Orchard Road Singapore 2026: D09 Prices, Luxury Living & Investment Analysis

⚡ Quick Answer — Orchard Road Property 2026

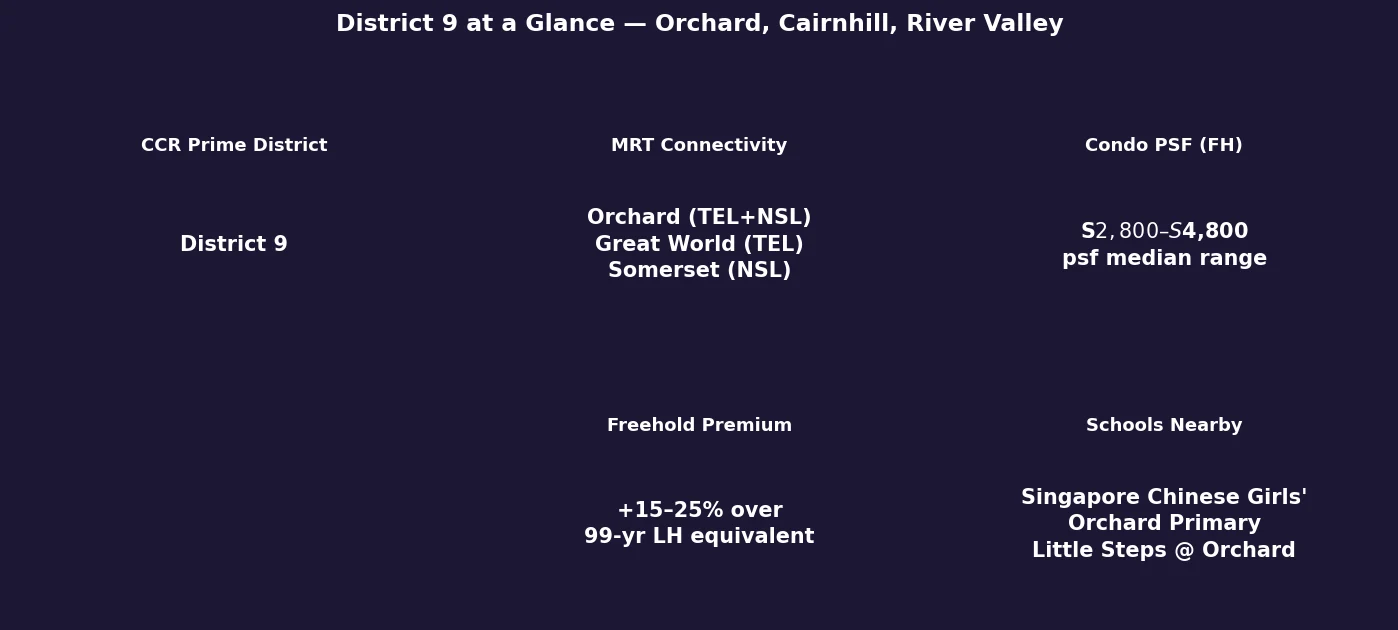

- Orchard Road sits in District 9 (D09), part of Singapore’s Core Central Region (CCR) — the island’s premier luxury residential address.

