Singapore Mortgage Calculator 2026: TDSR, LTV & Monthly Repayment Guide

⚡ Quick Answer — Singapore Mortgage Calculator 2026

- Your maximum monthly loan repayment for a bank loan must not exceed 55% of gross monthly income (Total Debt Servicing Ratio, or TDSR).

- For HDB flats and Executive Condominiums, an additional MSR cap of 30% applies — meaning your HDB/EC loan repayment cannot exceed 30% of gross income.

- Bank loans: maximum 75% LTV (first property); HDB concessionary loans: maximum 80% LTV but for HDB flats only.

- At 3.5% p.a. over 25 years, a S$1,000,000 loan costs approximately S$5,012 per month.

- The standard annuity formula determines monthly repayment: M = P × [r(1+r)^n] / [(1+r)^n − 1], where P = principal, r = monthly rate, n = months.

- TDSR stress-tests use a floor rate of 4.0% — banks must ensure borrowers can still pass TDSR at 4.0% even if the offered rate is lower.

- CPF Ordinary Account savings may be used to fund the downpayment and monthly repayments (subject to the CPF usage limits tied to the property’s remaining lease).

- Always compare rates from at least 3 banks and check for lock-in periods, prepayment penalties, and rate re-pricing clauses before committing.

What Is a Singapore Mortgage Calculator and Why Do You Need One?

A Singapore mortgage calculator is a financial tool that computes your estimated monthly home loan repayment based on the loan amount, interest rate, and loan tenure. It is the starting point for any property purchase in Singapore — before you can assess affordability, check TDSR compliance, or compare loan packages across banks, you need to know what a given loan size will cost you each month.

In Singapore, the Monetary Authority of Singapore (MAS) regulates home lending through two key ratios: the Total Debt Servicing Ratio (TDSR) and, for HDB properties and Executive Condominiums (ECs), the Mortgage Servicing Ratio (MSR). Understanding both is essential before signing any Option to Purchase.

The Core Formula: How Monthly Repayment Is Calculated

Singapore bank home loans use the standard reducing-balance annuity method. The formula is:

Where: M = monthly repayment; P = principal loan amount; r = monthly interest rate (annual rate ÷ 12); n = total number of monthly payments (years × 12).

At 3.5% p.a. over 25 years: r = 0.035 ÷ 12 = 0.002917; n = 300. For P = S$1,000,000: M = 1,000,000 × [0.002917 × (1.002917)^300] / [(1.002917)^300 − 1] ≈ S$5,012 per month.

