HDB Key Collection Singapore 2026: Complete Guide to Defects Inspection, DLP and What to Do After Getting Your Keys

Quick Answer: HDB Key Collection Singapore 2026 — Key Takeaways

- Key collection is the final step in both the BTO and resale HDB purchase process — once keys are collected, the 5-year Minimum Occupation Period (MOP) clock starts immediately.

- Before key collection, HDB invites you to a pre-completion inspection to identify and log defects in the flat.

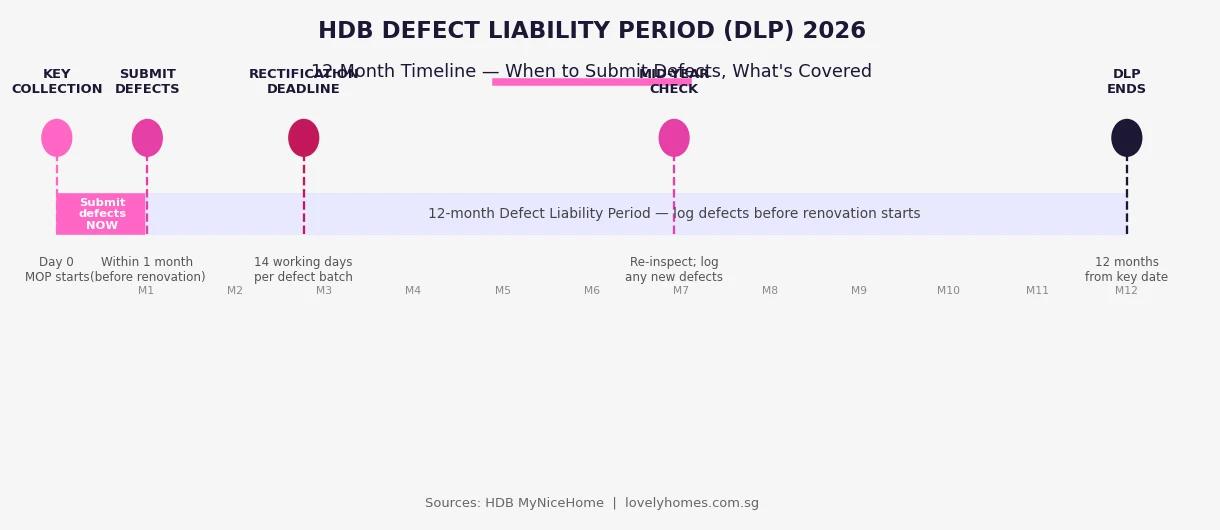

- Submit all defects within one month of key collection and before renovation begins — defects reported after renovation starts are much harder to attribute to the original construction.

- The Defect Liability Period (DLP) is 12 months from the date of key collection — HDB’s main contractor is responsible for rectifying valid defects at no cost to you during this period.

- Use the MyHDB Portal app (or visit your Building Service Centre) to submit defects electronically with photos — do this room by room within the first week.

- Bring to key collection: NRIC for all owners, cashier’s orders for outstanding payments, HDB loan letter or bank acceptance, and CPF withdrawal authorisation if applicable.

- Resale flat key collection follows a different process from BTO — completion happens at HDB Hub, and MOP is calculated from the date on the resale completion letter, not the original TOP date.

What Is HDB Key Collection and Why Does It Matter?

Key collection is the final milestone in the HDB flat purchase journey — the moment when legal ownership is formally transferred and the physical keys to your new home change hands. For a BTO (Build-to-Order) flat, this follows three to five years of waiting from the ballot exercise, triggered when the flat achieves its Temporary Occupation Permit (TOP) and HDB issues individual collection invitations. For a resale flat, key collection happens at the HDB-facilitated completion appointment, typically six to eight weeks after the Option to Purchase is exercised and HDB grants approval.

