Quick Answer: HDB MOP Singapore 2026

- Standard HDB BTO and resale flats have a 5-year Minimum Occupation Period (MOP) counted from the date you collect the keys (TOP/possession date), not from when you sign the Sales & Purchase agreement.

- Plus and Prime (PLH) classification flats introduced from the August 2024 BTO exercise have a longer 10-year MOP, reflecting their more desirable locations and heavier subsidy.

- During MOP, you cannot sell your flat, rent out the entire flat, or purchase any other residential property in Singapore — including private property or an overseas residential investment.

- You CAN rent out individual HDB bedrooms with prior HDB approval, and run approved home-based businesses from your flat during MOP.

- Executive Condominiums (ECs) have a 5-year MOP before they can be sold to Singapore Citizens and PRs, and a 10-year window before they are fully privatised and open to foreign buyers.

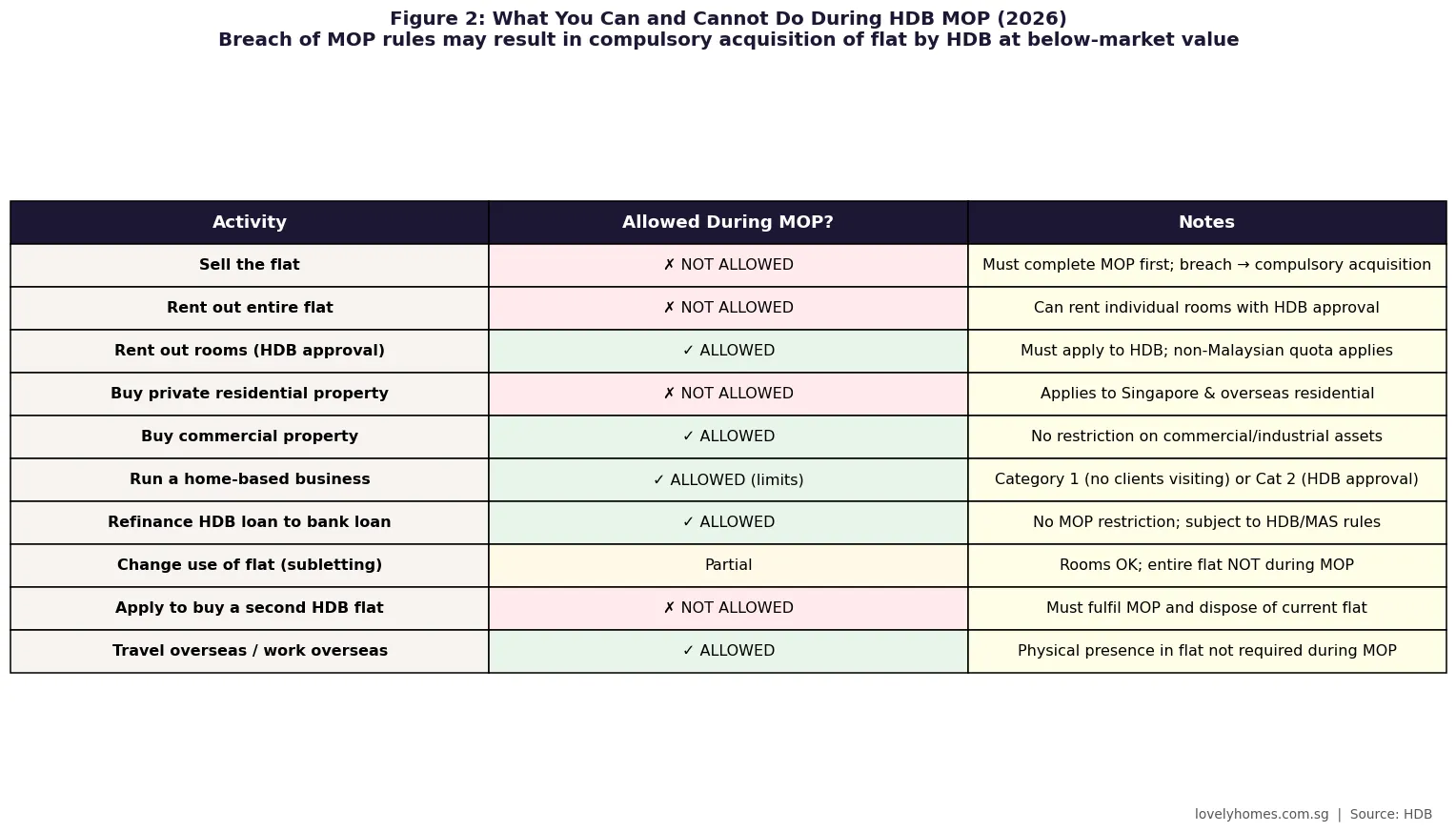

- Breaching MOP rules can result in compulsory acquisition of the flat by HDB at a value set by HDB — typically below market value. Criminal penalties may also apply under the Housing & Development Act.

- After MOP, you can sell the flat, upgrade to a private property, and — for HDB sellers upgrading to private — apply for ABSD remission if you complete the sale within 6 months of purchasing the private property.

What Is the HDB Minimum Occupation Period (MOP)?

The Minimum Occupation Period (MOP) is a statutory rule administered by the Housing & Development Board (HDB) that requires flat owners to physically occupy their HDB flat for a minimum period before they can sell it on the open market, rent it out entirely, or purchase other residential property in Singapore. The MOP is a key plank of Singapore’s public housing philosophy: HDB flats are subsidised national assets intended primarily as homes rather than investment vehicles, and the MOP is one mechanism through which HDB ensures flats remain owner-occupied.

The MOP was first introduced in the 1970s and has been refined multiple times since, most recently in 2024 with the introduction of the Plus and Prime flat classifications under the enhanced HDB framework. Understanding which MOP applies to your flat — and what you can and cannot do during that period — is critical before making any property decisions.

