First-timer families can receive up to S$80,000 in Enhanced CPF Housing Grant (EHG) for BTO or resale flats (household income ≤ S$9,000/month).

Singles buying a 2-Room Flexi BTO qualify for up to S$40,000 EHG (individual income ≤ S$4,500/month).

Resale buyers can stack the Family Grant (up to S$50,000) with the EHG and the Proximity Housing Grant (PHG, up to S$30,000) — potentially S$160,000 in total grants.

The PHG has no income ceiling and rewards buyers who live near or with parents or children.

All CPF grants go into your CPF Ordinary Account (OA) and are used against the purchase price — but they accrue interest that must be refunded upon sale.

Grants do not eliminate your cash component of the downpayment — at least 5% cash is still required for bank loans.

Applications are via the HDB flat portal and must be completed before exercising the Option to Purchase (OTP).

What Are CPF Housing Grants and Who Administers Them?

CPF Housing Grants are direct subsidies paid by the Singapore Government into the buyer’s CPF Ordinary Account (OA) to help Singaporeans afford their first — and in some cases, second — HDB flat. They are administered jointly by the Housing & Development Board (HDB) and the Central Provident Fund Board (CPF Board), with eligibility rules updated periodically to reflect prevailing market conditions and government housing policy.

Unlike an ABSD remission or a bank subsidy, a CPF Housing Grant is a genuine cash transfer from the public purse into your CPF OA. It immediately reduces the amount you need to borrow or fund from savings, which lowers your monthly mortgage instalment. However, grants are not free in the accounting sense: when you eventually sell the flat, the grant amount — plus accrued interest at the CPF OA rate of 2.5% per annum — must be refunded back into your CPF OA. The net effect is deferred rather than eliminated cost.

As of 26 April 2026, the key grant types in force are the Enhanced CPF Housing Grant (EHG), the Family Grant, the Proximity Housing Grant (PHG), and the Step-Up CPF Housing Grant for eligible second-timers under the Fresh Start Housing Scheme.

Enhanced CPF Housing Grant (EHG) — Rates and Eligibility

The Enhanced CPF Housing Grant, introduced in September 2019 to replace the Additional CPF Housing Grant (AHG) and Special CPF Housing Grant (SHG), is the flagship subsidy for first-timer buyers. It is progressive — the lower the household income, the higher the grant — and applies to both new BTO flats and resale HDB flats, making it more flexible than its predecessors.

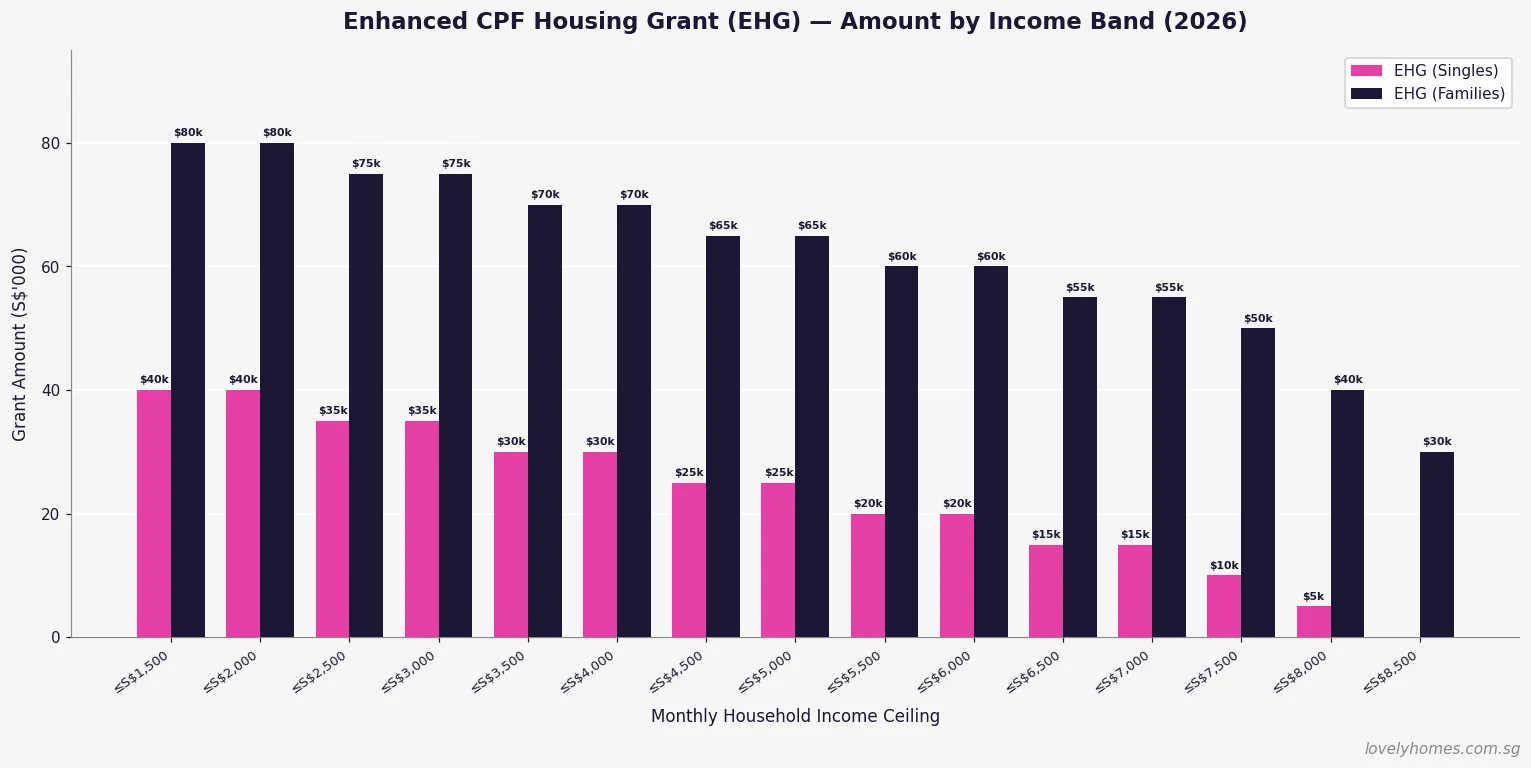

Figure 1: EHG amounts (S$’000) for singles vs families, by monthly household income band. Source: HDB (2026).

EHG for Families

For married or engaged couples — including those applying under the Fiancé/Fiancée Scheme — the EHG ranges from S$5,000 (household income ≤ S$8,000/month) to S$80,000 (household income ≤ S$1,500/month). The income assessed is the average gross monthly income of both applicants over the 12 months preceding the application. If the combined household income exceeds S$9,000/month, no EHG is payable.

EHG for Singles

First-timer singles aged 35 and above buying a 2-Room Flexi BTO flat in a non-mature estate qualify for EHG on a scaled basis, up to S$40,000 (individual income ≤ S$1,500/month). A single with income ≤ S$4,500/month qualifies for a minimum S$5,000 grant. Singles buying resale flats under the Single Singapore Citizen (SSC) scheme are also eligible, provided they purchase a 5-room flat or smaller.

Monthly Gross Income (Household)

EHG — Families

EHG — Singles

≤ S$1,500

S$80,000

S$40,000

≤ S$2,500

S$75,000

S$35,000

≤ S$3,500

S$70,000

S$30,000

≤ S$4,500

S$65,000

S$25,000

≤ S$5,500

S$60,000

S$20,000

≤ S$6,500

S$55,000

S$15,000

≤ S$7,500

S$50,000

S$10,000

≤ S$9,000

S$30,000–S$40,000

Not eligible

Family Grant — For Resale HDB Buyers

The Family Grant is available exclusively to buyers of resale HDB flats and is stackable on top of the EHG. It acknowledges that resale flat prices in many estates carry a premium over BTO prices, and provides an additional buffer for buyers who prefer a specific location or immediate occupancy over the BTO ballot process.

