Few parts of the Singapore housing system are as life-changing — and as easy to get wrong — as CPF housing grants. A fully-stacked grant package can shave a year or two of mortgage payments off a typical HDB purchase. Miss one, and you leave tens of thousands of dollars on the table.

This guide sets out the 2026 eligibility and quantum tables for the three grants most first-timer buyers will care about, plus how they interact with the Loan Eligibility / Housing Financial Eligibility (HFE) process. If you are earlier in the buying journey, start with our first-time buyer walkthrough.

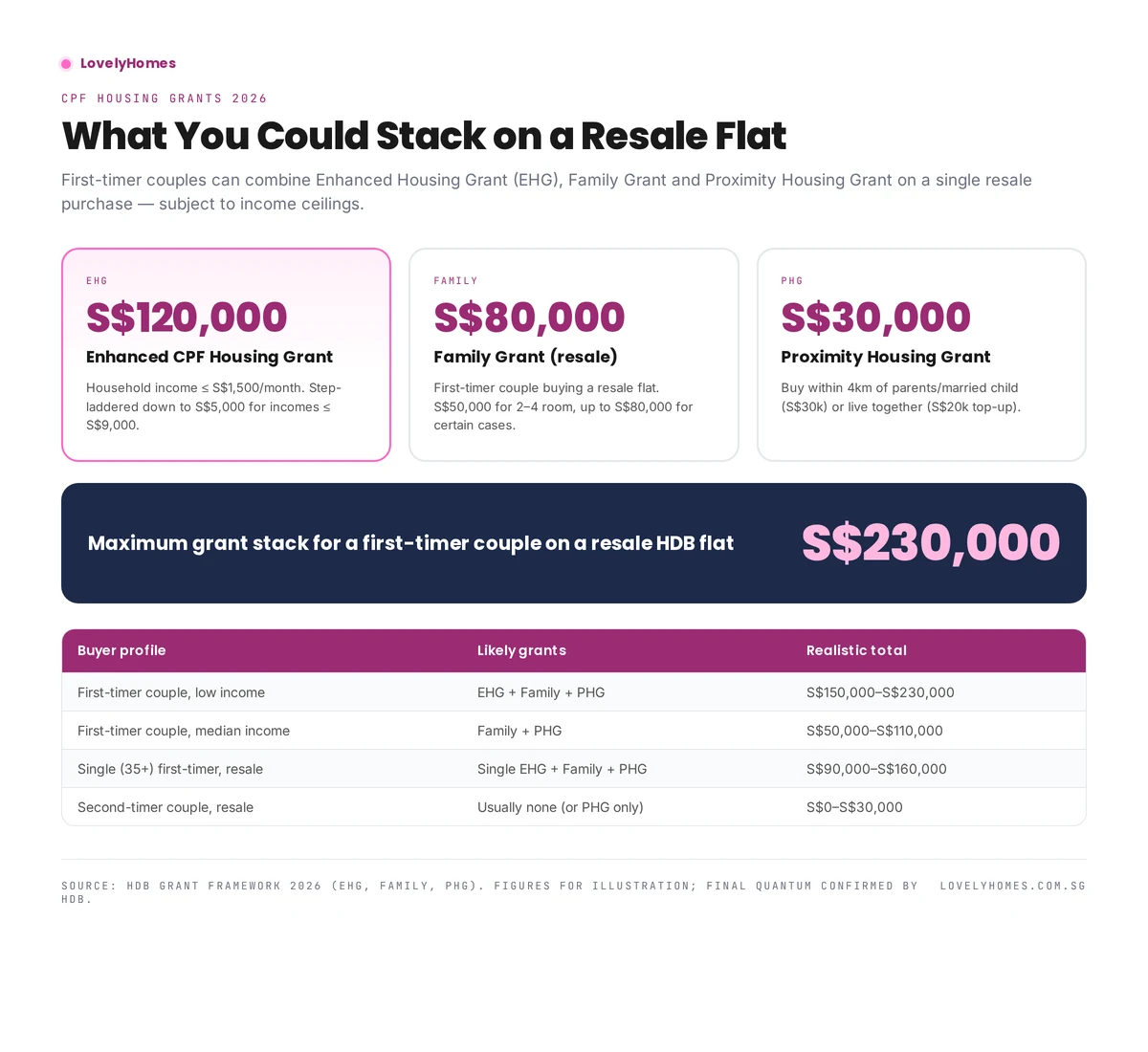

The three main grants, at a glance

| Grant | Max quantum | Applies to | Core eligibility |

|---|---|---|---|

| Enhanced CPF Housing Grant (EHG) | S$120,000 | BTO & resale | First-timer; income-laddered; 12 months continuous work |

| Family Grant | S$80,000 | Resale only | First-timer couple (or family nucleus); income ≤ S$14,000 |

| Proximity Housing Grant (PHG) | S$30,000 | Resale only | Buy within 4km of parents / married child (or live with them) |

Singles (aged 35+) get a parallel set of grants at roughly half the quantum, so a single first-timer can still stack a meaningful amount if they buy near parents.