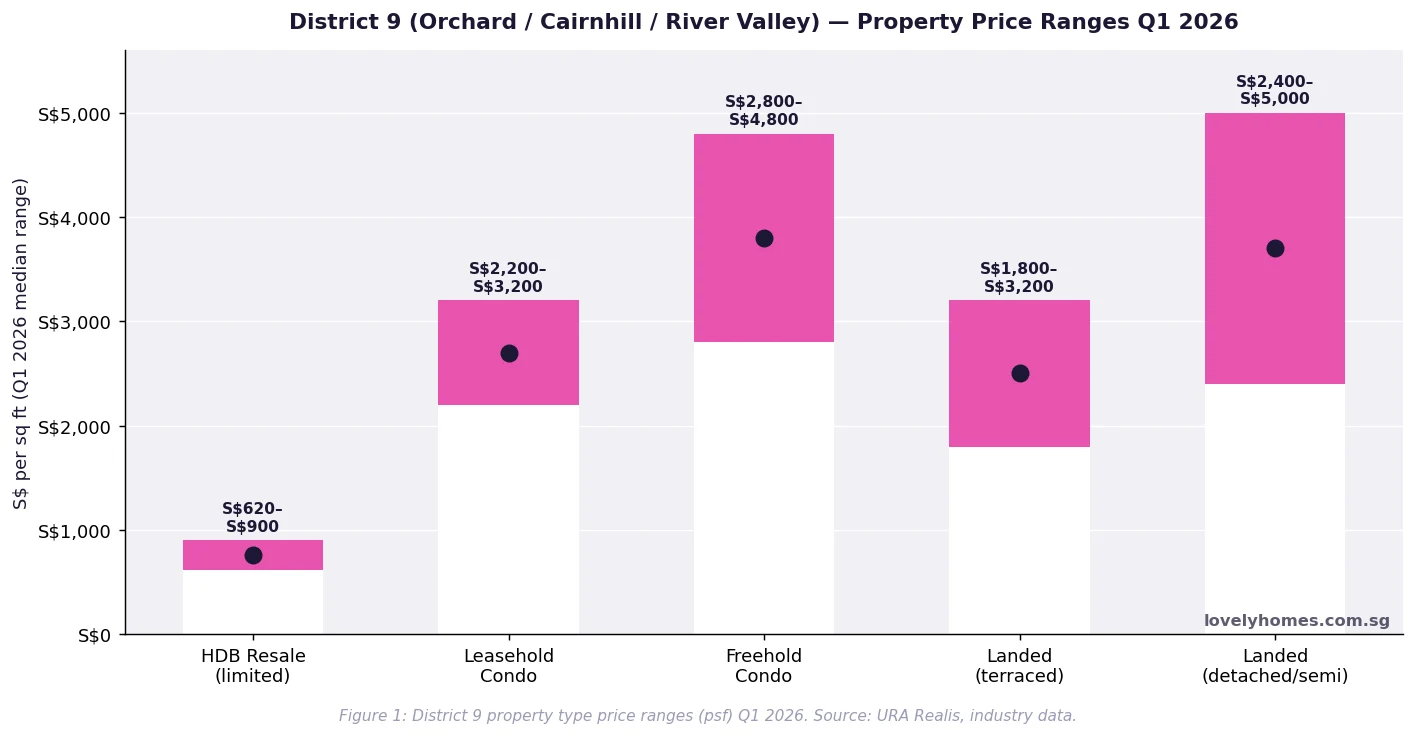

- Freehold condo median prices range from S$2,800 to S$4,800 psf in 2026; leasehold units fetch S$2,200–S$3,200 psf.

- TEL’s Orchard and Great World stations now give the precinct triple MRT access (Thomson–East Coast Line, North–South Line).

- Gross rental yields average 2.5–3.2% — lower than OCR but underpinned by multinational corporate and diplomatic demand.

- Freehold properties command a 15–25% premium over equivalent leasehold units in the same sub-district.

- HDB supply is extremely limited (old Rochor/ Cairnhill estate stock only) — almost all residential stock here is private condo or landed.

- ABSD applies to all purchases: Singapore Citizens buying a second property pay 20%, Permanent Residents 25% (first), foreigners 60%.

- Capital appreciation over the 2019–2026 period has averaged +5–7% per annum for freehold D09 condos in the mid-luxury tier.

What Is District 9 and Why Does Orchard Road Matter?

District 9 — officially encompassing the planning areas of Orchard, Cairnhill, Leonie Hill, and River Valley — is Singapore’s best-known luxury address. The Orchard Road shopping belt, which stretches roughly 2.2 kilometres from Tanglin Road to Dhoby Ghaut, is both a retail landmark and the spine around which the surrounding residential market is priced. Properties within walking distance of Orchard MRT command a persistent scarcity premium: supply is structurally constrained by conservation zones, a dense grid of existing freehold developments, and the absence of Government Land Sales (GLS) Confirmed List sites since 2019.

