HDB BTO Process 2026: Complete Step-by-Step Guide from HFE to Key Collection

- Before you apply: you must hold a valid HDB Flat Eligibility (HFE) Letter from HDB’s MyHDBPage portal — it confirms your eligibility, grants, and loan quantum.

- Exercises are now quarterly (approximately Feb, May, Aug, Nov each year), each covering several towns and flat types.

- Application fee: S$10 non-refundable, applied within a 5–7-day window per exercise.

- Ballot results are released approximately two months after the application period closes; you receive a queue position if successful.

- Option fee at flat booking: S$500 for 2-Room Flexi, S$1,000 for 3-Room, S$2,000 for 4-Room and above.

- Construction wait: approximately 3–4.5 years from the booking date to Temporary Occupation Permit (TOP).

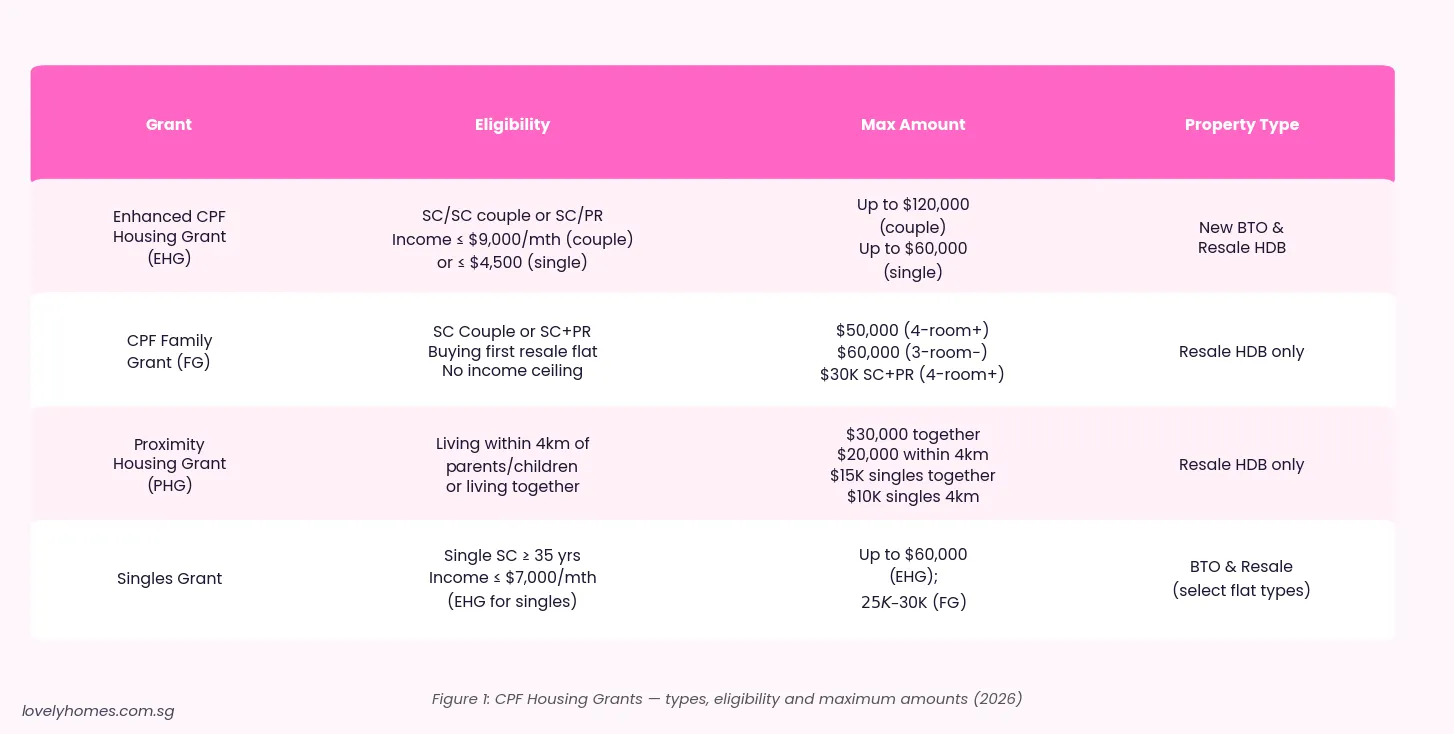

- Key grants for BTO: the Enhanced CPF Housing Grant (EHG) up to S$80,000 for first-timer couples; no Family Grant (FG) or Proximity Housing Grant (PHG) for BTO purchases — those apply to resale flats only.

