The HDB Concessionary Loan Singapore 2026 is the financing instrument that quietly powers the majority of Build-To-Order purchases in this country. It carries a 2.6 per cent annual interest rate, an 80 per cent Loan-to-Value cap, and a one-Singapore-Citizen-per-household eligibility rule. For first-time buyers it is almost always cheaper than any private bank loan a Singapore household can access — and yet it comes with restrictions that catch a surprising number of upgraders out, especially the lifetime two-loan cap and the irreversible direction of refinancing.

This guide walks through how the HDB Concessionary Loan works in 2026, why HDB sets the rules the way it does, what eligibility actually means in practice, and how a typical Singapore Citizen household sees its loan sized and stacked. Figures and rules are administered by the Housing & Development Board, with the rate set in reference to the Central Provident Fund Ordinary Account (CPF OA) rate published by the CPF Board.

Quick Answer — HDB Concessionary Loan at a glance

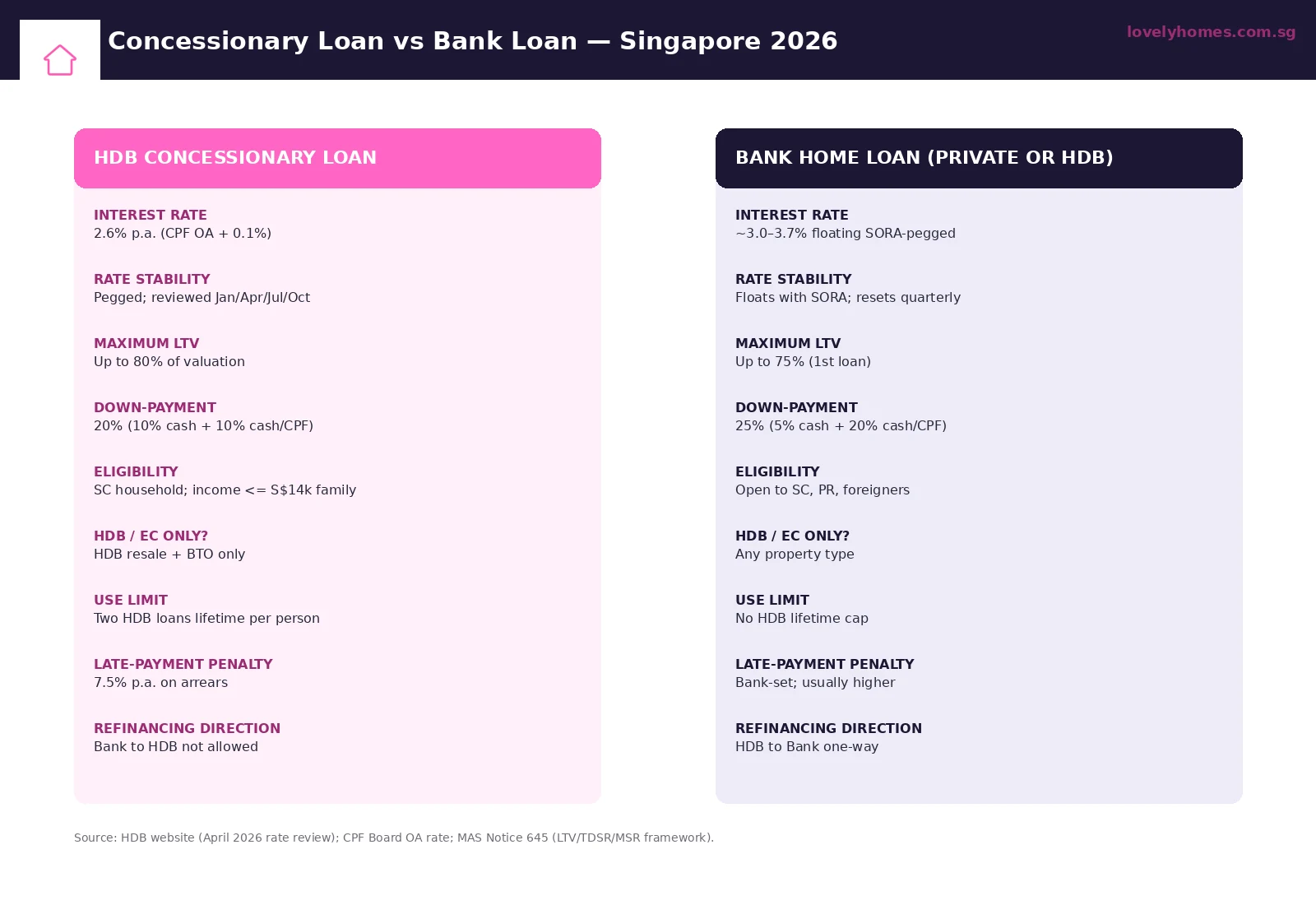

- Who can use it: at least one Singapore Citizen in the household (PR-only households are not eligible).

