Click outside or press Esc to close

For most Singaporeans, the CPF Housing Grant system is the single most valuable financial lever available when buying an HDB flat. The right grant — or combination of grants — can reduce the purchase price by S$30,000 to S$160,000 and cut the cash outlay needed at the point of sale dramatically. Yet many buyers remain unclear about which grants they qualify for, how the grants interact, and what happens when eligibility conditions change before completion. This guide covers every HDB CPF Housing Grant available in 2026: the Enhanced CPF Housing Grant (EHG), Family Grant, Step-Up CPF Housing Grant, Proximity Housing Grant (PHG), and the Singles Grant — with full eligibility tables, income ceiling rules, and a worked example.

- The Enhanced CPF Housing Grant (EHG) provides up to S$80,000 for first-timer SC couples buying BTO or resale flats (income ceiling S$9,000/mth).

- The Family Grant provides S$80,000 (SC couple, BTO) to S$50,000 (resale), on top of EHG — making combined grants up to S$160,000 for qualifying couples.

- The Step-Up CPF Housing Grant gives second-timer SC families S$15,000 towards a 4-room or smaller BTO flat.

- The Proximity Housing Grant (PHG) provides S$30,000 (living with) or S$20,000 (living near) parents or child — for resale buyers.

- The Singles Grant gives eligible single SC applicants aged ≥35 up to S$25,000 towards a resale flat or S$25,000 for a 2-room BTO.

- All grants are administered by HDB and applied via the HDB Flat Portal (homes.hdb.gov.sg) — not through the CPF Board directly.

- Grants offset the purchase price and reduce the HDB loan quantum required; they are not paid in cash to the buyer.

What Are HDB CPF Housing Grants and Who Administers Them?

HDB CPF Housing Grants are subsidies provided by the Housing and Development Board (HDB) under Singapore’s public housing policy. Despite the “CPF” label, the grants are designed and administered entirely by HDB; the Central Provident Fund (CPF) Board plays a secondary role in that CPF Ordinary Account (OA) savings may be used to fund the portion of the flat price not covered by grants. The grants exist because HDB’s policy mandate — set by the Ministry of National Development (MND) — is to ensure that public housing remains affordable across a wide income range. Grants are structured to taper off as household income rises, so they provide the greatest assistance to lower-income first-time buyers.

Importantly, grants are credited directly to reduce the flat’s purchase price or loan quantum — they are never paid to buyers in cash. This means they reduce the amount you borrow (and therefore the interest you pay over the loan tenure) rather than arriving as a lump sum in your bank account. Understanding this distinction is critical when doing upfront cost planning.