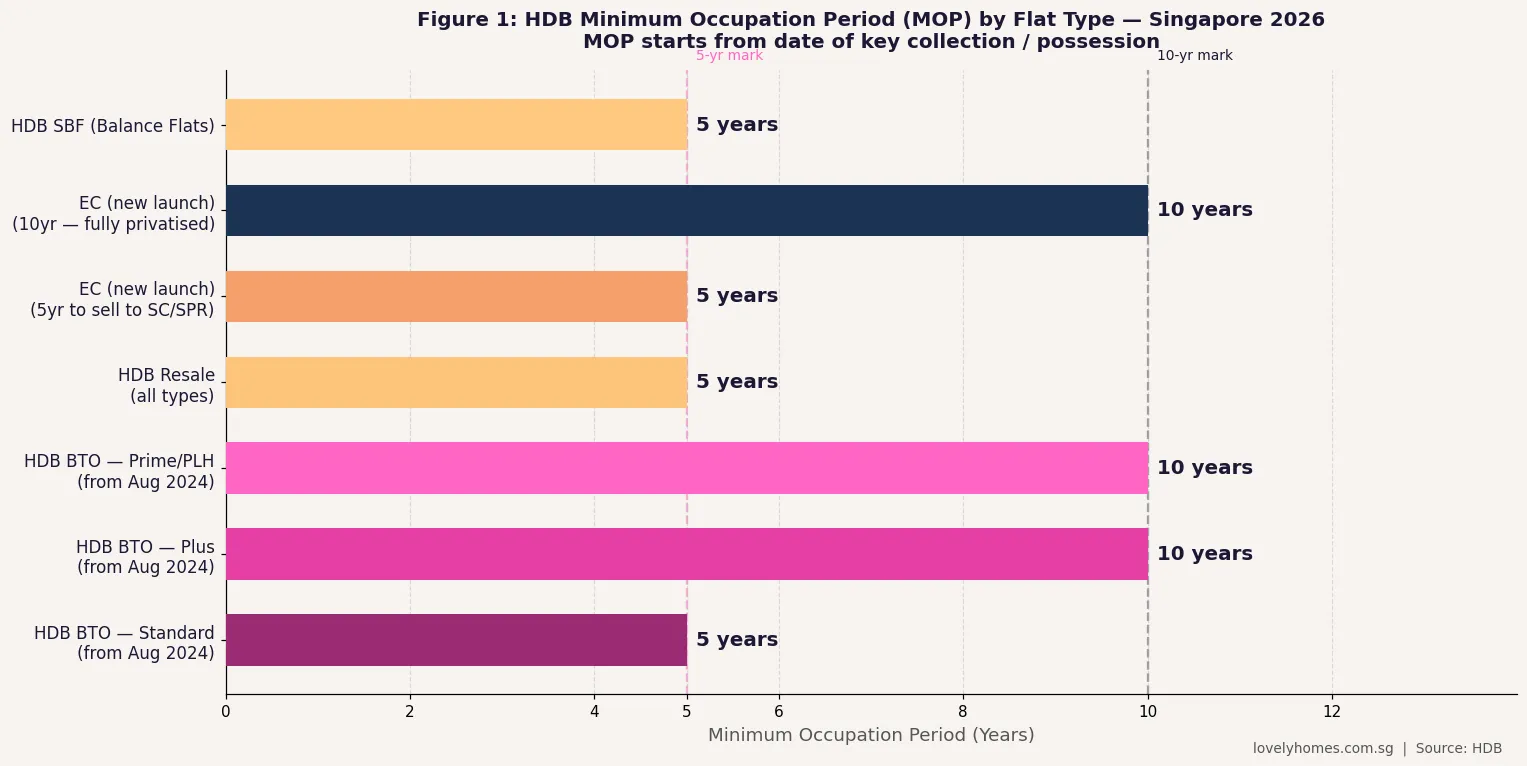

MOP Duration by Flat Type (2026)

| Flat Type | MOP Duration | MOP Start Date | Notes |

|---|---|---|---|

| Standard BTO Flat | 5 years | Date of key collection | Applies to all pre-Aug 2024 BTO; continued for Standard classification from Aug 2024 |

| Plus Classification BTO Flat | 10 years | Date of key collection | From Aug 2024 BTO exercise; typically near MRT/town centres; subsidy clawback on resale |

| Prime / PLH Classification BTO Flat | 10 years | Date of key collection | Central-location flats; subsidy clawback ~6–9% of resale price; income ceiling at resale |

| HDB Resale Flat | 5 years | Date of resale completion | Fresh 5-year MOP runs from the date the resale transaction is completed (not from when the previous owner moved in) |

| Executive Condominium (EC) | 5 years → 10 years | Date of TOP | At 5yr can sell to SC/PR; at 10yr fully privatised — open to foreigners (60% ABSD applies) |

| HDB Sale of Balance Flats (SBF) | 5 years | Date of key collection | SBF flats unsold from previous BTO exercises; Standard classification MOP applies |

Important note on the Plus and Prime MOP: The new 10-year MOP for Plus and Prime flats applies only to flats launched under the August 2024 BTO exercise onwards. Flats purchased in earlier exercises, even if they are in desirable locations that would now be classified as Plus or Prime, retain their original 5-year MOP. To confirm which classification applies to your flat, check your HDB flat portal or the original flat details under your BTO exercise.

What You Cannot Do During the HDB MOP

Selling the Flat

You cannot sell your HDB flat on the open resale market before your MOP is complete. This applies even if you face financial hardship — HDB does not grant MOP exemptions for distressed sellers. The only exception is a compulsory acquisition by HDB or by the State for public purposes, which is not initiated by the flat owner. If you attempt to sell before MOP, the transaction will be rejected by HDB’s system during the eligibility check.

Renting Out the Entire Flat

Renting out the entire flat (as a whole unit) is not allowed during MOP. This applies to both short-term and long-term rental arrangements. Platforms such as Airbnb and similar short-term rental services are also not permitted on HDB flats — the minimum lease tenure for any rental on HDB flats is three consecutive months. After MOP, whole-flat rental is allowed with HDB prior approval and is subject to the non-Malaysian foreign tenant quota.

Purchasing Other Residential Property in Singapore

During MOP, you and your co-owners on the flat cannot purchase any other private residential property in Singapore. This restriction extends to new launch condominiums, resale condominiums, Executive Condominiums (as a new buyer), landed property, and private apartments. Purchasing a second HDB flat is also not allowed during MOP.

