📌 Quick Answer: CPF Housing Grants in Singapore (2026)

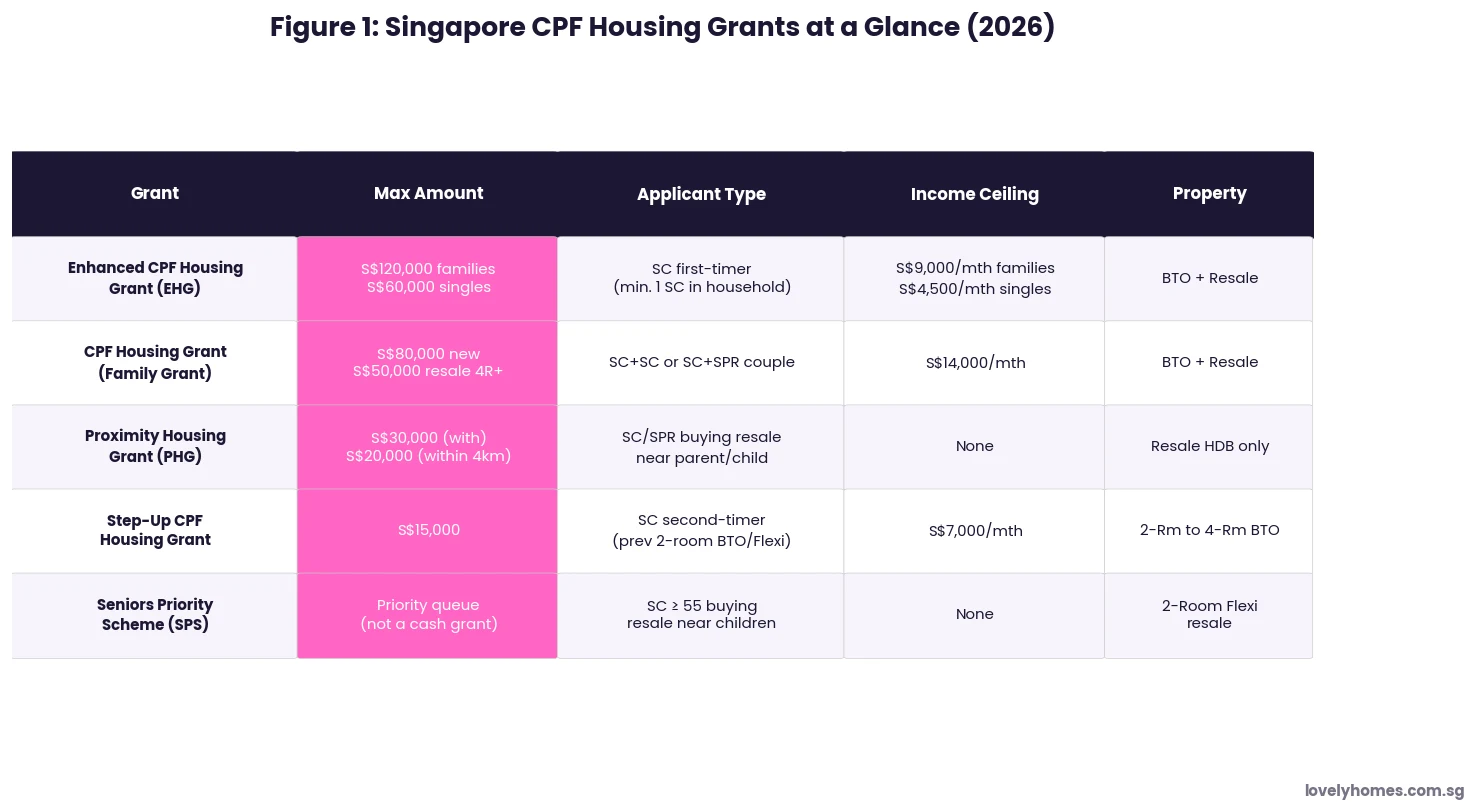

- Enhanced CPF Housing Grant (EHG): Up to S$120,000 for families earning ≤ S$9,000/month, or S$60,000 for singles earning ≤ S$4,500/month — available for both BTO and resale HDB flats.