- The rate: 2.6 per cent per annum, pegged at the CPF OA rate plus 0.1 percentage points; reviewed quarterly in January, April, July and October.

- Loan-to-Value: up to 80 per cent of the lower of valuation or purchase price.

- Down-payment: 20 per cent of valuation, of which at least 10 per cent must be cash for first-loan flats; the balance can come from CPF OA.

- Income ceiling: S$14,000 family / S$7,000 single under the Singles Scheme / up to S$21,000 for Extended and Multi-Generation households.

- Lifetime cap: each adult is limited to two HDB Concessionary Loans, ever.

- Penalty for late payment: 7.5 per cent per annum on arrears.

- Refinancing rule: a homeowner can refinance from an HDB Loan to a bank, but never the reverse. Once you walk away from HDB, you cannot come back.

- MSR cap: Mortgage Servicing Ratio of 30 per cent of gross household income still applies; TDSR 55 per cent runs in parallel.

What an HDB Concessionary Loan Actually Is

The HDB Concessionary Loan is a fixed-rate housing loan that the Housing & Development Board (HDB) extends directly to eligible Singapore Citizen households for the purchase of an HDB flat — both Build-To-Order (BTO) and resale. Unlike a bank loan, where the lender prices in its own funding cost, profit margin and credit risk, the HDB Loan is a policy instrument: HDB borrows from the Government on the strength of CPF balances, and lends to households at CPF OA plus a 0.1 percentage-point spread. That spread has stayed at 0.1 percentage points since 1993, and the headline rate has tracked CPF OA all the way through Singapore’s interest-rate cycles.

The result is a remarkably stable rate. Through the rate-up cycle of 2022–23, when 3M SORA peaked above 3.7 per cent and bank fixed-rate home loans crossed 4.5 per cent, the HDB Loan rate stayed glued at 2.6 per cent because CPF OA stayed glued at 2.5 per cent. That stability is the single biggest reason why a household with the option to take an HDB Loan almost always should — at least at the point of purchase.

How HDB Sets the 2.6 Per Cent Rate

The HDB Concessionary Loan rate is not negotiated, advertised or shopped around. It is computed mechanically as the prevailing CPF OA rate plus 0.1 percentage points, reviewed every quarter at the same time the CPF Board reviews the OA rate. Because the CPF OA rate is itself a floor at 2.5 per cent — set in the CPF Act and changed only by Parliament — the HDB Loan rate has effectively been a 2.6 per cent floor since 1999.

The CPF OA rate is computed off a basket of 12-month and longer fixed deposit and savings rates of the local banks, with a hard 2.5 per cent statutory floor. In practice the basket has not lifted the OA rate above 2.5 per cent in a quarter-century, even when SORA approached 4 per cent. This matters for borrowers because the most likely upward shock to the HDB Loan rate is not a rate-up cycle but a long, sustained period of high deposit rates that drives the basket above the 2.5 per cent floor — which has not happened in living memory.

The practical takeaway: a household stress-testing affordability against the HDB Loan should treat 2.6 per cent as the central case and 3.0 per cent as a pessimistic upper bound. Banks are required to use the MAS-prescribed 4.0 per cent stress test under the Total Debt Servicing Ratio framework even when the actual rate is 3.0 per cent — but the HDB Loan eligibility check uses the actual 2.6 per cent rate, not the 4.0 per cent stress rate. That gap alone widens borrowing capacity by 12 to 15 per cent for the typical first-timer.

