid-2026, floating-rate mortgages hovered around 2.1–2.6% and fixed-rate packages at 2.4–3.0% depending on tenure and lender. Maximum loan tenure is 30 years for private property (or up to age 65, whichever is shorter for certain lenders).

Stamp Duties: BSD and ABSD

Two stamp duties apply to all private property purchases: Buyer’s Stamp Duty (BSD) and — for non-first-SC-buyers — Additional Buyer’s Stamp Duty (ABSD). Both are administered by IRAS and must be paid within 14 days of the exercise date or the date of the purchase agreement, whichever is earlier.

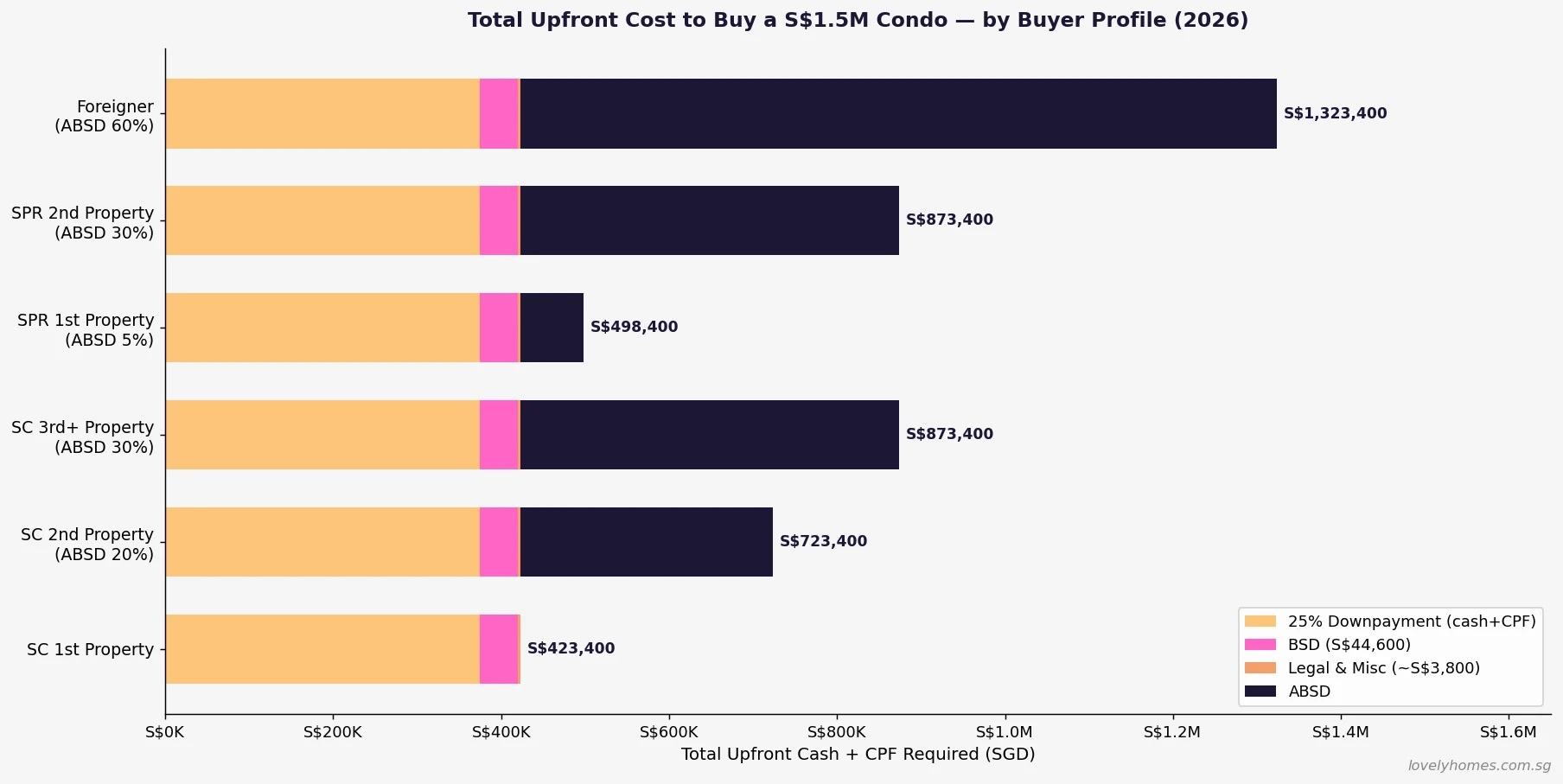

For a detailed breakdown of BSD rates and a worked calculator, see our Singapore Stamp Duty Calculator 2026 and our Complete ABSD Guide 2026. Key data points: BSD on a S$1.5M property is approximately S$44,600; ABSD at 20% for a second SC purchase adds S$300,000, bringing total stamp duties to S$344,600 — a significant upfront cash commitment.

Private Property Purchase Cost Summary

| Cost Item | SC — 1st Property | SC — 2nd Property | Foreigner | Notes |

|---|---|---|---|---|

| BSD (on S$1.5M) | ~S$44,600 | ~S$44,600 | ~S$44,600 | Applies to all buyers; progressive rates |

| ABSD | NIL (0%) | S$300,000 (20%) | S$900,000 (60%) | Cash only — CPF cannot be used for ABSD |

| Minimum cash downpayment | 5% of purchase price | 25% of purchase price | 25% of purchase price | LTV 75% / 45% / 35% by loan count |

| CPF downpayment (OA) | Up to 20% of valuation | Up to 20% of valuation | CPF not applicable | Subject to CPF Valuation Limit |

| Legal fees | ~S$2,500–S$5,000 | ~S$2,500–S$5,000 | ~S$3,000–S$6,000 | Solicitor fees for S&P and mortgage |

| Total upfront funds (1st SC) | ~S$426,100+ | ~S$722,100+ | ~S$1,316,600+ | All-in estimate on S$1.5M property |

Step-by-Step Private Property Buying Process

A typical private property purchase in Singapore takes 10–16 weeks from the granting of an Option to Purchase to completion and key handover. The SLA registers the title and the bank registers its mortgage charge at the conclusion of the process.

