Click anywhere or press Esc to close

The HDB Resale Levy is one of Singapore’s least understood property costs — and one of the most consequential for households planning to upgrade from a first subsidised flat to a second. Administered by the Housing and Development Board (HDB), the resale levy exists to ensure that the substantial housing subsidy granted to first-time buyers is partially recovered when those buyers choose to purchase a second subsidised flat from HDB. Understanding exactly who pays it, how much it is, and when it is collected can save upgrading households tens of thousands of dollars in planning errors.

✅ Quick Answer — HDB Resale Levy at a Glance

- What it is: A levy payable to HDB by second-timer applicants who received a housing subsidy on their first flat and are now buying a new subsidised flat.

- Who pays: Second-timers buying a new Build-To-Order (BTO), Sale of Balance Flat (SBF), or new Executive Condominium (EC before privatisation).

- Who does NOT pay: First-timers; buyers of resale HDB flats (the levy applies only to new-flat purchases); buyers who have not previously received a housing subsidy.

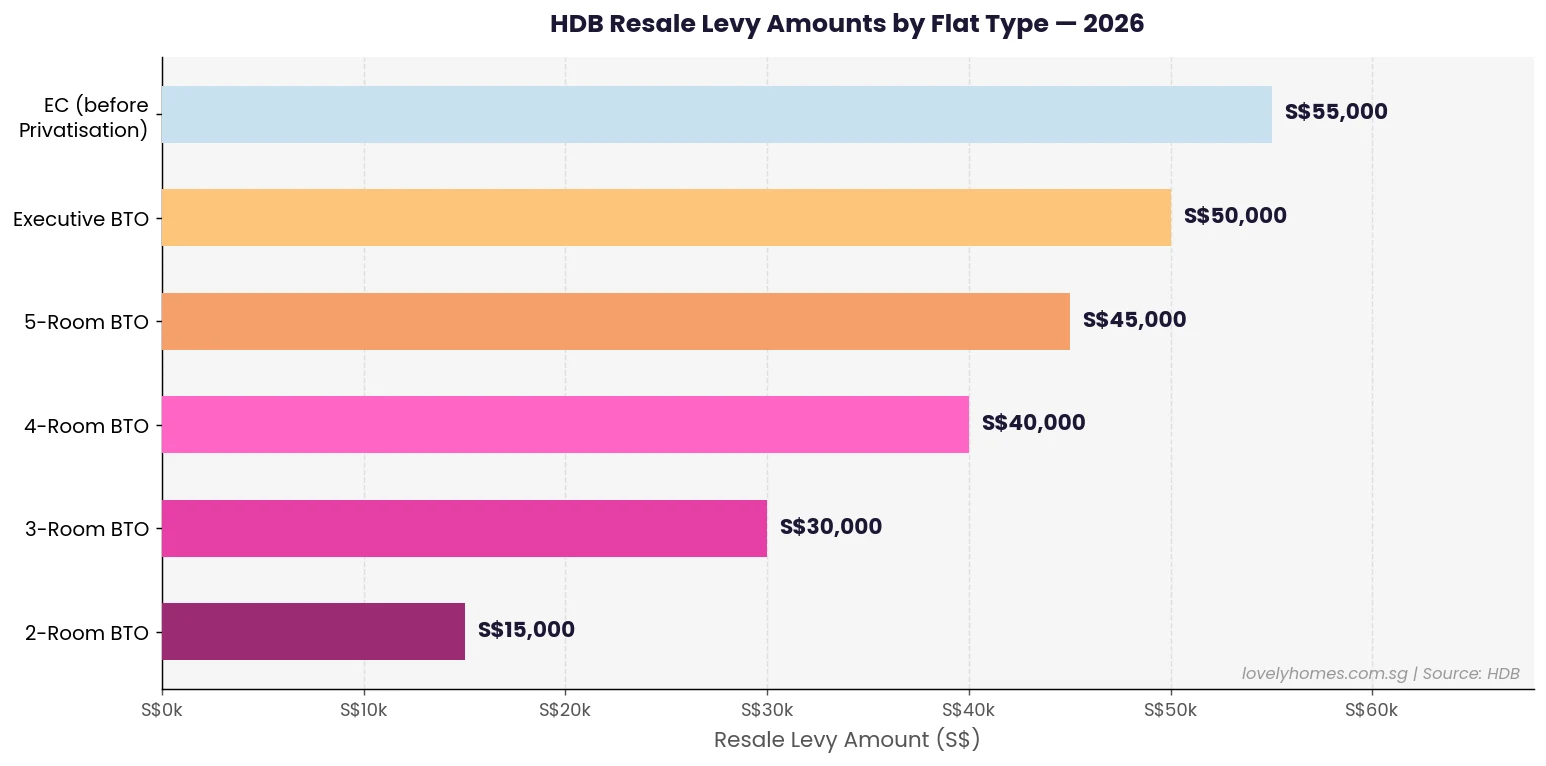

- Amounts (2026): S$15,000 (2-room) | S$30,000 (3-room) | S$40,000 (4-room) | S$45,000 (5-room) | S$50,000 (Executive) | S$55,000 (EC).

- When paid: Deducted from the sale proceeds of the first flat, or paid in cash if proceeds are insufficient.

- Official source: HDB’s Resale Levy Policy (www.hdb.gov.sg).

What Is the HDB Resale Levy and Why Does It Exist?

Singapore’s public housing system is built on the principle of one major housing subsidy per household in a lifetime. When a household buys its first BTO flat, it benefits from a significant subsidy — typically 20–40% below the market value of equivalent resale flats — funded by the Government through HDB’s development programme. This subsidy is the bedrock of Singapore’s high home-ownership rate (approximately 89% as at 2026).

