EHG is the grant that does most of the heavy lifting in any first-timer CPF housing grant package. It is also the most frequently miscalculated, because the income ladder and the employment rule together decide a number that can swing by S$90,000.

What EHG replaced

Before September 2019, first-timers navigated a confusing mix of Additional CPF Housing Grant and Special CPF Housing Grant, with different rules for BTO vs resale and for flat size. EHG rolled them into a single sliding ladder that applies equally to BTO and resale flats. The headline change: the income ceiling rose to S$9,000 (from S$5,000–S$8,500 depending on scheme), so many middle-income households now qualify for at least a modest grant.

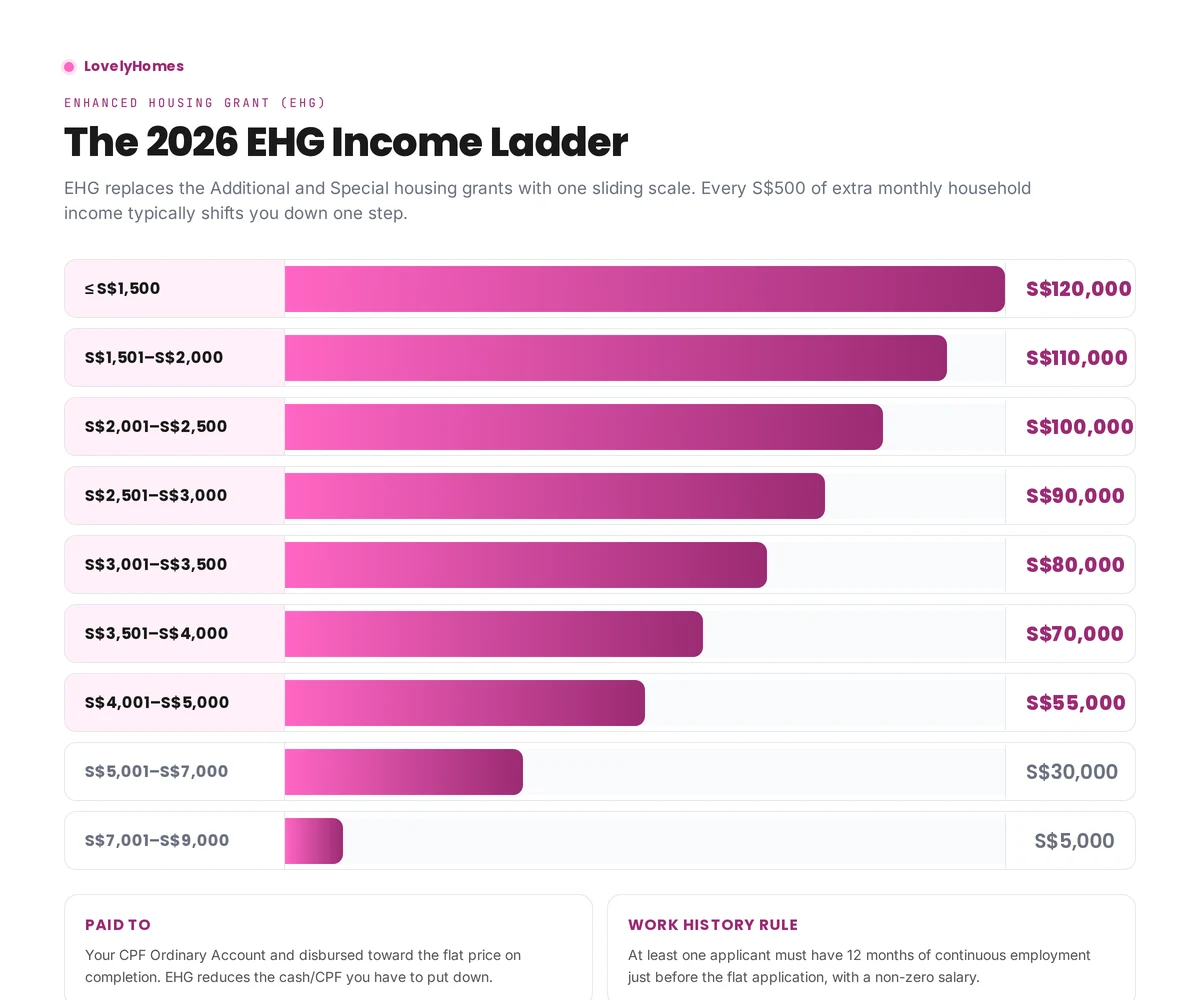

The 2026 quantum ladder

| Gross monthly household income | EHG quantum |

|---|---|

| ≤ S$1,500 | S$120,000 |

| S$1,501 – S$2,000 | S$110,000 |

| S$2,001 – S$2,500 | S$100,000 |

| S$2,501 – S$3,000 | S$90,000 |

| S$3,001 – S$3,500 | S$80,000 |

| S$3,501 – S$4,000 | S$70,000 |

| S$4,001 – S$5,000 | S$55,000 |

| S$5,001 – S$7,000 | S$30,000 |

| S$7,001 – S$9,000 | S$5,000 |

| > S$9,000 | Not eligible |

Singles aged 35 and above get roughly half the quantum under the Singles EHG variant, with an equivalent income ceiling of S$4,500.

Eligibility beyond income

Three gates matter beyond income:

- First-timer status. You (and your spouse, for couple applications) must never have received a housing subsidy, BTO flat, DBSS flat, EC direct from developer, or CPF housing grant.

- Singapore Citizen. At least one applicant must be an SC. For couple applications, the spouse can be an SC or SPR.

- Continuous work. At least one applicant must have worked continuously for the 12 months immediately before the flat application, with a non-zero salary. Short gaps (e.g. a fortnight between jobs) are usually tolerated; extended career breaks usually disqualify.

How EHG is paid out

EHG is not cash. It is credited into your CPF Ordinary Account and immediately disbursed toward the flat price on completion. The practical effect is that your CPF OA deduction and the amount you have to put down in cash / loan fall by the grant amount.

Because the grant lands in CPF OA first, it is treated like a CPF withdrawal for accrued-interest purposes. When you sell the flat, you refund the grant amount plus CPF accrued interest to CPF OA — not back to HDB.

EHG on BTO vs resale

| Aspect | BTO | Resale |

|---|---|---|

| Quantum | Same ladder | Same ladder |

