HDB 2-Room Flexi Flat Singapore 2026: Complete Guide for Singles and Seniors

Quick Answer — HDB 2-Room Flexi Flat at a Glance

- What it is: A compact HDB flat type (approx. 36–45 sqm) with flexible lease options, designed for seniors aged 55 and above or eligible singles aged 35 and above.

- Lease flexibility: Seniors may choose a short lease of 15, 20, 25, 30, 35, 40 or 45 years; singles and couples buy on the standard 99-year lease.

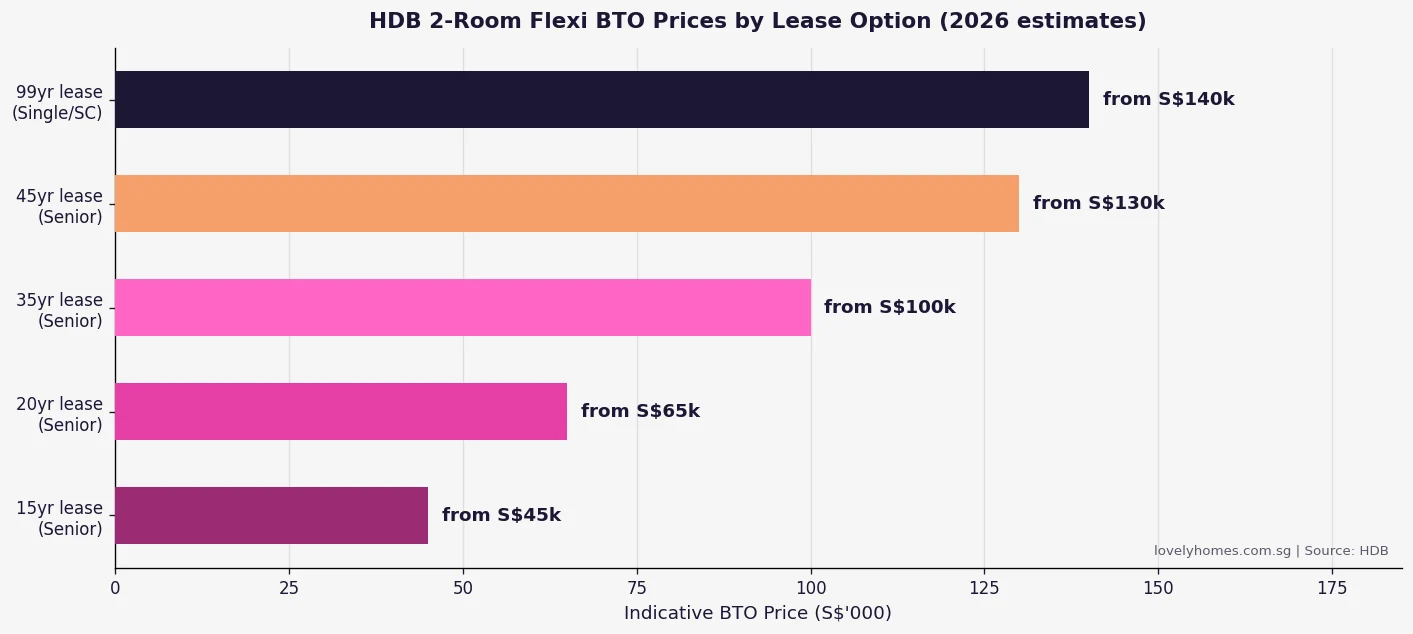

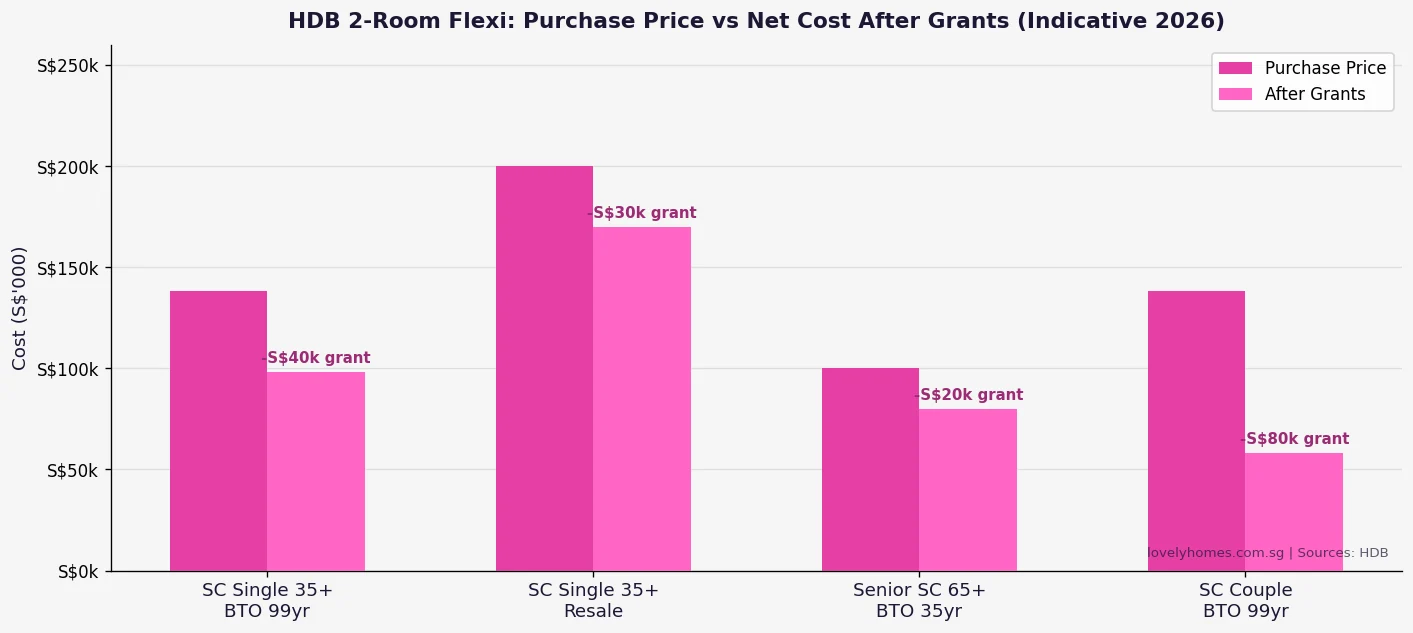

- BTO price range: From approximately S$45,000 (senior, 15-year lease, non-mature estate) to S$140,000 (single, 99-year lease, non-mature estate BTO). Resale 2-room flats are priced by the open market.