Step 1 — Eligibility and ABSD check: Confirm your buyer profile (SC, PR, foreigner), count existing properties for ABSD tier purposes, and verify any outstanding ABSD remission (for example, SC upgraders who sold their HDB within 6 months of buying a private property). Foreigners should confirm the property type is eligible — non-landed condos are unrestricted; landed property is not.

Step 2 — Secure financing (AIP): Approach banks to obtain an Approval In Principle (AIP), which locks in a loan quantum for typically 30 days. Review your TDSR position, existing loan commitments, and CPF balances. An AIP is not a binding commitment but gives sellers confidence and helps you set a realistic budget.

Step 3 — View units and negotiate: Once your budget is set, shortlist properties and arrange viewings. For new launches, attend the developer’s showflat; for resale, engage a solicitor early. Commission structures are typically 1% of the sale price, paid by the seller.

Step 4 — Exercise the OTP: Sellers grant an Option to Purchase (OTP), which is a contractual right to purchase within 21 days. Buyers typically pay a 1% option fee at this stage. Exercising the OTP commits both parties — a further 4% (or 9% for new launches) exercise fee is payable. BSD and ABSD must be calculated from this date for payment purposes.

Step 5 — Sign the Sale & Purchase Agreement and pay stamp duties: BSD and ABSD must be paid to IRAS within 14 days of the exercise date. Both may be paid via IRAS’ stamp duty system online. BSD may be paid from CPF OA; ABSD must be paid in cash.

Step 6 — Mortgage formalisation: The bank conducts a formal valuation and issues a Letter of Offer. Your solicitor reviews the terms, witnesses your signature, and lodges the mortgage with the SLA. Banks will usually disburse the loan in a single tranche at completion for resale properties, or progressively for new launches under the Progressive Payment Scheme (PPS).

