- A valid will is the most reliable way to direct how your property passes to your chosen beneficiaries.

- Without a will, the Intestate Succession Act 1967 distributes your estate — your property may not go to whom you intend.

- CPF savings (used for your home) do not form part of your estate — they are distributed separately via CPF nomination or CPF’s default rules.

- Joint Tenancy (JT) transfers property automatically to the surviving co-owner by right of survivorship, bypassing probate.

- Beneficiaries who inherit property and already own another property will pay Additional Buyer’s Stamp Duty (ABSD) on the inherited share.

- Probate for straightforward estates typically takes 2–6 months; complex or contested estates can take 2+ years.

- Singapore has no inheritance tax or estate duty (abolished 2008).

What Is Property Succession and Why It Matters in Singapore

Property succession is the legal process by which real estate and related assets transfer from a deceased owner to heirs or beneficiaries. In Singapore, property is typically the single largest asset most families own — a 4-room HDB resale flat now trades at roughly S$498,000 median, while a typical Outside Central Region (OCR) condominium changes hands above S$1.5 million. Without a structured succession plan, a lifetime of asset accumulation can be frozen in probate, contested by family members, or distributed according to the government’s default intestacy rules rather than the owner’s wishes.

Singapore’s legal framework for property succession is administered across three principal bodies: the Ministry of Law (MLaw) oversees wills and the Probate and Administration Act 1967; the Singapore Land Authority (SLA) registers all property transfers including transmission on death; and the Central Provident Fund Board (CPF) controls the distribution of CPF monies — including the portion withdrawn to finance your home purchase — entirely separately from your estate.

Understanding how these three streams interact is essential for any property owner in Singapore, regardless of whether you own an HDB flat, a private condominium, or a landed property.

Dying With a Will: How Property Passes Under a Valid Will

A valid will is a written document signed by the testator (the person making the will) before two witnesses who are present simultaneously, and who are not beneficiaries under the will. Under the Wills Act 1838, the will must be made by a person aged 21 or older and of sound mind. Singapore does not recognise oral or holographic (handwritten, unwitnessed) wills.

When the testator dies, the named executor applies to the High Court for a Grant of Probate. Once granted — typically within 6–12 weeks for straightforward estates — the executor can instruct the SLA to transmit the property title to the named beneficiary. The full legal process, including final distribution, typically takes 4–8 months for an uncomplicated estate, and longer if property needs to be sold or if there are disputes.

ABSD on inherited property: A beneficiary who receives property via a will pays Buyer’s Stamp Duty (BSD) on transmission, and also pays ABSD at their applicable profile rate if the inherited property is their second or subsequent property. For a Singapore Citizen (SC) receiving an inherited condominium as their second property, ABSD is 20% of the property’s market value at the time of transmission. This is often an unwelcome surprise for beneficiaries who had not budgeted for a six-figure stamp-duty bill.

Dying Without a Will: Intestate Succession in Singapore

If a Singapore resident dies intestate (without a valid will), the Intestate Succession Act 1967 determines how the estate is distributed. The Act creates a statutory hierarchy: spouse and children take priority, followed by parents, then more distant relatives. For a married property owner with children, the distribution is typically half to the surviving spouse and half equally among the children. The surviving spouse does not automatically inherit the entire estate, which often surprises families who assume a jointly named spouse will receive everything.

For Muslims in Singapore, the Syariah Court issues an Inheritance Certificate under Islamic inheritance (faraid) law instead, and the proportions differ from the Intestate Succession Act. Muslim property owners should take specific advice from an accredited Islamic estate planner.

Intestate estates require a Grant of Letters of Administration rather than a Grant of Probate — functionally similar, but the court must appoint an administrator (who is typically the next-of-kin) rather than confirming an executor named in a will. This process tends to be slower and more expensive, and the outcome is fixed by law rather than the deceased’s wishes.

CPF Nomination: The Most Overlooked Part of Property Succession

CPF savings used to purchase your property — whether for the downpayment, monthly mortgage instalments, or BSD — do not form part of your estate when you die. CPF monies are distributed entirely separately, either to your nominated beneficiaries (under a CPF Nomination) or, if no nomination has been made, to the Public Trustee for distribution under the Intestate Succession Act.