The Urban Redevelopment Authority (URA) classifies D09 as part of the Core Central Region (CCR) — the most tightly regulated of Singapore’s three residential market segments. CCR properties attract the highest stamp duties for non-citizens and are subject to the full suite of Additional Buyer’s Stamp Duty (ABSD) cooling measures introduced and refined between 2011 and 2023.

Property Landscape: What You Can Buy in D09

The D09 residential market is almost entirely composed of private non-landed and landed properties. The key segments are:

Leasehold condominiums (99-year): typically newer developments built post-2000, PSF ranges S$2,200–S$3,200 in 2026. Examples include Highline Residences and 1919 (formerly Noisy Elephant). Leasehold developments offer more flexibility in financing but carry a lease-decay risk that buyers must factor in for re-sale after 2050.

Freehold condominiums: the dominant premium tier, with PSF ranging S$2,800–S$4,800 depending on storey, renovations, and project prestige. Established freehold addresses along Cairnhill, Emerald Hill, and Orchard Boulevard include projects whose 30-to-40-year-old vintages still command strong re-sale premiums due to their perpetual tenure and walk-to-Orchard-MRT location.

Landed (terrace and semi-detached): a small but significant segment, with terrace houses along Cairnhill Road and Ardmore Park environs transacting at S$1,800–S$3,200 psf on land. Semi-detached and detached bungalows (Good Class Bungalow fringe) sit at S$2,400–S$5,000+ psf on land. Foreigners are generally not permitted to purchase landed property in Singapore without Ministerial approval.

HDB resale flats: extremely rare in D09. The few remaining HDB blocks near Cairnhill and the old Rochor estate are among the most idiosyncratic properties in Singapore — priced S$620–S$900 psf due to their central location, but subject to stringent Ethnic Integration Policy (EIP) quotas and conventional HDB resale restrictions.

D09 at a Glance: Key Facts for Buyers

MRT Connectivity: Why the TEL Changed Everything

For most of Singapore’s modern history, D09’s primary MRT connection was Orchard station on the North–South Line (NSL), opened in 1987. The Thomson–East Coast Line (TEL) Stage 3, which began operating in November 2022, transformed connectivity in the district in two significant ways.

First, Orchard station became an interchange between the NSL and TEL — dramatically cutting travel times to Thomson, Bishan, Woodlands, and the eastern corridor without changing trains. Second, Great World station (TEL), opened in 2022, gave the River Valley sub-district its own direct MRT access for the first time, adding a meaningful premium uplift to residential properties within 400 metres of the station. Industry estimates suggest the Great World TEL opening contributed a 6–10% PSF uplift to the immediately surrounding catchment.

Somerset station (NSL) anchors the Orchard Road retail strip’s southern end and serves as a secondary access point for Orchard sub-market properties. The combined station density — Orchard, Somerset, and Great World within roughly 1.5 km — gives D09 an MRT connectivity score that few other Singapore districts can match.

Rental Market and Investment Yields

D09 draws a high proportion of expatriate tenants from multinational corporations (particularly financial services, technology, and professional services firms) who prefer central locations with proximity to international schools and the CBD. This profile supports relatively stable rental demand even when broader market rental cycles soften.

Gross rental yields in D09 average 2.5–3.2% for condominiums in 2026. By comparison, OCR districts such as D27 (Yishun) or D23 (Bukit Panjang) offer 3.4–4.2%. The D09 yield discount is structural: absolute capital values are higher, which compresses the yield percentage even when absolute rental income is also elevated. A two-bedroom freehold condo at S$2.5M might fetch S$7,500–S$9,000 per month in rent — a 3.6–4.3% gross yield in dollar terms, but modest relative to the entry price.

Net yields after management fees, maintenance, property tax, and vacancy allowances typically run 1.8–2.5%. Investors in D09 are largely buying for capital appreciation and portfolio positioning rather than yield maximisation.