Beyond the emotional significance of receiving your keys, the date of key collection carries substantial legal and financial consequences. The five-year Minimum Occupation Period — the rule preventing most HDB owners from selling before they have physically occupied the flat — begins on the key collection date. The 12-month Defect Liability Period, during which HDB’s contractor must rectify construction defects at no charge, also starts on this date. Miss the one-month window for defect submission and you significantly weaken your ability to claim rectification from HDB.

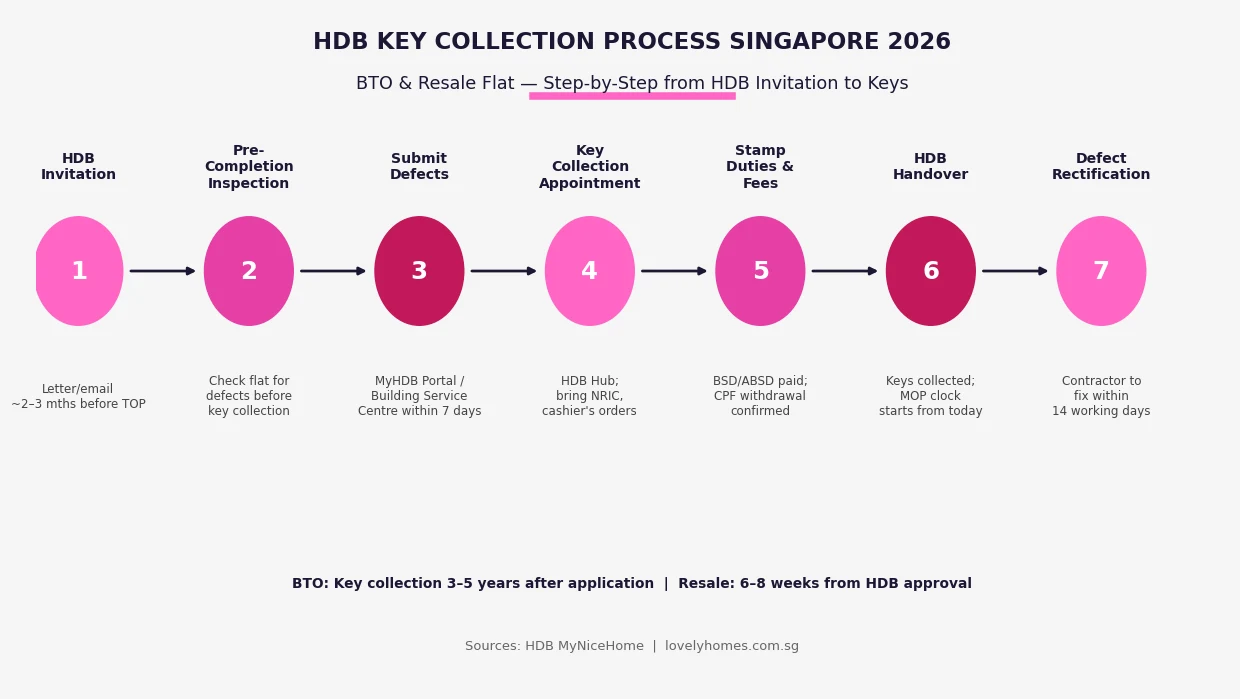

BTO Key Collection: Step-by-Step Process 2026

HDB sends a written invitation by post and through the MyHDB portal approximately two to three months before your flat’s key collection date. The invitation includes a date and time slot for the pre-completion inspection, and separately for the formal key collection appointment itself.

Step 1: Pre-Completion Inspection

Before keys are collected, HDB offers a pre-completion inspection of your flat. This is your first opportunity to walk through the unit with HDB’s building inspector and identify construction defects. Defects identified at this stage are formally logged and HDB’s main contractor is required to rectify them before or shortly after key collection. Do not skip this inspection — defects that are not formally logged during this appointment are more difficult to claim under the DLP later.

Bring a torch, a marble (for tile-tapping), a portable socket tester, a spirit level, and your phone for photography. Walk every room systematically. The inspection is free and takes approximately 45 minutes to one hour for a 4-room flat.

