Buying a condominium in Singapore is one of the largest financial decisions most households will ever make. Whether you are a first-timer upgrading from an HDB flat, a permanent resident purchasing your first private home, or a foreigner entering Singapore’s property market, the process involves multiple stages, strict regulatory requirements, and substantial upfront costs. This guide walks you through every step — from checking your eligibility and financing to collecting your keys and settling in — so you can proceed with confidence and without surprises.

- A Singapore condo purchase follows 10 distinct stages: eligibility check → search → offer → OTP → solicitor/valuation → exercise OTP (S&P) → bank loan → requisitions → completion → post-completion.

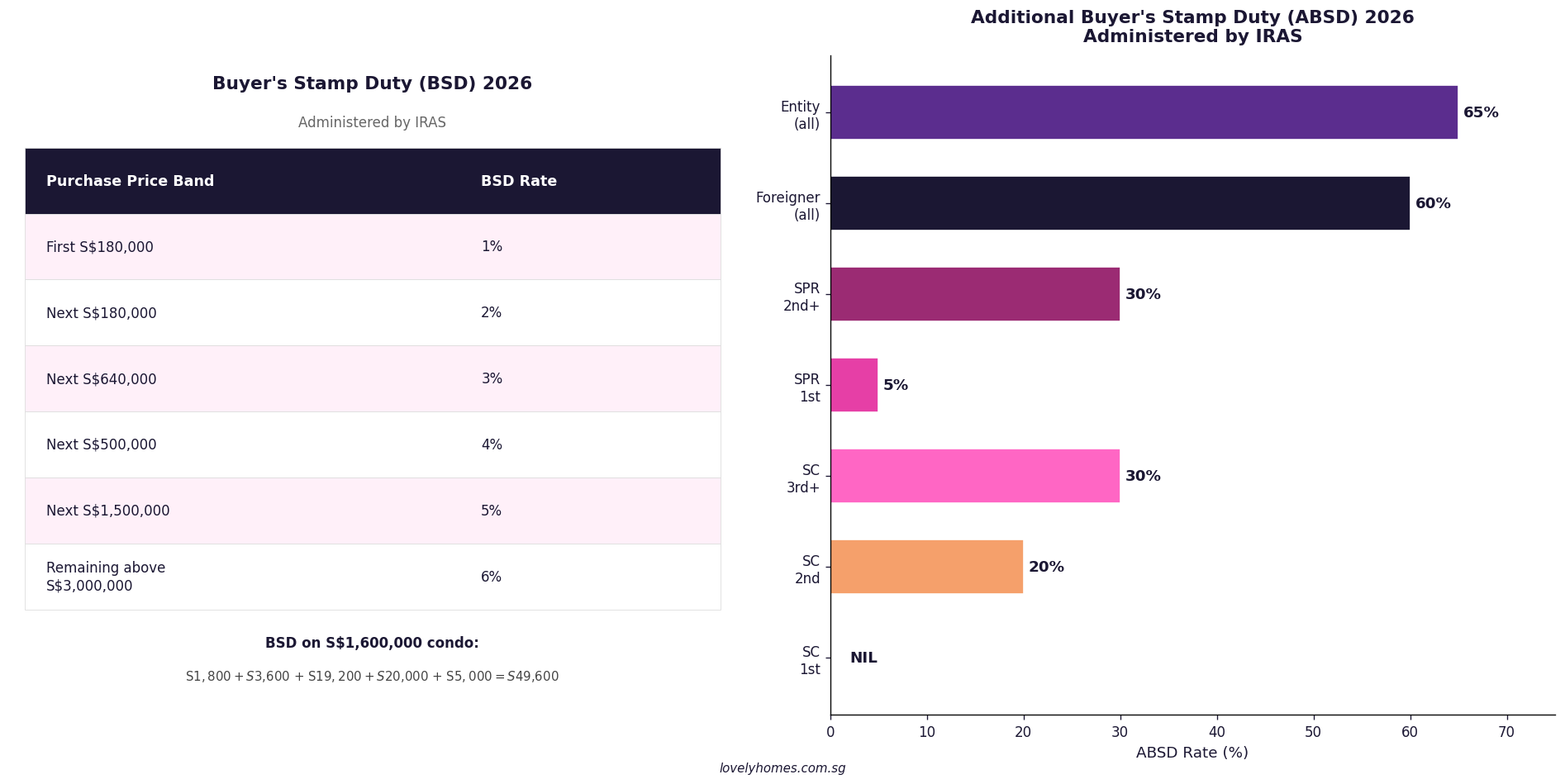

- Buyer’s Stamp Duty (BSD) is payable by all buyers; rates run from 1% to 6%, administered by IRAS.

- Additional Buyer’s Stamp Duty (ABSD) applies to Singapore citizens purchasing a second or subsequent residential property, Singapore Permanent Residents from their first purchase, and all foreigners — rates range from 5% to 65% of the purchase price.

- The Total Debt Servicing Ratio (TDSR) cap is 55% of gross monthly income; the Mortgage Servicing Ratio (MSR) cap of 30% applies only to HDB loans, not private condo purchases.

- The minimum cash down payment is 5% of the purchase price (for bank loans); the remainder of the 25% LTV shortfall can come from CPF Ordinary Account funds.

- Completion of a resale condo typically takes 10–12 weeks after option exercise; a new launch can take 3–5 years to TOP depending on construction progress.

- Legal fees for a condo purchase typically run S$2,500–S$4,000 for a standard transaction, covering title search, requisitions, and completion.

- A In-Principle Approval (IPA) from your bank should be obtained before making any offer — it costs nothing and lasts 30 days.

What Is a Condominium in Singapore?