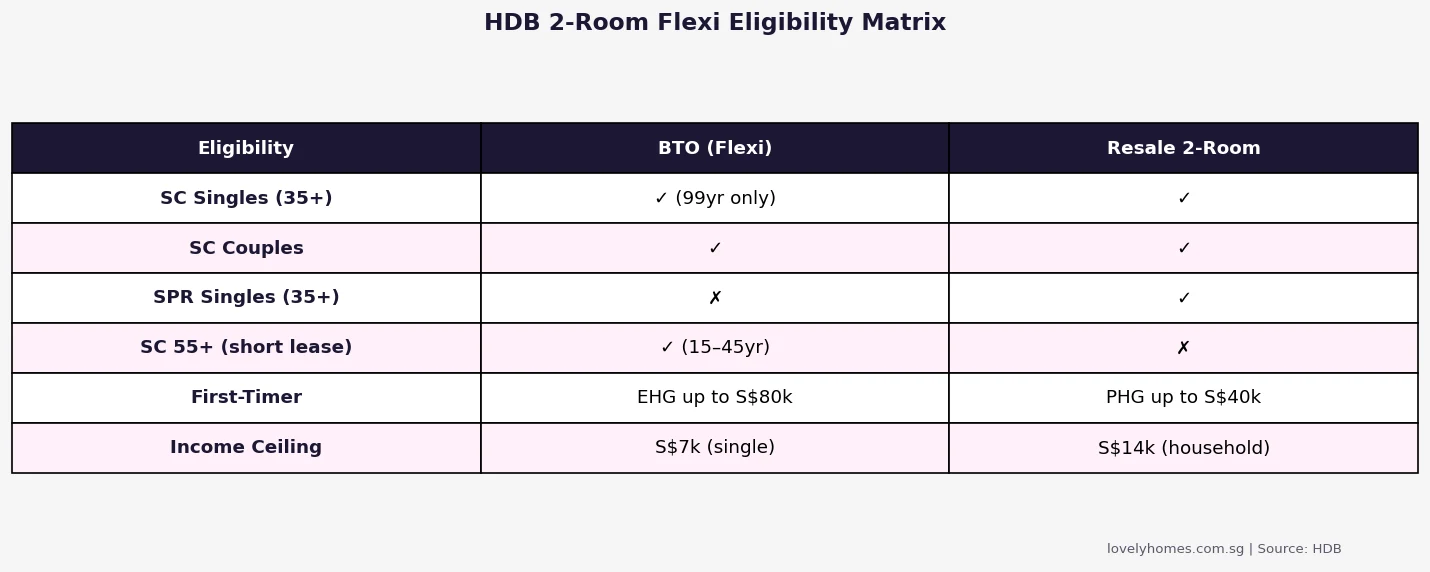

- Who can buy: SC singles (35+), SC/SPR couples where at least one is SC, and SC households aged 55+ (short-lease sub-type).

- Income ceiling: S$7,000/mth for singles; S$14,000/mth for households.

- Grants available: Enhanced Housing Grant (EHG) up to S$80,000 for eligible first-timers; Proximity Housing Grant (PHG) up to S$30,000 for resale buyers near family.

- CPF usage: CPF Ordinary Account savings may be used for downpayment and monthly instalments, subject to CPF withdrawal limits and the flat’s remaining lease covering the youngest buyer to age 95.

- MOP: Standard 5 years for regular 2-room Flexi flats; subletting of the whole flat is not allowed during MOP.

- Resale restriction: Short-lease flats (below 99 years) may only be sold back to HDB — they are not on the open resale market.

- Key regulator: All 2-Room Flexi applications are managed by the Housing & Development Board (HDB) at hdb.gov.sg.

What Is the HDB 2-Room Flexi Flat?

The HDB 2-Room Flexi flat is a purpose-designed public housing type introduced in 2015 to replace the earlier 2-room flat. Measuring between 36 and 45 square metres, it is the smallest flat type offered in Singapore’s public housing system. The “Flexi” in its name refers to the scheme’s most distinctive feature: eligible buyers aged 55 and above may opt for a short, right-sized lease rather than committing to the standard 99-year term.

The 2-Room Flexi was designed primarily in response to Singapore’s rapidly ageing population and the Government’s broader policy aim of allowing seniors to right-size their housing expenditure. A senior who no longer needs a large flat — or who wishes to monetise equity from an existing property — can purchase a short-lease 2-Room Flexi for a fraction of the cost of a standard flat, freeing up capital for retirement while remaining in the public housing ecosystem.

At the same time, the scheme remains open to younger singles aged 35 and above on a 99-year lease basis, giving unmarried Singaporeans their first route to public homeownership without the need to form a household with another person. This makes the 2-Room Flexi structurally significant as the only HDB flat type that a single Singaporean citizen aged 35 or above may purchase directly from HDB in a Build-To-Order (BTO) exercise.

Two Sub-Types of the 2-Room Flexi Flat

The 2-Room Flexi scheme comprises two distinct sub-types, which differ fundamentally in lease term, eligible buyers and exit options:

| Feature | Standard Lease (99yr) | Short Lease (15–45yr) |

|---|---|---|

| Who may apply | SC singles (35+), SC/SPR couples | SC households aged 55+ |

| Lease term | 99 years (from land grant) | 15, 20, 25, 30, 35, 40 or 45 years (buyer’s choice) |

| Indicative BTO price | From ~S$138,000 (non-mature) | From ~S$45,000 (15yr, non-mature) |

| CPF usage | Yes, subject to lease-CPF rules | Yes, subject to lease-CPF rules |

| Resale on open market | Yes, after 5-year MOP | No — must be sold back to HDB |

| Subletting (whole flat) | After MOP, with HDB approval | Not permitted |

| Key grant available | EHG (up to S$80k), PHG | Silver Housing Bonus (SHB) |

Short-lease buyers should note the critical exit restriction: unlike standard 99-year flats, a flat purchased on a short lease cannot be sold on the open resale market after the MOP. Instead, it must be returned to HDB at the end of the chosen lease term (the flat effectively reverts to HDB), or it may be sold back to HDB before lease expiry if the owner wishes to exit early. This means short-lease 2-Room Flexi flats carry zero capital appreciation potential and are explicitly designed as consumption housing rather than investment assets.