Crucially, HDB’s definition of “residential property” in the MOP context refers to Singapore property only. There is no restriction on purchasing overseas residential property during MOP — only Singapore residential property is covered.

Purchasing a Second HDB Flat

HDB’s policy generally allows only one HDB flat per family nucleus at any time. Applying for a second BTO, SBF, or resale flat during MOP is not permitted. Once MOP is fulfilled, you may apply for a second HDB flat under specific schemes (e.g., the Studio Apartment scheme for elderly, or a new BTO after disposing of the first flat).

What You CAN Do During the HDB MOP

Rent Out Individual Rooms

Renting out individual bedrooms in your HDB flat (while you continue to live in the flat) is permitted during MOP, subject to HDB’s prior written approval. You must apply through the HDB Flat Portal before subletting. Each tenancy must be for a minimum of six months (for whole-flat subletting after MOP) or at least three months for room rental. Non-Malaysian foreign tenants are subject to the non-Malaysian quota: a maximum of two non-Malaysian foreign tenants per flat in the same block is the guideline, though HDB publishes real-time quota data by block.

Run Approved Home-Based Businesses

HDB permits flat owners to operate home-based businesses during MOP, subject to type and scale restrictions. Category 1 businesses (no employees visiting, no clients visiting, no signage) are allowed without prior approval. Category 2 businesses (up to two non-resident employees, clients may visit in small numbers) require prior approval from HDB. Manufacturing, food businesses, or any business that involves goods storage, noise, or frequent deliveries is not permitted.

Refinance to a Bank Loan

Switching from an HDB housing loan to a bank loan (or switching between bank loan packages) is allowed during MOP. There is no MOP restriction on refinancing decisions, and many flat owners take advantage of the 5-year MOP period to monitor interest rate movements and refinance when rates are favourable. MAS’s LTV and TDSR rules govern the refinancing terms.

When Does the MOP Start and End?

The MOP starts from the date you collect your keys (for BTO and SBF flats, this is the TOP date; for resale flats, this is the date of completion of the resale transaction — both milestones are reflected in your HDB Flat Portal). The MOP does not start from the date you sign the Sales & Purchase Agreement or from the date you pay the initial booking fee.

You can check your MOP end date in the HDB Flat Portal under “My Flat” → “Purchase Details”. The portal clearly shows whether your MOP has been fulfilled. Do not rely on verbal estimates from agents or CPF advisers — always verify on the portal directly.

One nuance: physical occupation is expected during MOP. HDB conducts periodic checks to ensure flat owners are residing in the flat. Extended overseas absences without HDB’s knowledge have been cited in compulsory acquisition cases. If you must be overseas for an extended period (e.g., for work), inform HDB and keep the flat in a lived-in condition.

