Singapore Executive Condominium Guide 2026: Eligibility, Prices, MOP and Investment Outlook

ℹ Quick Answer: Singapore Executive Condominiums 2026

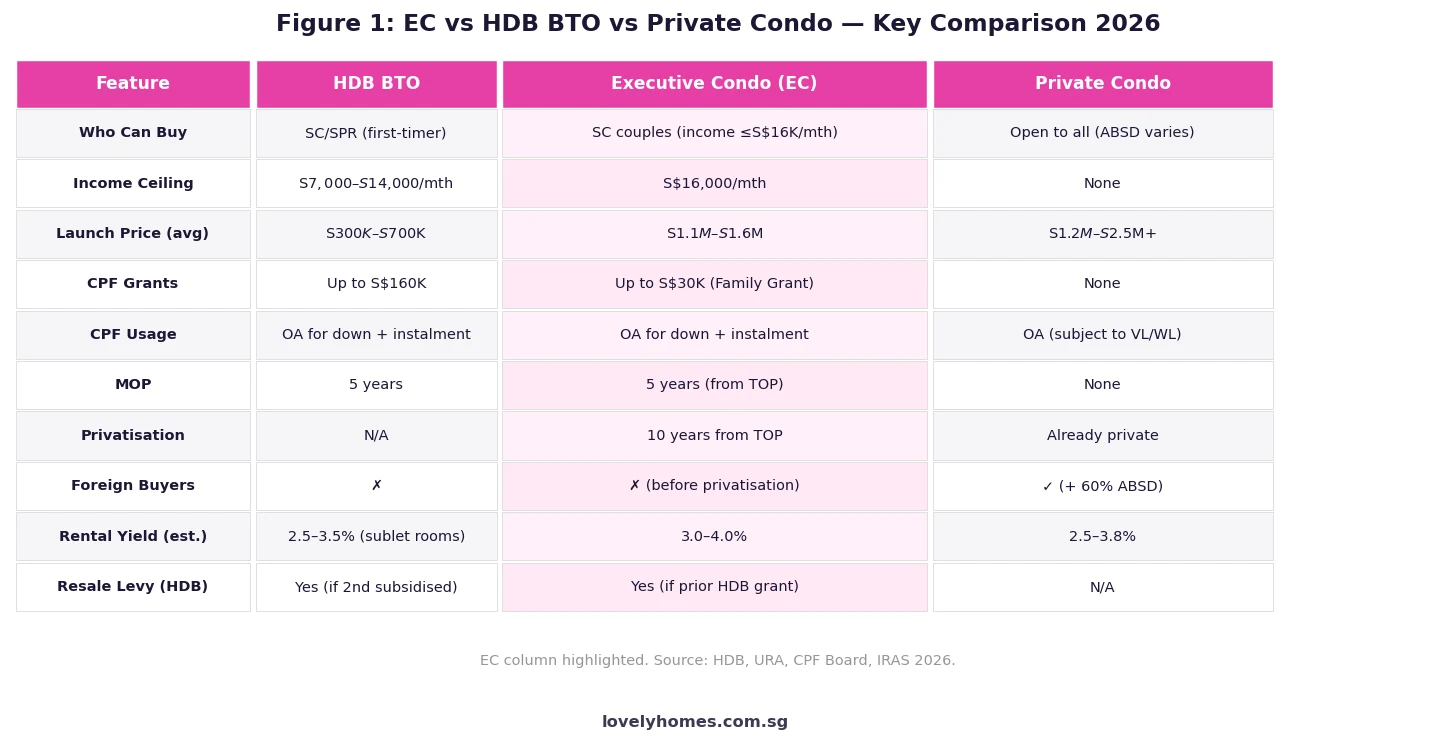

- What is an EC? An Executive Condominium (EC) is a hybrid housing type developed by private developers but sold under HDB eligibility rules. It offers full condo facilities at a subsidised price relative to purely private developments in the same area.

- Who can buy a new EC? Singapore Citizen households (at least one SC) with a monthly household income of S$16,000 or below, buying as a family nucleus (at least two applicants forming a family). Singles cannot buy new ECs.