Eligibility — Who Qualifies?

The Housing & Development Board (HDB) sets out clear eligibility conditions for the 2-Room Flexi scheme. As at 2026, the key criteria are:

For the Standard 99-Year Lease (Singles and Couples)

- Citizenship: At least one applicant must be a Singapore Citizen. SPR singles may not apply for a BTO 2-Room Flexi; they may only purchase on the resale market.

- Age: At least 35 years of age for singles; standard family nucleus formation rules apply for couples (21 years and above).

- Income ceiling: Gross monthly household income must not exceed S$7,000 for singles or S$14,000 for households (combined all income sources).

- Property ownership restriction: Applicants must not own or have disposed of any private residential property (local or overseas) within the 30 months preceding application.

- Existing HDB flat: Singles who currently own an HDB flat and are applying as first-time applicants may still be eligible, subject to conditions regarding the sale of the existing flat.

For the Short Lease (Seniors Aged 55+)

- Citizenship: Singapore Citizens only.

- Age: All applicants must be aged 55 or above at point of application.

- Chosen lease term: The lease selected must cover the youngest applicant to at least age 95. For a 55-year-old, the minimum viable lease is therefore 40 years (55 + 40 = 95). HDB enforces this as a hard minimum.

- Income ceiling: S$14,000/mth household (same as standard). No income ceiling applies if buyers intend to monetise their flat through the Silver Housing Bonus (SHB) scheme.

- Existing property: Senior applicants may proceed even if they currently own an HDB flat, provided they commit to selling the existing flat (or subletting where applicable) within a prescribed period after collecting keys.

CPF Usage and Loan Mechanics

CPF Ordinary Account (OA) savings may be used to fund both the downpayment and monthly loan repayments for 2-Room Flexi purchases, subject to the CPF lease coverage requirement: the flat’s remaining lease must be able to cover the youngest buyer to age 95 for full CPF usage to be available.

For a 99-year BTO flat, this is rarely a constraint for applicants under 60. For short-lease buyers, the arithmetic matters. A 60-year-old buying a 35-year lease flat (lease ends when buyer is 95) meets the threshold exactly, allowing full CPF usage. A 60-year-old buying a 30-year lease (expires at 90) does not meet the threshold and will face CPF withdrawal limits, meaning more cash is required for the purchase.

The HDB Concessionary Loan at 2.60% per annum is available for eligible buyers of 2-Room Flexi flats, subject to the standard HLE (HDB Loan Eligibility) letter application and the Mortgage Servicing Ratio (MSR) test: monthly repayments must not exceed 30% of gross monthly household income.

Grants Available for 2-Room Flexi Buyers

| Grant | Who It Applies To | Maximum Amount | Eligibility Condition |

|---|---|---|---|

| Enhanced Housing Grant (EHG) | First-timer SC buying BTO or resale | S$80,000 (individual) / S$160,000 (family) | Income ≤ S$9,000/mth; continuous employment ≥12 months |

| Family Grant | SC/SC or SC/SPR couples, resale | S$50,000 (SC/SC) / S$40,000 (SC/SPR) | First-timer family nucleus; income and property conditions apply |

| Proximity Housing Grant (PHG) | Resale buyers living near/with parents | S$30,000 (within 4km) / S$20,000 (same town) | At least one applicant lives within 4km of parents/children |

| Silver Housing Bonus (SHB) | Seniors selling existing flat to right-size | Up to S$30,000 cash bonus | 55+; sold existing flat; purchase ≤ 3-room flat; top up to CPF RA |

| Singles Grant | SC single buying resale ≤ 5-room | S$25,000 | 35+, first-timer, income ≤ S$7,000/mth |

Grant stacking rules are complex and income-dependent. As a general principle, BTO buyers may access the EHG only (Family Grant is for resale), while resale buyers may stack the Family Grant, EHG and PHG subject to eligibility. Full grant conditions are published by HDB at hdb.gov.sg and change periodically in line with policy reviews.