Under Singapore law, a condominium is a privatised residential development governed by the Building Maintenance and Strata Management Act (BMSMA), administered by the Building and Construction Authority (BCA) and the relevant Management Corporation Strata Title (MCST). Condominiums differ from HDB flats in that they are privately built and sold, carry strata titles, are managed by an MCST, and typically feature shared amenities such as a swimming pool, gymnasium, and security. They can be sold on a freehold, 999-year leasehold, or 99-year leasehold basis. The Urban Redevelopment Authority (URA) regulates the development, sale, and advertising of private residential property, while IRAS administers stamp duties.

Step 1 — Check Your Eligibility and Financing

Before viewing a single showflat or property listing, establish your financial position. Singapore’s Monetary Authority of Singapore (MAS) mandates that all residential loans are subject to the Total Debt Servicing Ratio (TDSR) of 55% — meaning all monthly debt obligations (including the proposed mortgage) cannot exceed 55% of gross monthly income. Unlike HDB purchases, private condo purchases are not subject to the 30% Mortgage Servicing Ratio (MSR) cap.

Obtain an In-Principle Approval (IPA) from a bank before making any offer. The IPA is free, takes one to three working days, and tells you the maximum loan quantum, indicative interest rate, and monthly repayment. As at 1 July 2026, Singapore bank SORA-linked packages are pricing at approximately 1.15%–1.35% spread over the 3-Month Compounded SORA (currently around 1.07%), giving effective rates of approximately 2.22%–2.42%. Fixed-rate packages for two-year terms are available at approximately 2.55%–2.80%.

Simultaneously, check your ABSD profile: Are you a Singapore Citizen (SC), Permanent Resident (SPR), or foreigner? How many residential properties do you currently own or have you previously owned? Your ABSD liability — which can add 0% to 65% of the purchase price — will directly affect your cash requirements.

Step 2 — Property Search and Viewings

Search listings on URA’s Real Estate Information System (REALIS) for actual transacted prices, which reflect what buyers actually paid rather than asking prices. For new launches, request access to the developer’s showflat; for resale units, arrange viewings through the seller’s representative. Compare stacks, floor plans, and psf prices across comparable transactions before forming a view on value.