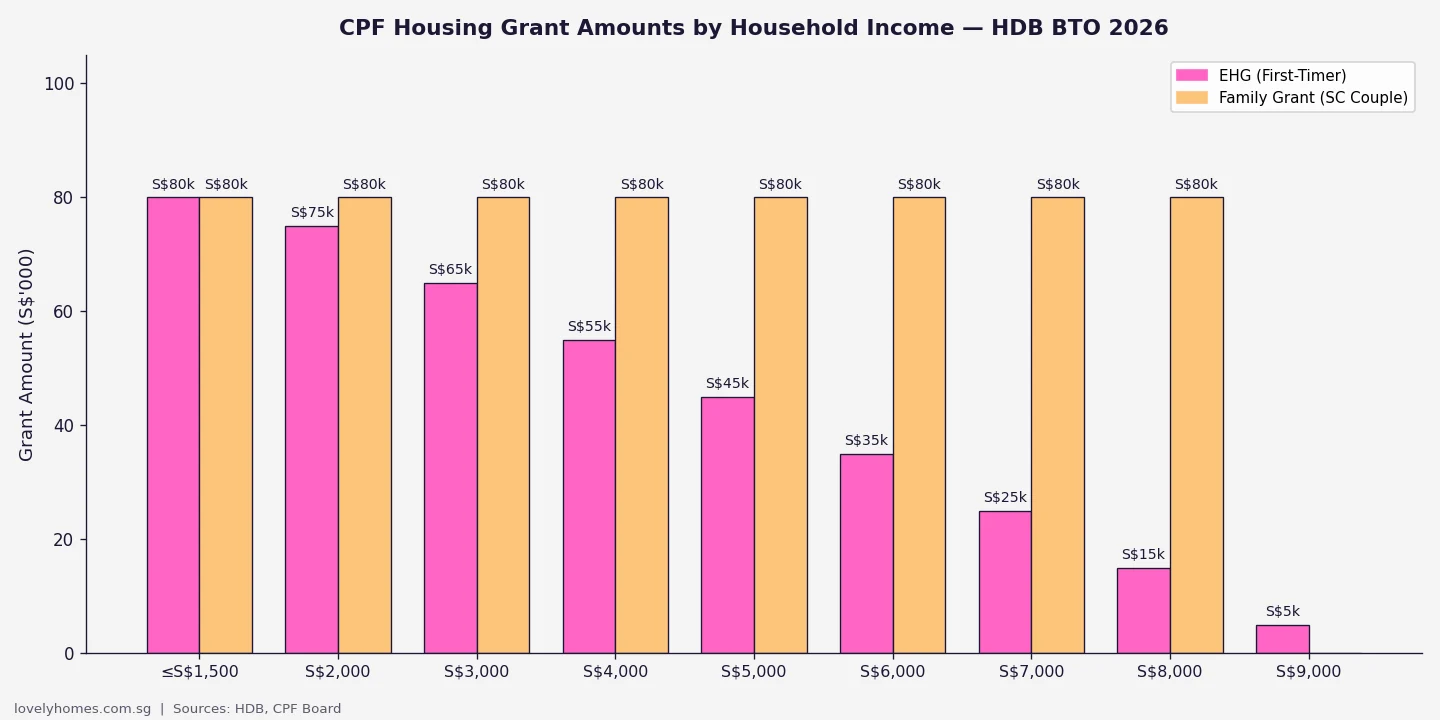

Grant Amounts by Household Income — EHG and Family Grant

The EHG is the largest single grant available and applies across a wide income spectrum. Its key feature is that the grant amount decreases as income rises, in S$5,000–S$10,000 steps, from a maximum of S$80,000 for couples earning S$1,500 per month or less, stepping down to S$5,000 for couples earning between S$8,500 and S$9,000 per month. Couples with a gross monthly income above S$9,000 do not qualify for the EHG. Importantly, “household income” for grant purposes is the average gross monthly income of all working persons listed on the flat application, typically the two applicants and any occupants who are working.