Step 7 — Completion and key collection: On the completion date — typically 8–12 weeks after OTP exercise for resale properties — your solicitor settles the balance purchase price (less the option fee and exercise fee already paid), the outstanding BSD/ABSD if not yet paid, and any adjustments for property tax and maintenance. The seller hands over keys and the SLA registers the change of ownership.

Worked Example: SC Couple Buying a Second Property

Mr and Mrs Tan, both Singapore Citizens, own a 4-room HDB resale flat and wish to purchase an OCR condo for investment. They identify a 3-bedroom unit priced at S$1,650,000.

Stamp duties: BSD on S$1,650,000 works out to approximately S$49,600 (payable from CPF OA). ABSD at 20% = S$330,000 — payable entirely in cash.

Financing: With one existing housing loan (HDB), the LTV cap is 45%, meaning a maximum bank loan of S$742,500. Minimum cash downpayment is 25% = S$412,500, of which at least S$82,500 must be in cash (5% of purchase price); the remaining S$330,000 may be funded by CPF OA.

Monthly repayment: S$742,500 loan at 2.50% per annum over 25 years gives approximately S$3,329 per month. Combined household income of S$20,000 per month → TDSR: (S$3,329 + S$2,147 existing HDB repayment) ÷ S$20,000 = 27.4%. Well within the 55% TDSR cap.

Total upfront funds required:

- Cash downpayment: S$82,500 (5% cash minimum)

- ABSD: S$330,000 (cash, cannot use CPF)

- CPF OA used: S$330,000 (20% of S$1.65M from CPF) + S$49,600 (BSD)

- Legal fees: ~S$4,500

- Total cash required: ~S$417,000; total CPF used: ~S$379,600

This example illustrates why second-property purchases — even for SC — require significant liquid cash reserves given the 20% ABSD alone on a S$1.65M purchase equates to S$330,000.

Why Private Property Matters as an Asset Class in Singapore

Singapore’s private residential market has delivered consistent long-term capital appreciation driven by constrained land supply, strong demand from both local and permanent resident buyers, and sustained economic growth. URA’s Private Residential Property Price Index (PPI) rose by over 75% from 2010 to mid-2026, significantly outpacing headline CPI over the same period.

Rental yields from private condos — while compressed by rising prices — have recovered since 2022 and averaged 3.0–4.0% gross on OCR units and 2.5–3.2% on CCR units as at mid-2026. Unlike HDB flats, there is no minimum occupation period before private property can be rented out, giving buyers immediate flexibility to generate income.

International comparison is instructive: Hong Kong’s ABSD equivalent (Special Stamp Duty) reaches 30% for non-permanent residents, making Singapore’s policy more punitive for foreigners (60%) but still competitively structured for SC. Australia charges no nationwide ABSD equivalent but states levy surcharge duties of 7–8% on foreign purchases.

What Might Come Next for Private Property Policy

The following represents editorial analysis and speculation — not official government guidance.

With the URA Q2 2026 Flash Estimate showing a +0.5% QoQ rise in the PPI — driven primarily by CCR — and HDB resale prices declining for two consecutive quarters, the market is bifurcating. A partial relaxation of ABSD rates for Singapore PRs buying their first property (currently 5%) is periodically discussed as a mechanism to attract high-net-worth permanent residents, though no policy change has been signalled as at July 2026.

The Government Land Sales (GLS) Confirmed List for 2026 supplies roughly 9,320 new private residential units across 1H and 2H, which should moderate supply constraints. Watch for Q2 2026 full URA data expected around 24 July 2026 for a clearer signal on transaction volumes and price trajectories by segment.

Frequently Asked Questions

Can I use CPF to pay ABSD on a private property purchase?