Step 2: Key Collection Appointment

The key collection appointment takes place at HDB Hub, Toa Payoh. You must attend in person (all registered owners must be present or represented by a Power of Attorney). Bring the following documents and payments:

- NRIC of all flat owners (originals required)

- Cashier’s order(s) for any outstanding payments (stamp duties, mortgage shortfall, admin fees)

- HDB loan letter acceptance, or bank’s letter of offer and mortgage documents

- CPF withdrawal authorisation forms, if CPF Ordinary Account funds are being used

- Resale levy cashier’s order, if applicable (second-timer buyers)

At the appointment, HDB processes the stamp duties, confirms the CPF and cash components, and registers the transfer with the Singapore Land Authority (SLA). The SLA registration typically completes within a few working days, after which you are the registered owner in the land register. The keys are handed over upon completion of the administrative process — typically within the same appointment.

Step 3: Submit Defects Immediately

Immediately after collecting your keys, conduct a second, more thorough inspection at your own pace. Use the MyHDB Portal (web or mobile app) to submit defects with photographs. The submission system allows you to tag defects by room and type. HDB’s standard rectification target is 14 working days per defect batch, though complex defects such as waterproofing issues or structural cracks may take longer. Submit everything within the first week; all defects must be submitted within one month of key collection and before any renovation work begins.

