Property due diligence in Singapore is the structured process of verifying every material fact about a property before you exercise the Option to Purchase (OTP). Skip it, and you risk buying a flat encumbered by a neighbour’s registered easement, a condo subject to a drainage reserve that prevents extension, or a resale HDB unit where the previous owner left behind outstanding Management Corporation fees. This guide walks you through every check — what it is, who runs it, and what a failure means for your purchase.

Quick Answer — Property Due Diligence at a Glance

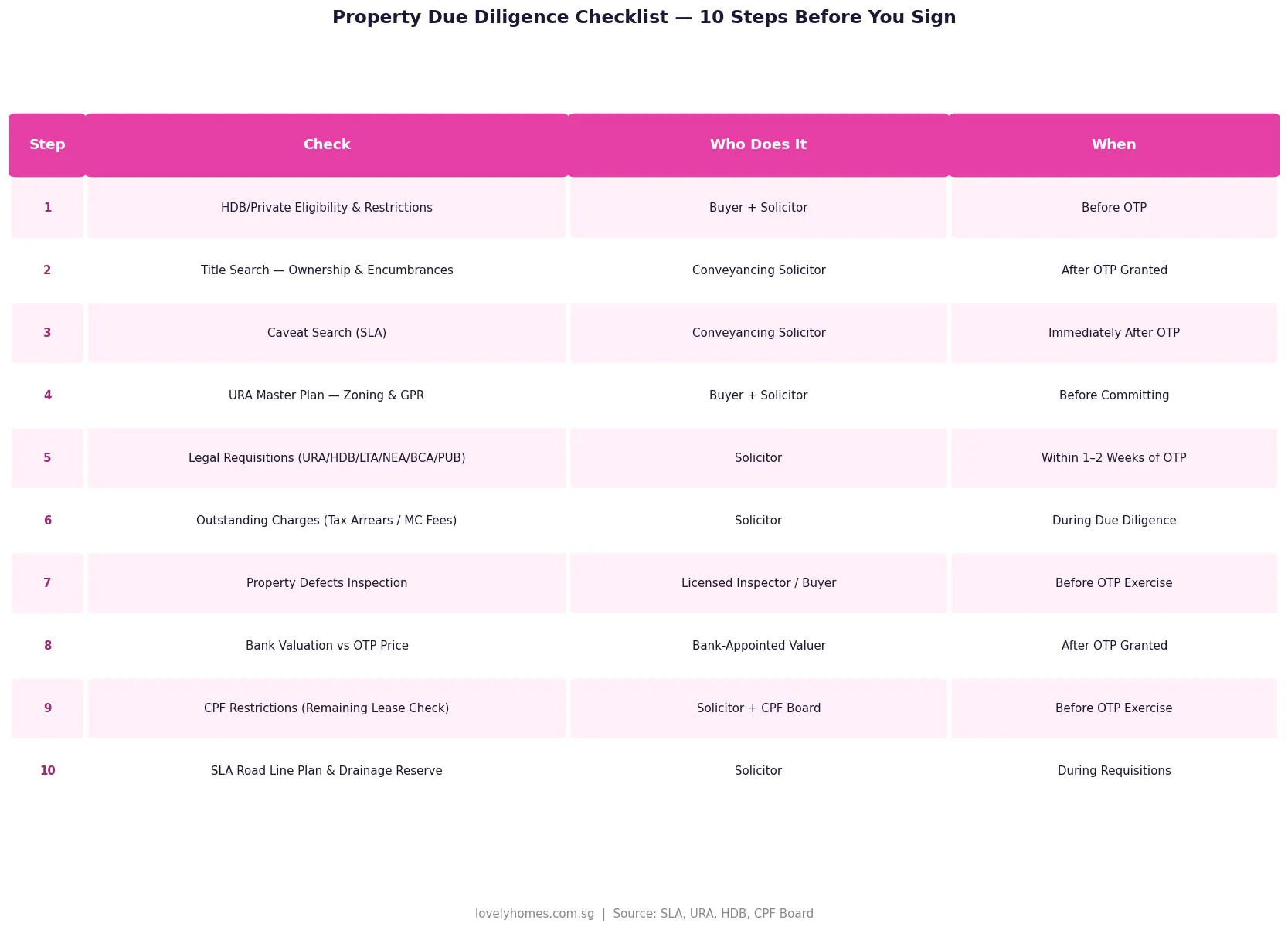

- Due diligence covers 10 distinct checks spanning legal title, planning, physical condition, and financial encumbrances.