Summary Table: D09 Property at a Glance

| Property Type | Typical PSF (2026) | Tenure | Gross Yield Est. | Best For |

|---|---|---|---|---|

| Leasehold Condo | S$2,200–S$3,200 | 99-year LH | 2.8–3.5% | Capital appreciation, lower entry |

| Freehold Condo | S$2,800–S$4,800 | Freehold | 2.5–3.2% | Long-term hold, scarcity premium |

| Terrace (landed) | S$1,800–S$3,200 (land psf) | Freehold | 1.5–2.5% | Generational wealth, redevelopment |

| Semi-D / Bungalow | S$2,400–S$5,000+ (land psf) | Freehold | 1.2–2.0% | Ultra-prime, lowest yield segment |

| HDB Resale (rare) | S$620–S$900 | Remaining lease | 3.0–4.0% | Owner-occupiers; EIP restrictions apply |

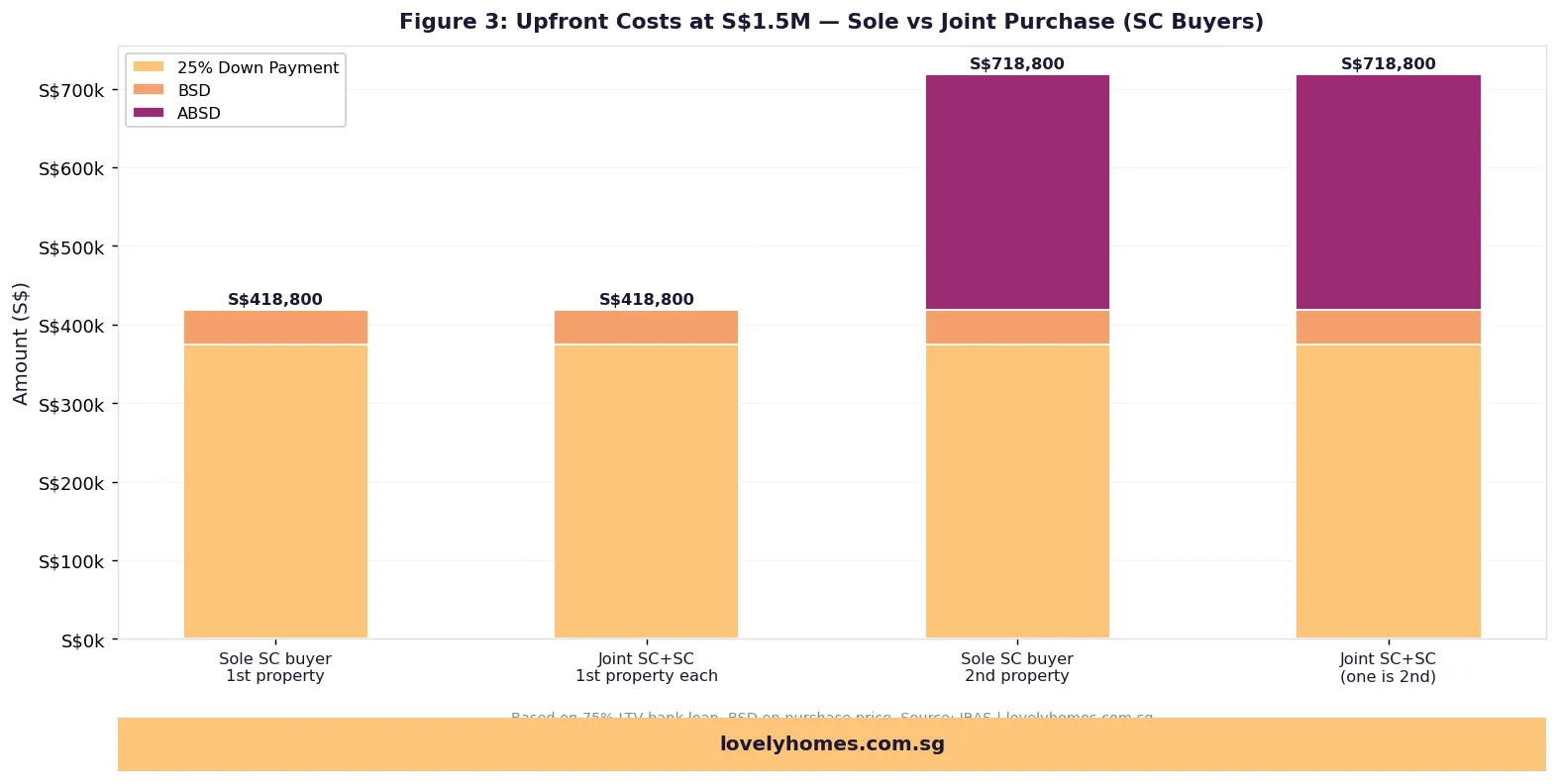

Worked Example: Buying a 2-Bedroom Freehold Condo in D09