- From application to keys: typically 4–6 years end-to-end, including the construction period.

What Is an HDB BTO Flat and Why Does It Exist?

Build-To-Order (BTO) is the Housing and Development Board’s (HDB’s) primary scheme for selling new public housing in Singapore. Rather than speculating on demand, HDB launches BTO exercises only after gauging the number of applicants during the application window. Flats are built only after sufficient uptake is confirmed, which is why the scheme is called “build to order.”

HDB administers the BTO programme under the Housing and Development Act. The scheme exists to keep public housing affordable — new BTO flats are priced significantly below market value, with prices set by HDB based on a “reasonable profit” model rather than open-market dynamics. In 2026, BTO prices for a new 4-Room flat in a non-mature estate typically range from S$350,000 to S$650,000, compared to resale prices of S$550,000 to S$800,000 for comparable flats in the same town.

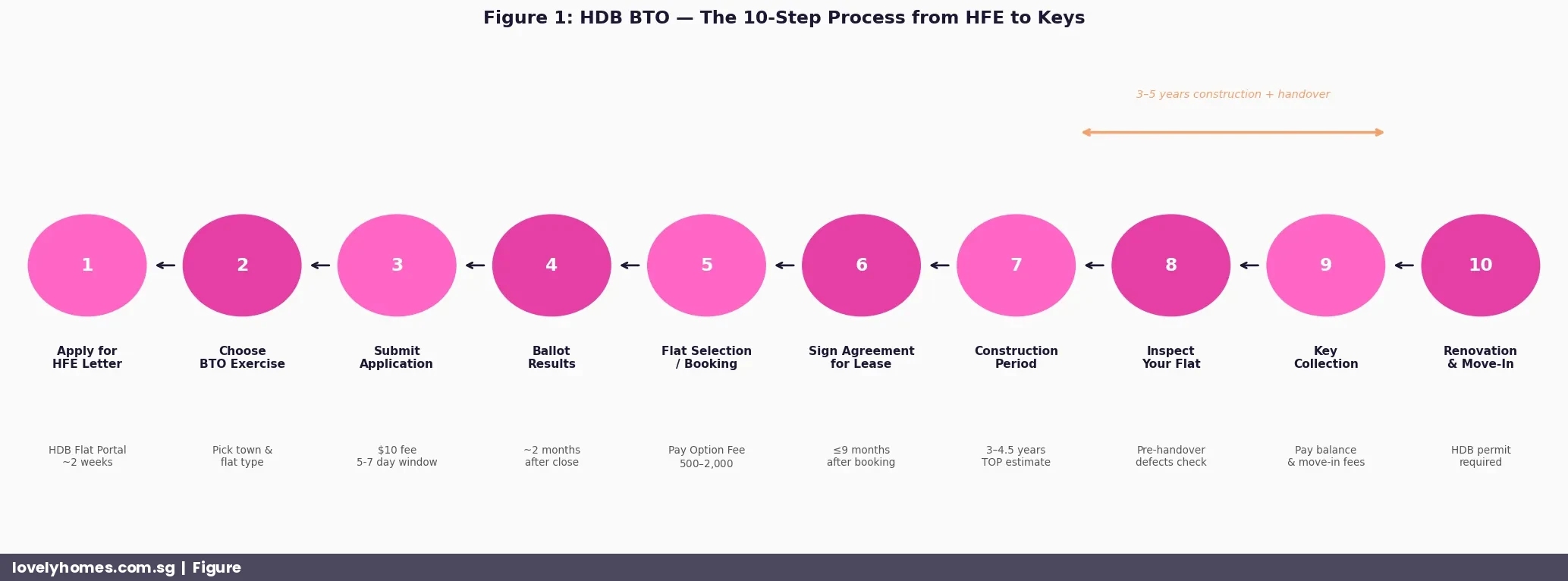

Step-by-Step: The 10-Stage HDB BTO Journey

Step 1: Apply for Your HFE Letter

Since 9 May 2023, every buyer must hold a valid HDB Flat Eligibility (HFE) Letter before applying for any BTO flat. The HFE replaces the former HDB Loan Eligibility (HLE) letter and serves as a single-stop document confirming your eligibility to purchase a flat, the grants you qualify for, and — if you plan to use an HDB concessionary loan — the loan quantum available to you.