- CPF Housing Grant (Family Grant): Up to S$80,000 for new BTO or S$50,000 for resale flats; income ceiling S$14,000/month for SC+SC or SC+SPR couples.

- Proximity Housing Grant (PHG): S$30,000 to live together with parents/children, or S$20,000 to live within 4 km — no income ceiling, resale flats only.

- Step-Up CPF Housing Grant: S$15,000 for second-timer families upgrading from a 2-room subsidised flat to a 2–4 room BTO; income ceiling S$7,000/month.

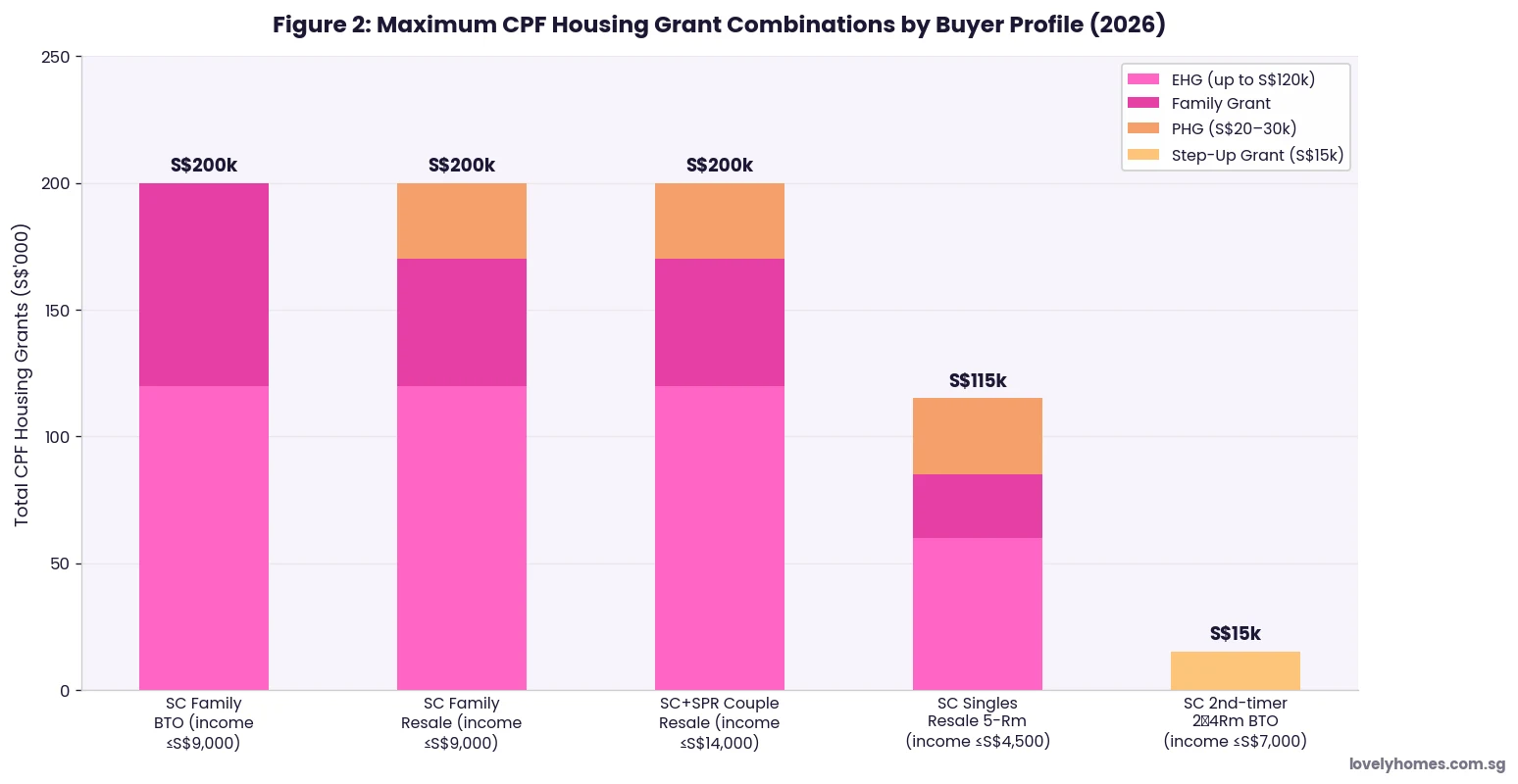

- Maximum stacking: A Singapore Citizen family buying a resale flat can receive up to S$230,000 by combining the EHG + Family Grant + PHG.