When your property is sold or when you die, all CPF monies withdrawn for the property — principal plus accrued interest at 2.5% per annum — must be refunded to your CPF Ordinary Account (OA). Your surviving family cannot access these funds simply by inheriting the property; the CPF refund clears before any equity passes to beneficiaries. This is why many families discover, on an intestate death, that the net cash proceeds from a property sale are significantly smaller than expected.

A CPF nomination directs your CPF savings directly to named individuals upon death, bypassing probate entirely and typically settling within weeks rather than months. You can make a CPF nomination online via the my.cpf.gov.sg portal or in person at any CPF Service Centre, with two witnesses.

Joint Tenancy: Automatic Succession Without Probate

Joint Tenancy (JT) is the default ownership structure for married couples purchasing HDB flats in Singapore, and is also common for private property. Under JT, each co-owner holds an undivided equal share, and when one co-owner dies, their share passes automatically to the surviving co-owner by right of survivorship — without the need for probate, a Grant of Letters of Administration, or any SLA transmission application. The surviving owner simply lodges a Transmission Application with SLA, supported by the death certificate and a Statutory Declaration.

This automatic nature of JT makes it powerful for succession planning, but it also creates rigidity: neither co-owner can bequeath their JT share under a will, and the survivor is entitled to the full property regardless of any separate testamentary wishes. JT can be severed by either co-owner (converting it to Tenancy in Common) by lodging a Notice of Severance with SLA, but this must be done before death — it cannot be done posthumously.

Tenancy in Common (TiC), by contrast, allows each co-owner to hold a specified percentage share (not necessarily equal) that can be bequeathed under a will. TiC is common in investment properties, property held with business partners, or where co-owners wish to preserve independent testamentary control over their respective shares.