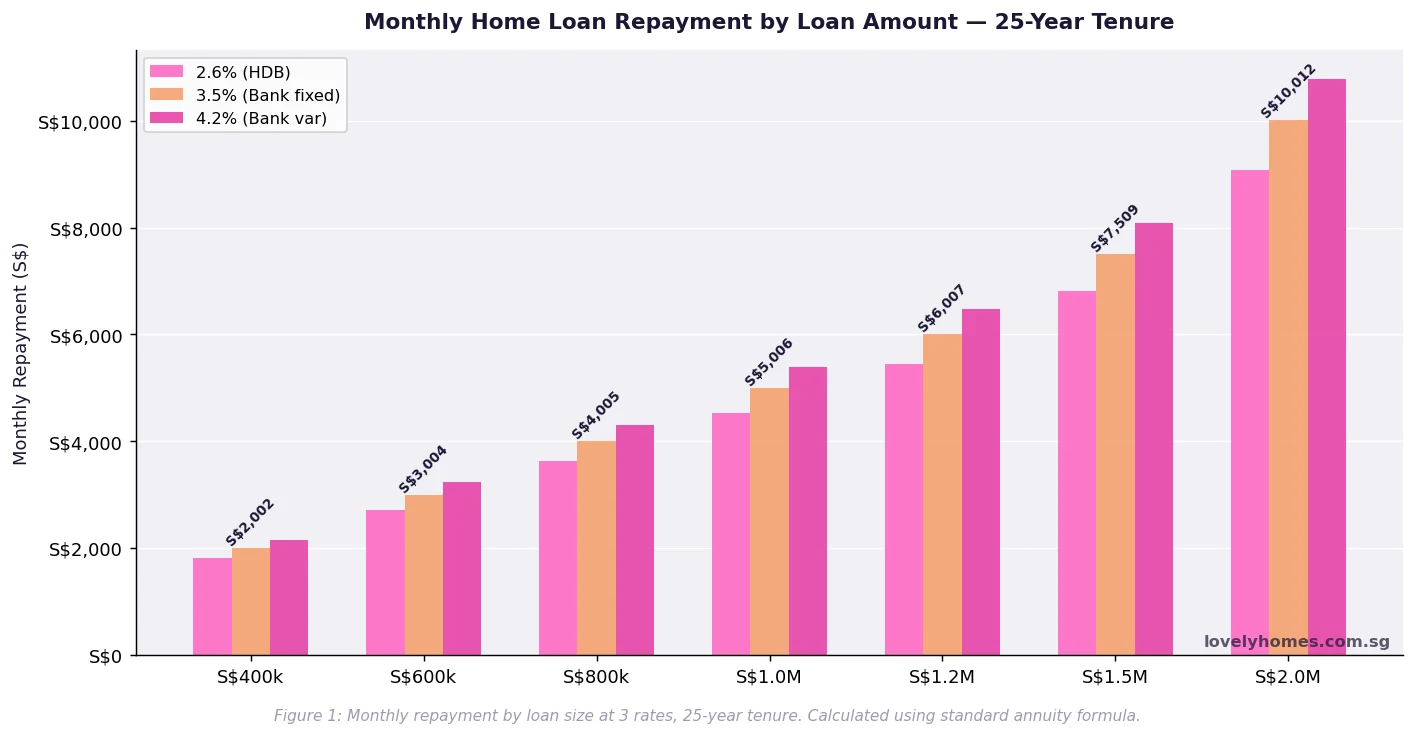

Monthly Repayments at Common Loan Sizes (2026)

At the prevailing 2026 range of bank fixed rates (approximately 3.2–3.9% p.a.) and HDB concessionary rate (2.6%), the chart above illustrates how steeply monthly costs rise with loan size. A S$800,000 loan at 3.5% costs S$4,010 per month — a figure that requires a combined gross monthly income of at least S$7,290 to pass TDSR at 55%. At S$1.5M, you need S$13,655+ in combined monthly income to pass TDSR.

TDSR: What It Is and How It Limits Your Loan

The Total Debt Servicing Ratio (TDSR) was introduced by MAS in 2013 and tightened to its current 55% threshold in 2022. TDSR measures the proportion of a borrower’s gross monthly income that goes toward servicing all debt obligations — not just the home loan, but also car loans, credit cards (30% of outstanding balance counts), personal loans, and other property loans.

The practical implication: if your gross household income is S$10,000 per month, your total debt repayments across all outstanding loans cannot exceed S$5,500 per month to qualify for a new bank home loan. If you already have a car loan of S$800/mth and credit card outstanding of S$5,000 (counted at S$1,500/mth for TDSR), your maximum new home loan repayment is S$5,500 − S$800 − S$1,500 = S$3,200/mth — even if you have enough income for more.

Banks are required by MAS to stress-test TDSR using a floor interest rate of 4.0%. This means that even if your actual loan rate is 3.0%, the bank runs your TDSR calculation at 4.0% to ensure affordability under rate increases. This effectively reduces maximum loan eligibility by approximately 5–8% compared to a simple calculation at the offered rate.