📌 Case Study: Mr & Mrs Tan — 2-Bedroom Freehold Condo, D09

Profile: Singapore Citizen + Singapore Citizen, joint purchase of their first residential property. Combined gross monthly income S$18,000. Buying a 2-bedroom freehold condo at S$2,200,000.

Buyer’s Stamp Duty (BSD): First S$180,000 × 1% = S$1,800; next S$180,000 × 2% = S$3,600; next S$640,000 × 3% = S$19,200; next S$500,000 × 4% = S$20,000; next S$700,000 × 5% = S$35,000 ≈ S$79,600 BSD (effective rate ~3.62%)

ABSD: First property for both SC purchasers → S$0 ABSD

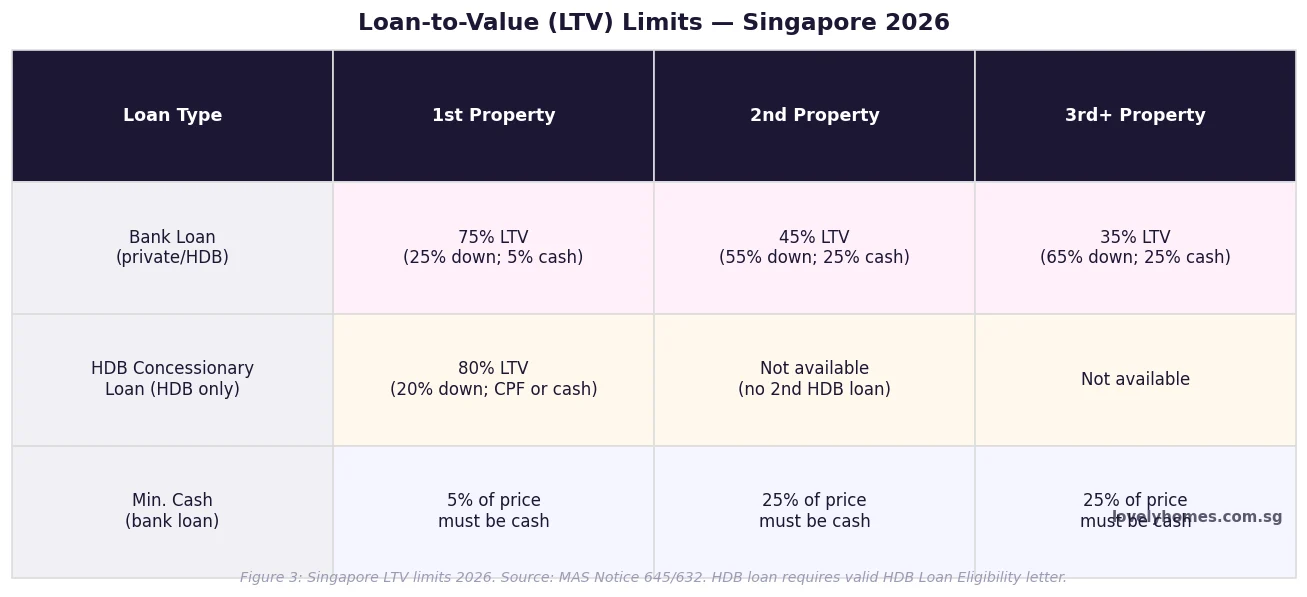

LTV and financing (bank loan): 75% LTV max → loan S$1,650,000. At 3.5% p.a., 25-year tenure: monthly repayment = S$8,272. TDSR: S$8,272 / S$18,000 = 45.9% — below the 55% TDSR cap → PASS.