Worked Example: Senior Buying a 2-Room Flexi (Short Lease)

Case Study — Mr Tan (SC, 62), Right-Sizing to a 2-Room Flexi

Profile: Mr Tan, Singapore Citizen aged 62, retired, monthly income S$1,800 (CPF LIFE payout). Currently owns a 4-room HDB flat in Bishan (sold for S$720,000, net proceeds after CPF refund: S$210,000 cash). No outstanding housing loan.

Target: 2-Room Flexi BTO, Hougang estate (non-mature), 35-year lease (youngest occupier Mr Tan, aged 62 → lease expires at age 97 → meets the age-95 threshold for full CPF usage). Indicative BTO price: S$100,000.

Silver Housing Bonus (SHB) eligibility:

- Sold 4-room flat: ✓

- Right-sizing to ≤ 3-room: ✓

- Top-up to CPF Retirement Account (RA): required for SHB disbursement

- SHB amount: S$20,000 cash (subject to RA top-up of S$60,000 minimum from sale proceeds)

Financing:

- Purchase price: S$100,000

- Less EHG (income S$1,800/mth, eligible): S$20,000 (indicative; exact amount determined by HDB based on income at time of application)

- Net purchase: S$80,000

- HDB loan (80% LTV): S$64,000 @ 2.60% over 25 years

- Monthly repayment: ~S$291/mth

- MSR check: S$291 / S$1,800 = 16.2% — PASS

Upfront cash:

- 20% downpayment: S$16,000 (payable via CPF OA, as lease covers to age 97)

- BSD on S$100,000: 1% × S$100,000 = S$1,000

- Legal and admin fees: ~S$1,500

- Total cash needed: approximately S$2,500 (remaining from CPF OA and cash)

Outcome: Mr Tan retains approximately S$210,000 net cash from the sale of his Bishan flat, gains S$20,000 SHB cash, and moves into a new flat with monthly repayments of S$291 — effectively freeing up substantial retirement capital while maintaining HDB homeownership in a new estate close to existing community networks.

Note: SHB amounts, EHG amounts, CPF withdrawal limits and HDB loan eligibility are all subject to prevailing HDB policy at time of application. The above is a simplified indicative illustration only.

What the 2-Room Flexi Scheme Means for Singapore’s Housing Market

The 2-Room Flexi scheme plays a structural role in Singapore’s housing policy architecture. For seniors, it provides a formal right-sizing pathway that releases larger flats back to the resale pool — supporting supply for young families who need more space. For singles, it is the de facto entry point into HDB ownership, filling a gap left by the original public housing framework that was designed around family nuclei.

Internationally, Singapore’s right-to-buy-back policy for short-lease flats is unusual. Most countries with public housing allow open-market resale of all units regardless of lease structure. Singapore’s decision to ring-fence short-lease stock within the HDB system prevents speculative resale of taxpayer-subsidised elderly housing and keeps the scheme’s fiscal cost manageable — but it also means seniors must plan carefully: once a short-lease flat is purchased, capital is largely locked in until the lease expires or the flat is sold back to HDB at a regulated price.

Looking ahead, the Government has signalled continued refinement of the Flexi scheme as the population ages. The Lease Buyback Scheme (LBS) — which allows seniors to sell part of their remaining lease back to HDB in exchange for CPF RA top-ups — complements the Flexi scheme and is likely to be expanded further. Seniors nearing retirement should consider modelling both options (right-sizing via 2-Room Flexi vs staying in their existing flat and using LBS) as part of a holistic retirement planning exercise.

Frequently Asked Questions

Can a single person buy a 2-Room Flexi flat?