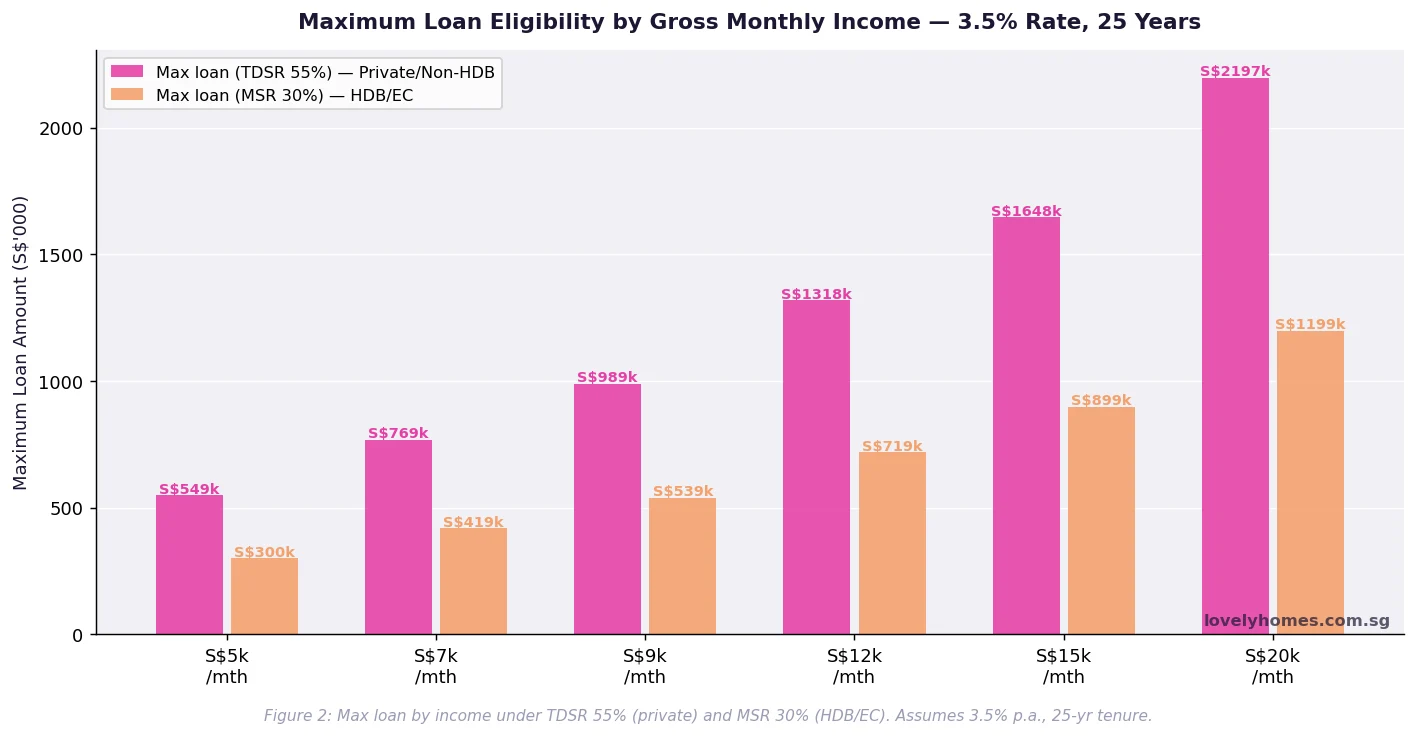

Maximum Loan Eligibility by Income

The chart makes clear the significant difference between the TDSR-governed private property market and the MSR-governed HDB/EC market. A household earning S$12,000 per month can in principle qualify for a bank loan of up to ~S$1.32M for a private condo under TDSR 55% — but if buying an HDB resale flat or EC, the MSR cap of 30% limits the same household to a loan of ~S$724,000.

MSR: The Additional Constraint for HDB Flats and ECs

The Mortgage Servicing Ratio (MSR) applies specifically to HDB residential flats and ECs. It caps the monthly repayment on the HDB or EC loan at 30% of gross monthly income — a stricter constraint than TDSR for these property types. Both TDSR and MSR must be satisfied simultaneously when purchasing HDB or EC.

For example, a household with S$9,000/mth gross income: TDSR allows up to S$4,950/mth total debt (55%); MSR caps the HDB loan component at S$2,700/mth (30%). The HDB loan must fit within S$2,700/mth — meaning a maximum HDB loan of approximately S$539,000 at 2.6% HDB rate over 25 years.