Upfront cash requirement: 5% cash = S$110,000; balance 20% down (CPF or cash) = S$440,000; BSD S$79,600; legal/misc ~S$8,000. Total upfront ≈ S$637,600.

Note: If buying a second property or if either buyer is not SC, ABSD applies. A second-property SC purchase adds S$440,000 (20%) ABSD. Foreign buyers add S$1,320,000 (60%) ABSD. See our ABSD Complete Guide for full rates.

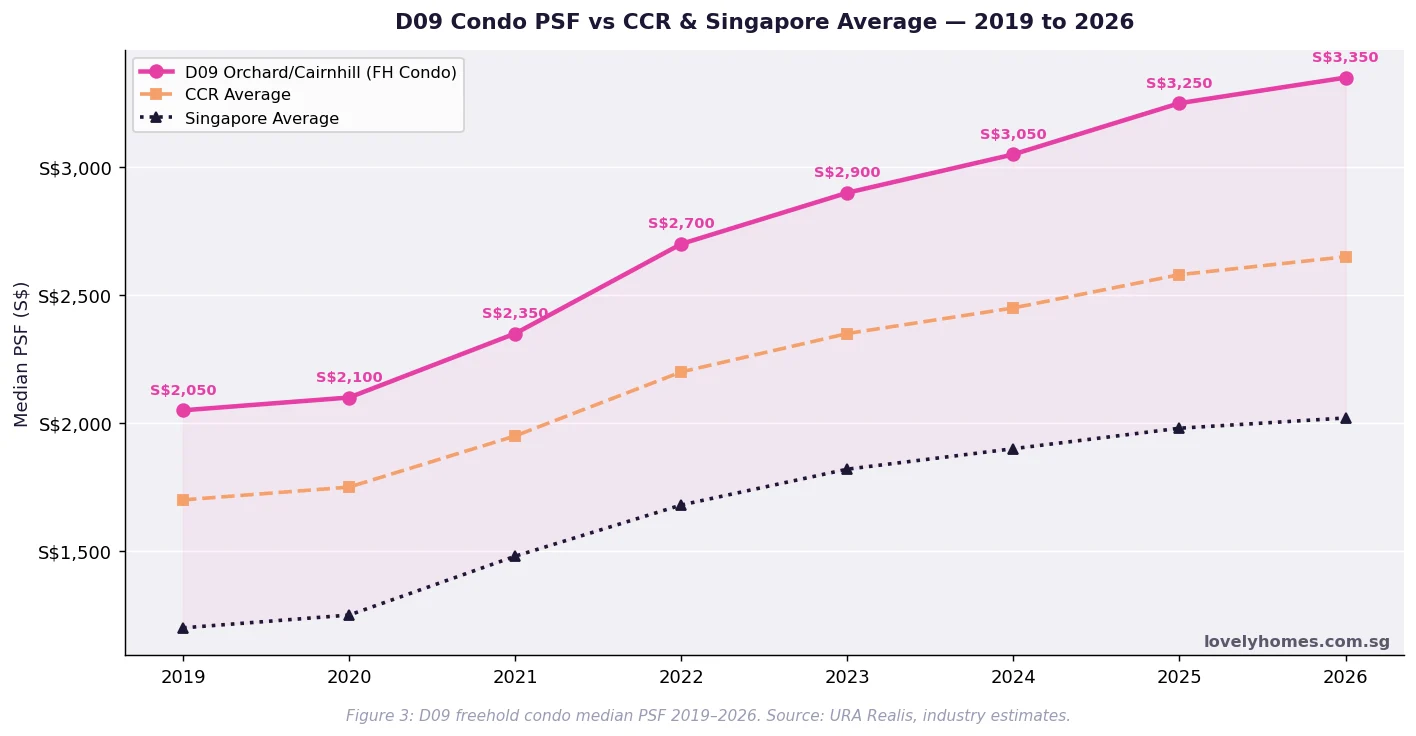

D09 Price Trend: How Orchard Road Condos Have Performed Since 2019

Freehold D09 condominiums appreciated from a median ~S$2,050 psf in 2019 to approximately S$3,350 psf by Q1 2026 — a 63% increase over seven years, or roughly 7% per annum compounded. This comfortably outpaced both the CCR average (+56%) and the Singapore-wide average (+68% from a much lower base).