EHG — the workhorse grant

EHG is the single biggest number on most HDB grant statements. It replaced the older Additional CPF Housing Grant and Special CPF Housing Grant in 2019 and now covers both BTO and resale flats. Quantum is a sliding income ladder: every extra S$500 of monthly household income typically drops you down one step of the ladder.

For the detailed income ladder and the employment rule, see our EHG deep-dive.

Family Grant — the resale booster

Family Grant only applies to resale purchases. For a first-timer Singaporean couple buying a 4-room or smaller resale flat, the quantum is typically S$50,000; for 2- to 4-room flats bought by first-timers, HDB has published enhancements that can push it toward S$80,000 in specific cases. The income ceiling sits at S$14,000 for the standard variant.

If only one spouse is a first-timer, the grant is normally halved (the “Half-Housing Grant” variant).

Proximity Housing Grant — the location reward

PHG is the grant that quietly reshapes purchase decisions. S$30,000 for buying within 4km of parents or a married child is big enough to nudge many buyers toward a particular estate or town. For the full rule set — including what “within 4km” actually means, how HDB measures it, and how singles qualify — see the Proximity Housing Grant guide.

How stacking works in practice

Grants are applied sequentially against the flat price and your CPF Ordinary Account at completion. They do not come to you as cash. The stack changes your effective purchase price, which in turn changes the amount you need to cover from CPF savings, cash, and housing loan.

A common error is assuming that you always get the headline maximum. In reality, the first-timer couple with S$7,000 monthly income will rarely see EHG of S$5,000 and Family Grant and PHG all at once — they usually skip EHG because the ladder has run out.

Worked example: first-timer couple, resale 4-room

| Assumption | Value |

|---|---|

| Combined household income | S$6,500/month |

| Flat bought | 4-room resale at S$650,000 |

| Distance from parents | 3.2km (straight line) |

| EHG (indicative) | S$30,000 |

| Family Grant | S$50,000 |

| Proximity Housing Grant | S$30,000 |

| Total grant | S$110,000 |

| Effective price | S$540,000 |

How and when to apply

Grants are decided as part of your HFE letter and the subsequent resale or BTO application. You do not apply for each grant separately — HDB computes your eligible stack based on the information you declare. The practical sequence is:

- Apply for an HFE letter on the HDB Flat Portal before you shop. The HFE already tells you which grants you are likely to receive.

- Keep your documents ready — income proofs (Income Tax NOA, CPF contribution history), parents’ addresses for PHG, and the first-timer statuses of both applicants.

- Submit the application (BTO ballot or resale application). HDB confirms your final grant eligibility once the flat is identified.

- Disbursement happens at completion (resale) or key collection (BTO). Grants top up your CPF OA and flow into the flat payment.

Common pitfalls

Four traps catch buyers most often: (a) one spouse quietly failing the 12-month continuous-work rule for EHG; (b) using gross vs net income incorrectly when estimating; (c) assuming PHG automatically applies to in-laws — it applies to married children, and to the biological or adoptive parents of either spouse; and (d) not realising Family Grant halves if only one of you is a first-timer.

Frequently asked questions

Can I get EHG twice?

No. EHG is a first-timer grant. If you already used EHG on a BTO, you cannot receive it again on a later resale purchase — you become a second-timer for grant purposes.

Do I need to pay the grant back if I sell?

The grant amount (plus accrued interest) is treated like a CPF withdrawal. When you sell the flat, you refund the grant + accrued interest to your CPF Ordinary Account — not back to HDB.

Does PHG require me to live in the same flat as my parents?

No. The S$30,000 PHG is for living within 4km. A S$20,000 variant applies for living together (as part of a single application with parents or married child).

Can singles apply?

Yes, from age 35 for most resale grants, at roughly half the couple quantum. Single EHG, Single Family Grant, and a singles version of PHG all exist.

Related guides

- First-time home buyer walkthrough — hub page covering HFE, budget and timeline.

- How to buy an HDB resale flat — the step-by-step process grants plug into.

- BTO application guide — EHG also applies to BTO purchases.

- Category: CPF for Property.

This guide is for general information only and is accurate as of April 2026. CPF grants, scheme quantum and eligibility rules are set by HDB / the Ministry of National Development and can change. Always confirm current rules on the HDB Flat Portal or with an HDB officer before committing. We are not a financial or legal advisor.

0 Comments