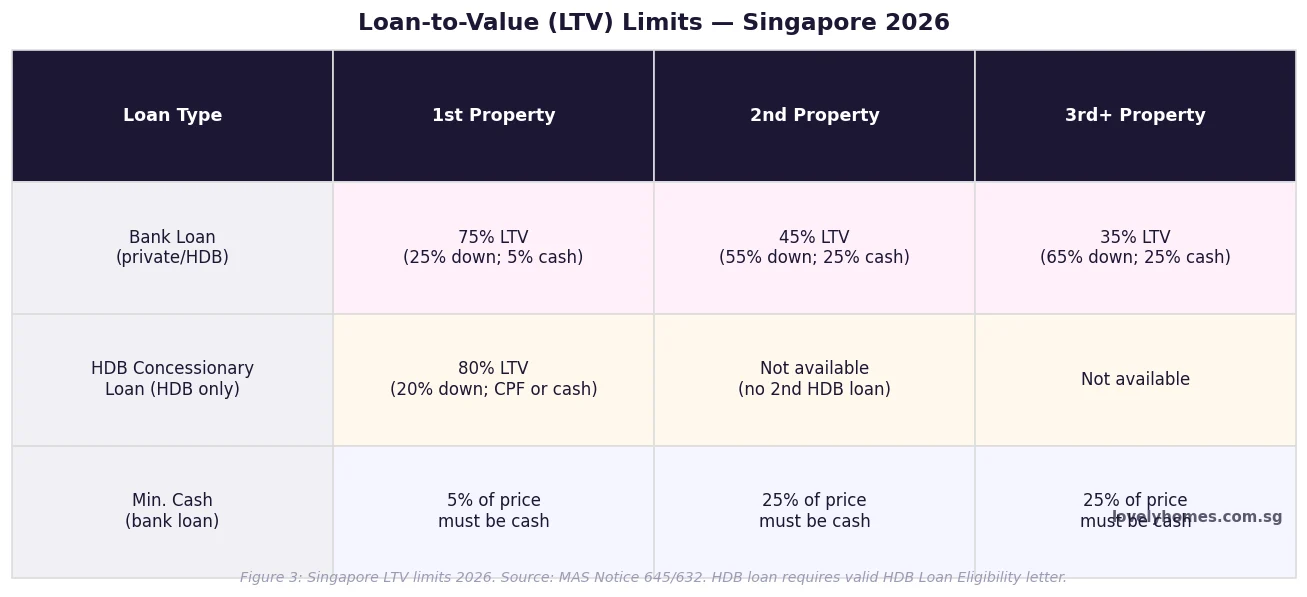

LTV Limits: How Much Can You Borrow?

The Loan-to-Value (LTV) ratio is the maximum proportion of a property’s purchase price (or valuation, whichever is lower) that a lender will finance. In Singapore, LTV limits are set by MAS and depend on how many outstanding property loans a borrower holds at the time of purchase.

Summary Table: Key Mortgage Parameters for Singapore Home Buyers (2026)

| Parameter | Bank Loan (Private/HDB) | HDB Concessionary Loan (HDB only) |

|---|---|---|

| Max LTV (1st property) | 75% | 80% |

| Min cash (1st property) | 5% of price (cash only) | Can be all CPF |

| TDSR cap | 55% of gross income | 55% (TDSR applies) |

| MSR cap (HDB/EC) | 30% (HDB/EC only) | 30% |

| Max loan tenure (< 65 yrs old) | 30 years (condo); 25 years effective (HDB) | 25 years |

| Stress-test floor rate | 4.0% p.a. (MAS mandated) | No stress test — fixed rate 2.6% |

| Eligibility for HDB loan | Any borrower | Must hold valid HLE; income ceiling applies |

| Repayment method | CPF OA or cash | CPF OA, HDB deduction, or cash |

Worked Example: The Lim Family Buying Their First HDB

📌 Case Study: The Lim Family — 4-Room HDB Resale in Ang Mo Kio

Profile: Married couple, SC/SC, ages 32 and 30. Combined gross monthly income S$8,500. Buying a 4-room HDB resale flat in Ang Mo Kio at S$580,000. Eligible for Enhanced Housing Grant (EHG) of S$50,000 and Family Grant of S$50,000 (total grants S$100,000). Seeking HDB concessionary loan (HLE confirmed).