Apply via HDB’s MyHDBPage portal. Processing typically takes about two weeks. You will need to provide Singpass-verified income data (through IRAS and CPF), current CPF OA balances, and details of any existing properties owned.

Step 2: Monitor BTO Exercises and Choose Your Town

HDB announces BTO exercises quarterly via press releases and the HDB Flat Portal. Each exercise covers multiple towns across Singapore — both mature estates (such as Toa Payoh, Queenstown, Ang Mo Kio) and non-mature estates (such as Tengah, Kallang/Whampoa, Woodlands). Non-mature estate flats are generally priced lower and carry no eligibility restrictions for first-timer couples, but carry a stricter Minimum Occupation Period (MOP) of five years before resale.

You may only apply for one flat type in one town per exercise. Study the flat type, floor, orientation, and proximity to MRT and schools carefully at the sales launch brochure — these factors cannot easily be changed later.

Step 3: Submit Your Application and Pay the S$10 Fee

Applications are submitted via the HDB Flat Portal during a window that typically runs for 5–7 days. A non-refundable S$10 application fee is charged. You do not need to pay anything further at this stage.

Step 4: Check Your Ballot Results

HDB publishes ballot results approximately two months after the application period closes. Log in to MyHDBPage to see your queue number. A queue number does not guarantee a flat — it indicates your priority in the flat selection queue. If your number is not called in the current exercise, you are not penalised and may apply again in future exercises.

Step 5: Flat Selection and Booking

HDB invites applicants to book a flat based on their queue position, typically four or more weeks after ballot results are released. You will receive an appointment slot roughly two weeks in advance. At the booking appointment, you choose your specific unit (block, floor, stack), review the floor plan, and pay the Option Fee: S$500 for 2-Room Flexi, S$1,000 for 3-Room, and S$2,000 for 4-Room and larger. At this stage, your chosen grants (EHG, if eligible) are also confirmed.

Step 6: Sign the Agreement for Lease

Within nine months of booking your flat, HDB will invite you to sign the Agreement for Lease — the formal legal document committing both parties to the transaction. At signing, you will:

- Pay the Buyer’s Stamp Duty (BSD) — typically from your CPF Ordinary Account (OA) — which for a S$560,000 flat comes to approximately S$11,400.

- Make the downpayment: 20% of purchase price if using an HDB concessionary loan (payable from CPF OA), or at least 25% (5% minimum cash) if using a bank loan.

- Your EHG grant (if applicable) will be credited to your CPF OA at this stage, reducing the net amount you need to draw from your own CPF savings.

Step 7: The Construction Period

Once the Agreement for Lease is signed, HDB proceeds with construction. The wait is typically 3–4.5 years from the booking date to TOP, though delays can extend this. During construction, you receive periodic status updates from HDB via MyHDBPage. There are no further progress payments for HDB concessionary loan holders — the HDB handles disbursements internally. Bank loan holders will have their bank disburse funds in stages as construction milestones are met, but this is handled automatically between HDB and the bank.

Step 8: Inspect Your Flat

Before key collection, HDB will invite you to conduct a pre-completion inspection of your flat. At this appointment, you check for defects — cracks, misaligned fittings, water stains, and any incomplete works. Defects are logged on the HDB Defects Inspection Form, and HDB’s main contractor is required to rectify all valid defects before or shortly after key collection. A one-year Defects Liability Period (DLP) applies from the date of key collection.

Step 9: Key Collection

Key collection is the most anticipated milestone. At this appointment you receive the physical keys to your flat, pay any outstanding fees (such as the one-time administration charges), and take possession. From this date, the five-year Minimum Occupation Period (MOP) begins — during which you must live in the flat as your principal place of residence and cannot sell or rent out the entire flat.

Step 10: Renovation and Move-In

Before commencing any renovation, you must apply for an HDB Renovation Permit through the HDB Flat Portal. Major structural works (e.g., hacking walls, installing bay windows, altering wet areas) require additional approval. All renovation contractors must be registered with HDB. Work is typically completed within six to twelve weeks, after which you can move in. Renovations may only be carried out during stipulated hours (Monday to Saturday, 9 am to 5 pm; prohibited on Sundays and public holidays).