- The title search (run by your solicitor) reveals mortgages, caveats, and encumbrances registered against the property at the Singapore Land Authority (SLA).

- URA Master Plan zoning tells you what the land is approved for — critical if you are buying a shophouse or a property in a conservation area.

- Legal requisitions go to 8–12 government agencies (URA, HDB, LTA, NEA, BCA, PUB, NParks, SCDF) and typically take 2–3 weeks to return.

- A bank valuation below your OTP price means the shortfall must be funded in cash — CPF and loan proceeds are capped at the lower of price or valuation.

- CPF withdrawal for private property is restricted if the remaining lease is short; check this before committing.

- Defects inspection costs S$400–S$800 and should always be done before exercising the OTP for a resale property.

What Is Property Due Diligence and Why Does It Matter?

In Singapore’s property market, the OTP commits you legally to the purchase once exercised. You will forfeit your option fee (typically 1% of the purchase price for private properties) if you walk away after granting. For high-value transactions, this can mean losing S$15,000–S$30,000 or more if you discover a problem after the OTP is signed but before you exercise it — and substantially more if you exercise and then discover defects or legal complications.

Due diligence is your window to uncover these problems before you are locked in. Singapore’s Torrens title system (administered by SLA under the Land Titles Act) means that most legal interests are registered on the land register and are therefore discoverable — but only if you look. Unregistered interests such as verbal agreements, side letters, or informal easements are not discoverable through a title search and represent a residual risk in all real estate transactions.

Your conveyancing solicitor handles the bulk of the legal checks once the OTP is granted. But several steps — particularly the physical inspection, the URA zoning check, and the CPF remaining-lease calculation — are things you should carry out before signing the OTP, while you still have negotiating leverage and can still walk away cleanly.

Step 1: Establishing Ownership and Basic Eligibility

Before signing anything, confirm the identity of the legal owner using the SLA’s Integrated Land Information Service (INLIS). You can pay S$5 to search by property address and obtain the registered proprietor’s name. Discrepancies between the SLA record and the seller’s identity should be flagged immediately to your solicitor. For HDB resale, log on to the HDB Resale Portal to check eligibility — specifically the Ethnic Integration Policy (EIP) quota for the block and neighbourhood, and whether the seller has fulfilled the Minimum Occupation Period (MOP) and is entitled to sell.

For private property, confirm whether there are any Qualifying Certificate (QC) obligations on the seller (relevant for foreign developer-owned properties) or any Additional Buyer’s Stamp Duty (ABSD) implications on your own buyer profile. Our ABSD Singapore 2026 Complete Guide covers this in full.

Step 2: Title Search — What the Land Register Reveals

A title search is run by your conveyancing solicitor using SLA’s land register. It reveals every registered interest on the title at that moment: mortgages, caveats, cautions, restrictions, and in some cases, easements. The search is conducted both at the time of the OTP and again shortly before completion to ensure no new interests have been registered in the interim.

Mortgages registered against the title must be discharged on completion — your solicitor will direct the sale proceeds to the seller’s bank and obtain a formal discharge before the transfer is registered in your name. Caveats lodged by the seller’s previous buyer (who never completed) must also be removed before you can take clean title. Restrictive covenants — which may limit use to residential purposes, prohibit subdivision, or require consent for structural alterations — bind all subsequent owners and can significantly affect a property’s development potential.

Step 3: Lodging Your Caveat After the OTP

Once you have signed the OTP and paid the option fee, your solicitor should lodge a caveat against the property on your behalf as soon as practicable. This caveat notifies the world that you have an equitable interest in the property as the pending purchaser. Without a caveat, a dishonest seller could theoretically sign a second OTP for the same property with another buyer, or the seller’s creditors could register a charge that clouds the title before you complete. SLA charges S$64.45 per caveat as at 2026. The caveat is removed by SLA upon completion and registration of the transfer in your name.