Step 1 — Loan amount: Purchase price S$580,000 minus grants S$100,000 = net S$480,000. HDB loan max 80% LTV of S$580,000 = S$464,000. But net after grants is S$480,000; applying 80% LTV to S$580,000 = S$464,000. Loan = S$464,000. Downpayment (20%) = S$116,000 — may be entirely from CPF OA.

Step 2 — Monthly repayment: HDB concessionary rate 2.6% p.a., 25-year tenure. M = 464,000 × [0.002167 × (1.002167)^300] / [(1.002167)^300 − 1] = S$2,094/mth.

Step 3 — MSR check: S$2,094 ÷ S$8,500 = 24.6% — below 30% MSR cap → PASS.

Step 4 — TDSR check: Assuming no other debt. S$2,094 ÷ S$8,500 = 24.6% — well below 55% TDSR → PASS.

Step 5 — BSD: First S$180,000 × 1% = S$1,800; next S$180,000 × 2% = S$3,600; remaining S$220,000 × 3% = S$6,600. Total BSD = S$12,000.

Total upfront cost: Downpayment S$116,000 (CPF) + BSD S$12,000 (CPF or cash) + legal fees ~S$3,000 + COV (if any) cash. Indicative upfront ≈ S$131,000 (mostly from CPF OA), with likely S$5,000–S$15,000 in cash for legal fees and any COV.

How Interest Rate Movements Affect Your Repayment

Singapore bank home loan rates are primarily linked to SORA (Singapore Overnight Rate Average), which replaced SIBOR/SOR as the benchmark rate in 2024. SORA is set daily by MAS and reflects the volume-weighted average rate of unsecured overnight SGD interbank transactions. Variable-rate packages are typically quoted as 3-month compounded SORA plus a spread (e.g., SORA + 0.75%). Fixed-rate packages lock the interest rate for 2–5 years before re-pricing.

As of mid-2026, the 3-month compounded SORA is approximately 2.8–3.0%, giving effective all-in variable rates of 3.55–3.75% for competitive packages. Fixed rates for 3-year locks are approximately 3.2–3.5%. The rate environment suggests that borrowers who locked in 2-year fixed rates in 2024 at ~3.8% are now approaching competitive re-pricing opportunities.

A 1% rise in interest rates on a S$1,000,000 loan over 25 years adds approximately S$500–S$560 per month to the repayment. Borrowers should stress-test their budgets at rates 1.5–2.0 percentage points above their current package to ensure they can absorb rate movements without TDSR breach.

What Might Change in Singapore Mortgage Regulation

MAS reviews TDSR and LTV parameters periodically as part of its macro-prudential framework. In a scenario of sustained high interest rates or rising household debt levels, further tightening (lower LTV caps, reduced TDSR thresholds) is possible. Conversely, if the property market softens significantly, regulators have historically relaxed restrictions to support demand. The 2022 TDSR reduction (from 60% to 55%) is the most recent change; the prior benchmark was 60% from 2013. Buyers should not assume current parameters will remain constant over a long holding period.

Forward-looking commentary is speculative and subject to MAS policy decisions which cannot be predicted.

Frequently Asked Questions

How do I use the TDSR formula to check my eligibility?

Calculate your total monthly debt obligations: add up all existing loan repayments (car loan, personal loan, credit card at 30% of outstanding balance, any other property loans). Then add the projected new home loan repayment. Divide the total by your gross monthly income. If the result is 0.55 or below, you pass TDSR. Banks calculate TDSR using a stress-test rate of 4.0% p.a., so use 4.0% when doing your own check to ensure accuracy. For joint borrowers, both gross incomes may be combined. However, if one borrower has existing debts, those are also included in the TDSR calculation against the combined income.

Can I use CPF to pay for my home loan repayments?

Yes, CPF Ordinary Account (OA) savings can be used for both the initial downpayment and ongoing monthly loan repayments on residential properties. There are three key limits to note. First, CPF usage is capped at the Valuation Limit (VL) — the lower of purchase price or market valuation. Second, once your CPF usage reaches the VL, further withdrawals require the property to have a remaining lease of at least 30 years and the remaining lease to extend beyond the youngest buyer’s age of 95. Third, CPF accrued interest (currently 2.5% p.a.) is added to the principal used, and this entire sum must be refunded to CPF on sale — reducing net cash proceeds. For HDB loans, CPF usage rules are more generous and integrated into the HDB payment process directly.