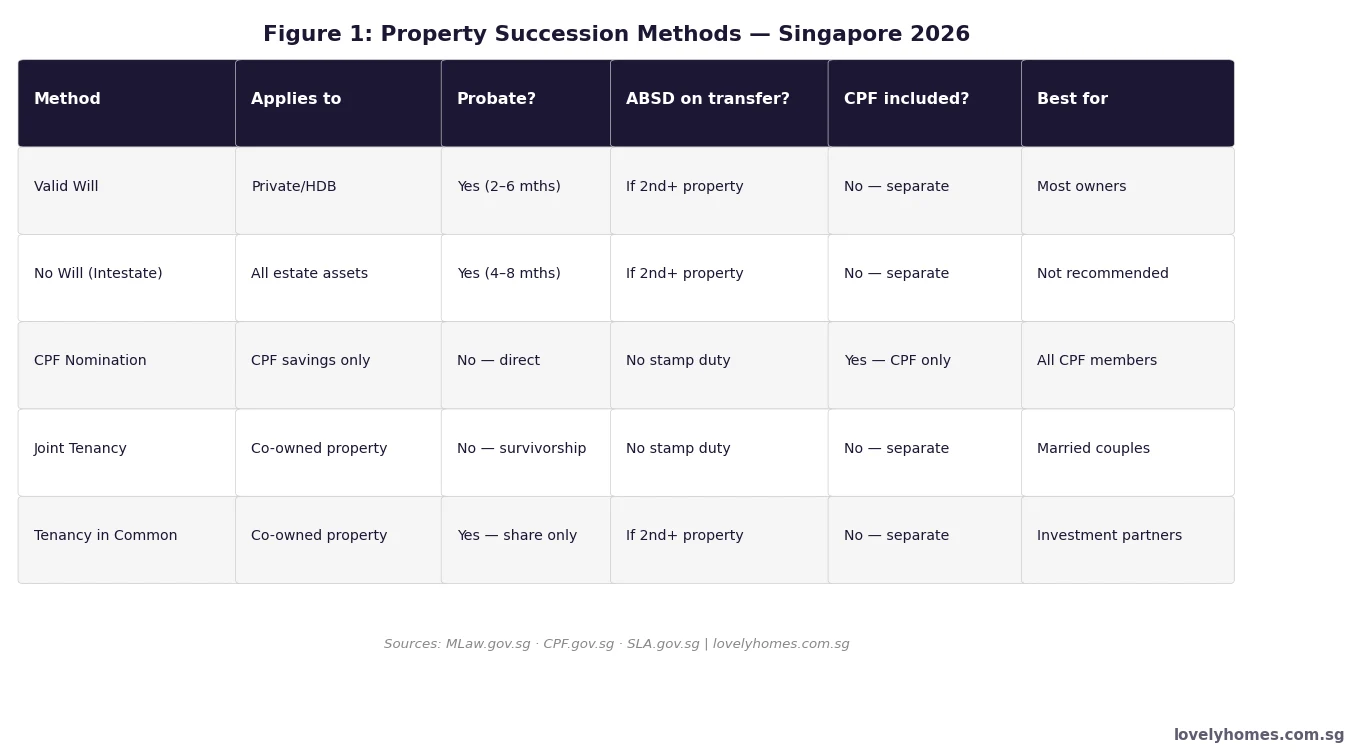

Summary Table: Property Succession Rules at a Glance

| Succession Route | Probate Required? | ABSD on Transfer? | CPF Included? | Timeline |

|---|---|---|---|---|

| Valid Will | Yes — Grant of Probate | If 2nd+ property | No — CPF separate | 4–8 months typical |

| Intestate (no will) | Yes — Letters of Admin | If 2nd+ property | No — CPF separate | 6–12 months typical |

| CPF Nomination | No | No | Yes — CPF only | Weeks |

| Joint Tenancy death | No — SLA Transmission | No | No — CPF separate | 4–8 weeks |

| Trust structure | No — if in trust | Depends on trust type | No | As per trust deed |

Worked Example: The Tan Family — HDB Flat and Investment Condo

Scenario: Mr Tan Ah Kow (SC, age 62) owns a 5-room HDB flat in Ang Mo Kio under Joint Tenancy with his wife, Mrs Tan (SC). He also owns a 2-bedroom resale condominium in District 15 under Tenancy in Common (60% share, market value S$1.6 million, his 60% share worth S$960,000) as an investment property. His CPF Ordinary Account balance is S$285,000. He has no current will and no CPF nomination.

On Mr Tan’s death:

- HDB flat: Passes automatically to Mrs Tan by right of survivorship (JT). No probate. SLA transmission application settled in approximately 4–6 weeks. No ABSD (Mrs Tan was already a JT owner; this is transmission, not a purchase).

- Investment condo (60% TiC share): Because there is no will, the estate goes intestate. A Grant of Letters of Administration must be obtained from the High Court — taking approximately 6–10 months. Distribution under the Intestate Succession Act: 50% to Mrs Tan (S$480,000 value), balance 50% equally among Mr Tan’s children. Mrs Tan now receives S$480,000 worth of a TiC share in the condo — as her second property (she already owns the HDB), she pays ABSD of 20% = S$96,000. Each child inherits a share proportional to their portion of the 50% balance; if any child already owns property, they also pay ABSD on their inherited share.

- CPF savings (S$285,000): With no CPF nomination, the Public Trustee distributes this under intestacy rules — 50% to Mrs Tan, 50% split among children. Distribution takes 3–6 months. The CPF accrued interest on the flat is also refunded to CPF and distributed the same way.

What Mr Tan should have done: (1) Make a will directing his TiC condo share to the beneficiary least likely to already own property, or to a trustee for eventual distribution. (2) Make a CPF nomination directing his CPF savings directly to Mrs Tan or his children. (3) Review the ABSD implications on each beneficiary before gifting a property share by will — consider whether a trust structure would avoid ABSD on the bequest.