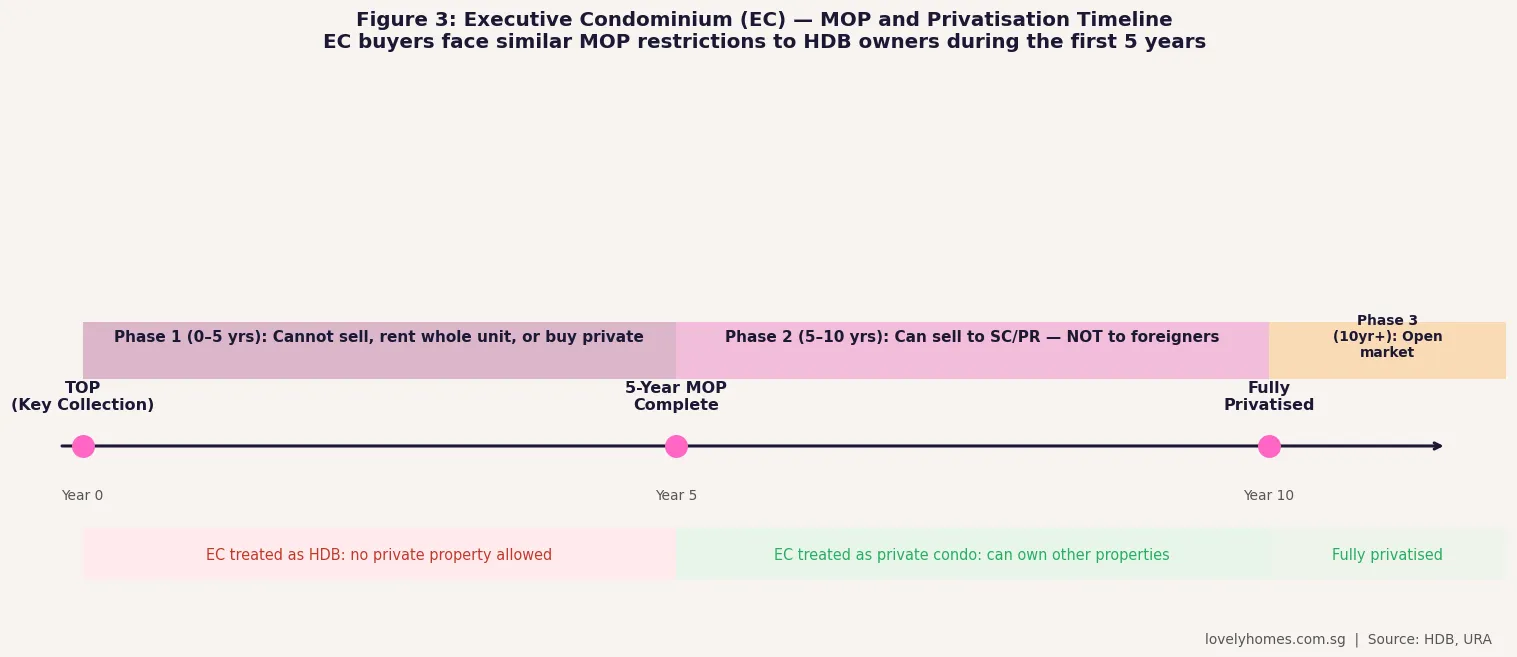

Executive Condominium (EC): The Hybrid MOP Rules

Executive Condominiums occupy a hybrid position between public and private housing. They are built by private developers but are sold at a subsidised price to qualifying buyers (income ceiling S$16,000 per month household income as of 2026). From a MOP standpoint, ECs are treated like HDB flats for the first 5 years:

During years 1–5: EC owners cannot sell their unit, rent out the whole unit, or purchase any other Singapore residential property. The rules are identical to HDB MOP. Critically, the 5-year MOP runs from the TOP date, not the booking date — for large EC projects, this can mean a 3–4 year gap between booking and TOP, followed by 5 more years of MOP, making the effective holding period 8–9 years from initial purchase commitment.

After year 5 (first privatisation): The EC can be sold on the open resale market to Singapore Citizens and Singapore PRs. It cannot yet be sold to foreigners, and ECs in the first 5–10 year window are not listed on the private market as “privatised condos” — they trade in a narrower SC/SPR market. ABSD rules for the buyer apply (5% for PR 1st property, 30% for PR 2nd+, etc.).

After year 10 (full privatisation): The EC is fully privatised and treated identically to a private condominium. Foreigners may purchase it, though the 60% foreigner ABSD applies. Owners may also rent the entire unit without prior HDB approval at this stage.

Plus and Prime Flat Additional Restrictions After MOP

The 2024 housing framework introduced substantive additional conditions for Plus and Prime classification flats beyond just the longer 10-year MOP. These are restrictions that run with the flat even after MOP and affect future resale:

Subsidy clawback: When you sell a Plus or Prime flat after your MOP, HDB claws back a portion of the subsidy embedded in the original purchase price — approximately 6–9% of the resale price, payable to HDB. This clawback is calculated as a percentage of the resale transaction price, not the original purchase price, so it increases in dollar terms as the flat appreciates.

Income ceiling for buyers: Buyers of Plus and Prime resale flats are subject to an income ceiling (the ceiling is the same as for BTO buyers — S$14,000/month for 4-room and larger Plus flats as of 2026). This narrows the pool of eligible resale buyers and may dampen price appreciation relative to Standard flats.