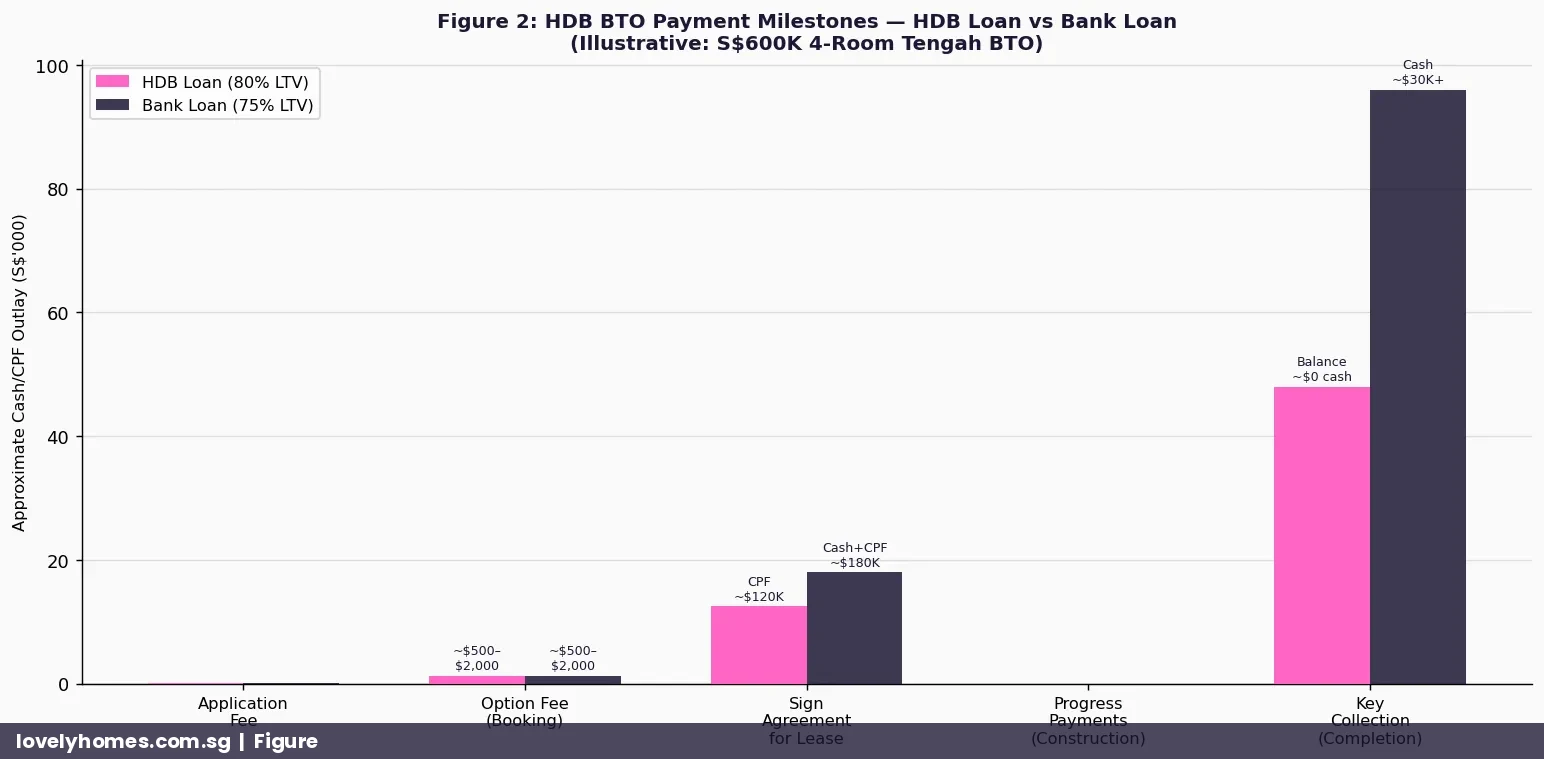

BTO Financing: HDB Loan vs Bank Loan

When financing your BTO flat, you choose between an HDB concessionary loan and a bank mortgage. The HDB loan charges a pegged rate (currently 2.60% per annum as at July 2026, pegged at 0.1% above the prevailing CPF OA interest rate of 2.50%), with an LTV of 80% and a maximum loan tenure of 25 years for the total remaining lease of the flat, or 65 years minus the oldest applicant’s age — whichever is shorter.

A bank loan typically offers a lower headline rate on fixed or SORA-linked packages, but the LTV is capped at 75% (requiring a minimum 5% cash downpayment) and refinancing is at the bank’s discretion. HDB also applies the Mortgage Servicing Ratio (MSR) of 30%: monthly repayments cannot exceed 30% of gross household income.