The Family Grant is administered by HDB and paid into the CPF OA of eligible applicants. Key parameters as of 2026:

SC + SC couple or family: S$50,000

SC + SPR couple or family: S$40,000

Singles (SSC scheme, resale 5-room or smaller): S$25,000

Income ceiling: S$14,000/month combined household income

Flat type restriction: any resale flat type; no restriction by town or estate

The S$14,000/month income ceiling makes the Family Grant accessible to many dual-income professional couples who earn too much for the EHG but still value the additional subsidy when purchasing resale.

Proximity Housing Grant (PHG) — Rewarding Family Ties

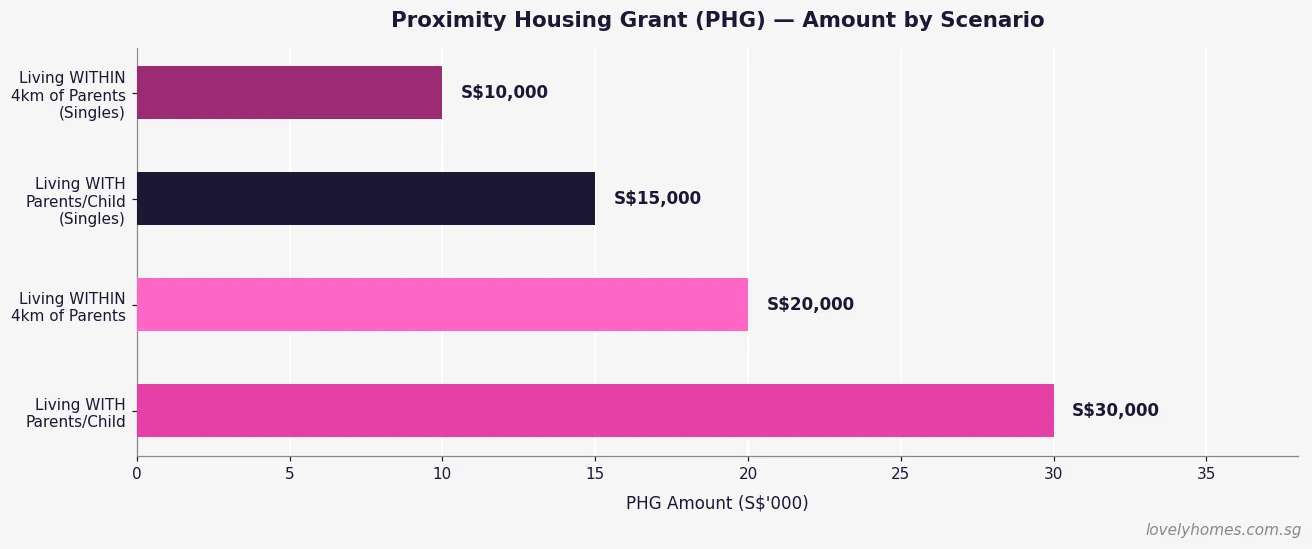

Introduced in August 2015, the Proximity Housing Grant is one of the most distinctive features of Singapore’s housing policy. It uses a direct cash subsidy to incentivise multi-generational proximity — encouraging adult children to live near, or with, their elderly parents. It applies only to resale HDB flats and has no income ceiling, meaning higher-earning buyers can benefit too.

Figure 3: PHG amounts by proximity scenario, for families and singles. Source: HDB (2026).

The PHG has four tiers based on whether you are buying as a family or single, and whether you are moving with parents or children (same household) or within 4 km of them:

Buyer Type

Living With Parents/Child

Living Within 4 km

Families (married/engaged couples)

S$30,000

S$20,000

Singles (SSC scheme)

S$15,000

S$10,000

The “living with” criterion requires the parent or child to be registered on the same flat as an occupier. The “within 4 km” criterion uses the straight-line distance between postal codes, verified at the point of application. The PHG is a one-time benefit — once received, it cannot be claimed again on a subsequent flat purchase.

Step-Up CPF Housing Grant — Fresh Start Scheme

The Step-Up CPF Housing Grant is a targeted measure for a specific group: second-timer applicants who previously owned a subsidised flat and now qualify for a second chance at affordable owner-occupied housing under HDB’s Fresh Start Housing Scheme, which was introduced in October 2016 and expanded over subsequent years.

Eligibility is tightly defined: second-timer families with at least one child aged under 16; monthly household income ≤ S$7,000; must apply for a 2-Room Flexi BTO flat; must not currently own a flat or private residential property; and must fulfil a 5-year Fresh Start Housing Scheme Minimum Occupation Period on the new flat. The grant amount is up to S$50,000. It is not stackable with the EHG.

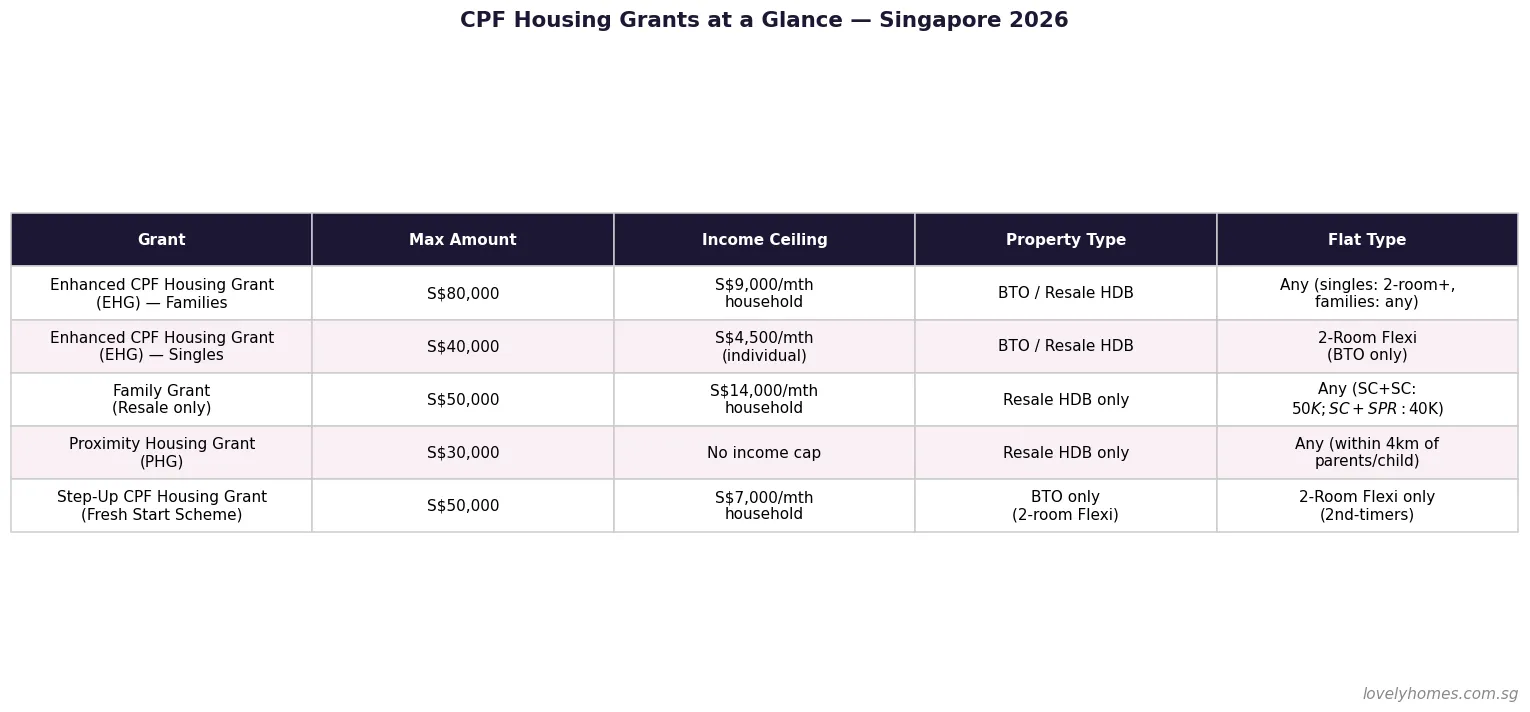

CPF Housing Grants at a Glance — Summary Table

Figure 2: Summary of all CPF Housing Grant types — amounts, income ceilings, and eligible property types. Source: HDB / CPF Board (2026).