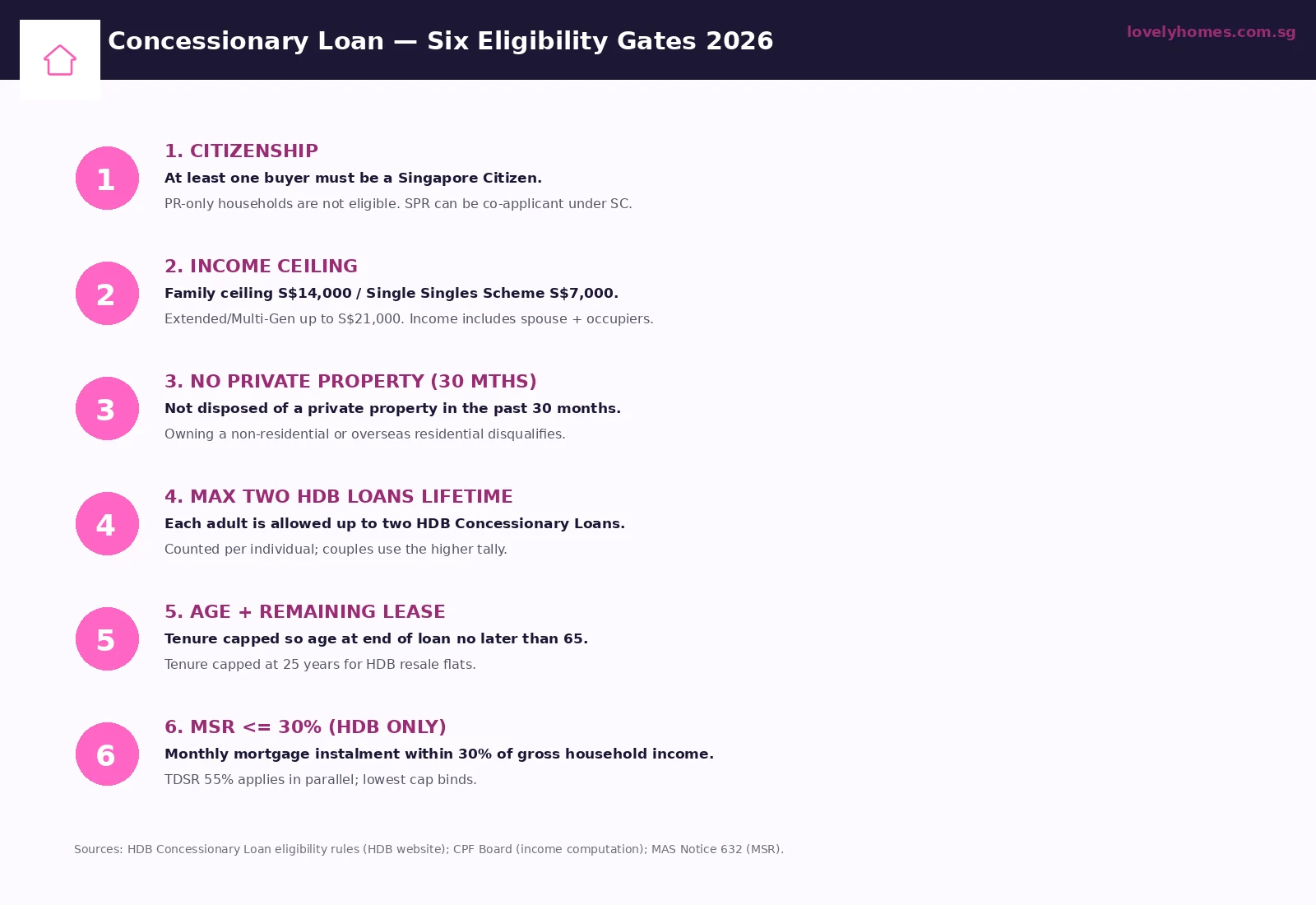

The Six Eligibility Gates

HDB applies six criteria before issuing a Loan Eligibility (HLE) letter, and an applicant must satisfy all six to qualify. The HLE is the gateway document — without it, neither the option-to-purchase nor the conveyancing solicitor can move forward on an HDB Loan.

Gate 1 — Citizenship. At least one of the buyers (or proposed occupiers, depending on the scheme) must be a Singapore Citizen. A Singapore Permanent Resident may co-apply, but a PR-only household cannot take an HDB Loan even if they qualify for the flat itself. This is the single largest filter against the HDB Loan: any household that becomes PR-only through citizenship change is automatically pushed to bank financing on its next purchase.