- Launch prices 2026: New ECs are typically priced S$1.1M–S$1.6M for a 3-bedroom unit, depending on location and developer.

- MOP: 5-year Minimum Occupation Period (MOP) from TOP date. During MOP, you cannot sell, sublet the entire unit, or purchase private residential property in Singapore.

- Privatisation: ECs are privatised 10 years from the date of TOP. Once privatised, the unit is treated as private property and foreigners may purchase in the resale market (subject to 60% ABSD).

- CPF grant available: Family Grant of up to S$30,000 for eligible SC+SC couples (S$20,000 for SC+SPR).

- ABSD on EC purchase: Singapore Citizens buying an EC as their first property are exempt from ABSD. Second-time SC buyers pay 20% ABSD on the EC purchase price.

- Resale levy: If you previously bought a subsidised HDB flat (or prior EC), a resale levy of S$55,000 (for ECs) applies when you buy your next HDB flat or EC from HDB.

What Is an Executive Condominium in Singapore?

The Executive Condominium scheme was introduced by HDB in 1995 as a “sandwich class” housing option — targeting households that earn too much for standard BTO flats but still find private condominiums financially out of reach. Legally, an EC is a private residential development built and sold by a private developer who acquires the land through a Government Land Sales (GLS) tender specifically designated for EC use. Despite the private developer involvement, the initial sale is governed by HDB’s rules on eligibility, income ceilings, and holding conditions.

The EC structure creates a distinctive investment trajectory. At launch, ECs are priced at a discount to nearby private condominiums — typically 15–25% below a comparable private development. After five years (the MOP), the unit may be sold on the open market to Singapore Citizens and Permanent Residents. After ten years from TOP, the EC is fully privatised and can be purchased by foreigners subject to the standard 60% Additional Buyer’s Stamp Duty (ABSD).

EC Eligibility: Who Qualifies to Buy a New Launch EC?

Eligibility for a new EC purchase (from the developer) is tightly defined by HDB. As of 2026, the core requirements are:

Citizenship and Family Nucleus

At least one applicant must be a Singapore Citizen. The buyers must form a recognised family nucleus, which includes:

- Married or intending-to-marry SC+SC or SC+SPR couples.

- SC parent(s) with children (orphans and seniors may apply under the joint singles or senior schemes for HDB flats, but not for ECs).

- Unmarried SC individuals aged 35 and above cannot buy a new EC. They may buy in the resale market after MOP.

Income Ceiling

The combined gross monthly household income of all buyers and occupiers must not exceed S$16,000 per month. This ceiling was raised from S$14,000 in the 2023 Budget, bringing an additional segment of dual-income couples within EC reach. Income is assessed as an average of the 12 months prior to application.

Property Ownership Bar

Neither the applicant nor any listed occupier may own or have disposed of any private residential property (locally or overseas) within 30 months before the EC application date. If you currently own an HDB flat, you must dispose of it within six months of the EC’s key collection date.

First-Timer vs Second-Timer

First-timer applicants enjoy priority balloting and are eligible for the Family Grant. Second-timers (who previously bought a subsidised HDB flat or an EC) pay a resale levy and have lower ballot priority. The resale levy for ECs is S$55,000 if the prior subsidised unit was a 5-room flat or larger, stepping down to S$15,000 for a 2-room or smaller prior flat.