| Payment timing | On key collection | On legal completion |

| Effect on income eligibility | Checked at balloting | Checked at HFE + resale application |

| Stackable with Family Grant | N/A (Family is resale only) | Yes |

| Stackable with PHG | N/A | Yes |

Worked example

Daniel and Priya earn a combined S$5,500 per month. They plan to buy a 4-room BTO flat in Tengah. EHG drops them into the S$5,001–S$7,000 band: S$30,000. That grant reduces their CPF OA deduction on key collection; their cash-over-CPF contribution stays the same, but their ongoing mortgage is based on a smaller principal.

Two years later, their incomes rise to a combined S$7,200 — no clawback applies, because EHG eligibility is assessed at application time only. If they had applied after the pay rise, they would have fallen into the S$7,001–S$9,000 band and received only S$5,000 — a S$25,000 swing driven purely by timing.

Common mistakes

The biggest mistake is mis-reporting income. HDB verifies income against CPF contribution records and NOA, so overstating (to qualify for a bigger loan) or understating (to qualify for a bigger grant) is caught quickly. The second biggest mistake is underestimating the 12-month employment rule — freelancers and variable-income workers should keep careful CPF contribution records.

Frequently asked questions

Can I get EHG if my spouse does not work?

Yes, as long as the working spouse meets the 12-month continuous employment rule and the household income is within the ceiling.

Is EHG taxable?

No. CPF housing grants are not taxable income.

What counts as “income” for EHG?

Gross monthly household income — salary, allowances, bonuses pro-rated across the year, and variable commissions. Excludes CPF contributions and reimbursements. HDB uses a rolling 12-month average where relevant.

Can EHG be used with the HDB Concessionary Loan?

Yes. EHG simply reduces the purchase price you need to finance — it works with both HDB Concessionary Loans and bank loans.

Related guides

- CPF Housing Grants 2026: complete eligibility table.

- TDSR & MSR affordability — how EHG affects your loan sizing.

- HDB loan vs bank loan.

This guide is for general information only and is accurate as of April 2026. CPF grants, scheme quantum and eligibility rules are set by HDB / the Ministry of National Development and can change. Always confirm current rules on the HDB Flat Portal or with an HDB officer before committing. We are not a financial or legal advisor.

0 Comments