When a subsidised household later sells its flat and applies to buy a second new subsidised flat (another BTO or a new EC), it would effectively be receiving a second government subsidy. The resale levy is designed to partially recoup the first subsidy, ensuring fair allocation of public resources across generations of Singaporeans. It applies regardless of the sale price achieved for the first flat — the levy is fixed by flat type, not by capital gain.

The levy was first introduced in 1995 and has been revised several times. The current levy schedule (below) has been in place since 2006 with minor adjustments, and no changes were announced in 2025 or early 2026.

Resale Levy Amounts — 2026 Schedule

| Type of First Subsidised Flat | Resale Levy (S$) | Payable To |

|---|---|---|

| 2-Room Flexi BTO | 15,000 | HDB |

| 3-Room BTO / DBSS / SBF | 30,000 | HDB |

| 4-Room BTO / DBSS / SBF | 40,000 | HDB |

| 5-Room BTO / DBSS / SBF | 45,000 | HDB |

| Executive Flat / Maisonette BTO | 50,000 | HDB |

| Executive Condominium (new, pre-privatisation) | 55,000 | HDB |

The levy is determined by the type of the first subsidised flat, not the second. If a household sold a 4-room BTO and is now buying a 5-room BTO, it pays the 4-room levy of S$40,000 — not the 5-room levy of S$45,000. This distinction often surprises upgraders who assume the levy scales with their new purchase.

Who Pays — and Who Is Exempt

The two conditions that must simultaneously be met for the levy to apply are: (1) you or your co-applicant previously received a housing subsidy on a flat you own or have owned, and (2) you are now applying for a new subsidised flat (BTO, SBF, or new EC). If either condition is absent, no levy applies.

Common situations where the levy does NOT apply: buying a resale HDB flat on the open market (regardless of whether you owned a BTO before); buying a private condominium or landed property; buying an HDB flat from HDB as a first-timer with no prior subsidy; and any purchase after the levy has already been paid once (HDB does not charge it twice for the same household).