At this stage, commission your own valuation if considering a resale unit — banks will only loan against the lower of the transacted price or the formal valuation. A gap between the two means cash top-up from your own funds.

The 10-Step Buying Process — Visual Overview

Step 3–4 — Making an Offer and the Option to Purchase (OTP)

For a resale condo, the buying process is governed by the Controller of Housing under the Housing Developers (Control and Licensing) Act for new launches, and by common law for resale. In a resale transaction, the buyer and seller agree on a price, and the seller grants the buyer an Option to Purchase (OTP). The buyer pays an option fee (typically 1% of the purchase price), which grants them the exclusive right to buy the property within 14 calendar days. During this 14-day window, the buyer must arrange financing, engage a solicitor, and decide whether to proceed.

For a new launch, the process differs: buyers register an Expression of Interest (EOI) or join a ballot, attend a showflat, and — if selected — pay a 5% booking fee to receive the Sales & Purchase Agreement (S&P) from the developer. For a new EC (Executive Condominium), additional eligibility rules under HDB guidelines apply.

Step 5–6 — Engaging Your Solicitor and Exercising the OTP

Once you have decided to proceed, engage a solicitor immediately. Your solicitor will conduct a title search via the Singapore Land Authority (SLA) to confirm ownership, identify any caveats or encumbrances (outstanding mortgages, charges, or restrictive covenants), and raise legal requisitions with government agencies. To exercise the OTP, the buyer pays a further 4% of the purchase price (bringing the total deposit to 5%) and receives the signed S&P agreement. The balance of the purchase price is payable on completion, typically 10–12 weeks later for a resale unit.

BSD is payable within 14 days of exercising the OTP (for Singapore-issued documents) and can be paid from CPF Ordinary Account funds. ABSD is payable within 14 days of executing the S&P agreement and must be paid in cash.

Stamp Duty Deep-Dive: BSD and ABSD

BSD is levied on all residential property purchases in Singapore, at progressive rates administered by the Inland Revenue Authority of Singapore (IRAS): 1% on the first S$180,000, 2% on the next S$180,000, 3% on the next S$640,000, 4% on the next S$500,000, 5% on the next S$1,500,000, and 6% on amounts above S$3,000,000. On a S$1,600,000 condo, BSD amounts to S$49,600.

ABSD is an additional stamp duty introduced by the government to moderate investment demand. As at 1 July 2026, key ABSD rates are: SC 1st property 0%, SC 2nd 20%, SC 3rd+ 30%; SPR 1st property 5%, SPR 2nd+ 30%; foreigners (all) 60%; entities (all) 65%. ABSD must be settled in cash within 14 days of the date of the instrument — it cannot be paid using CPF funds.