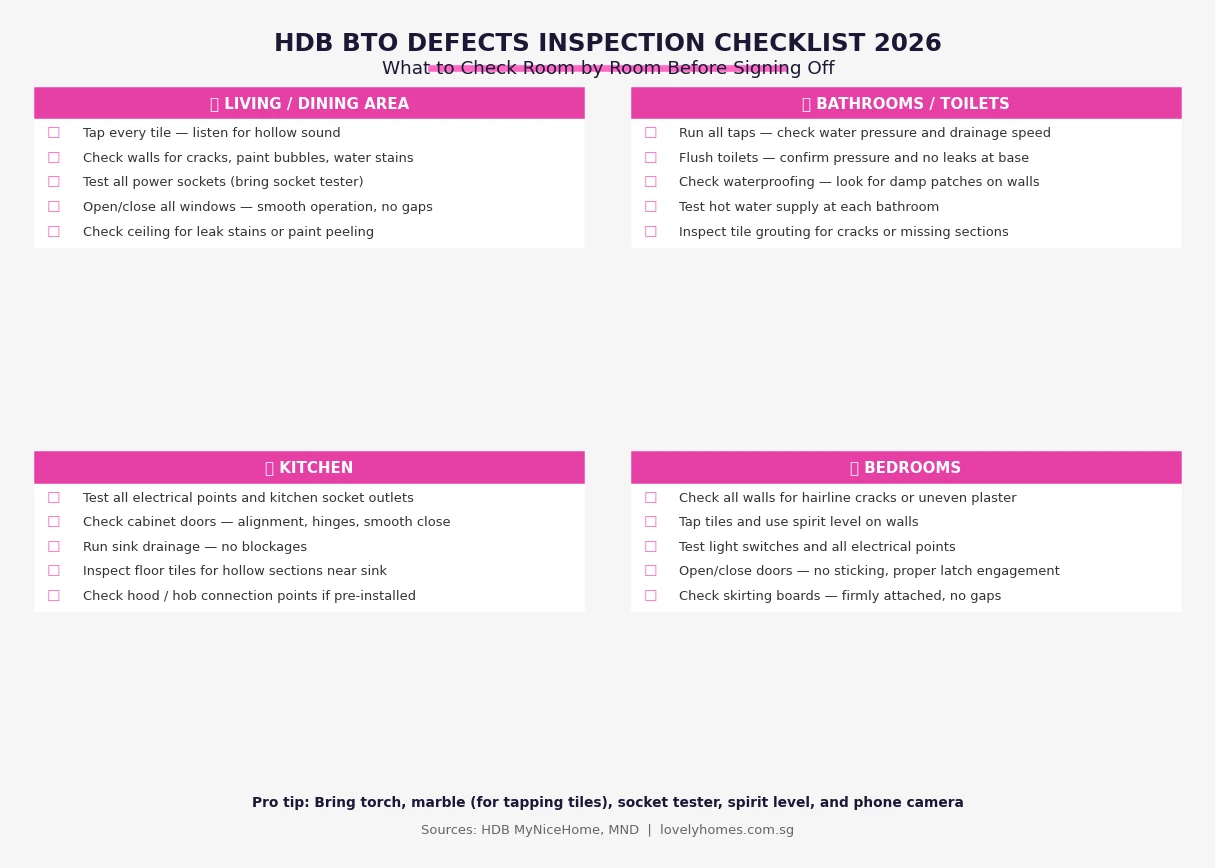

The Defects Inspection: What to Check Room by Room

A systematic inspection takes 60–90 minutes for a standard 4-room BTO flat. Work through each room methodically before moving to the next. Bring the following equipment: a torchlight (for dark corners and under cabinets); a marble or coin (for tile-tapping); a portable socket tester; a spirit level (for walls and floors); masking tape and a marker pen (to tag defects in situ); and your phone camera (photo evidence is essential for defect submissions).

Living Room and Dining Area

Tap every tile across the full floor area using a marble — a hollow or dull sound indicates poor bonding, which can cause tiles to crack or lift over time. Walk the entire floor and mark each hollow tile location with masking tape. Inspect all walls for hairline cracks, uneven plaster, paint bubbles, or water stains (especially around skirting boards). Test every power socket with a socket tester. Open and close all windows — they should slide or pivot smoothly with no significant gaps or draught ingress. Check the ceiling for water stains, paint peeling or cracks.

Bathrooms and Toilets

Run every tap and showerhead — check water pressure, drainage speed (should clear the basin within 10 seconds) and confirm no drips from joints. Flush all toilet cisterns — strong, clean flush with no leak at the base seal. Look for water stains or damp patches on walls adjacent to the shower zone, which may indicate waterproofing voids. Test the hot water supply at every bathroom. Inspect tile grouting for cracks, missing sections or staining around floor drains. Check that the bathroom door opens and closes properly and that the privacy lock engages fully.

Kitchen

Test all electrical points and the kitchen circuit — bring a socket tester and check the hood/hob electrical connection points if pre-fitted. Inspect cabinet doors for alignment, smooth hinges and proper magnetic or soft-close engagement. Run the kitchen sink to confirm drainage; check beneath the sink cabinet for moisture or drips. Tap floor tiles near the sink area for hollow sections. Confirm the gas pipe stub-out is present and capped if you are planning a gas hob installation.

Bedrooms

Check all walls for hairline cracks, especially at corners and around window frames. Use your spirit level on at least one wall per bedroom — significant lean may affect built-in carpentry. Test all light switches and power points. Open and close every bedroom door — it should close flush without sticking and the latch should engage cleanly. Check skirting boards for gaps or poor adhesion. Inspect ceiling corners and the top of walls for water staining, which may indicate condensation or waterproofing issues from the flat above.

| Area | Key Defects to Inspect | Tool to Bring |

|---|---|---|

| Floor tiles (all rooms) | Hollow sound, cracks, misalignment, lippage | Marble or coin |

| Walls (all rooms) | Hairline cracks, uneven plaster, paint bubbles, water stains | Torch, phone camera |

| Power sockets | Dead outlets, loose fittings, missing earth pin | Socket tester |

| Windows and doors | Stiff operation, gaps, misalignment, failed locks | Hands only |

| Ceiling | Water stains, paint peeling, cracks near corners | Torch |

| Bathroom walls and floors | Damp patches, grouting gaps, hollow tiles near drains | Marble, torch |

| Sanitary fittings | Drips from joints, slow drainage, weak flush | Running water |

| Kitchen cabinet doors | Misalignment, stiff hinges, failed soft-close | Hands only |

Resale HDB Key Collection: How It Differs from BTO

For resale flat buyers, the process is compressed into a single completion appointment at HDB Hub, typically held six to eight weeks after HDB approves the resale application. Both the buyer and seller (or their solicitors under the conveyancing process) attend. At the completion appointment: outstanding payments are exchanged; HDB processes the stamp duties and CPF withdrawals; SLA registers the ownership transfer; and the seller hands over the keys. There is no pre-completion inspection equivalent for resale flats — the buyer is expected to have inspected the flat thoroughly during the option exercise period.