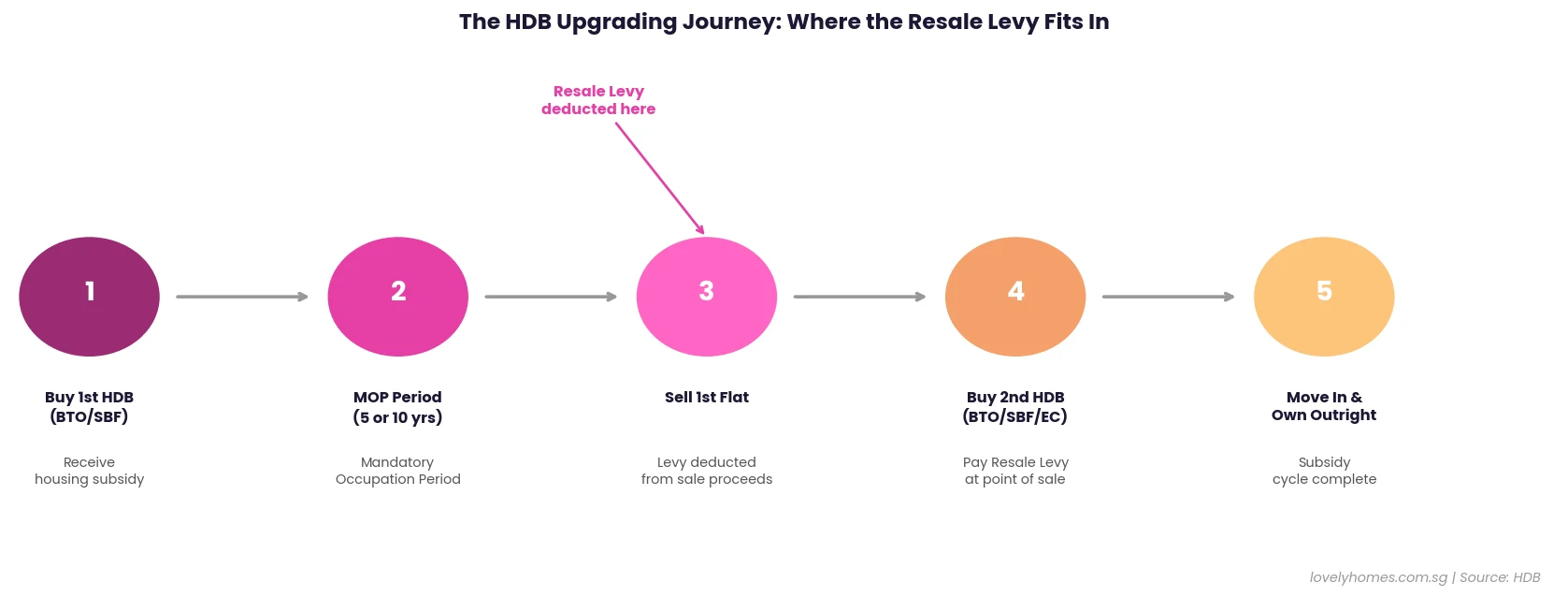

When Is the Resale Levy Collected?

The levy is collected at the point of completion of the sale of the first flat, not at the point of booking the new flat. In practice, HDB deducts the levy directly from the sale proceeds — meaning it never passes through the seller’s hands. If the net sale proceeds (after repaying the outstanding HDB loan and refunding CPF with accrued interest) are insufficient to cover the levy, the shortfall must be paid in cash.

This sequencing has an important implication for households planning their upgrade: you must complete the sale of your first flat before or concurrently with the booking of the new flat. HDB will not proceed with the new flat application until it can confirm the levy payment from the sale proceeds. In practice, HDB typically requires a signed Option to Purchase (OTP) on the sale of the first flat before confirming the new flat booking.

Can the Resale Levy Be Paid in CPF?

No. The HDB Resale Levy must be paid in cash or deducted from the net cash proceeds of the first flat’s sale. It cannot be paid using CPF Ordinary Account (OA) savings. This is a common misconception and a frequent source of financial surprise for upgraders who assumed their CPF could cover all transaction costs.