- How to apply: All CPF housing grants are applied for through the HDB Flat Eligibility (HFE) letter — there is no separate application form; the grants are assessed automatically.

- CPF OA for private property: Grants do not apply to private property purchases; however, your CPF Ordinary Account balance can be used for the down payment, monthly instalments, and stamp duties on private property — subject to the Valuation Limit and Withdrawal Limit.

What Are CPF Housing Grants?

CPF housing grants are cash subsidies administered by the Housing and Development Board (HDB) and funded from the government’s housing budget. They reduce the cash or CPF Ordinary Account (OA) outlay required to purchase a subsidised HDB flat, effectively lowering the loan quantum needed and the monthly instalment burden for eligible Singapore Citizens and Permanent Residents.

Unlike bursaries or income supplement schemes, CPF housing grants are credited directly into the buyer’s CPF Ordinary Account once the flat purchase is completed, and are applied first to reduce the purchase price at the point of resale or disbursed at key collection for BTO flats. They do not count as accrued interest and do not need to be repaid upon sale, but the grant amount — along with accrued interest at 2.5% per annum on any CPF used — must be refunded to CPF upon the sale or transfer of the flat.

The grant landscape was significantly reformed on 20 August 2024, when the EHG for families was raised from S$80,000 to S$120,000 and the singles grant doubled from S$30,000 to S$60,000. The Family Grant and PHG remain at their current levels as of June 2026.

Enhanced CPF Housing Grant (EHG): The Largest Grant

The EHG is the flagship CPF housing grant, designed to help lower-income Singaporeans purchase their first flat. It replaced the Additional CPF Housing Grant (AHG) and Special Housing Grant (SHG) in September 2019, combining them into a single, more generous scheme with a sliding scale tied to household income.

Key eligibility conditions for the EHG (2026):

- At least one applicant must be a Singapore Citizen, and the household must include at least one other Singapore Citizen or Permanent Resident.

- All applicants and occupants must be first-timer applicants (no prior ownership of an HDB flat or private property in Singapore).

- Monthly household income must not exceed S$9,000 (families) or S$4,500 (singles buying a 2-room Flexi under the Single Singapore Citizen Scheme).

- All working applicants must have been employed continuously for at least 12 months and must be working at the time of the HFE letter application.

- The flat purchased must have a remaining lease of at least 20 years and must cover the youngest buyer until at least age 95.