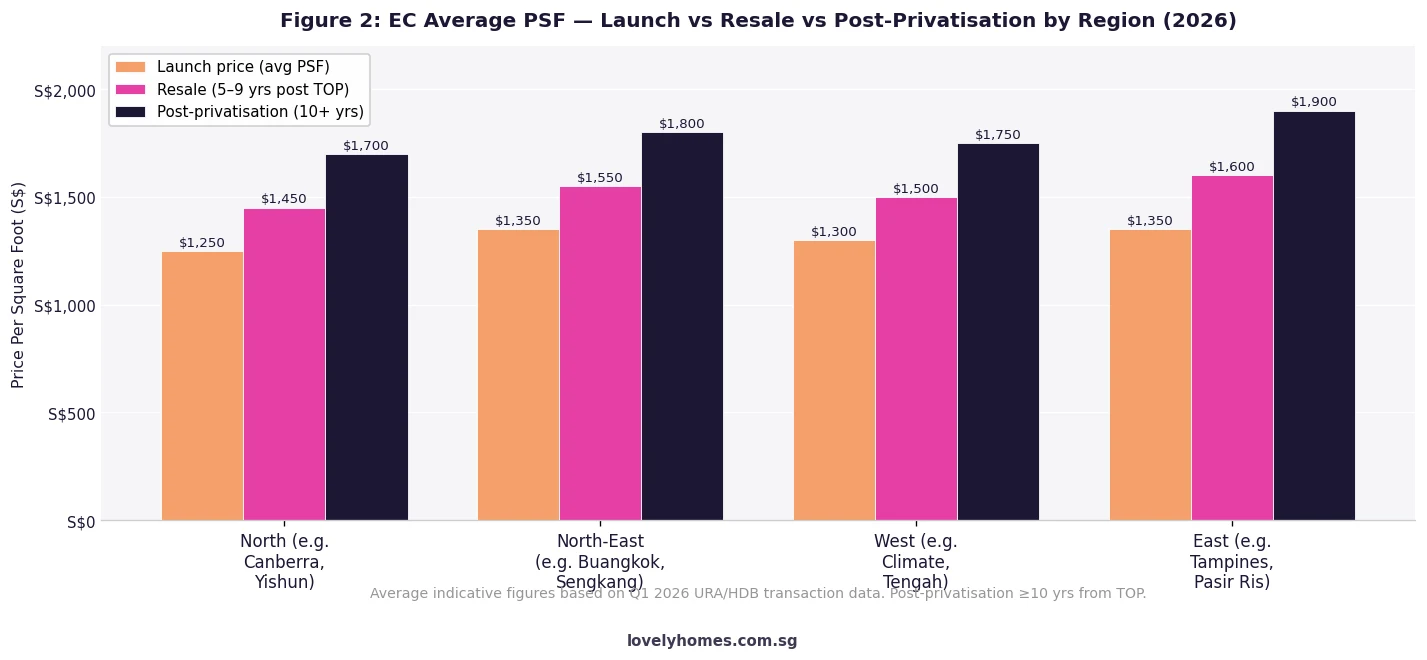

EC Pricing: How Developers Set Launch Prices

EC land parcels are tendered through the GLS Confirmed or Reserve List. Developers bid for the right to develop the site and must sell to eligible buyers under HDB’s framework. This GLS land cost is typically lower than for fully private residential sites of comparable attributes — reflecting the eligibility restrictions on the first 10 years of ownership.

In practice, 2026 EC launch prices range from approximately:

| Region | Typical Launch PSF | Typical 3BR Price | Typical 4BR Price |

|---|---|---|---|

| North (Yishun, Sembawang) | S$1,200–S$1,300 | S$1.1M–S$1.25M | S$1.35M–S$1.55M |

| North-East (Sengkang, Punggol) | S$1,300–S$1,450 | S$1.2M–S$1.4M | S$1.5M–S$1.65M |

| West (Tengah, Jurong) | S$1,250–S$1,400 | S$1.15M–S$1.3M | S$1.4M–S$1.6M |

| East (Tampines, Pasir Ris) | S$1,300–S$1,500 | S$1.25M–S$1.45M | S$1.55M–S$1.75M |

These prices are 15–25% below the equivalent private condominium launch in the same neighbourhood, reflecting the initial eligibility constraints. The discount narrows in the resale market once MOP is passed, and largely disappears at the 10-year privatisation mark.