What is the difference between a fixed-rate and a variable-rate (SORA) home loan?

A fixed-rate package locks your interest rate for a defined period (typically 2–5 years), providing certainty over monthly repayments. After the fixed period, the loan re-prices to the bank’s prevailing rate — usually a SORA-linked package. A variable/SORA-linked package tracks the 3-month compounded SORA plus a spread. Your repayment fluctuates as SORA moves, but you benefit directly from rate cuts. In 2026, the choice between fixed and variable depends on your view of the SORA trajectory and your risk tolerance. Fixed packages are typically locked in for 2–3 years; leaving early incurs prepayment penalties of 1.0–1.5% of the outstanding loan amount. Always read the lock-in clause carefully before committing.

What happens if my TDSR exceeds 55% after I take the loan?

TDSR compliance is assessed at the point of loan application. Once the loan is granted and drawdown occurs, you are not in breach if your circumstances change (e.g., income drops, additional debt is taken on). However, if you wish to refinance to a new lender or take an additional loan, the new lender will re-assess TDSR at that point. If you fail TDSR, you cannot refinance or borrow more. Practically, this means maintaining a TDSR well below 55% is prudent — leaving buffer for life events such as job changes, medical expenses, or taking on a car loan. MAS requires banks to conduct TDSR reassessment when borrowers request loan top-ups or restructuring.

Is the HDB concessionary loan always better than a bank loan?

The HDB concessionary loan has a stable rate pegged at 0.1% above the CPF Ordinary Account rate — currently 2.6% p.a. — which provides predictability and does not carry lock-in penalties. However, bank loans often offer lower headline rates for the first 2–3 years (fixed packages at 3.0–3.5% have been available in recent cycles, and SORA packages can be lower still). The trade-off is rate risk after the fixed period. Practically: if you have limited cash reserves and need stability, the HDB loan is lower-risk. If you have buffer to absorb rate movements and can refinance actively, a bank loan may be cheaper over the full tenure. Once you take a bank loan for your HDB flat, you cannot switch back to an HDB loan on that property.

What is the maximum loan tenure in Singapore?

For bank loans, the maximum tenure is 30 years for private property (condo, landed) and effectively 25 years for HDB resale flats (banks may grant 30 years on paper but MAS caps the tenure at 25 years + borrower’s age ≤ 65, so younger buyers can access up to 30 years in practice). For HDB concessionary loans, the maximum is 25 years or up to age 65 for the youngest borrower, whichever is shorter. Longer tenures reduce monthly repayments but increase total interest paid significantly. A S$800,000 loan at 3.5% over 25 years costs S$321,500 in total interest; over 30 years it costs S$398,000 — S$76,500 more despite only S$490 lower monthly repayment.

Related Articles

- Singapore Home Loan Interest Rates 2026: SORA vs Fixed Rate Complete Guide

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Buyer’s Stamp Duty Singapore 2026: Complete Guide to BSD Rates

- HDB CPF Housing Grant Guide 2026: EHG, Family Grant, Step-Up and Singles Grant

- HDB Lease Decay Singapore 2026: CPF Limits, Bank LTV and What Buyers Must Know

- CPF for Property Purchase Singapore 2026: Complete Guide

- Singapore Condo Resale Guide 2026: Step-by-Step Buyer’s Complete Guide

Disclaimer

All loan calculations in this article are illustrative estimates based on the standard annuity formula. Actual monthly repayments, TDSR outcomes, and loan eligibility depend on each lender’s assessment criteria, prevailing interest rates at the time of application, borrower credit history, and MAS regulatory requirements in force at the time. Readers should not rely on these calculations as a guarantee of loan approval or as financial advice. Before applying for a home loan, consult a licensed mortgage broker, your preferred bank’s home loan officer, or a licensed financial adviser regulated by the Monetary Authority of Singapore (MAS). MAS home loan regulations: mas.gov.sg. CPF usage rules: cpf.gov.sg. HDB loan eligibility and HLE: hdb.gov.sg.

Click anywhere or press Esc to close