Gate 2 — Income ceiling. The household monthly income ceiling depends on flat type and scheme. Standard families face S$14,000. The Singles Scheme (where one Singapore Citizen aged 35 or above buys alone) caps at S$7,000. Extended Family Schemes — for two-generation households or families assisting parents — go up to S$21,000. The income calculation includes the gross monthly income of all proposed occupiers, with bonuses and variable pay annualised over the past 12 months. Applicants with self-employed income are assessed off two years of IRAS Notice of Assessment.

Gate 3 — No private property in the past 30 months. Buyers (and their proposed occupiers) must not have disposed of a private residential property in Singapore or overseas within the 30 months immediately before the HLE application. This rule is what prevents an upgrader who sold a private condo last year from “downgrading” back into a heavily-subsidised HDB Loan. Owning a non-residential property (industrial, retail, commercial) does not disqualify, but holding any private residential property at the point of application does.

Gate 4 — Two HDB Loans lifetime per adult. Each adult Singapore Citizen is allowed up to two HDB Concessionary Loans in their lifetime. Married couples count separately, but only the higher of the two tallies is recognised when they buy together. A buyer who has already taken two HDB Loans is shut out — full stop — even if every other condition is met. This rule is what nudges most second-time-upgrader households toward bank financing, even when they could theoretically still meet the other five gates.

Gate 5 — Age and remaining lease. The loan tenure must be capped so that the buyer does not exceed age 65 at the end of the loan, or that the remaining lease at the end of the loan is at least 60 per cent of the original lease — whichever is shorter. For HDB resale flats, the maximum tenure is 25 years; for BTO flats, 25 years (the BTO comes with a fresh 99-year lease, so the lease constraint rarely binds for a new flat).

Gate 6 — MSR within 30 per cent of gross income. The Mortgage Servicing Ratio cap, administered under MAS Notice 632, requires the monthly mortgage instalment to fit within 30 per cent of the household’s gross monthly income. The HDB Loan’s eligibility test uses the actual 2.6 per cent rate and proposed tenure to compute the instalment, while bank loans use the 4.0 per cent stress rate. TDSR (Total Debt Servicing Ratio at 55 per cent) runs in parallel — and for HDB purchases by income-leaner households, MSR is what binds.

How the 80 Per Cent LTV Reshapes the Down-Payment

The Loan-to-Value cap on a first HDB Concessionary Loan is 80 per cent of the lower of valuation or purchase price. That is five percentage points more than the 75 per cent LTV cap that a bank can extend on a first private property loan. The translation into the down-payment is meaningful.

For a S$650,000 four-room BTO, the down-payment under an HDB Loan is S$130,000 (20 per cent), of which 10 per cent (S$65,000) must be paid in cash. The other 10 per cent (S$65,000) can be drawn from the buyer’s CPF OA. By contrast, a bank loan on a S$650,000 resale would cap at 75 per cent LTV, giving a S$162,500 down-payment, of which the cash leg is at least S$32,500 (5 per cent) but the cash-or-CPF leg widens to S$130,000. The HDB Loan therefore demands a higher cash leg in absolute terms (S$65,000 versus S$32,500) but a lower total cash-and-CPF outlay (S$130,000 versus S$162,500). For a Singapore Citizen household with healthy CPF OA balances and modest cash savings, the HDB Loan is dramatically the cheaper path to keys.

The Enhanced CPF Housing Grant (EHG), worth up to S$120,000 for first-time families and up to S$60,000 for first-time singles, is layered on top. EHG is paid as cash from the Government to HDB and credited against the purchase price at completion, which directly reduces the buyer’s cash leg. For most lower-and-middle-income BTO buyers, EHG plus the HDB Loan combine to reduce the cash-out-of-pocket leg of the purchase to a few thousand dollars — sometimes less than the cost of furniture for the new flat.