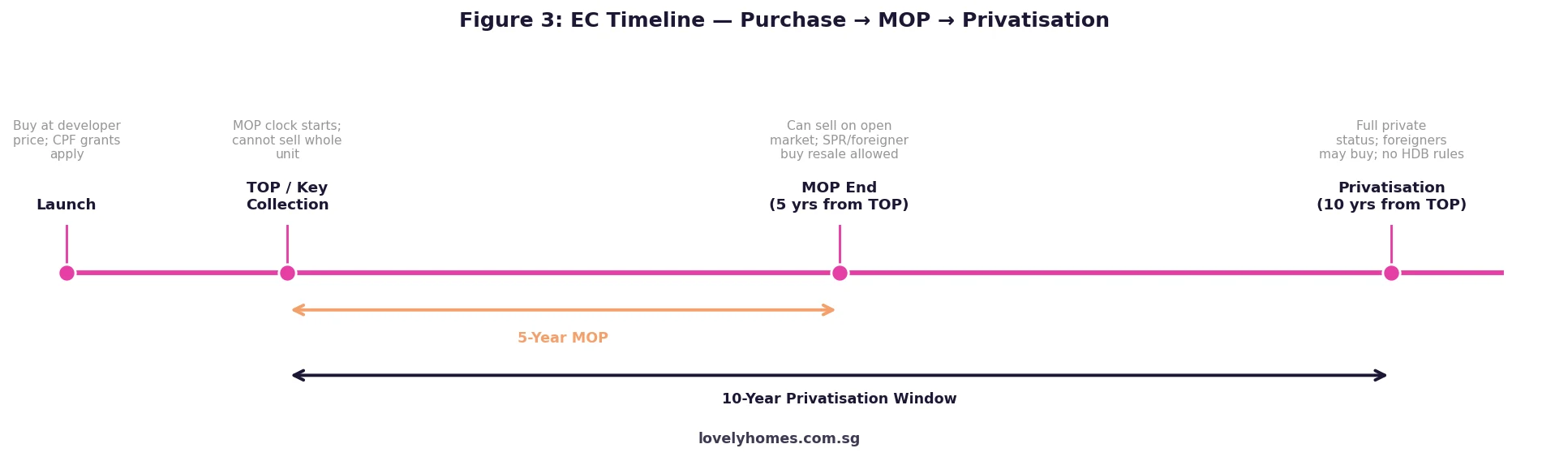

The MOP, Privatisation, and Ownership Timeline

Understanding the EC ownership timeline is essential to investment planning. The two critical milestones are the 5-year MOP and the 10-year privatisation:

During MOP (Year 0 to Year 5 from TOP)

- Cannot sell the whole unit (resale prohibited).

- Cannot sublet the entire unit (subletting individual rooms is permitted with HDB’s approval).

- SC buyers cannot purchase a new private residential property in Singapore.

- Can carry out renovations, refinance the mortgage, and apply to HDB for subletting of spare rooms.

Post-MOP (Year 5 to Year 10 from TOP)

- Can sell to Singapore Citizens and Permanent Residents (but not foreigners yet).

- Can sublet the entire unit without HDB approval.

- SC owners can purchase a private property (subject to ABSD for the second property).

- Resale prices typically reflect a premium of 10–20% above the launch price in real terms, adjusted for market conditions.

Post-Privatisation (Year 10+ from TOP)

- The EC becomes a fully private property. Foreigners may purchase subject to the prevailing 60% ABSD.

- CPF housing grant rules no longer apply; no HDB resale levy is triggered for future transactions.

- No minimum occupation period on subsequent resale or rental.

- The unit is classified as a private property for all ABSD, stamp duty, and CPF usage purposes going forward.

ABSD, Stamp Duty and Financing for ECs

The stamp duty treatment for ECs mirrors that of private residential properties, not HDB flats:

| Item | EC (New Launch) | Notes |

|---|---|---|

| Buyer’s Stamp Duty (BSD) | Up to 6% on first S$1M; 5% on next S$500K; 4% on next S$500K etc. | Same as private residential |

| ABSD (1st property, SC) | 0% | SC buying EC as first property: no ABSD |

| ABSD (2nd property, SC) | 20% | Applies if you currently own another residential property |

| ABSD (1st property, SPR) | 5% | SPR co-applicant on first property |

| Loan-to-Value (LTV) | Up to 75% for bank loans | HDB loans NOT available for EC purchases |

| Minimum Cash Down | 5% (if no outstanding housing loan); 25% if existing loan | CPF OA can cover remainder of downpayment |

| TDSR | 55% of gross monthly income | No MSR for EC (unlike HDB) |

An important distinction: HDB concessionary loans are not available for EC purchases. All EC buyers must use a bank loan, which means variable or fixed rates determined by the market (pegged to SORA or a fixed period rate), rather than the HDB’s fixed 2.6% per annum rate. This creates greater monthly instalment volatility compared with HDB flat buyers.