A critical difference for resale buyers is that the Defect Liability Period does not apply — that protection only extends to new HDB flats during the original construction period. Resale buyers should instead conduct a thorough pre-purchase inspection, ideally with a professional building inspector, and negotiate any defects or renovation-required conditions into the purchase price or as a condition of the Option to Purchase.

The Defect Liability Period (DLP): Your Rights in the 12 Months After Key Collection

The Defect Liability Period is a 12-month statutory protection period commencing on the date of key collection. During this period, HDB’s appointed main contractor is contractually obligated to rectify valid construction defects — cracks, waterproofing failures, defective tiles, faulty electrical installations — at no cost to the flat owner. This is a significant consumer protection, particularly given that BTO flat construction typically takes three to five years and construction quality can vary.

How to Submit Defects Under the DLP

The recommended submission method is the MyHDB Portal (via browser at my.hdb.gov.sg or the MyHDB app). Submit photos with each defect, tag the location within the unit, and describe the issue specifically (for example: “living room floor tile at coordinates 2m from entrance door, 1m from left wall — hollow when tapped, produces dull sound across approximately 30×30cm area”). A specific, photo-supported submission is significantly harder to reject than a vague one. Alternatively, visit your Building Service Centre (BSC) and submit a physical Defects Feedback Form.

HDB targets 14 working days for contractors to complete each batch of rectification. For complex defects — waterproofing voids, structural cracks, systemic electrical issues — the timeline may extend. Follow up in writing via the portal if the 14-day window passes without completion.

Submit Before Renovation Begins

This is the most important practical rule of the DLP: submit all defects before your renovation contractor begins work. Once hacking, tiling and carpentry are underway, any pre-existing defect becomes extremely difficult to attribute to the original construction versus the renovation contractor. HDB may decline to rectify a defect that appears after renovation has commenced, even if the underlying cause was a construction fault. Log everything in the first week after key collection, before any furniture is moved in and certainly before a single tile is replaced.

Summary: BTO vs Resale Key Collection at a Glance

| Aspect | BTO Flat | Resale HDB Flat |

|---|---|---|

| Timeline to key collection | 3–5 years from ballot exercise | 6–8 weeks from HDB approval |

| Pre-collection inspection | Yes — HDB-organised pre-completion inspection | No — buyer arranges own inspection |

| Key collection venue | HDB Hub, Toa Payoh | HDB Hub, Toa Payoh |

| Defect Liability Period | 12 months from key collection date | Not applicable |

| Defect submission window | Within 1 month of key collection; before renovation | Not applicable (negotiate pre-purchase) |

| MOP start date | Date of key collection | Date of key collection (completion date) |

| Stamp duties payable | BSD at completion; no ABSD for eligible first-time buyers | BSD and ABSD (if applicable) at completion |

| Keys from whom | HDB (direct from developer) | Seller (via completion appointment) |

Worked Example: BTO Key Collection for a First-Timer Couple, Tengah 2026

Case Study: Mr Rahman (Singapore Citizen) and Ms Tan (Singapore Citizen) — 4-Room BTO, Tengah Garden Walk, TOP March 2026

Background: First-timer SC couple. Applied in October 2022 ballot. Estimated key collection: Q1 2026. HDB invitation received 10 January 2026.