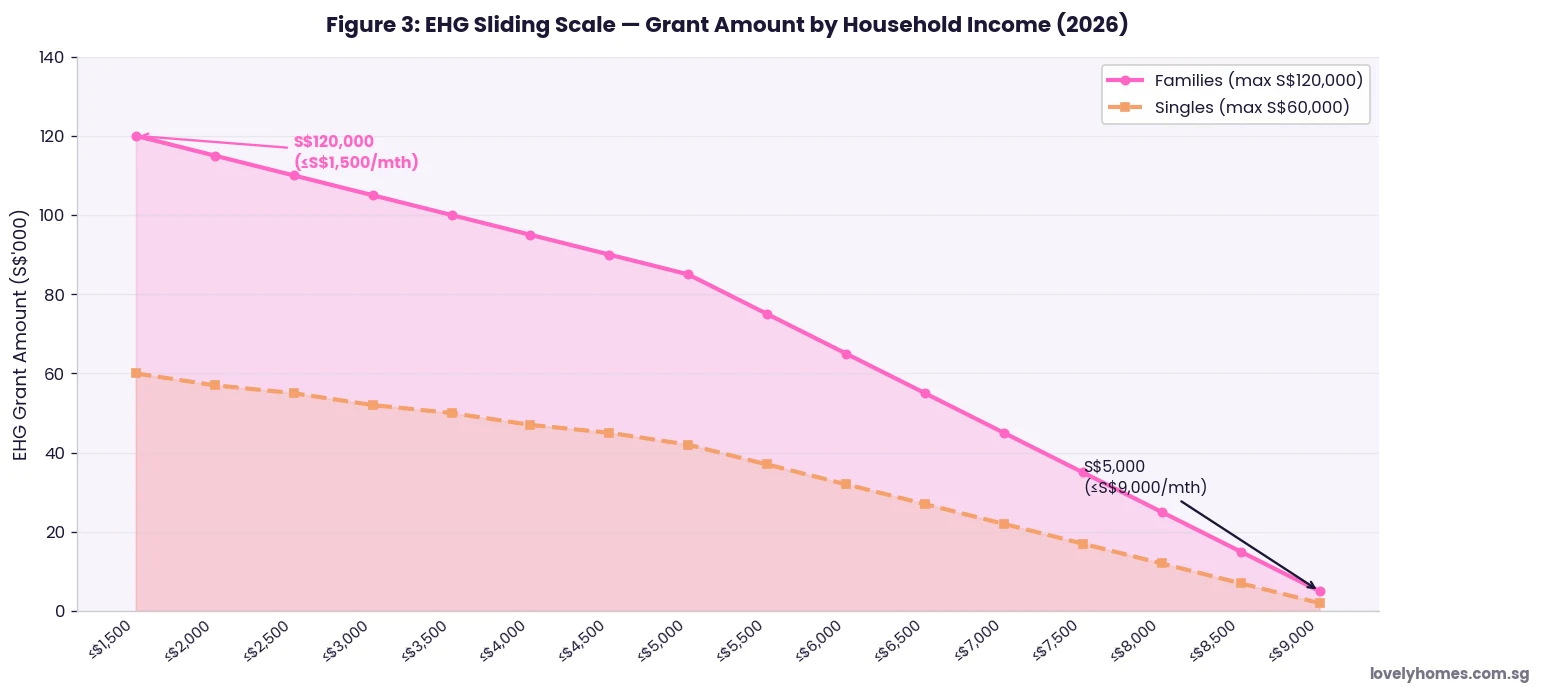

The EHG amount is determined on a sliding scale: applicants at the lowest income bracket (≤ S$1,500/month) receive the maximum S$120,000, tapering down to S$5,000 for households earning close to the S$9,000 ceiling. See Figure 3 for the full sliding scale. This design ensures that the subsidy is proportionally larger for those who need it most.

The EHG applies to both new BTO flats and resale HDB flats, making it one of the few grants usable across the full flat type spectrum. It does not apply to Design, Build and Sell Scheme (DBSS) flats or Executive Condominiums (ECs).

CPF Housing Grant (Family Grant): The Mainstream Grant

The Family Grant is available to Singapore Citizen households with a broader income range, up to S$14,000 per month. Unlike the EHG, it is not means-tested on a sliding scale — eligible buyers receive the full amount or nothing.

| Flat Type | Grant Amount (SC+SC) | Grant Amount (SC+SPR) | Income Ceiling |

|---|---|---|---|

| New 2-room Flexi to 4-room BTO | S$40,000 | S$30,000 | S$14,000/mth |

| New 5-room or larger BTO | S$40,000 | S$30,000 | S$14,000/mth |

| Resale 2-room to 3-room | S$40,000 | S$30,000 | S$14,000/mth |

| Resale 4-room and larger | S$50,000 | S$40,000 | S$14,000/mth |

| Singles (2-room Flexi resale only) | S$25,000 | N/A | S$7,000/mth |

Source: HDB, effective as of June 2026.

The Family Grant for resale 4-room and larger flats was raised to S$50,000 (SC+SC) and S$40,000 (SC+SPR) in the same August 2024 revision. This reflects the government’s effort to keep resale HDB flats affordable as median prices in many towns have risen sharply since 2020.