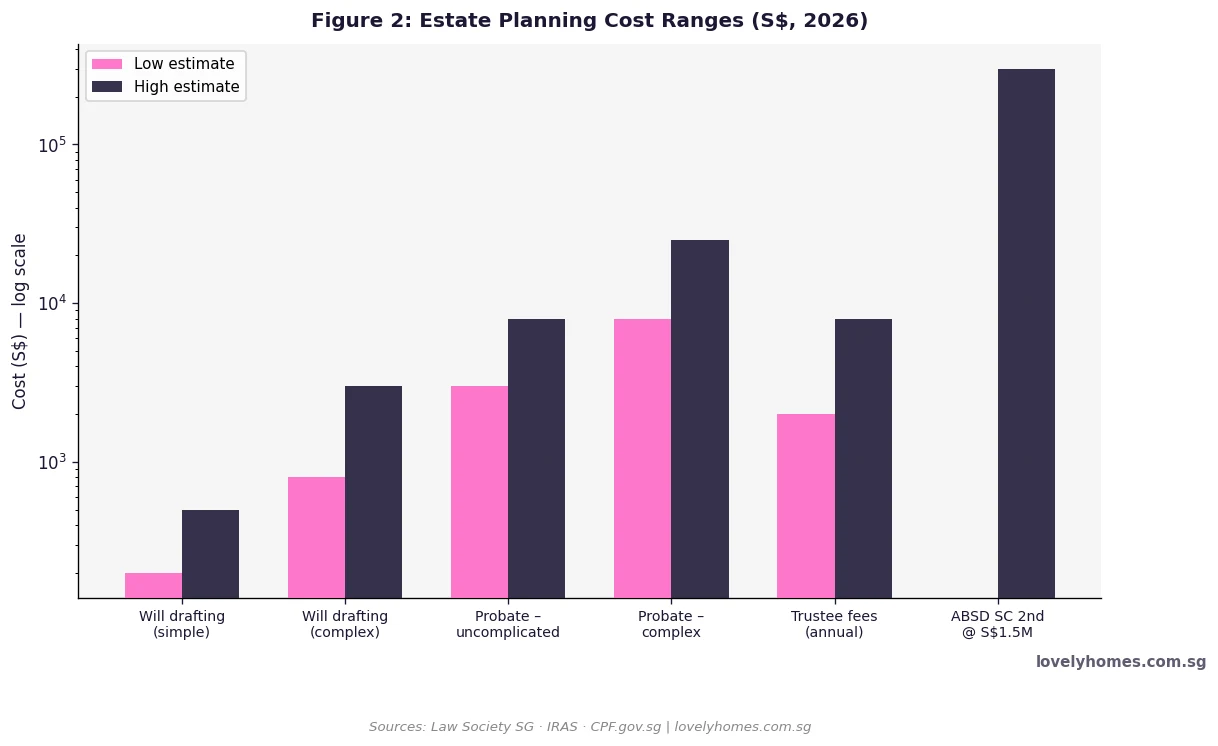

Estimated preventable cost with proper planning: A lawyer-drafted will costs S$500–S$3,000. A CPF nomination is free. The ABSD Mrs Tan unknowingly pays on the intestate distribution: S$96,000. The net saving from proper planning for this family: approximately S$93,000–S$95,500.

Singapore Has No Inheritance Tax — but ABSD Can Sting

Singapore abolished estate duty in 2008. There is no inheritance tax, no capital gains tax on property, and no wealth tax on property assets received by inheritance. This is one of Singapore’s most competitive features as an estate-planning jurisdiction.

However, ABSD can function as a de facto inheritance tax for beneficiaries who already own property. A child who owns a private condominium and inherits a parent’s second property as an SC pays 20% ABSD on the inherited market value — the same rate they would pay if purchasing the property themselves. This asymmetry encourages property owners to plan their succession carefully, directing high-value property to first-time-property beneficiaries where possible.

There is currently no ABSD remission scheme for inherited property (unlike the SC-couple remission for purchasing a second property), though practitioners often petition IRAS on a case-by-case basis for discretionary relief. IRAS grants such relief rarely and on strict conditions.