Worked Example — Maximum Grant Stack for a Resale Buyer

Scenario: SC + SC First-Timer Couple, Resale Flat Near Parents

Buyer profile: Mr and Mrs Tan — married, both Singapore Citizens, first-timer applicants. Combined monthly gross income: S$6,800. Mrs Tan’s parents reside in the same block as the resale flat they are purchasing in Ang Mo Kio.

EHG (family, income band S$6,500–S$7,500): S$50,000

Family Grant (SC + SC, resale): S$50,000

PHG (same block as parents = “living with”): S$30,000

Total grants: S$130,000

Purchase price: S$600,000 (4-Room resale, Ang Mo Kio) Effective net cost after grants: S$470,000 (before stamp duties and legal fees). BSD on S$600,000: approximately S$12,600. ABSD: Nil (first residential property, Singapore Citizen buyers). Legal / conveyancing fees: approximately S$2,500–S$4,000.

Taking an HDB concessionary loan at 90% LTV: loan = S$540,000 less S$130,000 grants = S$410,000 loan needed, reducing the monthly instalment significantly versus purchasing without grants.

The CPF Accrued Interest Rule — The Hidden Cost of Grants

Every dollar drawn from your CPF OA — including grant monies — accrues interest at the CPF OA rate (currently 2.5% per annum). When you sell the flat, the CPF Board requires you to refund the principal amount used (including grants) plus the hypothetical interest that amount would have earned in the OA. This refund is returned to your CPF OA — not the government — and is available for future use in retirement or a subsequent property purchase.

Practical implication: a S$80,000 EHG held for 10 years accrues approximately S$22,000–S$25,000 in interest (compounded at 2.5% p.a.), bringing the total CPF refund for the grant alone to roughly S$102,000–S$105,000. Plan for this when modelling net sale proceeds on exit. If the sale price is insufficient to cover the full CPF refund, you keep the shortfall — you are not personally liable to top up the difference.

Why CPF Housing Grants Matter for Singapore’s Property Market

CPF Housing Grants fulfil a dual function in Singapore’s property ecosystem. At the individual level, they represent one of the most powerful demand-side subsidies in the world — transferring significant public funds directly to low- and middle-income buyers to help them achieve owner-occupation without over-relying on private financing. At the market level, they compress effective pricing for first-timers in the HDB resale segment, sustaining affordability across economic cycles.

The 2019 introduction of the EHG deliberately raised the income ceiling to S$9,000/month (from S$6,000/month under the legacy AHG/SHG regime), reflecting the Government’s recognition that median household incomes had risen and the historical ceilings were excluding a growing segment of first-timers who genuinely needed assistance.

Compared with equivalent policies in Hong Kong — where the Home Ownership Scheme provides a flat discount on market price rather than a direct grant — or Australia, where the First Home Owner Grant is a modest flat sum, Singapore’s progressive, stackable grant framework is both more generous and more targeted to income need.

What Might Come Next — Grant Policy Outlook for 2026–2028

The CPF Housing Grant framework is reviewed periodically in tandem with BTO flat pricing and HDB resale indices. Three plausible near-term developments:

EHG income ceiling revision: With household income growth continuing, HDB may raise the S$9,000/month family ceiling to extend coverage to the lower-professional bracket — especially as Prime Location Public Housing (PLH) flat prices edge towards S$700,000–S$800,000 in central estates.

PHG extension to BTO buyers: Currently restricted to resale buyers, extending the PHG to BTO buyers in family-friendly towns like Tengah and Bidadari has been discussed in policy circles, though not confirmed as of this date.

Grant indexing to flat type or BTO pricing band: A flat S$80,000 EHG ceiling becomes proportionally less meaningful as PLH BTO prices climb. Grant amounts indexed to flat type could better reflect affordability gaps across different segments.

These are speculative. Always verify current grant levels at the HDB Grant Eligibility page before exercising any OTP.

Frequently Asked Questions

Can I use CPF Housing Grants towards the downpayment?

Grants are credited into your CPF OA and can be applied in the same way as your own CPF savings — towards the downpayment, the purchase price, and stamp duties (BSD). However, if you are taking a bank loan, the minimum 5% cash downpayment must be paid in cash; CPF (including grants) cannot cover this component. If you are taking an HDB concessionary loan, there is no mandatory cash component, so grants can fully offset the downpayment requirement alongside your other CPF OA balance.

Can both the EHG and Family Grant be claimed for the same resale flat purchase?

Yes. For resale flat purchases, a first-timer SC couple can claim both the EHG and the Family Grant simultaneously, provided they meet the eligibility criteria for each. If the couple also qualifies for the PHG — for example, buying near parents — that can be added on top. The theoretical maximum for an SC + SC couple buying resale is S$80,000 (EHG) + S$50,000 (Family) + S$30,000 (PHG living-with) = S$160,000, though achieving the maximum EHG requires a household income ≤ S$1,500/month, which is uncommon for buyers at today’s resale prices.

Does receiving a CPF Housing Grant affect my HDB Loan Eligibility (HLE)?

Grants and HLE are assessed separately. Your HDB Loan Eligibility letter determines the maximum HDB concessionary loan you can borrow, based on income, credit history, outstanding debts, and MSR/TDSR compliance. Grants reduce the net amount you need to borrow, but the HLE loan quantum is not directly inflated by the grant. You apply for both the HLE and the grant through the HDB flat portal before exercising the OTP.

I am a Singapore Permanent Resident married to a Singapore Citizen. What grants are we eligible for?

An SC + SPR couple counts as a mixed-citizenship household for CPF grant purposes. You are eligible for the EHG at the family rate (since one applicant is SC), the Family Grant at the reduced SC + SPR amount of S$40,000, and the PHG if applicable. You are not eligible for the full SC + SC Family Grant of S$50,000. The SPR spouse’s income is included in the combined household income calculation for EHG and Family Grant means-testing.

What happens to my grant if I divorce after purchasing the flat?

Divorce does not trigger a grant clawback. The grant remains in the CPF OA of the respective owner(s) and normal CPF refund-on-sale rules apply. However, if the divorce results in one party retaining the flat and the other being bought out, the outgoing party’s CPF contributions — including grant amounts attributed to them — must be refunded at that point, with accrued interest. This is handled through the matrimonial asset division process, usually with the assistance of a family law solicitor.

Can I appeal for a higher grant if my income is irregular or I am self-employed?