| Buyer Profile | BSD (S$1.6M) | ABSD Rate | ABSD Amount | Total Stamp Duty |

|---|---|---|---|---|

| SC — 1st property | S$49,600 | NIL | NIL | S$49,600 |

| SC — 2nd property | S$49,600 | 20% | S$320,000 | S$369,600 |

| SC — 3rd+ property | S$49,600 | 30% | S$480,000 | S$529,600 |

| SPR — 1st property | S$49,600 | 5% | S$80,000 | S$129,600 |

| Foreigner — any property | S$49,600 | 60% | S$960,000 | S$1,009,600 |

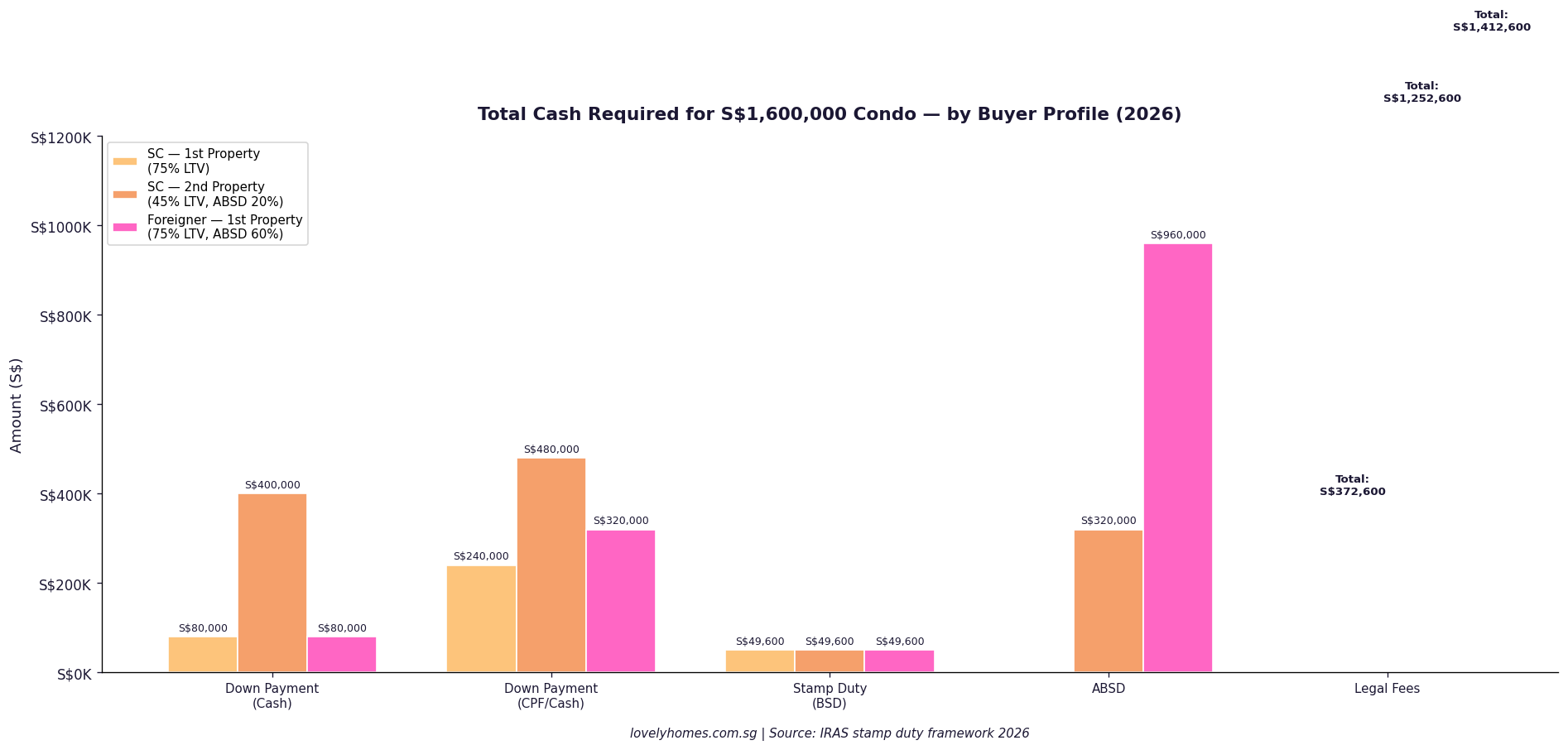

Total Cash Required — Three Buyer Profiles for a S$1.6M Condo

Step 7 — Applying for Your Bank Loan

After exercising the OTP, your solicitor notifies the bank to proceed with the formal loan. The bank issues a Letter of Offer (LO), which sets out the loan quantum, interest rate structure, lock-in period (typically two to three years), and prepayment penalty. Review the LO carefully before signing. The Loan-to-Value (LTV) limit for a first housing loan is 75% of the lower of the purchase price and the bank’s valuation; for a second outstanding housing loan, LTV drops to 45%; for a third or subsequent, 35%. These limits are set by MAS and were last revised in September 2022.

Note that CPF Ordinary Account funds can be used to service the monthly instalment and to pay for the BSD — but not for ABSD or cash top-up arising from a valuation gap.

