Singapore HDB Ethnic Integration Policy Guide 2026: EIP Quotas, Resale Impact and Buyer Strategy

Quick Answer: HDB EIP Singapore 2026 — Key Takeaways

- The Ethnic Integration Policy (EIP) was introduced by HDB in 1989 to prevent racial enclaves from forming in Singapore’s public housing estates.

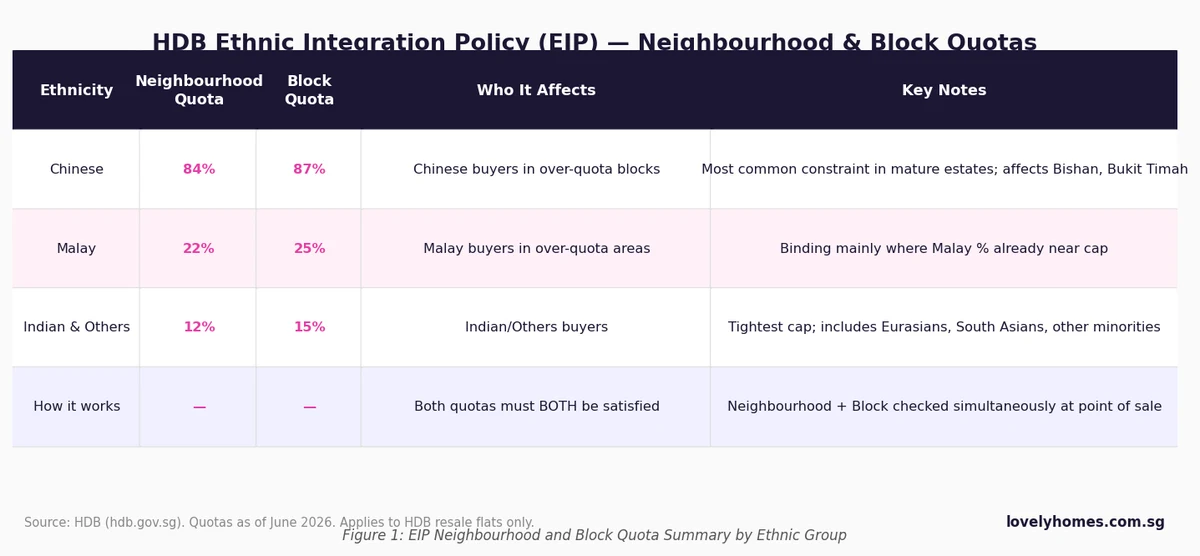

- EIP sets neighbourhood and block quotas for each ethnic group: Chinese 84%/87%, Malay 22%/25%, Indian & Others 12%/15%.

- EIP applies only to HDB resale flats — it does not apply to new BTO flats, private property, or HDB rental flats.

- If a block or neighbourhood has already reached the quota for your ethnic group, you cannot buy a resale flat there — regardless of any other eligibility criteria.

- Sellers in over-quota blocks face a restricted buyer pool: they can only sell to buyers whose ethnic group still has quota headroom, which can affect pricing and time on market.

- Always check the HDB Resale Portal before making any offer — EIP status is block-specific and changes as transactions are registered.

- EIP constraints are tightening in mature estates such as Bishan, Bukit Timah, Marine Parade, and Toa Payoh as proportions converge.

- Indian & Others buyers face the tightest cap (12% neighbourhood / 15% block) and are most frequently constrained in desirable central-region towns.

- Understanding EIP before shortlisting flats can save weeks of wasted negotiation and prevent abortive OTP costs.

What Is the Ethnic Integration Policy (EIP) and Why Does It Exist?

Singapore’s HDB towns are not only housing estates — they are, by deliberate government design, microcosms of the nation’s multiracial society. The Ethnic Integration Policy, administered by the Housing and Development Board (HDB) since 1 March 1989, is the mechanism that ensures Singapore’s public housing estates remain ethnically diverse rather than gradually concentrating into racial enclaves.

Before EIP, Singapore had begun to experience informal ethnic clustering in older estates. Certain mature towns developed notably higher concentrations of particular ethnic groups through natural social networks and community preferences. The government, recognising that segregated neighbourhoods could erode social cohesion — a cornerstone of Singapore’s national identity — introduced EIP to cap each ethnic group’s share at both the block and neighbourhood level, locking in a composition broadly reflective of Singapore’s national demographic make-up.