Yes. HDB uses average gross monthly income over the 12 months preceding the application for means-testing. If your income is irregular — for example, you are a freelancer, commission-based worker, or recently returned to employment — HDB has a declared income process for the self-employed and an appeal mechanism for unusual circumstances. Supporting documents such as Notice of Assessment from IRAS, payslips, or CPF contribution history are typically required. Speak to an HDB branch officer early in the process if your income situation is non-standard.

Do the grants expire if I do not use them within a certain period?

CPF Housing Grants are credited into your CPF OA at the point of flat purchase — they are not a time-limited voucher. However, your eligibility to receive grants can change: if your income rises above the ceiling before application, or if you purchase a private property before your HDB flat, you may lose eligibility. The grant application must be submitted before you exercise the Option to Purchase, and the grant is disbursed only upon completion of the purchase.

Disclaimer: This article is intended for general information only and does not constitute financial, legal, or tax advice. CPF Housing Grant amounts, income ceilings, and eligibility conditions are subject to change. Always verify current grant details on the official HDB Grant Eligibility page and the CPF Board Home Ownership page. Consult a licensed property agent (CEA-registered) or HDB branch officer before making any purchase decision.

Quick Answer — the May 2026 BTO launch in five bullets

HDB’s quarterly Build-to-Order exercise is expected to open in mid-May 2026, the second of four regular 2026 launches after February’s exercise.

The May window will sit inside the new Standard / Plus / Prime flat-classification framework, meaning subsidy-recovery clawbacks and 10-year MOP apply to any Plus or Prime flat selected.

Applicants should have CPF Housing Grant eligibility, HDB Financial Information (HFE) letter, and preferred-town shortlist ready before the launch opens — the application window is short (one week).

First-timer families with young children benefit most from the First-Timer (Parents and Married Couples) priority scheme introduced in the August 2024 exercise.

Balance-ballot strategy: in oversubscribed towns, a second-timer or non-priority applicant’s realistic chance of selection is often under 1 in 8 — pick towns where the queue-to-unit ratio is lower.

BTO Framework — Standard · Plus · Prime — LovelyHomes editorial infographic, 22 April 2026.

Why the May 2026 launch matters

The May 2026 BTO exercise lands at a pivotal moment for HDB policy. The Standard / Plus / Prime classification — rolled out from the October 2024 launch — has now been applied across five full launches, and the August 2024 refinement of the First-Timer priority scheme has reshaped how families are slotted into the ballot queue. Applicants who last studied the BTO rulebook before 2024 will find materially different mechanics.

The May slot also traditionally carries heavier volume than February: the Ministry of National Development’s 2026 guidance is approximately 19,600 BTO units across the year, and historically the May and November exercises each release roughly a quarter of annual supply. That means a realistic expectation is 4,500–5,500 units across non-mature and mature-town estates, with a meaningful portion earmarked under the Plus or Prime bands.

Standard, Plus, Prime — what the three bands actually mean

HDB reclassified BTO flats from “mature” / “non-mature” to a three-band framework in October 2024. The band is tied to the flat’s location attributes — proximity to the CBD, to MRT interchanges, to established amenities — rather than the age of the surrounding estate. Each band has its own pricing approach, subsidy profile, resale restrictions and income-ceiling rules.

BTO Classification Bands — May 2026 Framework

Source: HDB Standard/Plus/Prime guidelines · Effective from October 2024 BTO exercise

Band

Typical location

MOP

Resale conditions

Standard

Non-central towns with standard amenities

5 years

Standard resale rules; no subsidy clawback

Plus

Choicer locations, near amenities or transport

10 years

Subsidy clawback on resale; income ceiling on buyer

Prime

Most central or premium locations

10 years

Higher subsidy clawback; income ceiling; no renting out of whole flat

Key shift: under Plus and Prime, the subsidy recovery at resale is calculated as a percentage of resale price, not a fixed dollar figure — which protects HDB’s public investment when values appreciate meaningfully.

Which towns have featured in recent launches

Exact May 2026 town selection is announced by HDB approximately two weeks before the launch opens. Based on the pattern of recent launches, applicants can reasonably expect coverage spanning all three regions — typically two to three non-mature towns, two mature towns, and at least one site in a new or emerging estate such as Tengah or Bayshore.

In the February 2026 exercise, HDB launched units in Tampines, Woodlands, Queenstown, Toa Payoh, and Yishun, with a strong skew to Plus-classified units in the more central towns. The May launch is widely expected to include Punggol, Sengkang, Jurong West, Bukit Merah and Kallang/Whampoa — but this is projection, not confirmation.

Applicants who want the highest chance of selection should keep an open geographic mind: Bukit Batok, Choa Chu Kang, Bukit Panjang and Sembawang have historically carried queue-to-unit ratios below 2 for four-room Standard flats, versus ratios of 5–9 in choicer Plus or Prime locations.

The First-Timer priority reshuffle — who benefits most in May

From the August 2024 exercise onwards, HDB restructured the First-Timer priority scheme into three tiers:

First-Timer (Parents and Married Couples) — or FT (PMC) — married couples with at least one Singaporean child below 18, or engaged couples with a projected child, receive three ballot chances for any non-mature Standard, Plus or Prime flat.

First-Timer (Family) — or FT (F) — all other first-timer families without young children receive two ballot chances.

Non-First-Timers — one ballot chance for non-mature Standard flats only.

The practical impact: an FT (PMC) applicant’s effective probability of being invited to a selection appointment is approximately 1.5x that of an FT (F) applicant in the same queue — not a guarantee of selection, but a materially better ballot position. Couples expecting to apply in May 2026 and carrying a child below 18 should ensure their family nucleus is registered correctly on the HFE letter; a missed declaration loses the PMC priority.

The HFE letter — your pre-application gatekeeper

Since the May 2023 exercise, an HDB Financial Information (HFE) letter is required before submitting a BTO application. The HFE is an integrated eligibility assessment covering:

Flat and grant eligibility (CPF Housing Grants, EHG, Proximity Housing Grant)

HDB Housing Loan Eligibility Letter (where applicable)

Mortgage Servicing Ratio (MSR) and Total Debt Servicing Ratio (TDSR) assessment

Final affordability quantum based on income and CPF position

The HFE takes up to 21 working days to process. This means applicants who plan to bid in mid-May must apply for the HFE no later than the third week of April 2026 — right now is the realistic latest window. A late HFE is the single most common reason a motivated applicant misses the exercise window.

We have a full guide to the CPF Housing Grants stack for 2026 that explains how the EHG and Proximity Housing Grant combine with the HFE affordability figure — useful reading while waiting for the HFE result.

Income ceilings and grant quantum in 2026

The family-unit income ceiling for BTO flats remains S$14,000 per month (S$21,000 for extended families in 3Gen flats), unchanged since September 2019. For singles applying for a 2-room flexi flat in non-mature towns under the Single Singapore Citizen Scheme, the ceiling is S$7,000.

Grants available at the point of BTO application in May 2026 include:

Enhanced CPF Housing Grant (EHG) — up to S$80,000 for first-timer families, tiered by average household income.

EHG (Singles) — up to S$40,000 for first-timer singles buying a 2-room flexi.

Proximity Housing Grant (PHG) — applicable on resale only (not BTO), but worth noting that families planning a BTO now may still consider PHG-eligible resale as a backup.

At the top end, an FT (PMC) couple earning S$5,000 combined can receive up to S$80,000 EHG — which, combined with a 75% HDB concessionary loan and the 30-year repayment horizon, brings a four-room Plus flat at approximately S$550,000 valuation well within affordable-range for a dual-income Singaporean household.