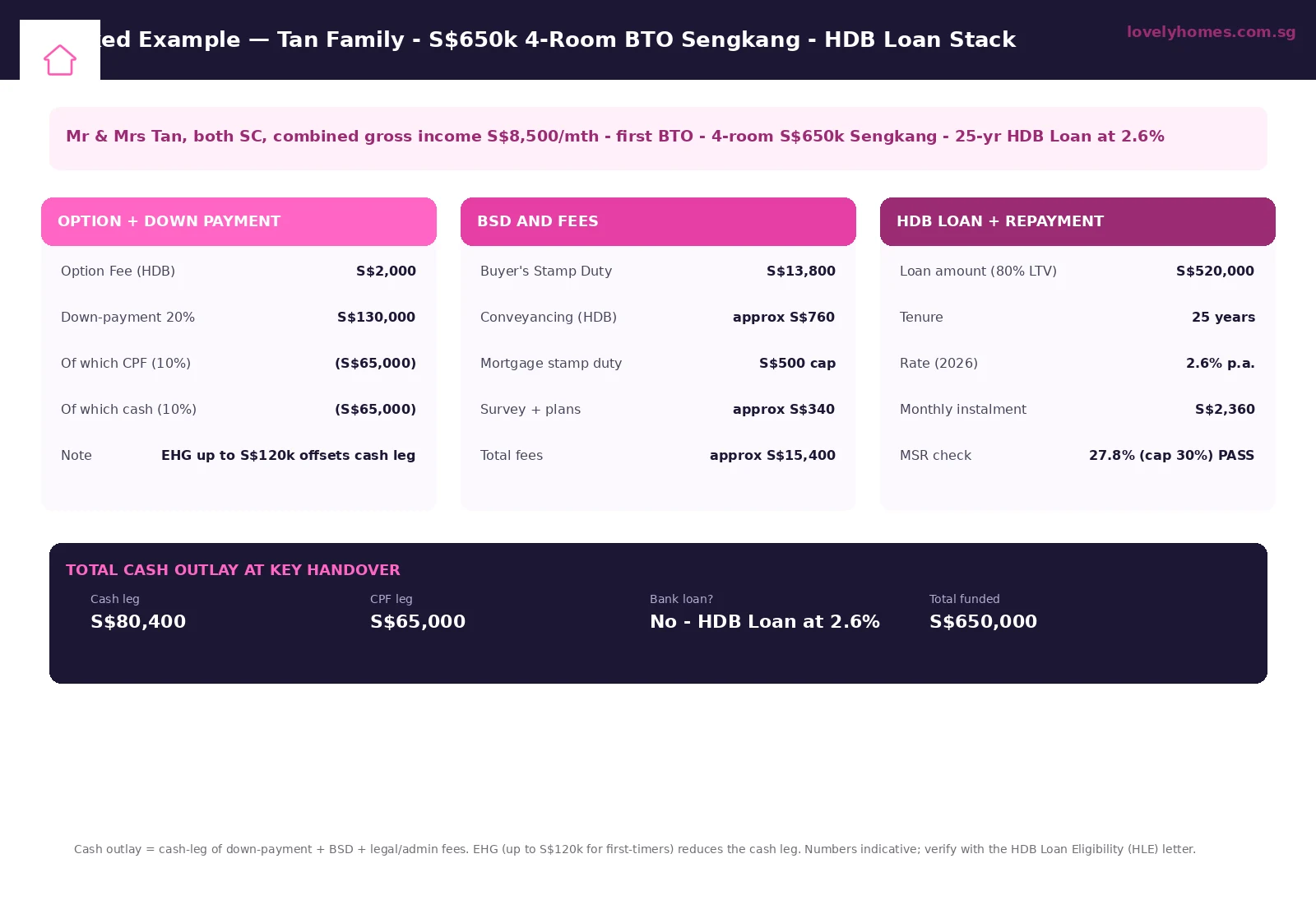

Worked Example — Tan Family, S$650,000 Sengkang BTO

Worked Example. Mr and Mrs Tan are both Singapore Citizens, aged 32 and 30. Their combined gross monthly income is S$8,500 (Mr Tan S$5,000, Mrs Tan S$3,500), no variable pay, no other loans. They have just been allotted a four-room BTO in Sengkang priced at S$650,000 with a 99-year lease commencing on key collection. They have S$200,000 in combined CPF OA and S$110,000 in joint cash savings.

Stacking the price. The maximum HDB Loan is 80 per cent of S$650,000 = S$520,000. The down-payment is S$130,000 (20 per cent), of which the minimum cash leg is S$65,000 (10 per cent of valuation). Mrs Tan can use S$65,000 from the CPF OA for the other 10 per cent.