No. ABSD must be paid entirely in cash and cannot be funded from CPF Ordinary Account savings. Only Buyer’s Stamp Duty (BSD) may be paid using CPF OA funds. For a SC buyer’s second property attracting 20% ABSD, this means having significant liquid cash — S$300,000 in cash on a S$1.5M purchase — available at the time of signing the Sale and Purchase Agreement.

Can a Singapore PR buy a landed house?

PRs who wish to purchase landed residential property in Singapore must obtain approval from the Singapore Land Authority (SLA) under the Residential Property Act. Approvals are granted only in exceptional circumstances — for example, where the PR has made significant economic contributions to Singapore. In practice, the vast majority of PRs who wish to live in a landed home either rent one or wait until they obtain SC. Sentosa Cove is a partial exception where PRs may purchase landed units subject to Ministerial approval.

Is there a Minimum Occupation Period for private condos?

No. Unlike HDB flats and Executive Condos (during their first 5 years), private condominiums and apartments have no MOP. You may sell or rent out a private property at any time after completion. However, a Seller’s Stamp Duty (SSD) applies if you sell within 3 years of purchase — 12% in Year 1, 8% in Year 2, and 4% in Year 3. See our SSD Guide 2026 for details.

How does ABSD remission work for SC upgraders?

SC married couples buying their first private property while still owning an HDB flat must pay 20% ABSD upfront. However, if they sell their HDB flat within 6 months of the private property’s completion (or date of S&P, for resale), IRAS will remit (refund) the ABSD. This 6-month window is strict — missing it means the ABSD is forfeited. For a full walkthrough of this process, see our HDB Upgrader Guide 2026.

What is the difference between freehold and 99-year leasehold private property?

Freehold property means the owner holds the land and building in perpetuity; 99-year leasehold means the owner holds the property from the State for 99 years from the date the lease commenced. In practice, most leasehold property in Singapore does not significantly underperform freehold counterparts until the lease drops below 60–70 years, at which point CPF usage restrictions and bank lending constraints begin to bite. Freehold properties typically command a 10–20% premium over comparable leasehold units in the same area.

Can a foreigner get a Singapore bank mortgage for a private condo?

Yes, foreigners may obtain a mortgage from a Singapore bank for a private condo, subject to the same TDSR (55%) and LTV limits that apply to all buyers. Banks will typically require additional documentation — proof of overseas income, employment pass validity, foreign tax returns — and some lenders offer products specifically packaged for non-resident borrowers. Note that the 60% ABSD means foreigners need enormous cash reserves upfront regardless of financing, limiting the pool of foreign private property buyers to high-net-worth individuals.

Does buying a commercial property or shophouse count as a “property” for ABSD purposes?

No. ABSD is levied only on residential property purchases. Commercial properties — including shophouses zoned for commercial use, industrial units, office space, and retail strata units — do not count towards your ABSD property count and do not incur ABSD themselves. BSD still applies to commercial property at the standard rate. This is why some investors who have exhausted their ABSD concessions on residential property pivot to shophouses or commercial strata as their next investment.

Related Articles on LovelyHomes

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Stamp Duty Calculator 2026: BSD and ABSD Explained

- Singapore Condo Buying Process 2026: Step-by-Step from Offer to Keys

- Singapore HDB Upgrader Guide 2026: Steps, Costs, ABSD Remission and Timing

- Singapore Seller’s Stamp Duty (SSD) Guide 2026

- Singapore New Launch Condo Buying Guide 2026

- Foreigner Buying Property in Singapore 2026: Complete Guide

- Singapore Property Cooling Measures 2026

Disclaimer: This article is for general information only and does not constitute financial, legal, or tax advice. ABSD rates, BSD schedules, LTV limits, and TDSR thresholds are subject to change by the Singapore Government. Always verify current rates with IRAS (iras.gov.sg) and URA (ura.gov.sg). Consult a licensed property agent (CEA registered), conveyancing solicitor, and/or a licensed financial adviser before making any property purchase decision. Property prices, interest rates, and market conditions can change rapidly.