Worked example — four-room Plus flat, May 2026

Worked scenario — FT (PMC) couple, combined S$8,500/month

Four-room Plus flat priced at S$620,000 (indicative)

EHG: S$45,000 (tiered on S$8,500 average)

Effective price after grant: S$575,000

Downpayment at 20% (HDB loan): S$115,000, of which up to 20% can be CPF Ordinary Account

HDB loan quantum: S$460,000 at 2.6% concessionary rate

Monthly instalment over 25 years: approximately S$2,090

This scenario assumes baseline HDB concessionary loan terms and does not include any bank-loan alternative; bank-loan applicants face a stricter TDSR ceiling of 55% and typically secure lower rates when the 3M SORA is running below 2.5%.

The seven-day window — what to do in each step

The application window is compressed. Planning each day in advance is what separates applicants who secure a booking from those who miss out:

T-14 days: HDB publishes town list, unit count by flat type, and indicative pricing. Shortlist two or three towns based on location and queue-to-unit ratio.

T-7 days: Application window opens. Submit within the first three days — no advantage to waiting.

T+7 days: Application closes. Ballot results are published approximately three weeks later.

Ballot notification: Selected applicants are invited for an HDB appointment within six weeks. Bring HFE letter, CPF statements, marriage certificate (or letter of intent for engaged couples), and photo ID.

Option fee: S$500 for 2-room flexi; S$1,000 for 3-room; S$2,000 for 4-room and above. Payable at flat selection.

Queue realities — setting a realistic expectation

Across the February 2026 exercise, application rates (applications per unit available) by broad category were approximately:

Four-room Prime — 8.2x oversubscribed

Four-room Plus — 5.6x oversubscribed

Four-room Standard (non-mature) — 1.9x oversubscribed

Three-room Standard (non-mature) — 1.4x oversubscribed

Five-room Standard — 3.1x oversubscribed

What this means: for a Plus or Prime four-room, even a PMC-priority applicant should expect multiple ballot attempts across launches before drawing a good queue number. For a Standard non-mature four-room, many first-time applicants secure a flat on their first or second attempt.

The resale alternative — when to switch tracks

For applicants facing short timelines — a planned wedding inside two years, a growing family, a parent needing close-proximity care — the BTO four-to-five-year wait from ballot to keys can be decisive. HDB resale offers an immediate-occupancy alternative, with the Proximity Housing Grant (PHG) of up to S$30,000 applicable for first-timer families buying near parents.

Resale volumes in Q1 2026 were stable, and median four-room resale prices across non-mature towns settled at approximately S$620,000 — roughly on par with a four-room Plus BTO selection price. That said, BTO remains the subsidised-entry path and is usually worth one or two rounds of attempt before switching.

Sale of Balance Flats — the May parallel track

Alongside the May BTO exercise, HDB will also conduct a Sale of Balance Flats (SBF) round covering unsold units from prior launches plus repurchased flats. SBF pricing is close to BTO pricing but waiting time is significantly shorter (often six to eighteen months to keys). Any applicant applying for BTO May 2026 should also apply for SBF simultaneously — there is no additional application cost and a separate ballot is run.

Market context — BTO versus the private market in 2026

Against the backdrop of Q1 2026’s private PPI flash estimate showing decelerating-but-firm growth, the BTO market is in a different rhythm. HDB Resale Price Index growth has slowed to sub-3% annualised through 2025, and the BTO subsidy profile ensures first-timer families still have a meaningfully cheaper path to homeownership than the private resale or new-launch private market.

The Plus and Prime classification is best thought of as HDB’s tool for capturing the value of public-land subsidy when the underlying land is in high-demand locations — the 10-year MOP and subsidy clawback are the price of access to the choicest catchments. For buyers with a longer-term horizon (10+ years to MOP and beyond), Plus and Prime remain attractive; for buyers who may need geographic flexibility within a decade, Standard flats offer cleaner resale mechanics.

FAQ — May 2026 BTO

Q1. When exactly will HDB open the May 2026 BTO launch? HDB has not announced the exact date at time of writing (22 April 2026). Based on the Feb / May / Aug / Nov cadence, the application window is expected mid-May. Monitor HDB press releases at hdb.gov.sg for the confirmed date.

Q2. Do I need an HFE letter before applying? Yes. The HFE is mandatory for all BTO applicants since the May 2023 exercise. It takes up to 21 working days — apply now if you plan to submit for May.

Q3. Can I apply for BTO and SBF at the same time? Yes, HDB typically runs the two exercises in parallel. Applying for both increases your chance of securing a flat within the same quarter.

Q4. What happens if I miss the application window? You wait for the August 2026 exercise. There is no mid-cycle application option outside the four annual launches.

Q5. My partner and I earn S$15,000 combined — can we still apply? No, the family income ceiling for a standard BTO flat is S$14,000. You may consider the Executive Condominium track (ceiling S$16,000) or resale-private routes.

Q6. What is the key difference between a Plus and a Prime flat? Both carry 10-year MOP and subsidy clawback on resale, and both impose an income ceiling on future resale buyers. Prime flats additionally prohibit renting out the whole flat; Plus flats allow whole-flat rental after MOP. Prime flats are also in the most central catchments.

Q7. Can a single Singaporean apply for a 4-room BTO? No. Singles under the Single Singapore Citizen Scheme are restricted to 2-room flexi flats in non-mature towns. For other room types, singles must apply jointly with an eligible occupier (e.g., parent or sibling) under a joint scheme.

Q8. If my ballot number is not called, do I keep a priority position for the next exercise? No — each exercise is an independent ballot. However, accumulating non-selection histories does boost the applicant’s queue position in certain priority schemes (e.g., the Married Child Priority Scheme retains its weighting across exercises).

Q9. Is there any advantage to submitting on day one versus day seven? No. The ballot is computer-randomised; submission time within the window has no effect on queue position.

Q10. When do I start paying for the flat? The option fee is paid at flat selection. Downpayment is payable in stages aligned to construction milestones (typically 15% at signing of Agreement for Lease, 5% at key collection for HDB loan). Monthly instalments begin only after key collection.

The May 2026 BTO exercise is an exercise in preparation: HFE letter in hand, town shortlist validated against queue-to-unit ratios, First-Timer priority correctly filed. Families applying as FT (PMC) for a Standard non-mature flat have realistic one-to-two-attempt odds; those targeting Plus or Prime in a choicer catchment should plan for several exercises of patience. The framework has changed since 2024 — re-read the rules even if you applied under the old mature/non-mature system.

Fresh Start Housing Scheme gives second-timer families with at least one child (aged 16 or below) who are living in rental or transitional housing a pathway to buy a 2-room Flexi short-lease BTO flat with up to S$75,000 of Fresh Start Grant. The scheme comes with a 20-year Minimum Occupation Period and mandatory financial counselling.

Fresh Start is Singapore’s second-chance scheme: a narrow but meaningful door back into HDB ownership for families who have already owned a flat, fallen out of ownership, and are raising children in rental housing. It is small in numbers — HDB allocates only a few hundred flats to it each year — but it is consequential for the families who qualify.