The rationale is straightforward: when neighbours share staircases, lifts, and void decks with people of different backgrounds, cross-cultural interaction occurs organically. EIP is the structural guarantee of that interaction. It operates not through direct regulation of individual choice — Singaporeans can still prefer certain towns, floor levels, or orientations — but by imposing a ceiling on the cumulative ethnic composition of any given block or neighbourhood.

How EIP Quotas Work: Neighbourhood and Block Levels

EIP operates at two simultaneous levels, and both must be satisfied for any resale transaction to proceed.

The neighbourhood quota reflects the ethnic composition of an entire planning area or neighbourhood zone (typically a cluster of several blocks). The block quota is more granular — it governs the ethnic proportion within a single HDB block. Because ethnic distributions are rarely uniform across a neighbourhood, a specific block may hit its ethnic ceiling even when the surrounding neighbourhood still has headroom. This means a buyer can be blocked at the block level even if the neighbourhood quota is technically not yet exhausted.

Crucially, these quotas are based on the resident population, not floor area. Each time a resale transaction is completed and a new household registers with HDB, the ethnic composition of that block and neighbourhood is recalculated. The thresholds — Chinese 84%/87%, Malay 22%/25%, Indian & Others 12%/15% — were originally calibrated to Singapore’s 1989 census ethnic composition and have remained substantially unchanged, though HDB reviews them periodically.

One important clarification: these quotas apply to the buyer’s ethnicity as declared on their NRIC, not to the seller’s ethnicity. A Chinese seller in a block that has reached its Chinese quota can only sell to a non-Chinese buyer — specifically, a Malay or Indian & Others buyer whose group still has remaining quota in that block. This restriction flips the usual power dynamic: in some over-quota blocks, sellers effectively have a constrained buyer pool regardless of the flat’s quality or market price.

EIP and Buyers: What to Check Before You Bid

For buyers, EIP is the first filter to apply — before engaging any conveyancer, before negotiating price, and certainly before exercising an Option to Purchase (OTP). The HDB Resale Portal (resale.hdb.gov.sg) provides a real-time EIP check for any block address. Buyers enter the block address and their NRIC ethnicity, and the system returns a pass or fail result. This check takes under a minute and is freely available to the public.

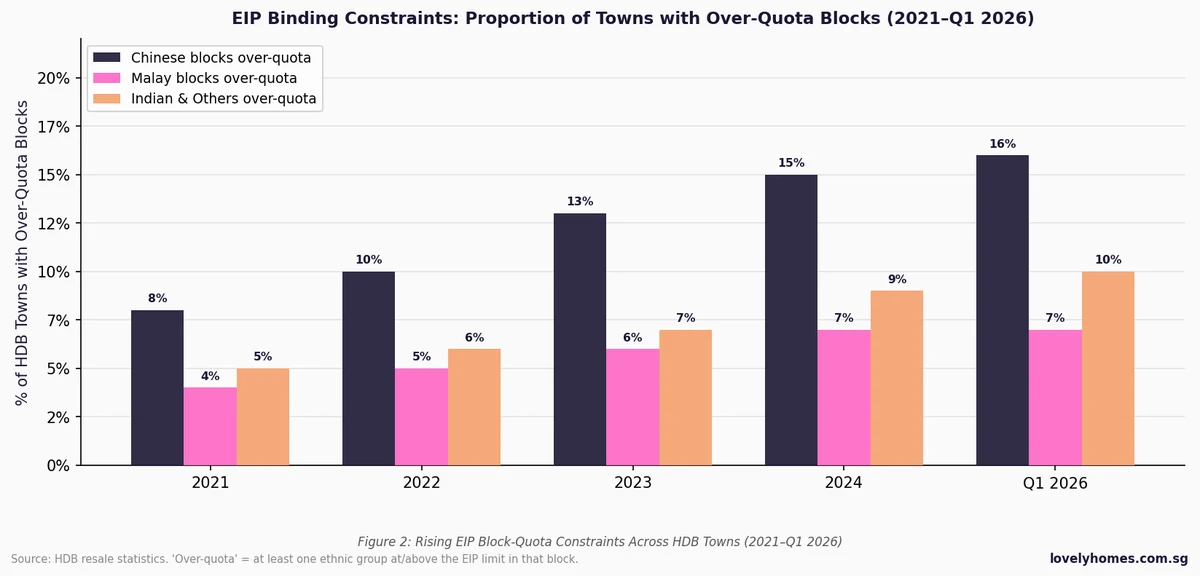

The trend in Figure 2 is instructive: the proportion of HDB towns with at least one over-quota block has risen steadily across all three ethnic categories since 2021. This is partly a function of natural demographic equilibration — as resale market activity in mature estates normalises ethnic proportions toward the cap — and partly driven by the prolonged resale boom since 2021. Higher transaction volumes accelerate quota convergence. Indian & Others buyers, working with the tightest caps, face the fastest-tightening constraints in central-region towns.