Worked Example: Buying an EC in Tengah 2026

📝 Case Study: The Lim Family, SC + SC, Monthly Income S$12,500

Profile: Mr and Mrs Lim, both Singapore Citizens, both first-timers. Monthly gross household income S$12,500. They are buying a 4-bedroom EC at a Tengah development (West region) at launch.

Purchase price: S$1,450,000 (4-bedroom, approx. 1,380 sqft)

- Family Grant (EC, SC+SC, first-timer): S$30,000.

- Buyer’s Stamp Duty (BSD): On S$1,450,000 → 1%×S$180K + 2%×S$180K + 3%×S$640K + 4%×S$450K = S$1,800 + S$3,600 + S$19,200 + S$18,000 = S$42,600.

- ABSD: S$0 (first property, SC).

- Bank loan (75% LTV): S$1,087,500 → at 3.4% fixed for 2 years, 30-year tenure → monthly instalment approx. S$4,815.

- TDSR check: S$4,815 / S$12,500 = 38.5% ✓ (below 55%).

- Downpayment: 25% = S$362,500 (5% in cash = S$72,500; remainder S$290,000 from CPF OA).

- Family Grant credited to CPF OA: S$30,000 reduces the CPF OA drawdown to S$260,000.

- Estimated total upfront cash outlay: S$72,500 (5% cash down) + S$42,600 (BSD) + S$3,500 (legal fees) = S$118,600 cash.

Investment horizon scenario: If the EC appreciates at a conservative 2% per annum in real terms, at privatisation (10 years from TOP, approximately 2038 for a 2026 TOP unit), the unit would be worth approximately S$1.77M. Net equity (after repaying the CPF principal and accrued interest on S$290K CPF used over 10 years ≈ S$80K) would be in the range of S$580K–S$650K cash, assuming the mortgage is fully refinanced or discharged.

Why ECs Occupy a Unique Niche in Singapore’s Housing Landscape

In most housing markets, public and private housing exist as entirely separate ecosystems. Singapore’s EC scheme is unusual in that it creates a managed transition from subsidised to fully private ownership over a defined 10-year window. This transition serves several policy goals:

Affordability for aspirational households: Dual-income couples earning S$10,000–S$15,000 per month often find themselves above the income ceiling for BTO but priced out of comparable private condominiums. ECs serve this exact demographic. The Family Grant (up to S$30,000) provides a modest subsidy even at these income levels.

Wealth accumulation for the middle class: The typical EC buyer who holds through privatisation has historically benefitted from significant capital appreciation. Industry data suggest ECs launched between 2010 and 2015 that have since privatised trade at 40–70% above their launch price in nominal terms, outperforming many mass-market private condominiums in the same period. The subsidised entry price is the key driver of this outperformance.

Supply discipline through HDB oversight: Because EC land is sold through GLS with designated EC use, the Ministry of National Development (MND) can calibrate EC supply in response to demand from the sandwich-class segment. The 2H 2026 GLS Confirmed List includes one EC site at Tampines Street 95 (approx. 610 units), continuing a steady pipeline that prevents the EC segment from overheating relative to underlying demand.

What Might Come Next: ECs in 2027–2028

The following reflects informed analysis, not confirmed policy.

- Income ceiling review: With the 2023 increase from S$14,000 to S$16,000 still relatively recent, a further revision before 2027 is possible but not widely anticipated. MND has indicated it reviews income ceilings periodically to ensure alignment with wage growth.

- New EC sites in Jurong Lake District: As the JLD masterplan advances, there is industry speculation about EC-designated parcels in the western growth corridor. The JLD White Site (July 2026 GLS launch) focuses on mixed-use development, but adjacent parcels could eventually include EC use if demand from the Jurong-Tengah corridor warrants it.

- Foreigners and privatised ECs: The 60% ABSD on foreigners buying private property (including post-privatisation ECs) is among the highest in the world. While some relief has been discussed in the context of attracting talent, official statements from MAS and MND through mid-2026 suggest no change to ABSD rates is imminent.

Frequently Asked Questions: Executive Condominiums Singapore 2026

Can singles buy an EC in Singapore?