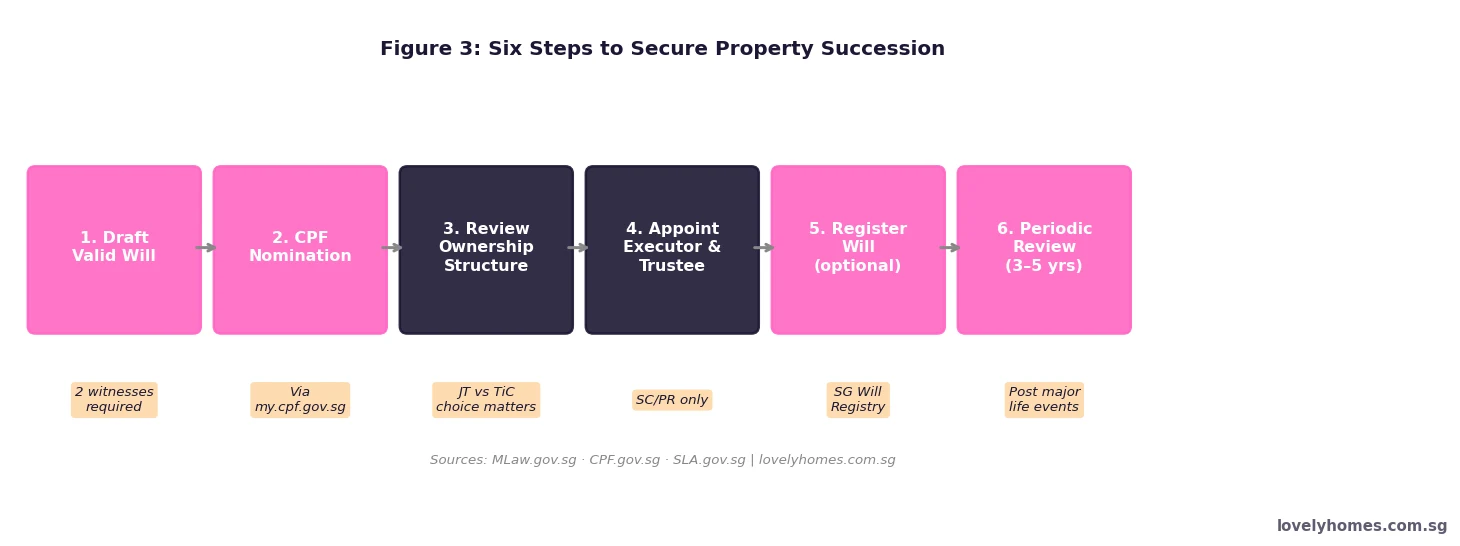

What Property Owners Should Do Now: A Practical Checklist

Based on the legal and stamp-duty framework above, here is a practical six-step succession checklist for Singapore property owners.

Step 1 — Draft a valid will: Engage a solicitor (not a template will-kit if your estate is complex). The will should specifically name each property, specify the percentage share bequeathed, and appoint both an executor and a trustee. A single will can address all your Singapore-based property, bank accounts, and other assets. Basic will-drafting costs S$200–S$500 (simple) to S$800–S$3,000 (complex, with trust clauses).

Step 2 — Make a CPF nomination: Do this online at my.cpf.gov.sg. It is free and takes under 15 minutes. Your CPF nomination should be consistent with your will to avoid inadvertent inequity between CPF and non-CPF beneficiaries.

Step 3 — Review your ownership structure: Decide whether your co-owned property should be held as JT or TiC. JT is typically right for primary homes owned by married couples; TiC is typically right for investment properties where each owner wants independent testamentary control. Changing from JT to TiC requires a Notice of Severance filed with SLA.

Step 4 — Appoint an executor and trustee: Your executor must be a Singapore Citizen or Permanent Resident aged 21 or above. A bank or a licensed corporate trustee can act as an executor if no suitable family member or friend is available. Consider whether a trust is advisable for minor children who cannot legally hold property until age 21.

Step 5 — Register your will (optional): Singapore operates the Will Registry through the Singapore Academy of Law. Registration does not make a will valid (validity depends on execution, not registration), but it does make the will easier to locate after death. Annual registration fee is S$60.

Step 6 — Review every 3–5 years, and after major life events: Marriage, divorce, the birth of a child, the death of a named beneficiary, a significant change in your property portfolio, or any change in ABSD rates should all trigger a will review. A will made before marriage is automatically revoked by the marriage in Singapore.

What Might Come Next: Future Policy Considerations

Singapore’s government has periodically reviewed whether to reintroduce some form of estate duty, particularly in the context of wealth inequality debates. The 2021 Budget commentary and subsequent parliamentary discussions have not signalled any near-term intention to do so, but property owners with high-value estates should monitor Budget statements each February. Any reinstatement of estate duty would likely be announced at least one year in advance to allow planning adjustments.

On the ABSD front, the existing 20% rate on a second-property SC beneficiary receiving an inherited property is an unintended consequence of ABSD’s original design as a market-cooling measure rather than a succession instrument. Industry groups and legal practitioners have lobbied for a dedicated ABSD exemption or remission route for inherited properties. MLaw and IRAS have not formalised any such scheme as at July 2026, but the matter continues to be raised in parliamentary questions.

Frequently Asked Questions

Does my HDB flat automatically go to my spouse when I die?

It depends on the ownership structure. If you hold the flat under Joint Tenancy (JT) with your spouse, it passes automatically by right of survivorship — your spouse becomes the sole owner without probate. If you hold it under Tenancy in Common (TiC), or if you are the sole owner, the flat forms part of your estate and passes under your will (or the Intestate Succession Act if you have no will), requiring a Grant of Probate or Letters of Administration. Most HDB flats bought by married couples are registered as JT by default, but you should confirm your ownership type on SLA’s myProperty portal.