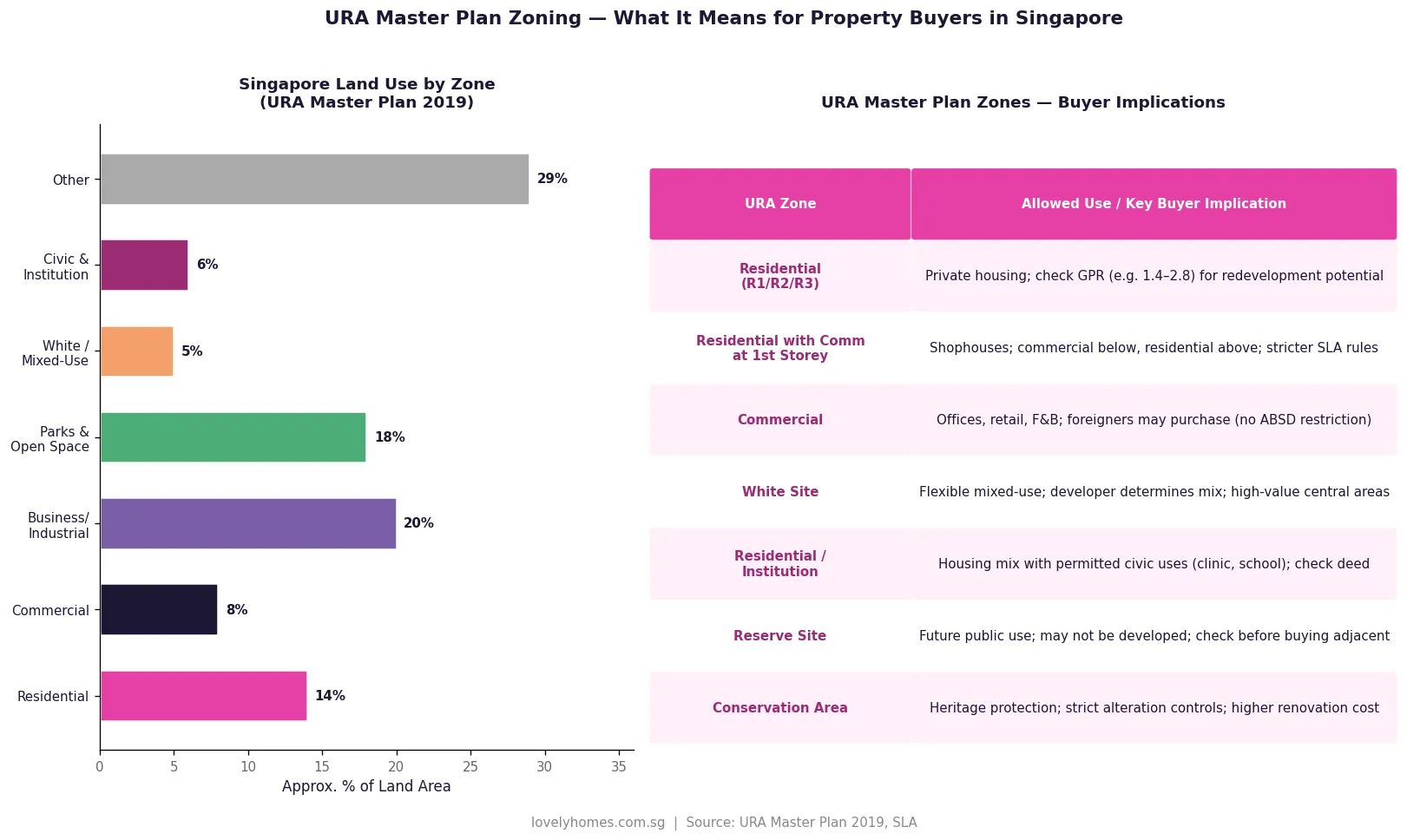

Step 4: URA Master Plan — Zoning, GPR and Allowable Use

The Urban Redevelopment Authority (URA) publishes the Master Plan 2019, which designates every parcel of land in Singapore with a zone and, for most zones, a Gross Plot Ratio (GPR). The GPR determines how much development is permitted — a site with a 1.4 GPR can have a total gross floor area of 1.4 times the land area, while a 2.8 GPR allows twice that.

For most buyers purchasing an existing strata title unit (condo, HUDC), the URA zone is primarily relevant for future redevelopment potential — a higher GPR means a more valuable en-bloc site and a potentially higher collective sale pay-out. For buyers of landed property or shophouses, the zone governs what you can build, extend, or convert. A mixed-use shophouse in a Conservation Area, for example, requires URA approval for any alteration and must retain the heritage facade — renovation costs and timelines are substantially higher.