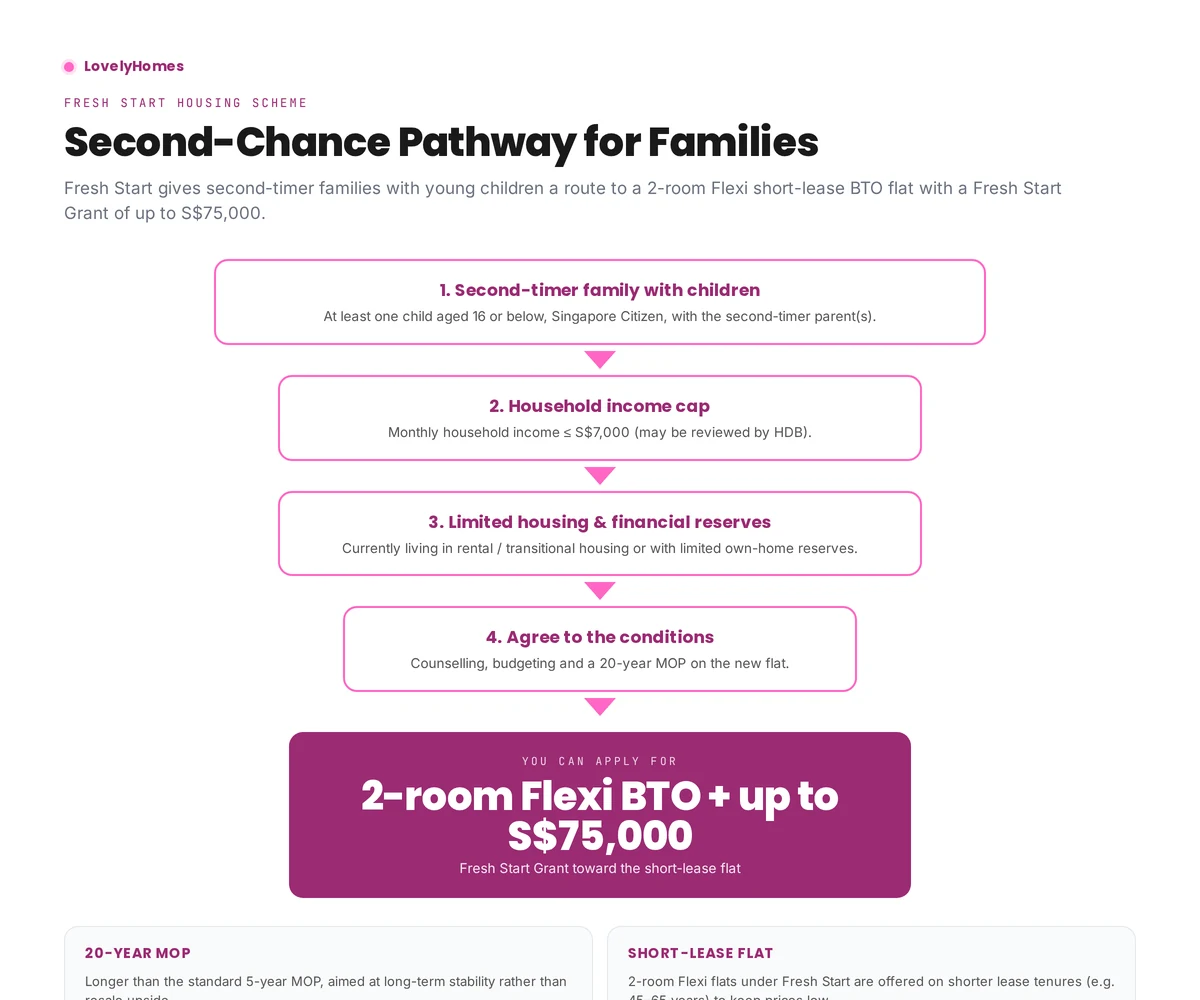

The four eligibility gates and the 2-room Flexi + S$75,000 Fresh Start Grant outcome.

Who Fresh Start is designed for

The scheme is aimed at low-income, second-timer families with young children who are currently in public rental flats or transitional housing under HDB’s schemes like the Interim Rental Housing Programme. HDB’s intention is to help the family stabilise rather than to offer a general upgrade path, so the scheme comes with heavier conditions than standard BTO.

The four eligibility gates

Second-timer family with children. At least one SC child aged 16 or below, living with the applicant family nucleus. Both parents — or a single-parent applicant — must have previously owned a flat.

Household income cap. Monthly household income is typically ≤ S$7,000 (HDB reviews this on a case-by-case basis).

Limited housing & financial reserves. The family is currently in public rental, transitional housing, or otherwise living with very limited financial and housing reserves.

Agree to the conditions. Mandatory counselling, a budgeting programme, and a 20-year MOP on the new flat.

The Fresh Start Grant

The grant is up to S$75,000, disbursed in stages rather than all at once. The structure HDB has published:

Disbursement stage

Amount

On key collection

S$25,000

Over the following years (as the family remains in the flat)

Up to S$50,000

Total

Up to S$75,000

The phased structure is intentional: it nudges families to stay in the flat long enough to stabilise, rather than viewing Fresh Start as a quick cash-out.

What you actually buy

Fresh Start families buy a 2-room Flexi flat on a short-lease tenure (often 45 to 65 years, depending on the applicant’s age and the precinct). Short leases keep prices affordable, but they also mean that the flat does not carry the same long-term resale upside as a standard 99-year flat.

The 20-year MOP trade-off

The 20-year Minimum Occupation Period is the biggest non-monetary cost. You cannot sell the flat on the open market or rent out the whole flat for 20 years. That is four times the standard MOP and is a clear signal that the scheme is designed for long-term stability, not trading.

Breaking the MOP without HDB’s approval has serious consequences, including the possibility of HDB repossessing the flat. HDB does allow sale back to HDB in genuine hardship cases, with grant clawback.

How to apply

Applications run through HDB’s Housing & Development Office (HDO) rather than the usual BTO portal. The process is more involved than a regular BTO application:

Approach HDB via your rental flat officer or a Family Service Centre.

Counselling & budgeting assessment over several sessions — non-negotiable.

Flat offer once HDB confirms eligibility and matches you to an available 2-room Flexi unit.

Financial plan signed off — HDB makes sure the family can afford the mortgage plus utilities.

Key collection with the first S$25,000 disbursed into CPF.

Frequently asked questions

Can Fresh Start applicants apply for other HDB grants?

The Fresh Start Grant is designed as the main support for this scheme. Stacking with other grants (like EHG) is generally not available — HDB consolidates the support into the Fresh Start Grant.

What happens if circumstances improve after I move in?

The phased disbursements continue as long as you remain in the flat and comply with the scheme conditions. Rising income does not trigger clawback.

Is the 20-year MOP negotiable?

No. It is a scheme condition, not a default. HDB considers early sale only in genuine hardship cases.

Can single parents qualify?

Yes. A single-parent household with a SC child qualifies subject to the same income and reserves tests.

This guide is for general information only and is accurate as of April 2026. CPF grants, scheme quantum and eligibility rules are set by HDB / the Ministry of National Development and can change. Always confirm current rules on the HDB Flat Portal or with an HDB officer before committing. We are not a financial or legal advisor.

The Proximity Housing Grant pays S$30,000 to a first-timer or second-timer household that buys a resale HDB flat within 4km (straight-line) of parents or a married child. Families that buy to live together receive a S$20,000 variant. Singles aged 35+ get S$20,000 for a resale flat within 4km of their parents.

PHG is the only CPF housing grant that rewards location choice rather than income. In practice, it reshapes a lot of purchase decisions: a S$30,000 grant is worth one to two months of mortgage payments on a median 4-room resale flat, and it tilts many couples toward estates their parents live in.