Pre-completion inspection: 15 January 2026. Defects logged: 3 hollow tiles (living room), 1 hairline crack (bedroom 2 wall, corner), 2 stuck window hinges (bedroom 1 and study), slow drainage (master bathroom). All logged on HDB Defects Inspection Form on the day.

Key collection appointment: 28 January 2026, 10:00am, HDB Hub. Documents brought: NRIC for both owners; cashier’s order S$8,400 (balance stamp duty after CPF); HDB loan letter acceptance; CPF withdrawal authorisation. Time taken: 50 minutes. Keys received 28 January 2026 — MOP starts 28 January 2026, expires 28 January 2031.

Defect submissions: Second inspection conducted 28–29 January 2026. Additional defects found: 4 more hollow tiles (master bedroom), 1 dead power socket (study), grout cracking at master bathroom drain. Submitted via MyHDB Portal on 29 January 2026 (1 day after key collection). Total defects submitted: 11 items.

Rectification: Contractor began rectification 10 February 2026 (9 working days). All 11 items cleared by 21 February 2026.

Renovation commencement: Contractor engaged 1 February 2026; APEX permit issued 14 February 2026; renovation commenced 15 February 2026 — after all DLP defects confirmed submitted. ✓ Compliant.

Financial summary at completion: Purchase price S$510,000. CPF used: S$126,000 (down payment S$51,000 + BSD S$9,600 + legal S$3,400 + balance drawdown S$62,000). Cash: S$8,400. HDB loan: S$382,500 @2.60% pa, 25 years → S$1,728/month. MSR: 24.0% ✓ PASS.

Why Getting Key Collection Right Matters for Your Long-Term Investment

The 12-month DLP is one of the most valuable consumer protections available to a BTO flat buyer — and it is almost entirely wasted if defects are not logged promptly and correctly. HDB’s main contractors typically complete BTO projects at significant scale; individual flat defects, while minor in isolation, accumulate across a project and the contractor has both the obligation and the budget to rectify them during the DLP window. A thorough defect submission in the first week after key collection typically results in clean, contractor-funded rectifications that would otherwise cost S$3,000–S$15,000 to remedy out of pocket after the DLP expires.

Beyond the DLP, getting the MOP start date right matters for investment planning. A common misconception among first-time BTO buyers is that MOP runs from the date of ballot or the TOP date. It runs from key collection date. If you delay key collection — or if administrative issues push the date forward — your MOP and subsequent resale or investment timeline shifts accordingly.

What Might Come Next: HDB Defect Handling and Technology

HDB has been progressively digitalising the defect submission and inspection process. The MyHDB app now supports geo-tagged photo submissions with AI-assisted defect classification — automatically categorising submissions as structural, waterproofing, tiling, electrical or plumbing and routing them to the relevant sub-contractor. HDB’s pilot in selected BTO projects uses smart sensors embedded in wall and floor elements to flag waterproofing failures before they manifest as visible damp patches — potentially allowing proactive rectification before owners even move in. If expanded, this technology could substantially reduce the volume of owner-reported defects at key collection by the time BTO projects launching in 2024–2025 reach TOP around 2028–2030.

Frequently Asked Questions: HDB Key Collection Singapore 2026

What happens if I find defects after the 12-month DLP ends?

Once the 12-month Defect Liability Period expires, HDB’s contractor is no longer obligated to rectify construction defects at no charge. Structural defects — cracks in load-bearing elements, significant waterproofing failures — may still be covered under a longer structural warranty (HDB maintains a 15-year structural defect warranty on the building itself, distinct from the flat-level DLP). For cosmetic and minor defects discovered after the DLP, the cost of rectification falls entirely on the flat owner. This is why thorough and timely defect submission in the first month is so important — it is genuinely your only cost-free window for flat-level defect rectification by the original contractor.

Can I send someone else to collect my HDB keys on my behalf?

All registered flat owners are required to attend the key collection appointment in person, unless you have authorised a representative under a valid Power of Attorney (PA). The PA must be a notarised original, and the representative must bring it along with their own NRIC. HDB does not accept informal authorisation letters or verbal confirmation. If one co-owner genuinely cannot attend due to travel or medical reasons, arrange the PA in advance — the appointment cannot proceed with an absent owner who has not executed a PA.