Step 5: Legal Requisitions — Eight Government Agencies in One Sweep

Legal requisitions are formal enquiries that your solicitor sends to government agencies after the OTP is granted. They are mandatory on all private property transactions and are standard practice for HDB resale transactions as well. The agencies typically covered are URA (planning permission history, road lines), HDB (resale approval, outstanding loans), Land Transport Authority (road line plans, MRT land acquisition, drainage reserves), National Environment Agency (pollution control orders), Building and Construction Authority (structural safety notices, building plan approvals), Public Utilities Board (sewerage connections, drainage reserves), National Parks Board (gazetted trees), and Singapore Civil Defence Force (fire safety certificates). Requisitions typically take 2–3 weeks to return. A drainage reserve from PUB, for example, means a strip of land along a boundary must remain clear for drainage access — any permanent structure within it may need to be removed. These findings are not deal-breakers in themselves, but they affect what you can do with the property and should factor into your negotiation and renovation plans.

Outstanding Charges: Property Tax, Maintenance, and Sinking Fund

Two categories of financial obligation attach to a Singapore property and can, if unpaid, transfer to the new owner as a statutory charge on the land. Property tax is levied by the Inland Revenue Authority of Singapore (IRAS) annually on the Annual Value of the property. If the seller has arrears, IRAS can pursue them as a debt secured against the property. Your solicitor will obtain an IRAS property tax certificate confirming no arrears as at completion, and any balance of the current year’s tax will be apportioned between buyer and seller. Management Corporation (MCST) fees and sinking fund contributions apply to all strata-title properties. These cover building maintenance, security, and the sinking fund for major repairs. Your solicitor obtains a certificate from the MCST confirming all charges are current; any arrears are deducted from the sale proceeds.

| Charge / Obligation | Levied By | Consequence of Arrears | How Resolved at Completion |

|---|---|---|---|

| Property Tax | IRAS | Statutory charge on land; IRAS can pursue buyer | Deducted from sale proceeds; IRAS issues clearance |

| MCST Maintenance Fees | Management Corporation | Debt against property; MCST has statutory lien | Deducted from sale proceeds; MCST issues clearance |

| Sinking Fund Arrears | Management Corporation | Same as maintenance fees | Deducted from sale proceeds; MCST issues clearance |

| HDB Outstanding Loan | HDB | HDB must be paid off before title transfers | Discharged from sale proceeds at completion |

| Town Council S&CC | HDB Town Council | Council may pursue buyer; HDB will not process resale with arrears | Seller must clear all arrears before HDB processes resale |

| Statutory Agency Orders | PUB, NEA, BCA | Outstanding order may pass to new owner | Solicitor flags via requisitions; buyer negotiates with seller |

Property Defects Inspection: What to Check Before You Exercise the OTP

A physical inspection by a professional building inspector examines structural integrity, mechanical and electrical systems, water ingress, and finishes. In Singapore, professional inspection fees typically range from S$400 to S$800 for a standard condo unit and S$800 to S$1,500 for a landed property. Key areas inspected include: structural walls and columns for cracks or movement; ceiling and floor slabs for water staining indicating leaks from above; windows for proper sealing; air-conditioning systems; plumbing; electrical outlets; and tiling for hollow spots or grout failure. If the inspection reveals defects, you have three options: negotiate a price reduction reflecting the cost of repair; require the seller to make good before completion; or accept the property as-is if the defects are cosmetic only.

Bank Valuation vs OTP Price: When the Numbers Don’t Match

Your bank appoints its own valuer to assess the property’s market value independently of the OTP price you have agreed. If the bank’s valuation comes in below the OTP price, your loan and CPF usage are capped at the lower valuation figure. The shortfall must be funded entirely in cash. For example: if you agree to buy a property at S$1.5 million but the bank values it at S$1.45 million, the S$50,000 shortfall cannot be funded via CPF or loan. On top of the standard cash outlay, you must produce an additional S$50,000 in cash. To mitigate this risk: ask your solicitor to engage the bank early for an indicative valuation before you sign the OTP. Our Singapore Property Financing Guide 2026 explains LTV ratios and CPF interaction in detail.

CPF Restrictions: Remaining Lease and the Age Equation

For private property, the CPF Board imposes restrictions on how much CPF can be used depending on the property’s remaining lease. The key rule: CPF OA savings can be used up to the applicable percentage of the lower of purchase price or valuation, provided the lease covers the youngest buyer to at least age 95. Where the lease falls short of that threshold, the CPF usage limit is pro-rated. Always compute the remaining lease-to-55 figure before committing to a purchase. A 1970s leasehold development with 47 years remaining may have severe CPF restrictions that alter the entire financing arithmetic. For HDB flats, separate rules apply — we cover these in our CPF Property Usage Guide 2026.