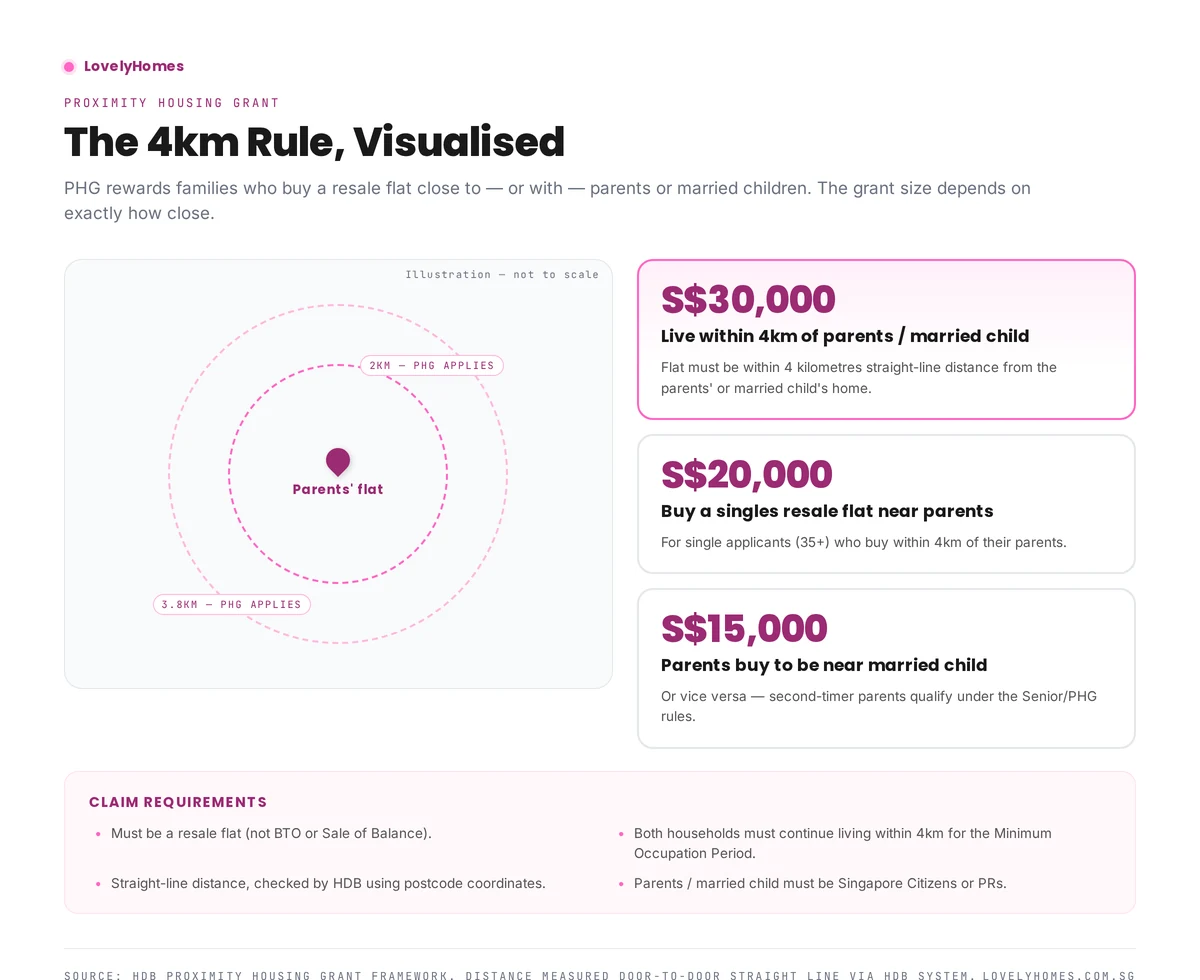

The three PHG variants and the 4km rule visualised (illustration, not to scale).

What PHG is (and isn’t)

PHG is a resale-only grant. It does not apply to BTO purchases, because HDB already allocates BTO flats through balloting and schemes like the Multi-Generation Priority Scheme. It applies to both first-timers and second-timers, which is unusual — most grants close once you have had one.

Three variants exist:

Variant

Quantum

Who

Live near parents / married child

S$30,000

Couples / families buying within 4km

Live with parents / married child

S$15,000 (top-up)

Joint purchase / same flat

Singles (35+) near parents

S$20,000

Singles-scheme resale buyers within 4km

How the 4km rule actually works

HDB measures straight-line distance between the postal centroids of your new flat and your parents’ (or married child’s) address. It does not care about walking distance, MRT travel time, or which town you’re in. A flat across a canal in a different town may still be within 4km; a flat in the same estate might fall just outside.

You can check the distance on the HDB portal before you commit to an OTP. Sellers often advertise whether a resale flat qualifies; verify it yourself before exercising, because getting the distance wrong means S$30,000 left on the table.

Who counts as parents / child

PHG is more generous about family definitions than many buyers assume. For a married couple, “parents” includes the biological or adoptive parents of either spouse — so living near your in-laws also qualifies. “Married child” means a Singapore Citizen or PR child who has formed a family nucleus of their own.

Step-parents generally do not qualify unless you were legally adopted. The parent(s) must be SC or SPR and must live in Singapore on a regular basis — HDB checks this against their NRIC-registered address.

The post-purchase obligation

PHG carries a follow-through obligation: both households must continue to live within the 4km threshold through your standard 5-year Minimum Occupation Period. If your parents sell up and move further away before MOP ends, you will normally keep the grant — the rule is tested at application time, not continuously — but HDB has clawed back grants in a small number of cases where the relocation happened unusually close to purchase.

A few buyers try to “pass the test” with an in-law’s short-term rental address. HDB has flagged this as a concern and routinely asks for evidence of genuine, stable parental residence.

Worked example

Field

Value

Buyers

Married SC couple, first-timers

Flat

4-room resale in Clementi at S$680,000

Parents’ flat

3-room HDB in Queenstown, 2.6km straight-line

PHG

S$30,000

Family Grant

S$50,000

EHG (income S$8,500)

S$5,000

Total grants

S$85,000

How PHG shapes negotiation

A PHG-qualifying flat is slightly more attractive than an identical flat that falls outside the 4km radius, which means well-informed buyers sometimes bid a touch more for it. Savvy sellers mention “within 4km of XYZ parents’ flat” in the listing because it widens the qualifying buyer pool.

Frequently asked questions

Does PHG apply to EC purchases?

No. Executive Condominiums do not qualify for PHG. It is HDB-resale only.

What if my parents move after I buy?

You are not normally required to refund the grant. However, the Minimum Occupation Period rules around residence still apply to you as the flat owner.

Can I use PHG with my in-laws?

Yes, if they are the legal parents of your spouse. Step-parents usually do not qualify.

Is PHG paid in cash?

No. Like other CPF housing grants, PHG is disbursed via your CPF Ordinary Account against the flat price.

This guide is for general information only and is accurate as of April 2026. CPF grants, scheme quantum and eligibility rules are set by HDB / the Ministry of National Development and can change. Always confirm current rules on the HDB Flat Portal or with an HDB officer before committing. We are not a financial or legal advisor.