The 2020 dip was shallow and brief: D09 benefited from an ultra-low interest rate environment and surging demand from ultra-high-net-worth buyers relocating to Singapore under the Global Investor Programme (GIP) and family office expansion. The 2023 ABSD increases (60% for foreigners, 65% for entities) dampened volume but exerted little downward pressure on freehold CCR pricing due to the structural scarcity of such units.

Why District 9 Matters in a Portfolio Context

For Singapore property investors, D09 serves a distinct portfolio role compared to OCR or RCR assets. Freehold tenure in D09 acts as a store-of-value comparable to a blue-chip equity position: low yield, low volatility in nominal terms, and a structural scarcity floor. The supply pipeline is thin — no major GLS site has been launched in the Orchard/Cairnhill sub-district since the 2010s — and the freehold nature of most existing stock means developers acquire sites only through collective sales, which cycle slowly and at significant cost.

Compared to peer markets such as Hong Kong’s Peak or Sydney’s Mosman, D09 freehold condo pricing at S$3,000–S$4,500 psf (approximately HK$26,000–HK$39,000 per sq ft or A$5,500–A$8,300 per sq ft) remains broadly competitive for a stable, AAA-sovereign-rated city with no capital gains tax, no inheritance tax, and full repatriation of rental income and sale proceeds.

What Might Come Next for Orchard Road Property

Two macro catalysts are worth watching. First, the URA Master Plan 2025 (gazetted December 2025) includes proposals to introduce limited residential GLS activity at the Orchard Boulevard fringe — potentially adding 600–800 new leasehold units to the precinct over the 2028–2032 horizon. If realised, this would modestly widen the leasehold–freehold PSF gap but is unlikely to cap freehold pricing. Second, TEL Stage 4 (Bayshore to Sungei Bedok) and Stage 5 completions are driving demand relocation from D09 toward D15/D16; while this eases upward pressure on D09 pricing, it also reflects a broader market deepening that historically lifts all CCR boats over the medium term.

Forward-looking commentary is speculative. Property markets are influenced by macro factors including interest rates, government cooling measures, and global capital flows that cannot be predicted with certainty.

Frequently Asked Questions

Can foreigners buy property on Orchard Road?

Yes, foreigners may purchase private condominiums in D09 (including Orchard Road and River Valley). However, the Additional Buyer’s Stamp Duty for foreign purchasers is 60% of the purchase price — a significant barrier. Foreigners are generally prohibited from purchasing landed residential property (terrace houses, semi-detached, detached bungalows) in Singapore without specific Ministerial approval. The restriction does not apply to units in strata-titled developments (condominiums). Foreigners who are Singapore Permanent Residents (SPR) pay a lower ABSD of 5% (first property), 30% (second), or 35% (third+), as at 2026.

What is the difference between Orchard Road, River Valley, and Cairnhill within D09?

District 9 covers three loosely overlapping sub-precincts. Orchard Road proper refers to the retail boulevard and its immediately flanking residential streets (Orchard Boulevard, Claymore Hill, Ardmore Park). Properties here command the sharpest freehold premiums. Cairnhill is the quieter residential enclave to the north of Orchard Road, characterised by mid-size freehold blocks on elevated terrain with city views. River Valley lies to the south and west, sloping towards the Singapore River; it is more mid-market relative to Cairnhill and has benefited most from the Great World TEL station opening, which added MRT-first access to a previously bus-dependent sub-precinct.

Are there HDB flats in Orchard Road / D09?

HDB flats in D09 are extremely rare. The handful of remaining HDB blocks near Cairnhill and the former Rochor estate are among the oldest in the stock (1970s–1980s vintage). They are resale only — no new BTO supply has been announced for D09 — and are subject to standard HDB resale eligibility rules including the Ethnic Integration Policy (EIP) quotas, which can constrain the buyer pool. The EIP quota for some blocks in the area is reached at times, particularly for Chinese-ethnicity buyers. Due to their central location, prices can reach S$700–S$900 psf, though resale volume is very low.