The practical consequence: if you are selling a 4-room BTO and your net cash proceeds after HDB loan repayment and CPF refund (with accrued interest) are less than S$40,000, you will need to top up the shortfall in cash from your personal savings. This situation is more common than buyers realise, particularly for flats sold in the early years after MOP, when capital appreciation has been modest and CPF accrued interest has significantly eroded the net cash component.

Resale Levy vs ABSD: Key Differences

| Feature | Resale Levy | ABSD |

|---|---|---|

| Administered by | HDB | Inland Revenue Authority of Singapore (IRAS) |

| Applies to | New subsidised HDB/EC purchases by second-timers | All residential property purchases (rates vary by profile) |

| SC first property | No levy (unless second-time buyer) | 0% ABSD |

| SC second property | No levy (resale market); levy if new HDB | 20% ABSD |

| Payable via CPF? | No — cash only | No — cash only |

| Fixed or variable? | Fixed by flat type, not price | Percentage of purchase price |

| Can be remitted? | No | Yes, under specific conditions (e.g., SC couples who sell first property within timeline) |

The ABSD remission scheme (where a SC married couple buying their second property simultaneously can sell their first within 6 months after completion and apply for ABSD remission) does not affect the resale levy — the two are entirely separate instruments with separate rules and separate authorities.

What This Means for Upgraders: Planning the Upgrade Correctly

The practical implications of the resale levy are most acute for households with a low outstanding HDB loan balance and moderate CPF accrued interest — a situation common among households who purchased their first BTO 8–12 years ago at subsidised prices and have mostly paid down their loan. Such households may find that their net cash proceeds after selling are barely above or even below the levy amount, making the cash flow management of the upgrade critical.

The recommended approach is to work backwards from the levy amount before booking a second flat. Calculate your estimated net cash proceeds: (1) estimated sale price of current flat, minus (2) outstanding HDB or bank loan balance, minus (3) CPF refund with accrued interest (mandatory), equals (4) net cash. If (4) is less than the applicable levy, plan for the shortfall before the upgrade timeline begins.

Does the Resale Levy Apply to Divorcees or Single Applicants?

Yes, with nuance. A divorced Singapore Citizen who previously owned a subsidised flat with an ex-spouse may be subject to the resale levy if they are applying for a new BTO as a second-timer. However, HDB applies a concession for divorcees applying under certain schemes (such as the Joint Singles Scheme or the Single Person Scheme under specific conditions) — eligibility for this concession depends on income, flat type applied for, and the specific circumstances of the divorce. Divorcees are strongly advised to consult HDB directly before making any booking.

📊 Worked Example: Family Selling 4-Room BTO and Buying a New EC

Profile: Lim family — SC/SC couple, age 38 and 36; bought a 4-room BTO in Punggol in 2015 for S$320,000 (HDB loan S$256,000, fully repaid by 2023); MOP completed 2020; now selling at S$620,000 and booking a new EC.

Step 1 — Gross sale proceeds: S$620,000

Step 2 — CPF refund with accrued interest:

Total CPF OA used (down payment + monthly instalments over 8 years): ~S$220,000

Accrued interest at 2.5% p.a. for average holding period (~6 years): ~S$34,000

Total CPF refund required: S$220,000 + S$34,000 = S$254,000

Step 3 — Outstanding loan balance: S$0 (fully repaid in 2023)

Step 4 — Net cash proceeds: S$620,000 – S$254,000 – S$0 = S$366,000 cash

Step 5 — Resale Levy (4-room BTO seller buying new EC): S$40,000 (levy is based on first flat type = 4-room, regardless of what they are buying)

Step 6 — Net after levy: S$366,000 – S$40,000 = S$326,000 net cash available for EC downpayment

New EC purchase: S$1,350,000; minimum 5% cash downpayment = S$67,500; next 15% via CPF OA = S$202,500; balance via bank loan S$1,080,000 @ 3.2% p.a. 25yr ≈ S$5,230/mth. TDSR = S$5,230 / combined income S$16,000 = 32.7% — PASS (TDSR cap 55%).