Worked Example: Ms Yeoh’s D15 Condo Purchase

Profile: Ms Yeoh (Singapore Citizen, 38, gross income S$9,500/month), buying her first private property — a District 15 freehold 2-bedroom condo resale, 969 sqft, OTP price S$1.5 million.

Eligibility (Step 1): Freehold, no EIP or HDB restrictions. First property — ABSD S$0, BSD S$44,600 (payable via CPF).

URA zoning (Step 4): Residential (GPR 1.4, 12-storey block). No conservation area, no road line plan issues. En-bloc potential noted but not material to current purchase.

Requisitions (Step 5): PUB returns a 1.5-metre drainage reserve along the northern boundary. This affects ground-floor garden units but not Ms Yeoh’s high-floor unit. URA: no outstanding development charges. LTA: no road widening planned.

Outstanding charges: IRAS reveals S$2,400 in property tax arrears. Solicitor directs seller to clear from sale proceeds. MCST clearance: all fees current.

Defects inspection (Step 7): Professional inspector (S$550 fee) finds 3 defects: hairline crack in bedroom wall (cosmetic, repair S$200); faulty fan coil in main bedroom (repair S$400); hollow tiles in wet kitchen, 12 tiles (re-grout S$350). Ms Yeoh negotiates a S$1,000 price reduction; seller agrees, OTP price revised to S$1.499 million.

Bank valuation (Step 8): Bank values property at S$1.48 million — S$19,000 below revised OTP. Cash top-up required: S$19,000. Loan: 75% LTV of S$1.48M = S$1.11 million at 3.1% over 30 years = S$4,740/month. TDSR: S$4,740 / S$9,500 = 49.9% — below the 55% cap, PASS.

CPF (Step 9): Freehold property, no remaining-lease restriction. CPF OA balance S$85,000 used for BSD (S$44,600) and partial down payment.

Total cash outlay: 1% option fee S$14,990 + 4% exercise balance S$59,960 + valuation shortfall S$19,000 + legal fees S$4,800 + defects inspector S$550 + valuation fee S$450 = approximately S$99,750 in cash, plus S$44,600 CPF for BSD.

Why This Matters for Singapore Property Buyers

Singapore’s regulatory framework provides unusually strong protections compared to other property markets in the region. SLA’s Torrens system gives indefeasibility of title — once a transfer is registered, you generally cannot be dispossessed by a prior unregistered interest. But indefeasibility does not protect against interests that were registered before your title, or against physical defects that no government agency records. The combination of high transaction taxes (BSD up to 6% plus potentially ABSD), legal costs, renovation costs, and agent commissions means that the total cost of getting a Singapore property transaction wrong can easily exceed S$100,000 on a S$1.5 million purchase. Due diligence is genuine risk management, not a bureaucratic hurdle.

International buyers, particularly those from markets where verbal agreements are common and title insurance is the norm, should note that Singapore does not have a title insurance market in the US sense. Your protection comes from the rigour of the Torrens register and from the due diligence process your solicitor runs. Engaging an experienced Singapore-qualified conveyancing solicitor is arguably the most important due-diligence step of all. For the full conveyancing process, see our Singapore Property Conveyancing Guide 2026.

What Might Come Next: Digital Due Diligence and Faster Requisitions

SLA has been progressively digitising Singapore’s land register and making INLIS data more accessible. The OneMap platform (jointly maintained by SLA and the Singapore Government) now overlays URA Master Plan zoning, road line plans, and SLA land boundaries on a single geospatial interface, reducing the time needed to assemble basic due diligence information. Looking forward, it is plausible that AI-assisted requisition processing could reduce the current 2–3-week response time for legal requisitions to days, allowing faster and more efficient property transactions without compromising thoroughness. The Ministry of Law has also been exploring reforms to simplify conveyancing procedures, though no specific timeline has been announced as at mid-2026.

Frequently Asked Questions

Can I do the due diligence myself, or do I need a solicitor?

You can and should personally carry out Steps 1, 4, and 7 (ownership check via INLIS, URA zoning check, and physical inspection) before signing the OTP. However, Steps 2, 3, 5, 6, 8, and 10 require a licensed solicitor who has access to SLA’s full search system and the authority to issue formal legal requisitions to government agencies. Attempting to run title searches or lodge caveats without a solicitor is inadvisable and, for most instruments, not legally permissible for a layperson. Solicitor fees for conveyancing typically range from S$2,500 to S$6,000 depending on the transaction value and complexity.

What if the legal requisitions reveal a drainage reserve on the property?