The practical implication is that buyers from minority groups should widen their shortlist geographically or be prepared to act quickly when a suitable flat in a quota-compliant block appears. It also means that a flat you viewed and loved on a Saturday may no longer be accessible by the following Wednesday if another transaction in that block tips it over the quota.

EIP and Sellers: Restricted Pools and Pricing Implications

For sellers, the EIP dynamic is less immediately visible but equally significant. If the block has reached or is near its quota for the seller’s ethnic group, the universe of eligible buyers shrinks to only those whose ethnic group still has headroom. In practice, this means a Chinese owner in a block already at 87% Chinese cannot sell to another Chinese buyer. The flat must be sold to a Malay or Indian & Others purchaser — and their demand in that specific block, at that price point, may be materially thinner.

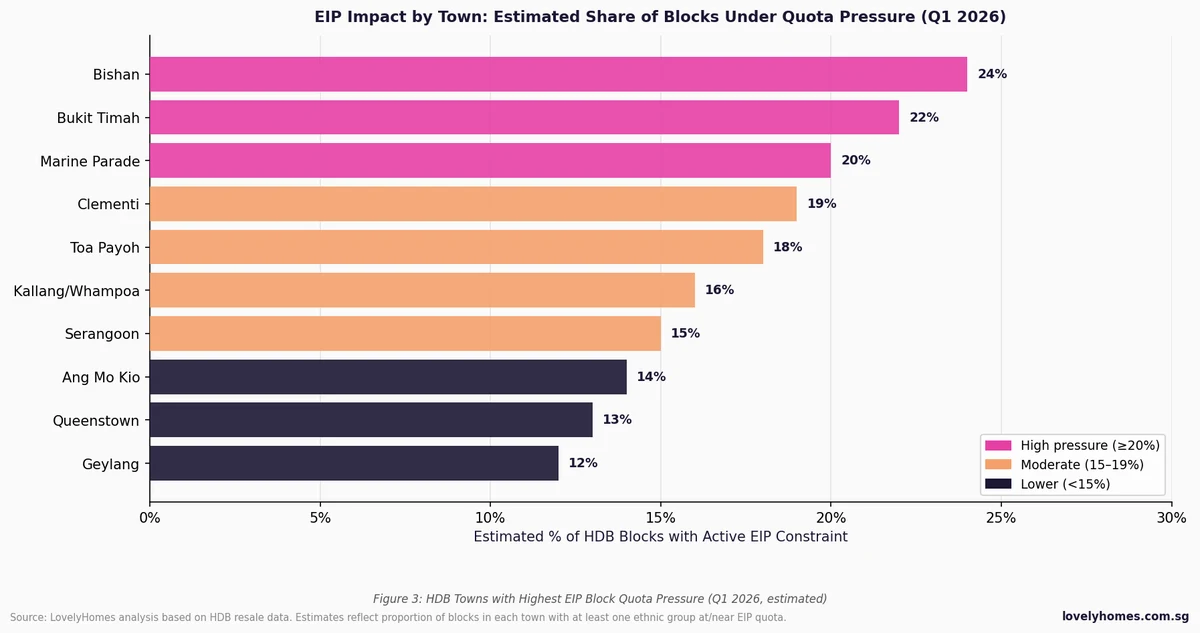

Towns with the highest EIP pressure (Figure 3) — including Bishan, Bukit Timah, Marine Parade, and Toa Payoh — are, notably, some of Singapore’s most sought-after mature estates with strong historical price appreciation. Sellers in these towns who happen to own flats in over-quota blocks may find that a smaller buyer pool translates to longer time-on-market and a need to price more competitively to attract the eligible ethnic minority. This can depress achieved prices relative to neighbouring quota-compliant blocks in the same town.

Conversely, sellers in blocks that remain quota-compliant — particularly in estates with robust Chinese demand — face no restriction on their buyer pool and can generally command fuller market prices. This creates an intra-town pricing differential that is sometimes overlooked by buyers and sellers alike.