Do I need to renovate immediately after collecting my BTO keys?

No. There is no obligation to renovate immediately. The BTO renovation permit window is three months from permit issuance — but you do not need to apply for the permit on the day you collect keys. Many flat owners wait several weeks after key collection to engage a contractor, finalise their design, and allow defect rectifications to complete before renovation begins. The practical constraint is that any defects you wish to claim under the DLP must be submitted before renovation work starts, so conduct your full defect inspection and submit to HDB before your renovation contractor commences hacking or tiling.

When does the MOP start for a resale HDB flat?

For a resale flat, the MOP begins on the date stated in the resale completion letter — the date on which the ownership transfer is formally registered by SLA and HDB. This is typically the date of the completion appointment at HDB Hub, at which point the buyer takes physical possession of the keys. The MOP does not start from the original TOP date of the resale flat, nor from the date the OTP was signed. If you are purchasing a resale flat specifically to use or sell after the MOP, count five years from your completion date, not from any earlier milestone in the transaction.

What is the difference between the pre-completion inspection and the defect submission after key collection?

The pre-completion inspection is an HDB-organised walk-through of your flat that takes place before key collection, typically one to four weeks prior. An HDB building inspector accompanies you, and any defects logged at this stage are formally recorded by HDB for contractor rectification. The post-key-collection defect submission is a second, self-conducted inspection that you carry out at your own pace after collecting the keys, submitted through the MyHDB portal or BSC. Both are important: the pre-completion inspection catches obvious construction issues early; the post-key-collection submission documents anything missed on the initial walk-through or discovered during a more thorough personal inspection. Submit all defects within one month and before renovation commences.

What is a Building Service Centre and what can it help me with?

A Building Service Centre (BSC) is an HDB service point located within or near major HDB estates. Each BSC handles the estate-specific management functions for the flats in its area, including defect submissions during the DLP, estate maintenance requests, lift breakdown reports, and minor statutory-regulated matters such as renovation permit endorsements for certain works. You can submit physical Defects Feedback Forms at your BSC as an alternative to the MyHDB portal. To find your BSC, search by your flat’s postal code on the HDB website under “Contact Us → Building Service Centre”.

What stamp duties are payable at BTO key collection?

For a BTO flat, Buyer’s Stamp Duty (BSD) is payable at the key collection appointment. The BSD rates (2026) are: 1% on the first S$180,000; 2% on the next S$180,000; 3% on the next S$640,000; 4% on the next S$500,000; and 5% on the remainder. For example, on a S$510,000 BTO flat: BSD = S$1,800 + S$3,600 + S$9,900 = S$15,300. Additional Buyer’s Stamp Duty (ABSD) does not apply to eligible first-timer Singapore Citizens buying an HDB flat as their first property. CPF Ordinary Account funds can be used to pay both BSD and legal fees at completion.

Related Articles

- HDB BTO Process 2026: Complete Step-by-Step Guide from HFE to Key Collection

- Singapore HDB BTO Eligibility Guide 2026: Who Can Apply, Income Ceilings and Priority Schemes

- Singapore Home Renovation Guide 2026: HDB Permits, APEX System, Condo Rules and Step-by-Step Process