For more detail on financing, see our Singapore Housing Loan Guide 2026.

Summary: BTO, SBF, and Open Booking Compared

| Feature | BTO Exercise | Sale of Balance Flats (SBF) | Open Booking |

|---|---|---|---|

| What Is It? | Brand-new flats built on demand | Unsold BTO or returned flats | Remaining SBF flats, ongoing |

| Waiting Time | 3–4.5 years (under construction) | Ready or near-ready (≤1 year) | Immediate or very short |

| Ballot Required | Yes — competitive | Yes — competitive | No — first-come, first-served |

| Price vs Resale | 20–30% below | 10–20% below | Similar to SBF |

| Unit Choice | High in early launches | Limited | Very limited |

| Grants Available | EHG (up to S$80K) | EHG (up to S$80K) | EHG (up to S$80K) |

| Best For | Patient first-timers wanting maximum subsidy | Buyers who want quicker delivery | Immediate housing need |

Table 1: BTO vs Sale of Balance Flats (SBF) vs Open Booking — comparison as at July 2026.

Worked Example: Fatimah and Reza’s Tengah BTO Journey

Fatimah and Reza are a Singaporean citizen (SC) couple in their late 20s. Their combined monthly income is S$6,500. They apply for a 4-Room BTO flat in Tengah Glen at a purchase price of S$560,000 in the August 2025 exercise.

- HFE Letter: applied via MyHDBPage in June 2025; HDB confirms eligibility, EHG of S$30,000 (income bracket S$6,001–S$6,500), and HDB loan quantum of S$448,000.

- Application fee: S$10 at application in August 2025.

- Ballot results: issued in October 2025; queue number 385 of 1,200 applicants for 4-Room in Tengah Glen — a competitive but viable position.

- Flat booking: appointment in November 2025; select a 12th-floor unit facing the park. Option fee paid: S$2,000.

- Sign Agreement for Lease (February 2026): BSD of S$11,400 paid from CPF OA. Downpayment 20% = S$112,000, offset by EHG S$30,000 credited to CPF OA → net CPF drawn from own savings: S$82,000.

- HDB loan: S$448,000 at 2.60% p.a. over 30 years → monthly repayment approximately S$1,792; MSR = 27.6% (within 30% cap). Approved.

- Estimated TOP: September 2029 (approximately 3.8 years of construction). Key collection estimated October–November 2029.

- Total cash outlay: approximately S$2,000 (option fee) + S$0 at signing (no minimum cash for HDB loan holders) = S$2,000 cash. The balance comes from CPF OA and EHG grant. Renovation budget estimated at S$40,000–S$60,000 (cash or CPF).

What This Means for You

The BTO scheme remains the most cost-effective pathway to homeownership for Singaporean first-timers. The subsidy embedded in BTO pricing — often 20–30% below resale market value — is the most significant financial benefit available to eligible citizens, dwarfing the value of grants like the EHG.

The trade-off is time. A four-to-six-year wait from application to keys requires renters to budget for interim housing costs, or couples to time their applications around other life plans. Singapore’s CPF system is specifically designed to ease this wait: CPF OA savings accumulate at 2.50% per annum while you wait, growing your downpayment fund in parallel with HDB construction.

BTO is also increasingly competitive in popular towns and mature estates. Over-subscription rates for mature estate 4-Room flats regularly exceed 8-to-1. First-timers are given priority ballot positions (two ballot chances before being treated as second-timers), but patience and willingness to consider multiple towns remain critical success factors.

What Might Come Next

HDB is actively expanding the BTO supply pipeline as part of the government’s commitment to ease housing access. The 2026 BTO pipeline includes major new towns such as Tengah (the eco-town), Bayshore (East Coast waterfront), and continued launches in Kallang/Whampoa close to the city. Pricing for Plus and Prime flat categories — introduced in 2024 under HDB’s reclassification framework — carries additional restrictions (15-year MOP, subsidy clawback on resale) to moderate speculation in highly sought-after locations.

HDB has also signalled a shift towards more predictable, smaller-sized exercises rather than large twice-yearly launches, reducing the “all-or-nothing” ballot dynamic that has characterised BTO since the early 2000s. Watch for possible further reforms to the HFE system, grant eligibility rules, and income ceiling thresholds as the government responds to population ageing and wage growth trends through 2027.

Frequently Asked Questions

Can I apply for a BTO flat if my income exceeds S$14,000 per month?