Yes. Singapore Citizens aged 35 and above who are single may purchase a 2-Room Flexi flat on the standard 99-year lease basis, either through a BTO exercise or on the open resale market. This is one of the very few HDB flat types available to singles. SPR singles may only purchase 2-Room Flexi flats on the resale market (not BTO). The income ceiling for single applicants is S$7,000/mth gross. Grant eligibility (EHG, Singles Grant for resale) depends on first-timer status, income and other conditions set by HDB. Note that under the HDB eligibility framework, singles purchasing a 2-Room Flexi BTO may only apply in non-mature estates — mature estate BTO exercises for 2-Room Flexi flats are reserved for seniors (55+) on the short-lease sub-type.

Can I sell my 2-Room Flexi flat on the open market?

It depends on the lease type. If you purchased a standard 99-year lease 2-Room Flexi flat, you may sell it on the open HDB resale market after completing the 5-year Minimum Occupation Period (MOP) — the same rules as any other HDB resale flat, subject to EIP quotas and SPR quota restrictions. However, if you purchased a short-lease 2-Room Flexi flat (15–45 year lease), it cannot be sold on the open market at any time. It may only be returned to HDB at the end of the chosen lease or sold back to HDB before lease expiry at a regulated price. This is a critical distinction that buyers must understand before committing.

What is the Minimum Occupation Period for a 2-Room Flexi flat?

The Minimum Occupation Period (MOP) for a 2-Room Flexi flat is 5 years from the date of key collection (or from the date the last registered occupier moves in, if later). During the MOP, the entire flat may not be sublet, though individual rooms may be rented out with HDB’s prior approval. The MOP requirement applies regardless of whether the flat is purchased on a 99-year or short-lease basis. After completing the MOP, the 99-year lease flat may be listed for open-market resale; the short-lease flat may only be returned to HDB. There is no provision to reduce the MOP for 2-Room Flexi flats under current policy.

How does the Silver Housing Bonus work with the 2-Room Flexi?

The Silver Housing Bonus (SHB) is a cash incentive for seniors who right-size from a larger HDB flat to a smaller one (3-room or smaller, including the 2-Room Flexi). Eligible seniors receive a cash bonus of up to S$30,000, paid by HDB, when they use a portion of their flat sale proceeds (typically S$60,000 or more) to top up their CPF Retirement Account (RA) — which in turn boosts their monthly CPF LIFE payouts in retirement. The SHB is designed to be used in conjunction with a 2-Room Flexi purchase: a senior sells their 4- or 5-room flat, receives the SHB cash bonus, tops up their CPF RA for higher LIFE payouts and moves into a new, fully subsidised Flexi flat. The exact SHB amount depends on the total CPF RA top-up made and prevailing policy parameters at time of application. Full details at hdb.gov.sg.

Can I use CPF to buy a 2-Room Flexi short-lease flat?

Yes, CPF Ordinary Account (OA) savings may be used for the downpayment and monthly loan repayments, but only if the flat’s remaining lease is sufficient to cover the youngest buyer to age 95. For example, a 58-year-old buying a 37-year lease flat (58 + 37 = 95) satisfies the threshold and can use CPF OA in full. A 60-year-old buying a 30-year lease flat (expires at age 90) does not meet the threshold and faces CPF withdrawal restrictions, requiring more cash out of pocket. Buyers should model the CPF usage calculation before selecting their preferred lease term, and HDB’s loan eligibility framework should be confirmed via an HLE application before committing to a BTO ballot or resale OTP.

What happens to the flat when the short lease expires?

When a short-lease 2-Room Flexi flat’s lease expires, ownership of the flat reverts to HDB. There is no compensation payable to the former buyer — the flat’s value was fully priced into the discounted purchase price, and the buyer would have received use of the property for the entire chosen lease period. This is analogous to an annuity: the buyer “spent” the purchase price buying the right to live in the flat for a defined number of years. If the owner passes away before the lease expires, the remaining lease value may be inherited by eligible successors (typically a spouse) subject to HDB’s inheritance and transfer rules. The Estate will not receive residual cash value for the remaining lease.

Are 2-Room Flexi flats available in mature estates?

2-Room Flexi BTO flats are launched in both mature and non-mature estates, but with different restrictions. In non-mature estates, both singles (99-year lease) and seniors (short lease) may apply. In mature estates, the BTO 2-Room Flexi allocation is typically prioritised for seniors aged 55 and above on the short-lease sub-type, with a smaller quota for singles. Applications by singles in mature-estate BTO exercises compete in a higher-demand ballot environment. For the open resale market, there are no estate restrictions — singles and couples may purchase any available 2-Room Flexi resale flat islandwide, subject to EIP and SPR quota availability in the target block. Mature estate 2-Room Flexi resale flats command a premium of 20–40% over comparable non-mature estate units due to location and amenity access.