EIP Rules at a Glance: Summary Table

| Rule / Parameter | Details |

|---|---|

| Administered by | Housing and Development Board (HDB) |

| Introduced | 1 March 1989 |

| Applies to | HDB resale flat transactions (not BTO launches, not private property) |

| Chinese quota | 84% (neighbourhood) / 87% (block) |

| Malay quota | 22% (neighbourhood) / 25% (block) |

| Indian & Others quota | 12% (neighbourhood) / 15% (block) |

| Determined by | Buyer’s declared ethnicity on NRIC |

| Both levels must pass | Yes — neighbourhood AND block quota checked simultaneously |

| How to check | HDB Resale Portal (resale.hdb.gov.sg) — free, real-time, block-specific |

| Consequence of breach | Transaction cannot proceed; no OTP can be exercised |

| Applies to SPR buyers | Yes — Singapore Permanent Residents declared on their Blue IC are subject to EIP |

Worked Example: The Tan Family’s EIP Navigation

Scenario: SC Indian couple upgrading to a 4-room resale flat in Queenstown

Mr and Mrs Selvam are Singapore Citizens (Indian ethnicity, NRIC declared). They have completed their HDB MOP on their 3-room Yishun flat and wish to upgrade to a 4-room resale flat in Queenstown (Queen’s Close / Tanglin Halt area) for the schools and proximity to work. Budget: S$700,000–S$750,000.

Step 1 — EIP Pre-check: They identify three blocks in the area. Using the HDB Resale Portal, they check each block against their Indian & Others ethnicity:

- Block A, Tanglin Halt Road — FAIL: Indian & Others block quota at 15% (over-quota). Cannot proceed.

- Block B, Commonwealth Drive — PASS: Indian & Others at 11%, headroom remains. Can proceed.

- Block C, Holland Avenue — FAIL: Neighbourhood quota at 12% ceiling. Cannot proceed.

Step 2 — Focus on Block B: A 4-room flat in Block B is listed at S$730,000. Valuation commissioned by HDB: S$718,000. Cash Over Valuation (COV): S$12,000 (must be paid in cash, cannot use CPF).

Step 3 — Cost breakdown:

BSD on S$730,000: First S$180,000 @ 1% = S$1,800 + Next S$180,000 @ 2% = S$3,600 + Remaining S$370,000 @ 3% = S$11,100 = S$16,500

ABSD: S$0 (SC couple buying first property as Indian & Others is not subject to ABSD on 1st purchase)

HDB resale admin fee: S$80 (for flat application)

Legal conveyancing: ~S$2,500

COV: S$12,000 (cash)

Total cash outlay (excluding down payment and loan): ~S$31,080

Outcome: By running the EIP check before negotiating, the Selvams avoided two abortive OTP exercises and focused their offer on the only compliant block. They secured the flat and received the HDB Flat Eligibility (HFE) letter confirming they meet all requirements including EIP.

Why EIP Matters: Social Engineering That Shapes Your Investment

EIP is one of the most distinctive features of Singapore’s housing system — a policy with no direct parallel in Hong Kong, South Korea, or Australia’s public housing sectors, all of which have faced varying degrees of ethnic concentration in social housing. Singapore’s approach is deliberately top-down: rather than leaving ethnic integration to market forces or individual goodwill, the government mandated it structurally.

From an investment standpoint, EIP creates a two-tier reality within the resale market. Quota-compliant blocks command the full market price because the buyer pool is unrestricted. Over-quota blocks may see price suppression — not because the flat is inferior, but because the eligible buyer pool is structurally smaller. Buyers who can only consider certain ethnic-group quotas must be particularly attentive to this dynamic, as it affects not only their own purchase but their eventual exit when they resell.

For upgraders from HDB to private property, EIP does not apply to the private transaction. However, the HDB flat they sell must comply with EIP — if they are selling from an over-quota block, they must find a buyer from the eligible ethnic group, which can extend the sale timeline and affect whether they can meet the 6-month window for ABSD remission on their subsequent private purchase.

What Might Come Next: The EIP in a Tightening Market

EIP quotas have remained largely static since 1989, calibrated to demographic proportions that have since shifted — Singapore’s Indian and Other Minority population share has grown modestly, while the Malay share has remained relatively stable. There is periodic academic and policy debate about whether the thresholds should be recalibrated to reflect updated census data, but HDB has not announced any revision as of June 2026.

As the resale market continues to transact at elevated volumes — driven by BTO supply shortfalls and strong demand from upgraders — EIP constraints in mature estates are likely to tighten further before any policy adjustment. Buyers in minority ethnic groups planning purchases in desirable central-region towns should factor in longer search timelines and a readiness to move quickly when compliant blocks become available. Those in the Chinese majority group face less immediate concern but should remain aware of the policy’s seller-side implications when they eventually exit their flats.