No. The household income ceiling for purchasing a new HDB flat (BTO, SBF, or Open Booking) is S$14,000 per month for families and S$7,000 for singles. If your household income exceeds this ceiling, you are not eligible for any new HDB flat. You may, however, purchase a resale HDB flat on the open market — resale flats have no income ceiling — or an Executive Condominium (EC) if your household income is below S$16,000 per month. EC units are developed by private developers but are subject to HDB eligibility rules for the first ten years.

What happens if I miss my flat selection appointment?

If you miss your selection appointment without a valid reason, your queue number is forfeited and you lose the S$10 application fee. There is no penalty beyond this, but you will need to reapply in a future exercise and undergo the ballot process again. HDB does allow rescheduling within a narrow window if you contact them before your appointment date, so it is worth requesting a change early if you foresee a scheduling conflict.

Can I use CPF to pay for everything — the option fee, BSD, downpayment, and monthly repayments?

Almost, but not quite. The S$10 application fee is a cash payment. The option fee (S$500–S$2,000) paid at booking is also a cash payment, though HDB typically offsets this against the final purchase price. The BSD and downpayment can be paid from your CPF OA. Monthly HDB loan repayments can be serviced from CPF OA. However, no CPF OA monies can be used to pay ABSD (if applicable), Cash-Over-Valuation (COV) amounts, renovation costs, or property tax. For a first-timer purchasing a BTO flat at a price below the HDB Loan quantum, the CPF OA will typically cover the full downpayment and BSD with no need for cash beyond the option fee.

What is the Minimum Occupation Period (MOP) and what can I not do during it?

The MOP is five years from the date of key collection (or TOP, if HDB deems it appropriate). During the MOP you cannot sell your BTO flat on the open market, sublease the entire flat, nor purchase a private residential property in Singapore (or overseas in certain circumstances). You may, however, rent out individual rooms (subject to HDB approval and rules), and you are free to own foreign property in most cases. After the MOP, you may sell the flat on the HDB resale market, purchase a private property, or apply for another subsidised flat (though the resale levy will apply if you purchase another subsidised flat).

Can I back out after signing the Agreement for Lease?

Technically yes, but the financial consequences are severe. If you withdraw after signing the Agreement for Lease, you forfeit the option fee (S$500–S$2,000), may lose the administrative booking fee, and HDB may impose a debarment period — typically one year for a first withdrawal — during which you cannot apply for any new HDB flat. The debarment is two years for a second withdrawal. Given these penalties, withdrawing after signing is rare and should only be considered as a last resort after seeking legal advice.

What if construction is delayed beyond the estimated TOP date?

Construction delays are not uncommon, particularly for large developments or those in complex worksites. HDB will notify you of any revised TOP via MyHDBPage and by post. If the delay exceeds a specified threshold set out in the Agreement for Lease, you are entitled to late-delivery compensation: currently S$10 per day for studios and 2-room flats, and up to S$20 per day for 4-room and larger flats. This compensation is typically deducted from your final payment rather than paid in cash. Delays of more than 12 months are uncommon but have occurred, typically due to contractor insolvencies or major supply disruptions.

Related Articles

- Singapore HDB Grants Guide 2026: EHG, Family Grant, PHG and All CPF Housing Grants Explained

- Singapore HDB Downpayment Guide 2026: How Much Cash Do You Need?

- Singapore Housing Loan Guide 2026: HDB Loan, Bank Loan, TDSR, MSR and Fixed vs Floating Rates

- Singapore HDB Resale Buying Process Guide 2026: Step-by-Step from HFE to Keys

- Singapore CPF for Property Guide 2026: How to Use Your OA, Valuation Limits and Accrued Interest Explained

- Singapore EC Complete Guide 2026: Executive Condominium Eligibility, ABSD, MOP and Privatisation

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

Disclaimer

This article is published by LovelyHomes Editorial Team for general informational purposes only and does not constitute financial, legal, or property advice. HDB BTO eligibility criteria, grant amounts, loan quantum limits, and process timelines are set by the Housing and Development Board (HDB) and are subject to change. Grant eligibility is also governed by CPF Board rules. Stamp duty obligations are administered by the Inland Revenue Authority of Singapore (IRAS). Readers should refer to official HDB, CPF, and IRAS sources for the most current information, and consult a licensed financial adviser or HDB-registered salesperson before making any property purchase decision. All figures cited are indicative as at July 2026 and may not reflect individual circumstances.