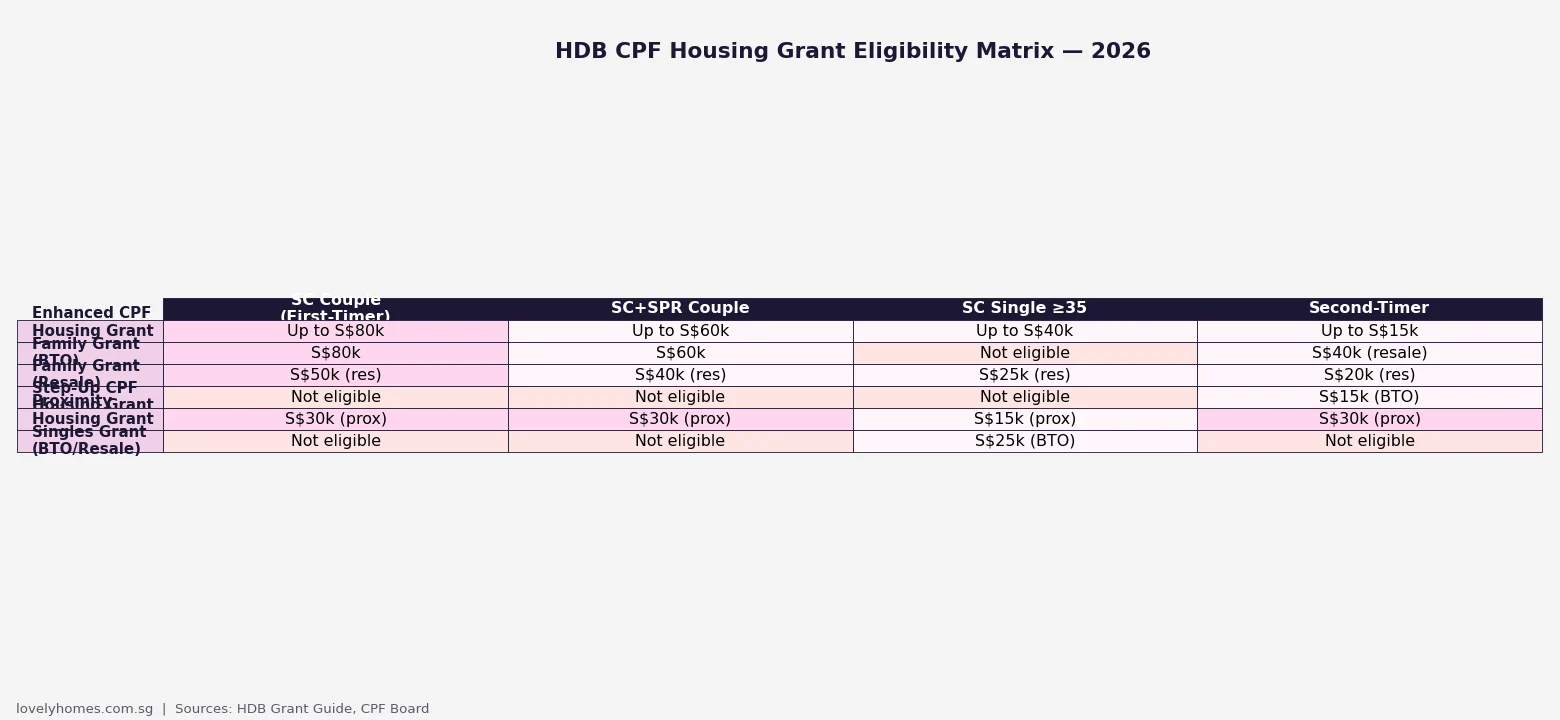

Grant Eligibility Matrix — Who Qualifies for What

The matrix above illustrates how grants are layered across buyer profiles. An SC couple buying a BTO as first-timers can potentially stack the EHG (up to S$80,000) and the Family Grant (S$80,000), for a combined S$160,000 grant — the maximum available under any HDB grant combination. SC/SPR mixed-citizenship couples receive the Family Grant at a lower quantum (S$60,000 for BTO; S$50,000 for resale) and are eligible for the EHG, but at the EHG rate applicable to the SPR-tier income rules. Singles aged 35 and above receive a dedicated Singles Grant and are eligible for a scaled-down EHG.

Deep Dive: The Five Main HDB Grants in 2026

1. Enhanced CPF Housing Grant (EHG)

The EHG replaced the Additional CPF Housing Grant (AHG) and Special CPF Housing Grant (SHG) in September 2019. It is the most broadly applicable grant and covers both BTO and resale applications. Key conditions include: both applicants must have worked continuously for at least 12 months before the application date; the flat must not exceed a purchase price ceiling (for resale, the flat must be valued within the HDB resale price cap for the flat type and town); and applicants must not currently own or have disposed of private residential property within 30 months of application. The EHG applies regardless of flat type or location — a unique feature distinguishing it from the old SHG, which was restricted to non-mature estates.

2. Family Grant (BTO and Resale)

The Family Grant is citizenship-tiered and applies on top of the EHG. For SC-SC couples purchasing a new BTO flat, the Family Grant is S$80,000 regardless of income (subject to the S$14,000/mth income ceiling). For SC-SPR couples, the BTO Family Grant is S$60,000. For resale purchases, the quantum is S$50,000 (SC-SC) or S$40,000 (SC-SPR). The Family Grant can also be claimed by first-timer applicants who are singles applying under the Joint Singles Scheme, though the quantum is halved. There is no separate income ceiling for the Family Grant beyond the general resale/BTO eligibility income ceiling of S$14,000 per month gross household income.

3. Step-Up CPF Housing Grant

The Step-Up Grant is specifically for second-timer SC families — meaning applicants who previously owned or occupied an HDB flat, received a housing subsidy (including previous BTO application grant), or are currently living in a subsidised rental flat. The grant amount is S$15,000 and applies only to the purchase of a 4-room or smaller BTO flat. It is HDB’s way of facilitating the upgrading or right-sizing journey for mature families, while channelling the most significant grants to genuine first-timers. The income ceiling is S$7,000 per month.

4. Proximity Housing Grant (PHG)

The PHG is unique in that it is available for resale flat purchases only — it does not apply to BTO. It rewards buyers who choose to live near their parents or adult children. The quantum is S$30,000 if you buy a resale flat to live with parents or an unmarried child, and S$20,000 if you buy within 4 km of parents or a married child’s home. PHG can be combined with the EHG and Family Grant for resale purchases, making it a powerful stacking grant for families with a proximity reason to choose resale over BTO. There is no income ceiling for the PHG — it is available across all income levels subject to basic HDB eligibility.

5. Singles Grant

The Singles Grant is available to SC singles aged 35 and above applying for a 2-Room Flexi BTO flat or a resale flat. The quantum is S$25,000 for resale (4-room or smaller) and a scaled-down EHG for 2-Room Flexi BTO applications. Since January 2024, singles have been able to apply for 4-room resale flats (previously restricted to 5-room or smaller), broadening the effective pool. Singles who subsequently marry and upgrade to a larger flat may be treated as first-timers for the purposes of the EHG and Family Grant, subject to HDB’s conditions at the time of the subsequent purchase.