Step 8–9 — Requisitions, Title Search and Completion

Your solicitor will raise legal requisitions with IRAS (property tax status), the Land Transport Authority (road interpretation plan), the Public Utilities Board (water and drainage charges), and other relevant authorities. These take five to ten working days. On completion, the buyer’s solicitor forwards the balance purchase price (net of the deposit already paid) to the seller’s solicitor, who simultaneously releases the title. Your caveat is lodged at SLA on the same day, protecting your interest. Keys are handed over and you become the registered proprietor.

Worked Example: The Teo Family — SC Couple Buying a 2nd Property

Mr and Mrs Teo are Singapore Citizens purchasing a 3-bedroom OCR condo in Tampines at S$1,600,000 as their second residential property. They currently own an HDB flat in Bedok (MOP cleared), which they are retaining. Their combined gross monthly income is S$18,000.

- BSD: S$49,600 — paid from CPF Ordinary Account.

- ABSD (20%, 2nd property SC): S$320,000 — paid in cash at signing.

- Down payment: 55% (LTV 45% for 2nd property) = S$880,000 total equity. Minimum 25% cash = S$400,000; remaining 30% (S$480,000) may come from CPF OA.

- Bank loan: S$720,000 at 2.35% (2yr fixed); monthly repayment ~S$3,180. TDSR = 17.7% — well below 55% cap.

- Legal fees: ~S$3,200.

- Total cash outlay at completion: S$400,000 (cash downpayment) + S$320,000 (ABSD) + S$3,200 (legal) = S$723,200 cash; CPF drawdown S$529,600 (BSD + remaining downpayment).

This example illustrates why a Singapore Citizen buying a second residential property must maintain substantial liquid reserves — ABSD alone accounts for S$320,000 that must be settled in cash.

Why This Matters: Cooling Measures and the Investment Calculus

Singapore’s layered stamp duty framework — BSD plus ABSD plus Seller’s Stamp Duty (SSD) — is a deliberate policy tool that the Ministry of Finance and MAS use to moderate speculative activity and maintain housing affordability. Since April 2023, when ABSD was raised sharply (SC 2nd property from 17% to 20%; foreigner from 30% to 60%), transaction volumes among investment buyers have moderated but have not collapsed. Demand from owner-occupiers and upgraders has remained resilient, underpinned by Singapore’s robust employment market and steady inflow of high-net-worth residents. URA’s Q2 2026 Flash Estimates, released 1 July 2026, show the overall PPI still rising — +0.5% QoQ — even as the market digests the significant supply pipeline of 61,000 units expected to complete over the next few years.

New Launch vs Resale — Which Should You Buy?

New launches offer the ability to select your unit from a plan, benefit from the Progressive Payment Scheme (PPS), and potentially capture price appreciation between the launch date and TOP. However, they carry construction risk, deferred occupation, and you cannot see the exact finished product. Resale condos offer immediate entry, known physical condition, and existing community — but require cash top-up for any valuation gap. A thorough due diligence process, including engaging a structural inspector (approximately S$300–S$600) and reviewing the MCST’s financials, is advisable for resale condos.

What Might Come Next

With 9,320 private residential units on the 2026 GLS Confirmed List — over 50% above the 10-year annual average — supply is rising. URA’s full Q2 2026 data (due 24 July 2026) will clarify whether the modest +0.5% QoQ growth reflects genuine price moderation or a base effect from a particularly strong Q1. Analysts are watching whether the Federal Reserve’s policy trajectory, MAS exchange rate management, and global economic uncertainty will affect the purchasing power of foreign buyers who still face a 60% ABSD threshold. For Singapore Citizens buying within their first property, the outlook remains favourable — ABSD-free access to the market at a time when interest rates are declining from their 2023–2024 peaks.

Frequently Asked Questions

Can I use my CPF to pay ABSD?