Proximity Housing Grant (PHG): Living Near Family

The Proximity Housing Grant was introduced in August 2015 to incentivise multi-generational proximity — a social policy objective as much as a financial one. It is unique in having no income ceiling, meaning even higher-income families can benefit from it when buying resale flats near parents or children.

The PHG pays S$30,000 if the applicant purchases a resale flat to live in the same flat as their parents or child (joint application or within the same household). It pays S$20,000 if the resale flat is purchased within 4 kilometres of the parent’s or child’s residence. The 4 km is measured using the straight-line distance between the two postal addresses. It applies to resale HDB flats only — it cannot be applied to BTO flats or DBSS flats.

To receive the PHG, at least one of the parents or child must be a Singapore Citizen or Permanent Resident. The proximity requirement must be maintained for five years after the key collection of the resale flat; failure to do so may result in a clawback of the grant.

Step-Up CPF Housing Grant and Other Targeted Grants

The Step-Up CPF Housing Grant of S$15,000 is specifically targeted at second-timer Singapore Citizen families who previously purchased a 2-room subsidised flat (BTO) and wish to upgrade to a 2-room to 4-room BTO flat. The income ceiling is S$7,000/month and the household must not own any other private property. This grant acknowledges the financial difficulty of moving up the housing ladder on a modest income.

The Seniors’ Priority Scheme (SPS) is not a cash grant but provides elderly Singapore Citizens aged 55 and above with priority allocation in BTO exercises when they are purchasing a 2-room Flexi flat near their adult children. Priority is given to multi-generational applicants — parents applying together with children — further reinforcing the proximity-and-community theme across Singapore’s housing grant framework.

How to Apply for CPF Housing Grants

All CPF housing grants are administered through a single gateway: the HDB Flat Eligibility (HFE) letter. Introduced in May 2023, the HFE letter replaced the previous system of separate Eligibility Letters for different grants. To apply, eligible buyers must log in to the HDB Flat Portal (flat.hdb.gov.sg) with their Singpass and submit an HFE application. The assessment is integrated with CPF and IRAS data and typically takes around 21 working days.

The HFE letter is mandatory before a buyer can:

- Book a BTO flat during a sales launch exercise;

- Exercise an Option to Purchase (OTP) for a resale HDB flat;

- Apply for an HDB loan.

Once issued, the HFE letter is valid for nine months. It confirms the buyer’s eligibility, the specific grants they qualify for and their amounts, and the maximum HDB loan they may borrow. Buyers must obtain a new HFE letter if their circumstances change materially (e.g., income, marital status, property ownership) or if the existing letter expires.

Grant Summary Table: All CPF Housing Grants at a Glance

| Grant | Max Amount | Min SC Required | BTO? | Resale? | Income Ceiling |

|---|---|---|---|---|---|

| EHG (Families) | S$120,000 | 1 SC | ✓ | ✓ | S$9,000/mth |

| EHG (Singles) | S$60,000 | Applicant is SC | ✓ | ✓ | S$4,500/mth |

| Family Grant (SC+SC) | S$50,000 resale 4R+ | 2 SC | ✓ | ✓ | S$14,000/mth |

| Family Grant (SC+SPR) | S$40,000 resale 4R+ | 1 SC | ✓ | ✓ | S$14,000/mth |

| PHG (living together) | S$30,000 | 1 SC/SPR | ✗ | ✓ | None |

| PHG (within 4 km) | S$20,000 | 1 SC/SPR | ✗ | ✓ | None |

| Step-Up Grant | S$15,000 | 1 SC | ✓ (2–4 Rm) | ✗ | S$7,000/mth |

Note: Buyers must be first-timers for EHG and Family Grant. Grants are not available for EC (Executive Condo) or private property purchases. Source: HDB, June 2026.

Worked Example: How Much Can Mr & Mrs Tan Actually Save?

📄 Worked Example — SC Couple Buying Resale 4-Room Flat in Tampines

Profile: Mr & Mrs Tan, both Singapore Citizens, first-time buyers. Combined household income S$7,800/month. Mrs Tan’s parents live in Tampines, 1.2 km from the flat they are considering. They have been employed continuously for 14 months.