Ethnic Integration Policy (EIP): As with all HDB resale flats, EIP quotas apply — both block and neighbourhood levels. Buyers must check the relevant block’s EIP availability before submitting an offer.

After MOP: Your Property Upgrade Options

Once your MOP is fulfilled, your options expand significantly. The most common upgrade path is from HDB flat to private condominium. The timing of this upgrade carries stamp duty implications:

Option A — Sell HDB first, then buy private: You clear the HDB flat, receive sale proceeds (net of CPF refund), and purchase the private property as a “first property” — no ABSD for SC buyers, 5% ABSD for PR buyers. This is the most common and financially efficient path but requires temporary accommodation between the two transactions.

Option B — Buy private first, then sell HDB (concurrent ownership): As an SC buying private property while still owning an HDB flat (post-MOP), you pay 20% ABSD on the private property purchase. You then have six months from the private property’s completion (or from the purchase date for resale private properties) to sell the HDB flat and apply for an ABSD remission from IRAS. If the HDB is sold within six months, IRAS refunds the 20% ABSD. If you miss the six-month window, the 20% ABSD is forfeited.

The six-month window starts from either the issue of Temporary Occupation Permit (TOP) for a new private property or the date of exercise of the OTP for a resale private property. Given the complexity of timing, many HDB upgraders consult a lawyer and financial adviser before committing to Option B.

The 15-Month Wait-Out Period: From Private Back to HDB

The wait-out period is often confused with MOP. They are different rules targeting different situations. The 15-month wait-out period (introduced in September 2022) applies to private property owners who want to purchase an HDB resale flat. If you own or recently disposed of a private property, you must wait 15 months from the date of disposal before you can purchase an HDB resale flat.

This rule does not apply to HDB MOP — it is a separate downstream restriction. For example, if you complete your HDB MOP, sell your HDB flat, buy a private condo, and then later want to downgrade back to HDB, you must wait 15 months after selling the private condo before buying an HDB resale flat. This rule applies to both SC and PR private property owners.

Worked Example: The Tan Family’s Upgrade Journey

Mr and Mrs Tan (both Singapore Citizens) purchased a 4-room BTO flat in Punggol under the Standard classification in September 2019. They collected their keys in August 2021. Their MOP end date is therefore August 2026 — five years from key collection.

In March 2026, Mrs Tan checks the HDB portal and sees MOP will end in 5 months. The couple begin their private condo search. They find a 3-bedroom OCR resale condo in Jurong East priced at S$1.5M in June 2026.

They choose Option B (buy private first). As SC buying a second property: BSD ~S$42,600 + ABSD 20% = S$300,000. They pay S$342,600 in stamp duties. Their flat is still within MOP (keys August 2021, MOP August 2026 — they are just before MOP end), so HDB must confirm MOP end before they list the flat for sale.

After August 2026 (MOP fulfilled), they list their HDB flat. Sell it in October 2026 for S$780,000 — within the 6-month window from the condo OTP exercise date of June 2026. IRAS refunds the S$300,000 ABSD. Net stamp duty retained: S$42,600 BSD only. The family books temporary accommodation for 2 months while bridging the purchase and sale timelines.

Total net proceeds from HDB: S$780,000 − CPF refund S$220,000 (principal + accrued interest) − agent 1% S$7,800 − legal S$2,500 = net S$549,700 cash. The upgrade is financially viable.

Will MOP Rules Change?

The 10-year MOP for Plus and Prime flats is a relatively recent policy (from August 2024) and unlikely to be rolled back in the near term. If anything, the trend in Singapore public housing policy has been toward tightening MOP and adding post-MOP conditions rather than relaxing them, as the government works to ensure HDB flats remain primary homes rather than investment properties. The subsidy clawback mechanism for Plus and Prime flats may be extended to more flat types if HDB determines that Standard flat resale prices are diverging too sharply from BTO prices in certain areas. Buyers should model their long-term exit strategy under current rules and build in buffer for possible tightening.

Frequently Asked Questions

Can I stay overseas during my HDB MOP?