No. ABSD must be paid entirely in cash. This distinguishes it from BSD, which can be settled using CPF Ordinary Account funds. ABSD must be paid to IRAS within 14 days of executing the instrument (typically the Sales & Purchase Agreement), so you must have the cash available before signing. This is one reason why financial planners recommend stress-testing your liquidity before committing to a second property purchase.

What happens if the bank valuation is lower than my purchase price?

If the bank’s formal valuation is S$1,550,000 but you are purchasing at S$1,600,000, the bank will only lend against the lower figure. With a 75% LTV, your loan quantum drops to S$1,162,500 instead of S$1,200,000 — meaning you must fund the S$37,500 shortfall from cash or CPF. This is known as a cash over valuation (COV) situation, though HDB uses this term more formally. For private condos, always check comparable transactions on URA REALIS and obtain a preliminary estimate from your bank before committing.

How long does a resale condo purchase take from offer to keys?

From the date the OTP is exercised to legal completion, the typical timeline is 10–12 weeks. The first four weeks involve legal requisitions, title search, and bank processing. Completion is then scheduled between the buyer’s and seller’s solicitors to align with the bank’s disbursement schedule. Delays can arise from outstanding property tax arrears, disputed caveats, or bank processing backlogs during peak periods. Build contingency time into your planning, especially if you need to vacate your current home simultaneously.

Do I need a solicitor, or can I use the developer’s panel firm for a new launch?

For a new launch, the developer’s solicitors handle the S&P agreement on a panel basis, and buyers can use them without engaging separate legal representation — the fee is typically absorbed by the developer. However, it is strongly advisable to engage your own independent solicitor (approximately S$2,500–S$3,500 for a standard new launch transaction) so that someone is specifically acting in your interests, reviewing payment schedules, and flagging any unusual conditions. For resale transactions, you must engage your own solicitor.

Can a foreigner buy any type of condo in Singapore?

Foreigners (non-citizens, non-PRs) may purchase units in private condominiums and apartments in Singapore without restriction, subject to the 60% ABSD. However, foreigners cannot purchase HDB flats, executive condominiums within the first 10 years of completion, or landed residential property (houses, bungalows, semi-detached, or terraced) without prior approval from the Land Dealings Approval Unit (LDAU) under SLA. Approval is rarely granted except in exceptional circumstances of permanent residency or significant economic contribution.

What is the Seller’s Stamp Duty (SSD), and does it affect my purchase?

SSD is payable by the seller, not the buyer — but it affects the seller’s net proceeds and can influence pricing and negotiation. SSD rates are 12% (if sold within 1 year), 8% (within 2 years), 4% (within 3 years), and nil beyond. If you plan to resell within three years, factor SSD into your exit modelling. On a S$1,600,000 condo sold at S$1,750,000 in 18 months, SSD at 8% = S$140,000 — wiping out most of the gross gain.

Is there a minimum occupation period for private condos?

There is no Minimum Occupation Period (MOP) for private condos in the same sense as HDB flats. However, the SSD effectively imposes a three-year hold before selling without penalty. If you purchased using an HDB resale flat that was originally classified under the MOP rules, you would also need to comply with those rules separately before buying the private property (unless you are an SC buying as a 2nd property). Confirm with HDB if any concurrent ownership obligations apply to your specific situation.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Seller’s Stamp Duty (SSD) Guide 2026

- Singapore Home Mortgage Guide 2026

- Singapore New Launch Condo Buying Guide 2026

- Singapore Property Due Diligence Guide 2026

- Singapore Property Market Forecast 2H 2026

- Singapore Property Seller Complete Guide 2026

Disclaimer: This article is produced for general informational purposes only and does not constitute financial, legal, or investment advice. Property prices, stamp duty rates, LTV limits, TDSR thresholds, and interest rates are subject to change by the relevant Singapore authorities (URA, IRAS, MAS, SLA, HDB, CPF Board). Readers should consult licensed financial advisers, solicitors, and CEA-registered property salespersons before making any property purchase decisions. Always verify current rates directly with IRAS at www.iras.gov.sg and MAS at www.mas.gov.sg.

0 Comments