Flat: 4-room resale HDB flat in Tampines, asking price S$620,000.

Grants they qualify for:

- EHG: Household income S$7,800/month → approximately S$35,000 (sliding scale; income ≤ S$7,500/month band).

- Family Grant (SC+SC, resale 4-room): S$50,000.

- PHG (within 4 km of Mrs Tan’s parents): S$20,000.

Total grants: S$35,000 + S$50,000 + S$20,000 = S$105,000

Effective purchase price after grants: S$620,000 − S$105,000 = S$515,000

Buyer’s Stamp Duty (BSD): On S$620,000 — 1% × S$180,000 + 2% × S$180,000 + 3% × S$260,000 = S$13,200

HDB Loan (at 80% LTV on effective price S$515,000): S$412,000 at 2.6% p.a. over 25 years → monthly instalment S$1,864/month (MSR: 23.9% — PASS at 30% ceiling).

Cash outlay at completion (5% cash + BSD + legal): 5% × S$515,000 + S$13,200 + S$2,500 (legal) = S$41,450 cash. Balance of CPF OA available for the remaining 15% down payment.

Note: Grant amounts are illustrative based on the published EHG sliding scale. Actual grant eligibility is confirmed via the HFE letter. BSD calculated on full purchase price (not after grants). CPF accrued interest at 2.5% p.a. applies to all CPF withdrawn.

Why CPF Housing Grants Matter: The Broader Policy Context

Singapore’s CPF housing grant framework is one of the most generous owner-occupier subsidy systems in Asia. In a city where median resale HDB flat prices have risen by roughly 40–55% since 2020, grants of S$100,000–S$230,000 provide meaningful relief for households in the S$4,000–S$9,000/month income band — the working and lower-middle class that earns too much for full public housing in many neighbouring countries but faces real affordability pressure in Singapore’s private market.

The August 2024 doubling of the EHG was a direct policy response to research showing that pre-grant affordability had deteriorated for first-timers in the S$5,000–S$9,000 income band since 2020. By front-loading the subsidy into the capital cost rather than the monthly instalment, HDB avoids the MAS mortgage stress-test complexity that would arise from an interest-rate subsidy model.

From a buyer’s perspective, the grants also have a leveraging effect: a S$120,000 EHG on a S$450,000 BTO flat reduces the loan quantum by 27%, lowering the debt-service burden by approximately S$540/month on a 25-year HDB loan — a meaningful improvement in household cash flow over the life of the mortgage.

What Might Change Next: Grant Policy Outlook 2026–2028

The August 2024 EHG increase followed roughly four years of HDB price inflation, suggesting that grant levels are periodically reviewed against affordability indices rather than adjusted on a fixed schedule. The following is editorial speculation based on observable trends and is not government policy.

Given that the URA private residential price index has continued to rise modestly in Q1 2026 (+0.5% QoQ) and HDB resale prices remain elevated (RPI 216.3 in Q1 2026), a further grant increase would not be out of place if the next round of BTO supply does not materially ease affordability pressure. The income ceiling for the EHG (S$9,000/month for families) was last revised in 2019; with median household income now at approximately S$10,000–S$11,000/month, there is a structural argument for raising the ceiling to include more middle-income households — though this would carry a significant fiscal cost.

There is also industry discussion about whether the PHG’s 4-km definition should be relaxed to accommodate households in sprawling new towns (Tengah, Punggol North) where the road network means 4 km of air-line distance may correspond to a 15-minute drive. Whether HDB adjusts the proximity metric to a travel-time standard remains to be seen.

Frequently Asked Questions

Can I use CPF housing grants for an Executive Condo (EC)?

If my income increases after receiving the grant, does HDB claw it back?

My parents live overseas. Can I still get the Proximity Housing Grant?

Can the grants be used to pay Buyer’s Stamp Duty or legal fees?

I previously sold an HDB flat and am buying again. Can I still get any grants?

What happens to the grants when I sell my flat?

Do foreigners or PRs qualify for CPF housing grants?

Related Articles

Click anywhere outside to close

0 Comments