Will my children have to pay ABSD when they inherit my condominium?

Yes, if the inherited property is not their first property. A Singapore Citizen child who already owns an HDB flat or condominium, and who inherits a condo share under a will or intestacy, pays ABSD at 20% on the market value of the inherited share. There is no ABSD exemption or remission for inherited property as at 2026. The ABSD is assessed at the date of transmission, using the market value determined by a valuation commissioned by the SLA. To minimise your children’s ABSD exposure, structure your will to direct property to the child (or other beneficiary) who owns the fewest properties.

What happens to my CPF savings if I die without a CPF nomination?

Your CPF savings — including any amounts withdrawn for your home — do not form part of your estate. Without a CPF nomination, the CPF Board transfers all your CPF monies to the Public Trustee (an officer of the Ministry of Law), who distributes them according to the Intestate Succession Act 1967. The distribution follows the same rules as your estate, but it is administered separately and takes approximately 3–6 months. The key risk is that without a specific CPF nomination, you have no ability to direct CPF savings to a particular individual or in a particular proportion beyond the intestacy formula.

Can I leave my HDB flat to anyone in my will?

Not freely. HDB has eligibility rules governing who can own an HDB flat, and these rules apply even to inheritance. Your will can only direct your HDB flat to someone who meets HDB’s eligibility criteria: Singapore Citizens or Permanent Residents who do not already own a private residential property, and who qualify under HDB’s family nucleus or other eligibility schemes. If your named beneficiary does not qualify to own an HDB flat, HDB typically requires the flat to be sold within a specified period. You should consult a solicitor to ensure your will accounts for HDB’s eligibility requirements.

Is a homemade or online will-kit valid in Singapore?

A will is valid in Singapore if it is in writing, signed by the testator, and witnessed by two witnesses who are present simultaneously and who are not beneficiaries. A will made using an online template or will-kit that satisfies these formal requirements is technically valid. However, legal practitioners strongly caution against will-kits for property owners with complex estates — ambiguous wording, failure to account for ABSD on beneficiaries, incorrect description of property titles, or inadequate trustee provisions can create disputes, delays, and additional costs that far exceed the savings on legal fees.

Does marriage or divorce affect my existing will?

Yes, both events affect your will significantly. Under Singapore law, a will is automatically revoked upon marriage. If you marry after making a will, the will is void and your estate will be distributed under the Intestate Succession Act until you make a new will. Divorce does not revoke a will automatically, but any appointment of your former spouse as executor, trustee, or beneficiary is automatically revoked and treated as if the former spouse had died before the testator. You should review and update your will immediately after marriage, divorce, or any other major change in your family circumstances.

How long does probate take in Singapore for a property estate?

For a straightforward estate — a single property, an uncontested will, and a cooperative beneficiary — a Grant of Probate can typically be obtained in 6–12 weeks from filing the petition. The full process including SLA title transmission and distribution can be completed in 4–8 months. Complex estates — multiple properties, overseas assets, disputed wills, or minor beneficiaries requiring court approval — can take 12–24 months or longer. Engaging a solicitor experienced in estate administration significantly reduces delays.

Related Articles

- Singapore Property Inheritance Law Guide 2026: Intestate Succession, CPF Nomination and Estate Planning

- Singapore Joint Property Ownership Guide 2026: Joint Tenancy vs Tenancy in Common

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore CPF Accrued Interest for Property 2026: What You Owe Your CPF When You Sell

- Singapore Private Property Buying Costs 2026: Complete All-In Cost Guide

- Singapore Property Decoupling Guide 2026: How to Save ABSD by Transferring Ownership

- Singapore Property Cooling Measures Guide 2026: ABSD, TDSR, LTV and SSD Explained

Disclaimer

This article is for general informational purposes only and does not constitute legal, tax, or financial advice. Estate and succession planning is a complex area of law and depends on your specific circumstances. Singapore property laws, CPF rules, and ABSD rates are subject to change by the relevant authorities — HDB, SLA, CPF Board, IRAS, and the Ministry of Law. Readers are strongly encouraged to consult a licensed Singapore solicitor for personalised estate-planning advice, and to verify current rules with the Ministry of Law (mlaw.gov.sg), CPF Board (cpf.gov.sg), IRAS (iras.gov.sg), and SLA (sla.gov.sg).

0 Comments