Related Articles

- HDB Prime, Plus and Standard Flats Singapore 2026: Complete Classification Guide

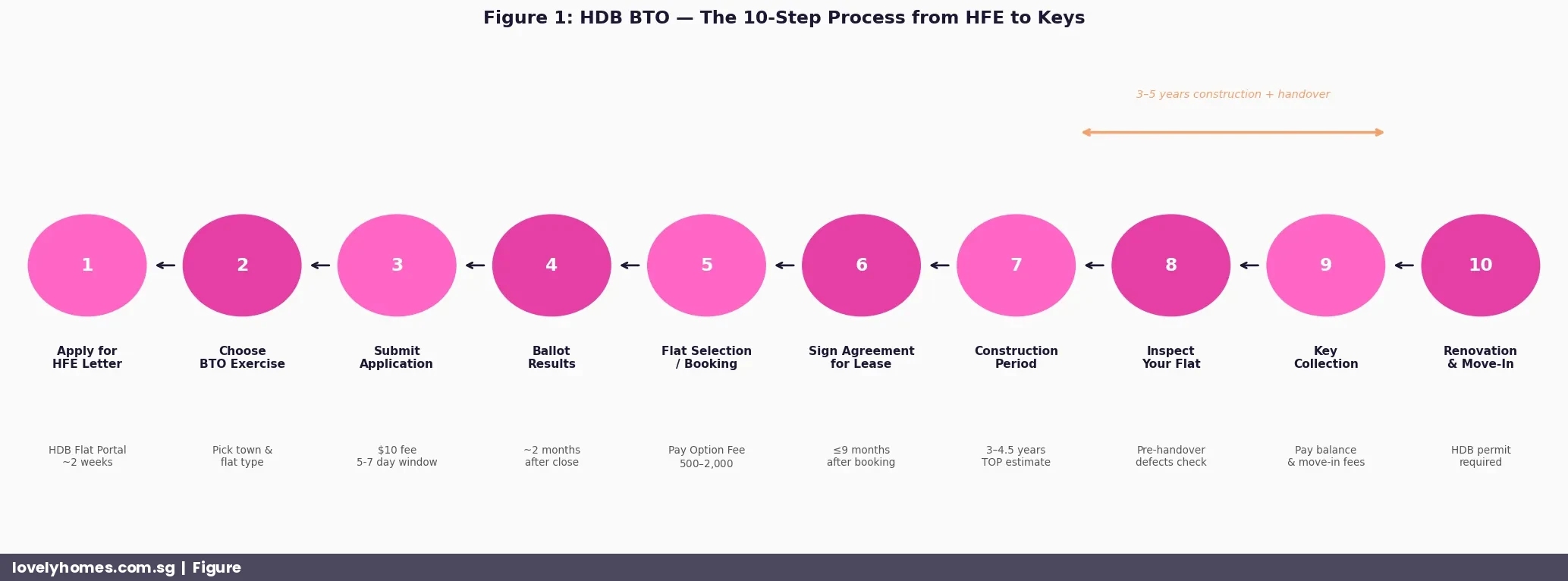

- HDB BTO Application Process Singapore 2026: Step-by-Step Guide

- HDB CPF Housing Grant Guide 2026: EHG, Family Grant, PHG and Singles Grant Explained

- HDB Lease Decay Singapore 2026: CPF Limits, Bank LTV and What Buyers Must Know

- Singapore Home Loan Interest Rates 2026: SORA vs Fixed Rate — Complete Guide

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore HDB MOP Complete Guide 2026