Frequently Asked Questions

Does EIP apply when I buy a new BTO flat directly from HDB?

No. EIP applies only to HDB resale transactions between private parties in the open market. When you purchase a new BTO flat directly from HDB at a launch exercise, HDB controls the allocation and manages ethnic integration through its own internal allocation criteria. You do not need to check EIP quotas for BTO applications. EIP becomes relevant only if you later sell your flat on the resale market, or if you are buying a resale flat from another owner.

Can I appeal to HDB if I fail the EIP check for a block I want?

There is no formal appeal mechanism to override an EIP failure for a specific block. The quotas are administered by HDB as hard limits — if the block or neighbourhood is over-quota for your ethnic group, the transaction simply cannot proceed in that block. Your practical options are: (a) search for another flat in a different block in the same town that is quota-compliant; (b) expand your search to a different town where quota headroom exists for your ethnic group; or (c) wait for an existing household in the over-quota block to sell and move out, which marginally reduces the ethnic proportion and may eventually restore headroom. HDB does not grant exceptions to EIP quotas for individual buyers.

Does EIP affect Singapore Permanent Residents (SPRs) buying HDB resale flats?

Yes. Singapore Permanent Residents are subject to the same EIP quotas as Singapore Citizens. HDB uses the ethnicity declared on the SPR’s Blue Identity Card (NRIC) to assess which ethnic group the buyer falls under for quota purposes. SPR buyers must satisfy both neighbourhood and block EIP quotas, in addition to the separate SPR eligibility rules for HDB resale flats (SPRs must form a family nucleus, must have held SPR status for at least 3 years, and are subject to their own resale eligibility conditions). Foreigners without SPR status cannot purchase HDB resale flats at all and are therefore unaffected by EIP.

What happens if EIP is breached after a sale — for example, if I make an error in my ethnicity declaration?

Making a false ethnic declaration to circumvent EIP is a serious offence under HDB’s framework and can constitute fraud. If HDB discovers that a buyer misrepresented their ethnicity — for example, declaring a different ethnic identity than that shown on their NRIC — HDB has the power to compulsorily acquire the flat at a price lower than market value, cancel the resale approval, or take other enforcement action. Buyers should use only the ethnicity as declared on their NRIC, even if they are mixed-race or identify differently culturally. Mixed-race buyers typically use the ethnicity registered with ICA on their NRIC, which may be either parent’s ethnicity depending on the registration at birth.

I am an Indian buyer. Can I buy a resale flat in a block where the Chinese quota is not yet reached, even if the Indian quota is full?

No. Your EIP eligibility is assessed based on your own ethnic group’s quota, not other groups’ quotas. If the Indian & Others block quota has been reached (15%), you cannot purchase that flat — regardless of whether the Chinese or Malay quotas still have headroom. The quotas function independently: each ethnic group’s proportion is measured against its own ceiling. The fact that another ethnic group still has room in the block does not create eligibility for an Indian & Others buyer whose group’s quota is full.

Does the EIP restriction affect landed HDB housing, such as terrace or semi-detached HDB properties?

HDB landed housing (such as the older HDB terrace houses in estates like Toa Payoh and Queenstown) is subject to EIP in the same way as HDB flats, as they are resale transactions on the open market. However, there is very limited HDB landed stock, and most of it is in mature estates where quota pressures can be acute. If you are considering an HDB landed property, you must run the same EIP check on the HDB Resale Portal. Note that HDB landed housing transactions are subject to all the usual HDB resale eligibility rules, MOP requirements, and HFE letter requirements in addition to EIP.

If I am selling an HDB flat in an over-quota block, how do I find eligible buyers efficiently?

The most effective approach is to advertise the listing with the EIP status disclosed upfront — noting which ethnic group(s) can purchase the flat — so that only eligible buyers engage with your listing. This saves time for both parties and reduces abortive OTP risks. Because the eligible buyer pool is smaller, you may need to price the flat more competitively or allow a longer marketing period. Note that while CEA-registered salespersons can help you market the flat, you remain responsible for ensuring EIP compliance — the HDB system will reject a resale application that fails the EIP check regardless of what has been agreed between buyer and seller. Always verify the buyer’s ethnicity against the current EIP status on the Resale Portal before exercising the OTP.

Click anywhere to close