Singles cannot buy a new EC directly from the developer. The EC scheme requires a family nucleus as defined by HDB — typically a married or intending-to-marry couple, or a parent with children. However, a Singapore Citizen aged 35 and above can buy an EC in the resale market (i.e., an EC that has passed its 5-year MOP) under the Joint Singles Scheme (with another SC single) or as a solo buyer if the EC has reached the 10-year privatisation mark and is now a fully private property. In the latter scenario, the purchase is treated as a standard private property transaction.

Do I pay ABSD when I buy an EC if I own an HDB flat?

If you currently own an HDB flat and you buy an EC, you are buying a second residential property. As a Singapore Citizen, you would pay 20% ABSD on the EC purchase price. For a S$1.4M EC, that is S$280,000 in ABSD alone. Many EC buyers avoid this by selling their existing HDB flat before or concurrently with the EC purchase. HDB’s rules require you to dispose of the HDB flat within 6 months of the EC’s key collection; if you can align the sale and purchase, you can potentially bridge the gap with a bridging loan and avoid the ABSD. Planning the timing carefully with your conveyancing solicitor is critical.

What is the difference between an EC MOP and an HDB flat MOP?

Both require a 5-year Minimum Occupation Period during which the whole unit cannot be sold or sublet. The key difference lies in the clock start: for an HDB flat, MOP runs from the date you receive the keys (completion); for an EC, MOP runs from the date of TOP (Temporary Occupation Permit), which is the date the Building and Construction Authority clears the development for occupation. In practice, for ECs bought at launch, MOP begins when you collect the keys, because keys are typically issued at or shortly after TOP. For resale EC purchases post-MOP, there is no additional MOP for the new buyer — only new-launch buyers serve the MOP from TOP.

Can I use my CPF OA to pay for an EC?

Yes. CPF Ordinary Account savings can be used for an EC purchase, subject to the standard Valuation Limit (VL) and Withdrawal Limit (WL) rules applicable to private residential property. The VL is the lower of the purchase price or market valuation, and the WL is 120% of the VL. For most EC purchases, the WL is comfortably above the loan amount, so CPF OA can fund the full downpayment (minus the 5% compulsory cash component) and subsequent monthly instalments. The Family Grant (if applicable) is credited to your CPF OA first and applied as part of this CPF usage.

How does an EC affect my ability to buy a private property during MOP?

During the EC’s MOP, the SC owner cannot buy any additional private residential property in Singapore. This restriction mirrors the HDB flat MOP restriction. Once MOP is over (5 years from TOP), you are free to purchase private property — though doing so while you still own the EC means you will be buying a second property and will be subject to 20% ABSD (for SC buyers). Many EC owners who upgrade to private property after MOP first sell the EC (or wait for the resale transaction to complete) to avoid ABSD on the private purchase, benefitting from the EC’s post-MOP appreciation in the process.

Are there stamp duty differences between buying a new EC and a privatised EC in resale?

Yes, in one important respect. When you buy a new EC from the developer, BSD is computed on the purchase price and ABSD (if applicable) on the purchase price at the relevant rate. When you buy a privatised EC in the resale market (10+ years from TOP), it is treated entirely as a private property: BSD and ABSD rates are identical to any other private condominium. However, there is no seller’s stamp duty (SSD) imposed on the seller of a privatised EC, since SSD only applies within 3 years of purchase. For resale ECs between 5 and 10 years from TOP (post-MOP but pre-privatisation), the same BSD applies to the buyer; foreigners still cannot purchase in this window.

What happens to the Family Grant if I sell the EC before privatisation?

The CPF Housing Grant (Family Grant) received for an EC is returned to your CPF Ordinary Account upon sale, exactly as with an HDB flat sale. The grant principal (without accrued interest) is refunded to CPF. Any remaining cash proceeds above the CPF refund and outstanding bank loan are yours to keep. If you sell within the 5-year MOP, the sale is generally not permitted (resale restriction); selling after MOP but before privatisation triggers CPF refund of the grant at the original quantum. There is no claw-back or penalty from HDB specifically for the grant — the CPF refund mechanism handles the recovery automatically at conveyancing completion.

Click anywhere to close