Summary Table — 2026 HDB Grant Quantum at a Glance

| Grant | Max Quantum | Income Ceiling | BTO / Resale |

|---|---|---|---|

| Enhanced CPF Housing Grant (EHG) | S$80,000 | S$9,000/mth | Both |

| Family Grant (SC couple, BTO) | S$80,000 | S$14,000/mth | BTO |

| Family Grant (SC couple, Resale) | S$50,000 | S$14,000/mth | Resale |

| Family Grant (SC+SPR, BTO) | S$60,000 | S$14,000/mth | BTO |

| Step-Up CPF Housing Grant | S$15,000 | S$7,000/mth | BTO (4-room or smaller) |

| Proximity Housing Grant — With | S$30,000 | No ceiling | Resale only |

| Proximity Housing Grant — Near | S$20,000 | No ceiling | Resale only |

| Singles Grant (Resale) | S$25,000 | S$7,000/mth | Resale (4-room or smaller) |

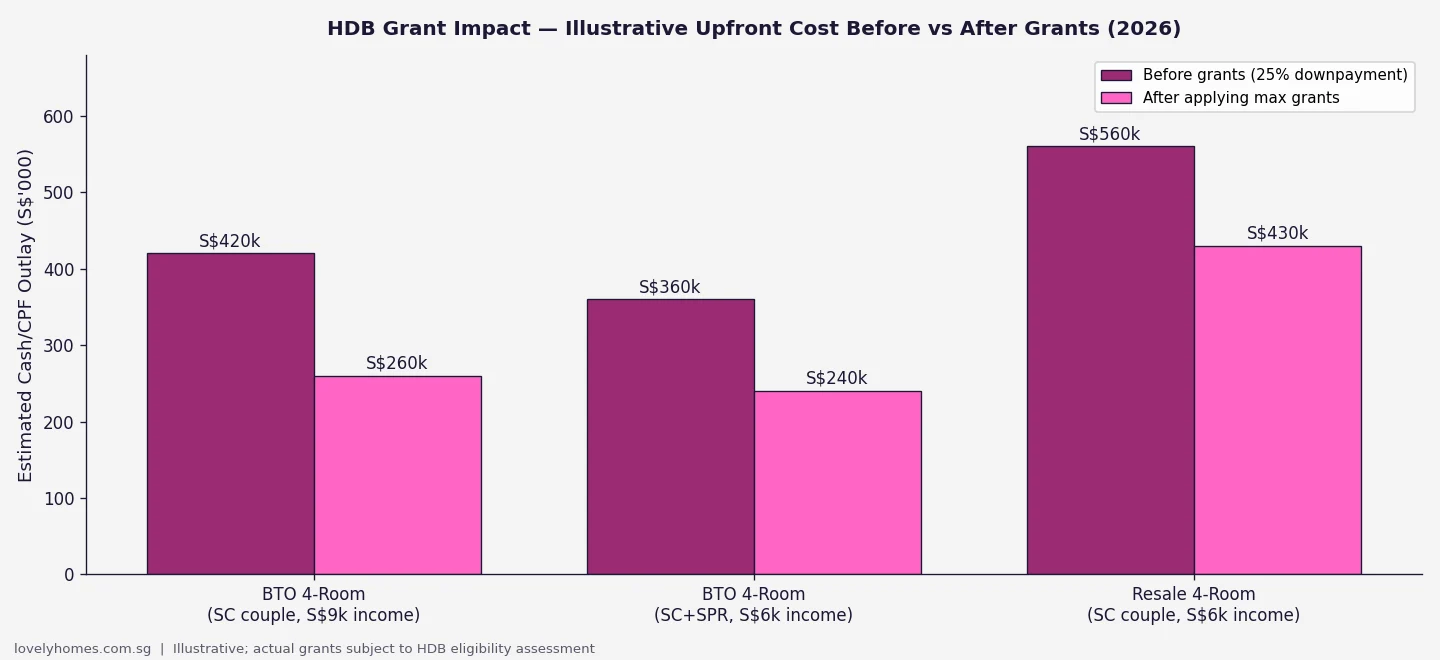

Grant Impact on Upfront Cost — Three Worked Scenarios

Scenario A — BTO 4-Room, SC Couple, S$9,000/mth household income: A 4-room BTO flat in a non-mature estate at S$420,000. Gross monthly income is S$9,000 — at the EHG ceiling, so EHG is S$5,000. Family Grant (BTO, SC couple) is S$80,000. Total grants: S$85,000. Adjusted purchase price for grant purposes: S$335,000. 10% downpayment (HDB loan): S$33,500 cash/CPF. BSD on S$335,000: S$5,350. Estimated upfront: ~S$38,850. Without grants: 10% of S$420,000 = S$42,000 + BSD S$6,900 = ~S$48,900. Grant saving: ~S$10,050 in upfront costs, plus S$85,000 reduction in loan principal.