What ABSD do I pay on a second property purchase in D09?

ABSD rates (effective 2023) applicable to second-property purchases: Singapore Citizens 20%; Singapore PRs 30%; foreigners 60%. For a S$2,200,000 condo in D09, a Singapore Citizen buying their second property would pay S$440,000 in ABSD on top of BSD (~S$79,600), for total stamp duty of ~S$519,600. This significantly raises the break-even holding period. Most buyers paying ABSD at the 20% rate need to hold the property for approximately 8–12 years before capital appreciation covers the stamp duty cost, depending on leverage and rental income. Our ABSD complete guide has a full worked example with holding-period analysis.

Is D09 a good district for rental investment?

D09 is well-suited to investors who prioritise capital preservation and portfolio prestige over yield. Gross rental yields average 2.5–3.2%, which is among the lowest in Singapore by district. However, the tenant base — predominantly corporate expatriates, senior professionals, and high-net-worth individuals — is financially resilient and generates stable occupancy rates. Vacancy rates in D09 have historically tracked below the national condo vacancy average. The key risk is yield compression during interest rate cycles: when bank loan rates rise to 3.5–4.0%+, the carry cost of a highly leveraged D09 property can turn negative. Investors should stress-test their numbers at prevailing bank rates before committing.

What are the most established condo projects in Orchard Road?

Several freehold developments along Orchard Road and Cairnhill have maintained strong resale markets across multiple property cycles. Ardmore Park (Ardmore Park Road), Four Seasons Park (Cuscaden Road), Grange Infinite (Grange Road), The Ardmore (Ardmore Park), and Leonie Parc View (Leonie Hill) are among the well-regarded addresses. These projects typically offer large unit sizes (1,500–3,500 sq ft is common), high ceiling heights, and established common facilities. Newer freehold launches in the precinct include 15 Holland Hill (technically D10 fringe). Always verify the remaining lease, MCST management quality, and any outstanding special levies before committing to a specific project.

How does the Orchard Road masterplan affect property values?

The URA Orchard Road masterplan — actively implemented since the mid-2010s — repositions the district from a pure retail belt to a mixed-use “live, work, play” precinct. This includes the introduction of residential uses in selected retail podiums, increased greenery, pedestrianisation of side streets, and the long-term redevelopment of older hotel and commercial sites. For residential buyers, the masterplan signals continued public-sector investment in the streetscape and connectivity — a positive indicator for long-term capital values. The introduction of residential GLS sites flagged in the 2025 Master Plan, if confirmed, would add supply but also validate the URA’s confidence in the precinct’s long-term demand fundamentals.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Tanjong Pagar Neighbourhood Guide Singapore 2026: D02 Prices, GSW & Investment Outlook

- Novena Neighbourhood Guide Singapore 2026: D11 Medical Hub, Prices & Investment Outlook

- Singapore Condo Resale Guide 2026: Step-by-Step Buyer’s Complete Guide

- Buyer’s Stamp Duty Singapore 2026: Complete Guide to BSD Rates & Calculator

- Seller’s Stamp Duty Singapore 2026: Complete Guide to SSD Rates & Exemptions

- Singapore Property Cooling Measures Timeline 2009–2026

Disclaimer

All property prices, PSF figures, rental yields, and market projections in this article are based on publicly available data from URA Realis, HDB, and industry sources as at Q1–Q2 2026. They are indicative estimates and do not constitute a valuation, investment advice, or recommendation to buy or sell. Singapore property transactions involve significant stamp duties, financing obligations, and regulatory constraints. Readers should consult a licensed property professional, licensed financial adviser, and legal counsel before making any property purchase decision. Official stamp duty rates and eligibility rules are published by the Inland Revenue Authority of Singapore (IRAS) at iras.gov.sg. Zoning and planning information should be verified with the Urban Redevelopment Authority (URA) at ura.gov.sg. HDB resale eligibility rules are published at hdb.gov.sg.

Click anywhere or press Esc to close