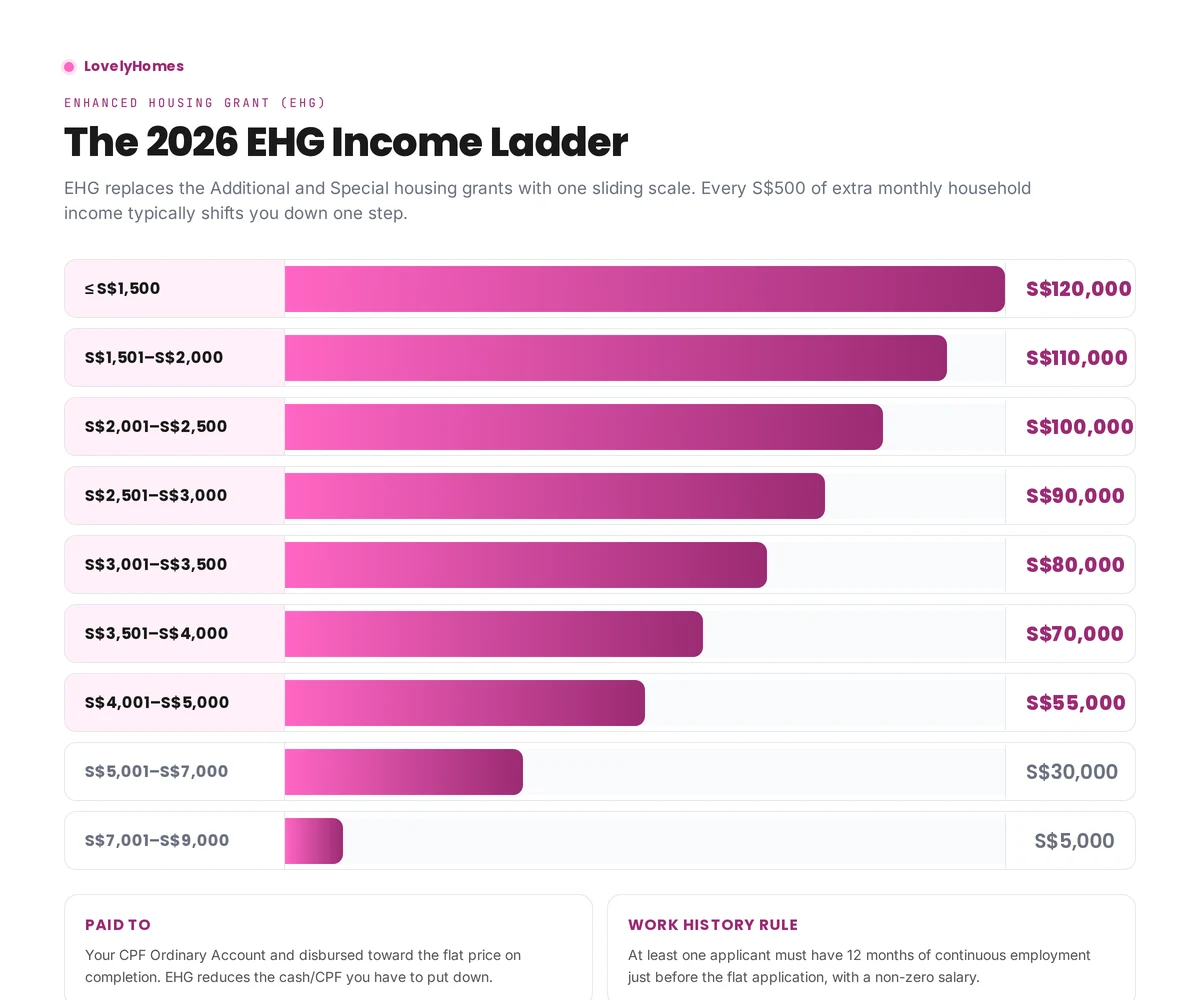

Enhanced CPF Housing Grant (EHG) pays up to S$120,000 to first-timer Singaporean buyers of a BTO or resale flat. Quantum steps down by S$10,000–S$15,000 for every S$500 increase in gross monthly household income, reaching S$5,000 at the top of the S$9,000 eligibility ceiling. At least one applicant must have worked continuously for 12 months before the flat application.

EHG is the grant that does most of the heavy lifting in any first-timer CPF housing grant package. It is also the most frequently miscalculated, because the income ladder and the employment rule together decide a number that can swing by S$90,000.

EHG steps down roughly every S$500 of extra monthly household income.

What EHG replaced

Before September 2019, first-timers navigated a confusing mix of Additional CPF Housing Grant and Special CPF Housing Grant, with different rules for BTO vs resale and for flat size. EHG rolled them into a single sliding ladder that applies equally to BTO and resale flats. The headline change: the income ceiling rose to S$9,000 (from S$5,000–S$8,500 depending on scheme), so many middle-income households now qualify for at least a modest grant.

The 2026 quantum ladder

Gross monthly household income

EHG quantum

≤ S$1,500

S$120,000

S$1,501 – S$2,000

S$110,000

S$2,001 – S$2,500

S$100,000

S$2,501 – S$3,000

S$90,000

S$3,001 – S$3,500

S$80,000

S$3,501 – S$4,000

S$70,000

S$4,001 – S$5,000

S$55,000

S$5,001 – S$7,000

S$30,000

S$7,001 – S$9,000

S$5,000

> S$9,000

Not eligible

Singles aged 35 and above get roughly half the quantum under the Singles EHG variant, with an equivalent income ceiling of S$4,500.

Eligibility beyond income

Three gates matter beyond income:

First-timer status. You (and your spouse, for couple applications) must never have received a housing subsidy, BTO flat, DBSS flat, EC direct from developer, or CPF housing grant.

Singapore Citizen. At least one applicant must be an SC. For couple applications, the spouse can be an SC or SPR.

Continuous work. At least one applicant must have worked continuously for the 12 months immediately before the flat application, with a non-zero salary. Short gaps (e.g. a fortnight between jobs) are usually tolerated; extended career breaks usually disqualify.

How EHG is paid out

EHG is not cash. It is credited into your CPF Ordinary Account and immediately disbursed toward the flat price on completion. The practical effect is that your CPF OA deduction and the amount you have to put down in cash / loan fall by the grant amount.

Because the grant lands in CPF OA first, it is treated like a CPF withdrawal for accrued-interest purposes. When you sell the flat, you refund the grant amount plus CPF accrued interest to CPF OA — not back to HDB.

EHG on BTO vs resale

Aspect

BTO

Resale

Quantum

Same ladder

Same ladder

Payment timing

On key collection

On legal completion

Effect on income eligibility

Checked at balloting

Checked at HFE + resale application

Stackable with Family Grant

N/A (Family is resale only)

Yes

Stackable with PHG

N/A

Yes

Worked example

Daniel and Priya earn a combined S$5,500 per month. They plan to buy a 4-room BTO flat in Tengah. EHG drops them into the S$5,001–S$7,000 band: S$30,000. That grant reduces their CPF OA deduction on key collection; their cash-over-CPF contribution stays the same, but their ongoing mortgage is based on a smaller principal.

Two years later, their incomes rise to a combined S$7,200 — no clawback applies, because EHG eligibility is assessed at application time only. If they had applied after the pay rise, they would have fallen into the S$7,001–S$9,000 band and received only S$5,000 — a S$25,000 swing driven purely by timing.

Common mistakes

The biggest mistake is mis-reporting income. HDB verifies income against CPF contribution records and NOA, so overstating (to qualify for a bigger loan) or understating (to qualify for a bigger grant) is caught quickly. The second biggest mistake is underestimating the 12-month employment rule — freelancers and variable-income workers should keep careful CPF contribution records.

Frequently asked questions

Can I get EHG if my spouse does not work?

Yes, as long as the working spouse meets the 12-month continuous employment rule and the household income is within the ceiling.

Is EHG taxable?

No. CPF housing grants are not taxable income.

What counts as “income” for EHG?

Gross monthly household income — salary, allowances, bonuses pro-rated across the year, and variable commissions. Excludes CPF contributions and reimbursements. HDB uses a rolling 12-month average where relevant.

Can EHG be used with the HDB Concessionary Loan?

Yes. EHG simply reduces the purchase price you need to finance — it works with both HDB Concessionary Loans and bank loans.

This guide is for general information only and is accurate as of April 2026. CPF grants, scheme quantum and eligibility rules are set by HDB / the Ministry of National Development and can change. Always confirm current rules on the HDB Flat Portal or with an HDB officer before committing. We are not a financial or legal advisor.