Key insight: The S$40,000 levy significantly reduces the Lim family’s available cash — from S$366k to S$326k — but is comfortably manageable given their sale price and income. Families with smaller sale proceeds or higher CPF accrual would face tighter cash positions.

Frequently Asked Questions — HDB Resale Levy

Do I pay the resale levy if I am buying a resale HDB flat (not BTO)?

No. The resale levy applies only when you are purchasing a new subsidised flat directly from HDB — that is, a BTO, Sale of Balance Flat (SBF), or a new Executive Condominium (EC, before it achieves privatisation at the 5-year mark). If you are buying a resale HDB flat on the open market from a private seller, no resale levy is charged, regardless of whether you previously owned a BTO or received a housing grant. This is a critical distinction — many upgraders choose the resale market specifically to avoid the levy, sacrificing subsidised pricing in exchange for levy-free transacting.

Can I avoid the resale levy by adding a new flat co-applicant who is a first-timer?

No. If any co-applicant on the new flat application is a second-timer (previously received a housing subsidy), the resale levy applies to the entire application. You cannot dilute the levy obligation by adding a first-timer co-applicant. HDB treats the household as a whole — if any member has received a prior subsidy, the levy is charged.

What if I am selling my first flat at a loss — do I still pay the levy?

Yes. The resale levy is a fixed amount determined by your first flat’s type, not by whether you made a profit or loss on its sale. Even if you sell your 4-room BTO below your purchase price (or break even after CPF and loan repayment), the S$40,000 levy still applies. In such cases — where net cash proceeds are insufficient — you must pay the levy shortfall in cash. This is one of the primary reasons that HDB advises households to plan their upgrade timeline carefully, ideally waiting until the flat’s market value has appreciated sufficiently to generate meaningful net cash proceeds.

Does the resale levy apply if I sold my first flat more than 10 years ago?

Yes, there is no time limitation on the resale levy obligation. Once you have received a housing subsidy on a flat, your status as a second-timer is permanent for HDB eligibility purposes. Even if you sold your first BTO 15 or 20 years ago, applying for a new BTO today would trigger the applicable levy. This surprises some buyers who assumed the passage of time or a change in marital status would reset their subsidy status — it does not, unless specific HDB concession conditions apply.

Do Singapore Permanent Residents (SPRs) pay the resale levy?

SPRs are generally not eligible to purchase new BTO flats, so the resale levy rarely applies to them directly. However, if an SPR purchased a resale flat as a first-timer (which SPRs are permitted to do) and later achieves Singapore Citizenship, they may apply for a BTO as a couple where one is SC and one was a former SPR — in which case HDB would assess whether any prior housing subsidy was received and apply the levy accordingly. The specific eligibility rules for mixed-status (SC/SPR become SC/SC) applicants are complex; consult HDB directly.

Can the resale levy be waived or reduced in hardship situations?

HDB does not have a published framework for waiving or reducing the resale levy on hardship grounds. The levy is a fixed statutory amount with no discretionary exemption for financial difficulty. Households who are unable to pay the levy from sale proceeds must arrange cash payment before HDB will proceed with the new flat transaction. If cash reserves are insufficient, households may need to consider alternative options such as purchasing a resale flat (no levy applies), deferring the upgrade, or liquidating other assets to meet the levy obligation. This is a situation where independent financial advice is strongly recommended before committing to a booking.

What happens to the resale levy if my new BTO booking is cancelled?

If you cancel your new BTO or SBF booking before completion, HDB will typically refund the resale levy — but the exact refund treatment depends on the stage of cancellation and whether the first flat has already been sold. If the first flat has been sold and proceeds used to pay the levy, the refund would be processed back to you in cash. If the cancellation is post-completion of the new flat, no refund applies. HDB’s cancellation and refund terms for BTO bookings are detailed on the HDB website and in your sales letter — review these carefully before booking.

0 Comments