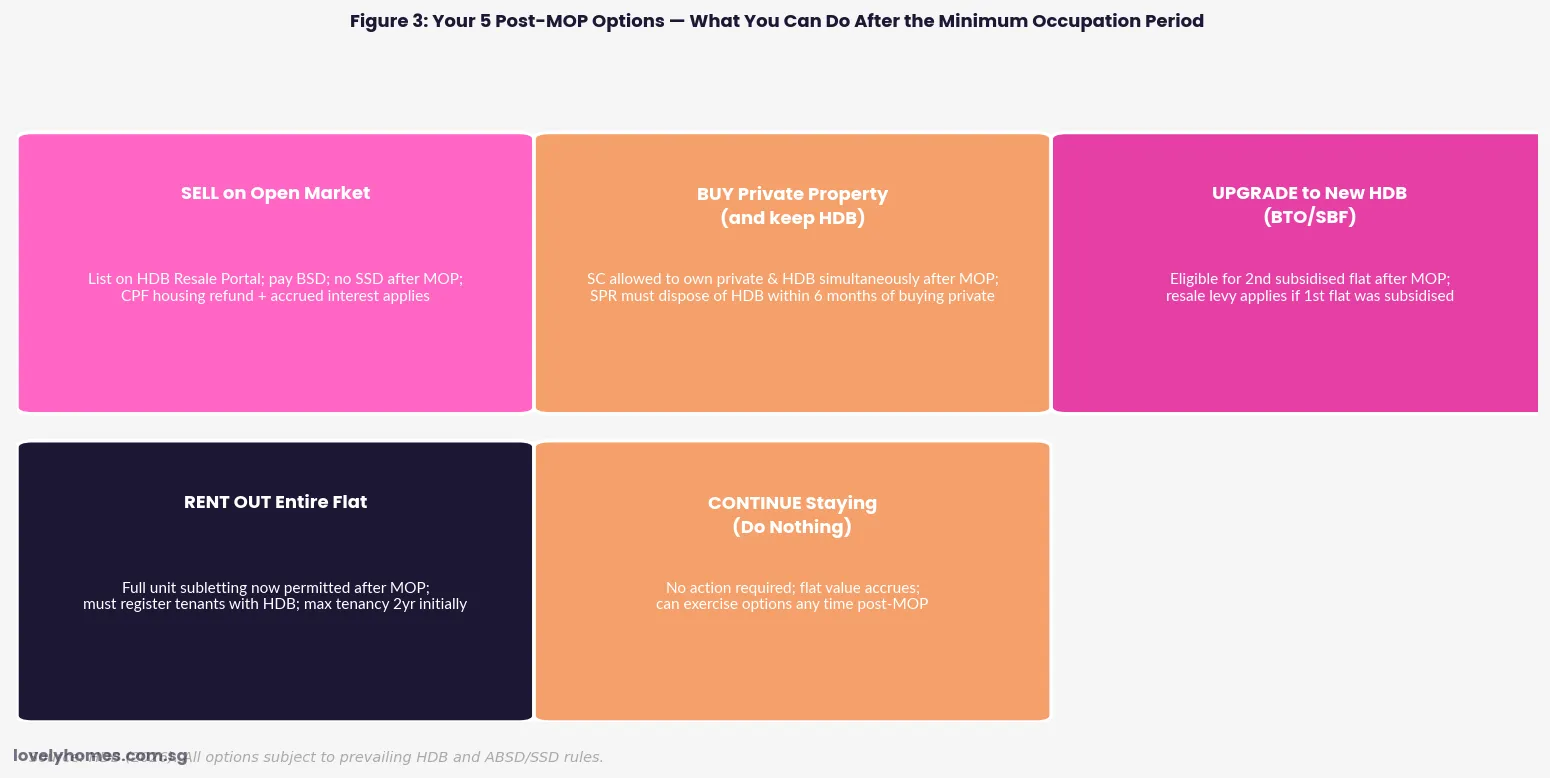

- Singapore Property MOP Guide 2026: HDB Minimum Occupation Period Rules Explained

- Using CPF Ordinary Account for Property in Singapore: Complete Guide 2026

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Renovation Cost Guide 2026: HDB, Condo and Landed Budgets Explained

Disclaimer: This article is for general informational purposes only and does not constitute legal or financial advice. HDB processes, defect liability procedures and stamp duty rates are subject to change. Verify current requirements directly with HDB at www.hdb.gov.sg and IRAS at www.iras.gov.sg. For resale flat transactions and complex conveyancing matters, engage a qualified solicitor.