A drainage reserve means PUB has a right of access over a strip of land (typically 1–3 metres wide along a boundary) for drainage maintenance. You cannot build permanent structures over the reserve. For high-floor condo units, this is generally not material — it affects the site boundary but not your unit. For landed properties or ground-floor units with garden access, it can restrict extension plans. You should factor this into your renovation budget and negotiate accordingly. A drainage reserve does not void the purchase and is not grounds to rescind the OTP, but it may affect the market value of the property if significant.

How long do I have to exercise the OTP after signing it?

For private resale property, the OTP is valid for 14 days from the date of grant (unless the parties agree a longer period). Within those 14 days, you must exercise the OTP by signing the acceptance copy and paying the exercise fee (typically 4% of the purchase price for private property, making the total deposit 5%). You cannot extend the OTP unilaterally — it requires the seller’s agreement. This 14-day window is precisely why you should complete the physical inspection and URA zoning check before signing the OTP, not after. For HDB resale, the OTP validity period is also typically 14 days from the date of grant.

Does due diligence differ for HDB resale flats?

Several checks are HDB-specific. For resale HDB flats, you must verify the seller has fulfilled the MOP (5 years for standard BTO and resale flats, 10 years for Prime Location Public Housing flats), check the Ethnic Integration Policy quota for the block and neighbourhood, confirm there are no outstanding Town Council service and conservancy charges, and ensure the seller’s HDB loan (if any) will be fully discharged at completion. Legal requisitions for HDB resale are processed through the HDB Resale Portal rather than through individual agency requisitions. You should also confirm the flat’s remaining lease and its impact on CPF and loan eligibility. Our HDB Resale Buying Process Guide 2026 covers the full HDB-specific process.

Can a seller misrepresent the condition of the property and what recourse do I have?

Singapore property transactions follow the principle of caveat emptor — let the buyer beware — for physical condition. However, sellers have a duty not to make fraudulent or negligent misrepresentations about material facts. If a seller actively conceals a known structural defect (for example, paints over a crack that was flagged in a prior structural report) and you can prove this, you may have a claim under the Misrepresentation Act or in tort. The practical challenge is proving knowledge and concealment. This is why a professional defects inspection creates a contemporaneous record before completion. For serious defects discovered after completion, seek legal advice promptly as time limits apply.

Do I need a separate building inspection for a new launch condo?

For new launch properties, you take possession at the point of vacant possession, typically 3–5 years after the OTP for off-plan purchases. At vacant possession, the developer issues a formal defects list period (often 12 months) during which they must rectify any defects reported. You should still conduct a thorough inspection at vacant possession with a professional inspector — the developer’s obligation to rectify only applies to defects formally reported within the defects period. After the defects period expires, rectification becomes your responsibility and can be costly for structural or waterproofing issues.

What is the SLA Road Line Plan and why does it matter for landed property buyers?

The SLA Road Line Plan (RLP) shows the planned final boundary of a road adjacent to or affecting the property. If your property sits within the planned road reserve, a portion of your land — typically at the front setback — may eventually be acquired by LTA for road widening. The acquisition is compulsory and is compensated at market value under the Land Acquisition Act, but the timing is uncertain. For landed properties, an RLP reservation affects how close to the boundary you can build and may reduce the effective usable area of the site. Your solicitor flags this in the LTA requisition response, and you should factor it into your purchase decision accordingly.

Related Articles

- Singapore Property Conveyancing Guide 2026: Complete Step-by-Step Process from OTP to Keys

- Singapore Private Property Buying Process 2026: Complete Step-by-Step Guide

- Singapore CPF Property Usage Guide 2026: OA Withdrawal, Accrued Interest and Retirement Sum Rules

- Singapore Property Financing Guide 2026: LTV, TDSR, MSR and HDB vs Bank Loan Explained

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Property Agent Guide 2026: CEA Rules, Commissions and Your Rights

- Singapore HDB Resale Buying Process Guide 2026: Step-by-Step from HFE to Keys

Disclaimer: This article is for general informational purposes only and does not constitute legal, financial or professional advice. Property transactions in Singapore involve complex legal and financial considerations. Always engage a Singapore-qualified solicitor, a licensed property agent, and a bank or financial adviser for advice specific to your circumstances. For the authoritative position on any matter, refer to the Singapore Land Authority (sla.gov.sg), the Urban Redevelopment Authority (ura.gov.sg), HDB (hdb.gov.sg), the Inland Revenue Authority of Singapore (iras.gov.sg), and the CPF Board (cpf.gov.sg).

0 Comments