You are expected to physically occupy the flat during MOP, but there is no absolute rule against overseas travel. Extended absences (months or years) without HDB’s knowledge can attract scrutiny, and in confirmed cases of non-occupation, HDB may commence compulsory acquisition proceedings. If you need to relocate overseas temporarily for work (e.g., on a company secondment), inform HDB in writing and keep the flat utilities active. HDB conducts inspection exercises and spot checks and has compulsorily acquired flats where owners were clearly not residing in them during MOP.

Does my MOP reset if I add or remove an owner from the flat?

No — adding or removing an owner (for example, through marriage or divorce) does not reset the MOP clock. The MOP continues to run from the original key collection date. However, any change of ownership within MOP is a restricted transaction and must be approved by HDB. Not all ownership changes are approved during MOP — for example, transferring a flat to an ineligible person would be rejected. Consult HDB or a lawyer before any ownership change within the MOP window.

Can I buy an overseas investment property during MOP?

Yes. The HDB MOP restriction applies only to Singapore residential property. There is no restriction on purchasing overseas property (residential or commercial) during MOP. You are not required to declare overseas property purchases to HDB. However, if you are financing an overseas property purchase with a Singapore bank loan, that loan will be factored into your TDSR for future Singapore loan applications. From a Singapore tax perspective, rental income from overseas property is taxable in Singapore as foreign-sourced income if remitted to Singapore.

What happens if I breach the MOP?

A breach of MOP (typically: selling the flat, subletting the entire flat, or buying other residential property in Singapore without completing MOP) can result in HDB compulsorily acquiring the flat. HDB sets the acquisition price, which is typically the assessed market value minus a penalty deduction — in practice, this means the owner receives significantly less than the open-market value they would have received after MOP. In the most serious cases involving deliberate deception or fraud (e.g., falsely declaring occupancy), criminal charges may be brought under the Housing & Development Act, which carries fines of up to S$5,000 and/or imprisonment.

Does MOP apply to inherited HDB flats?

If you inherit an HDB flat from a deceased owner, the MOP of the original owner does not transfer to you as a fresh 5-year obligation. Instead, the inherited flat is subject to HDB’s estate rules — the eligible inheritor (e.g., a spouse or child who meets eligibility criteria) may retain the flat. If the inheritor already owns a flat, they may need to dispose of one within six months. Inherited flats that have not yet met MOP at the time of death are subject to HDB’s direction — in practice, HDB often allows the eligible inheritor to complete the remaining MOP. Always consult HDB’s estate administration team for inherited flat cases.

Can I buy a private property if my HDB is still within MOP and my spouse is not on the HDB title?

No — the restriction applies to the entire family nucleus (owner and spouse / co-habitant), not just the named owners on the HDB title. If one spouse is within MOP on an HDB flat, the other spouse (even if not on the HDB title) is also restricted from purchasing Singapore residential property. HDB looks at the family nucleus holistically. Attempting to buy private property in a non-owning spouse’s name to circumvent MOP is a known scheme that HDB and IRAS are alert to — it will be scrutinised and may result in both the stamp duty assessment and a referral for investigation.

Is there a MOP for HDB shophouses or commercial units?

No. MOP is specific to HDB residential flat units. HDB shophouses (commercial properties on the ground floor of HDB blocks) are governed by different rules and do not carry a MOP. Commercial properties generally do not have any MOP equivalent — you can sell or rent them freely at any time after purchase. The restrictions and ABSD rules that apply to residential property do not apply to commercial property purchases.

Related Articles

- Singapore HDB CPF Housing Grants Guide 2026: EHG, Family Grant, PHG

- Singapore Condo Buying Process 2026: Step-by-Step Guide

- Singapore First-Timer Home Buyer Complete Guide 2026

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Executive Condominium Buying Guide Singapore 2026

- Singapore HDB Inheritance and Transfer Guide 2026

Disclaimer

This article provides general information about HDB MOP rules as at July 2026 and is not legal or financial advice. MOP durations, clawback percentages, and related policy conditions may change. Always verify current MOP status for your flat at hdb.gov.sg and check the specific BTO exercise details in your Lease Agreement. For estate planning, inheritance, and structural ownership changes, consult a Singapore-qualified lawyer. For ABSD remission eligibility, consult IRAS at iras.gov.sg.

Click anywhere to close

0 Comments