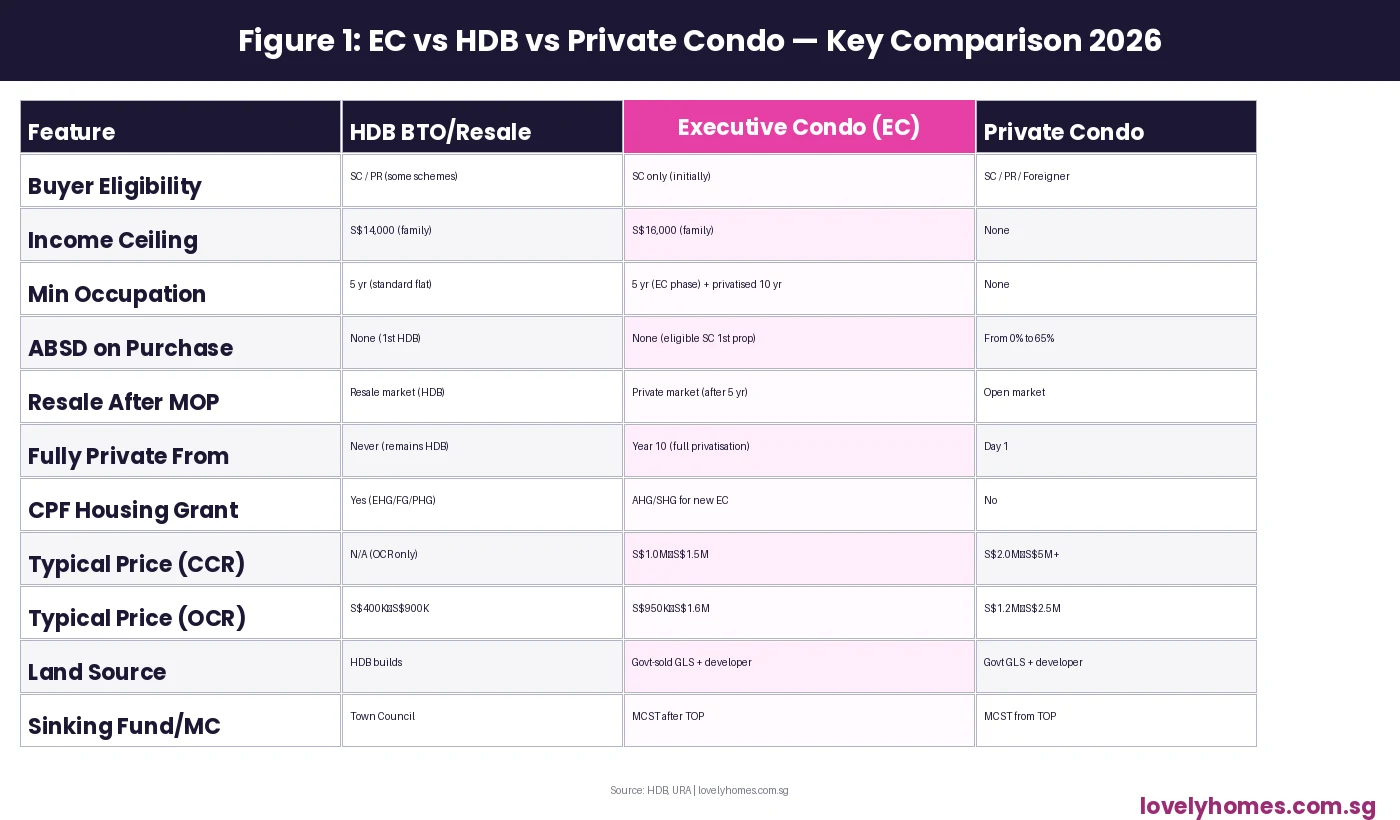

- Executive Condominium Buying Guide Singapore 2026

Disclaimer

The information in this article is provided for general informational and educational purposes only as at July 2026 and does not constitute financial, legal or property advice. HDB eligibility conditions, grant amounts, lease rules and CPF usage limits are set by the Housing & Development Board, CPF Board and relevant government agencies and are subject to change without notice. The worked example figures are indicative only and will differ based on individual circumstances. Readers should refer to HDB (hdb.gov.sg), CPF Board (cpf.gov.sg) and IRAS (iras.gov.sg) for authoritative and current information, and should consult a CEA-registered property agent and a licensed financial adviser before making any housing or retirement planning decision.

Click anywhere or press Esc to close