Scenario B — Resale 4-Room, SC+SPR Couple, S$6,000/mth income: Resale flat at S$560,000. EHG at S$6,000 income = S$35,000; Family Grant (resale, SC+SPR) = S$40,000; PHG (living near parents) = S$20,000. Total grants: S$95,000. Adjusted price: S$465,000. 25% downpayment (bank loan): S$116,250. BSD on S$560,000: S$12,200. Upfront: ~S$128,450. Without grants: 25% of S$560,000 = S$140,000 + BSD S$12,200 = ~S$152,200. Grant saving upfront: ~S$23,750 — largely via reduced loan principal.

Scenario C — Single SC, Aged 38, Resale 4-Room, S$5,000/mth income: Resale flat at S$380,000. Singles Grant: S$25,000. EHG (single, S$5,000 income) = S$40,000. Total: S$65,000. Adjusted price: S$315,000. HDB loan 90% LTV: S$283,500; 10% downpayment cash/CPF: S$31,500. BSD on S$380,000: S$6,300. Upfront: ~S$37,800. Without grants: S$38,000 + S$6,300 = ~S$44,300.

Common Pitfalls and Misconceptions

The most common misconception is that HDB grants are paid out as cash. They are not — they reduce the assessed purchase price or outstanding loan, so the benefit is realised over the loan tenure (less interest) rather than immediately. A second common error is failing to check whether either applicant has previously received a housing subsidy. Any prior CPF Housing Grant, AHG, SHG, or EHG will classify you as a “second-timer” for certain grants, which can significantly reduce your eligible quantum. Third, buyers sometimes conflate the EHG income ceiling (S$9,000/mth) with the general HDB eligibility income ceiling (S$14,000/mth for families; S$7,000/mth for singles buying new 2-room BTO). These are separate thresholds — you can be eligible to buy an HDB flat but not eligible for the EHG if your income exceeds S$9,000/mth.

What Might Change — HDB Grant Policy Outlook (2026–2028)

Editorial analysis — not financial advice or a government forecast. Grant amounts have been periodically revised upward since the EHG’s introduction in 2019 to keep pace with rising HDB resale prices. Given that median resale prices have risen materially since 2021, there is broad industry expectation that the income ceilings and/or grant quanta will be reviewed again in either the FY2026 or FY2027 Budget. The Singles Grant was enhanced in January 2024 to allow 4-room resale access; further extension to cover 5-room flats remains a periodic policy discussion. The PHG’s absence from BTO purchases is another area where advocacy groups have sought extension, particularly for couples who choose resale specifically for proximity to elderly parents.

Frequently Asked Questions

Can I get both the EHG and the Family Grant at the same time?

What counts as “household income” for grant eligibility?

Can permanent residents (SPRs) receive HDB grants?

What happens to the grant if I sell the flat within the Minimum Occupation Period (MOP)?

Does the Proximity Housing Grant apply if I buy near a sibling rather than a parent?

If I previously took a CPF Housing Grant, can I get another one for my next flat?

How do I apply for HDB grants and how long does approval take?

Related Articles

- Singapore HDB Resale Guide 2026

- HDB BTO June 2026 Launch — Complete Project Guide

- Singapore CPF Property Usage Guide 2026

- HDB Resale Levy Singapore 2026: Complete Guide for Second-Timer Buyers

- HDB Ethnic Integration Policy (EIP) Singapore 2026

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

Disclaimer: This article is produced by the LovelyHomes Editorial Team for informational purposes only and does not constitute financial, legal, or housing advice. Grant amounts, income ceilings, and eligibility conditions are set by HDB and are subject to change without prior notice. All figures cited are based on publicly available HDB data as at June 2026. Readers should verify current grant eligibility and quantum directly with HDB via the HDB Flat Portal (homes.hdb.gov.sg), the HDB InfoWEB, or by calling the HDB Sales/Resale Enquiry hotline. Consult a licensed financial adviser before making any housing or financial decisions.

0 Comments