Stamp duty and fees. Buyer’s Stamp Duty on a S$650,000 flat is computed under the residential rate ladder (1 per cent on first S$180k + 2 per cent on next S$180k + 3 per cent on next S$640k up to S$1m + 4 per cent on next S$500k up to S$1.5m, etc.). For S$650,000: BSD = 1,800 + 3,600 + 8,400 = S$13,800. Conveyancing through HDB Legal is approximately S$760, mortgage stamp duty caps at S$500, and HDB charges minor survey and plan fees of around S$340. The total fee leg is roughly S$15,400.

The repayment. A S$520,000 loan over 25 years at 2.6 per cent has a monthly instalment of S$2,360. Against the household’s S$8,500 gross monthly income, the MSR comes to 27.8 per cent — comfortably within the 30 per cent cap. The TDSR check is not binding because the family has no other debt; the same S$2,360 monthly instalment occupies just 27.8 per cent of income, well within the 55 per cent ceiling.

The grants. Because both buyers are first-timers and the household income is below S$9,000, the family qualifies for the maximum Enhanced CPF Housing Grant of S$80,000 (the full S$120,000 ceiling applies only to households below S$1,500 monthly income; the S$80,000 tier applies in the S$8,001–S$9,000 income band). EHG is paid into the buyer’s CPF OA and credited at key collection, effectively reducing the price to S$570,000 from the household’s perspective — but for HDB Loan computation, the loan and LTV are still anchored to the S$650,000 valuation. The grant flows back into CPF, deepening the OA balance for future top-ups or for offsetting future instalments.

Total cash outlay at key collection. Cash leg of down-payment S$65,000 + BSD S$13,800 + fees S$1,600 + option fee S$2,000 (offset later) = approximately S$80,400 in true cash. CPF OA leg = S$65,000. Total funded into the flat = S$650,000.

This is the structural reason the HDB Loan is the preferred instrument for first-timer BTO households in 2026: the maths simply works at a price-point and an income-level where bank financing leaves the buyer with a five-figure shortfall on the cash leg.

The Two-Loan Lifetime Cap — and Why It Bites

HDB allows each Singapore Citizen up to two HDB Concessionary Loans in a lifetime. The cap counts both BTO purchases and resale purchases that used HDB financing. Loans taken under earlier CPF-grant schemes (like the now-discontinued Special CPF Housing Grant) count toward the cap. Refinancing within the HDB Loan is a continuation of the same loan and does not consume an additional slot, but a redemption-and-reborrow against a new flat purchase does.

The cap binds most often when an upgrader couple — say, a Sengkang BTO bought in 2014 with their first HDB Loan, sold in 2024 for an HDB resale in Bishan with their second HDB Loan — wants to move again to a four-room in 2030. By then, both adults have used both their HDB Loan slots; they are forced into bank financing on the third purchase, even though the third purchase is still an HDB flat. This is a deliberate policy lever: HDB wants to ration its concessional finance toward first-and-second-time buyers and to push the capital-rich third-time buyer into the private banking sector.

The corollary is that an applicant with a partner who has already used both slots cannot extend their own remaining slots to the household — joint loans use the higher individual tally, but they cannot net off a fully-used partner against unused slots from the other side. This is the single most surprising rule for second-marriage households where one spouse has fully-utilised HDB Loan history. The household is forced to bank financing.

The One-Way Refinancing Door

An HDB Concessionary Loan can be refinanced to a bank loan at any time after the Minimum Occupation Period is fulfilled (or earlier with HDB consent for hardship cases). The reverse is not allowed: once an HDB flat owner has refinanced to a bank, they cannot move back to the HDB Loan, even if they later regret the move. The rule is hard and absolute.

This is a critical decision point for HDB-flat households at every quarterly rate review. In a low-rate environment — where bank floating rates briefly drop below 2.6 per cent — the household may be tempted to refinance to a bank for the cash-flow saving. But the saving is illusory if rates rise back above 2.6 per cent within 18 to 24 months: the household cannot reverse the move, and it now sits on a floating-rate loan whose stress-test ceiling at 4.0 per cent could comfortably exceed the original 2.6 per cent HDB rate.

The rule of thumb: do not refinance from HDB to bank unless (a) the bank’s quoted rate is at least 50 basis points below 2.6 per cent for the entire fixed-rate period, AND (b) the household has the cash buffer to absorb a return to 4.0 per cent under the 4.0 per cent TDSR stress without distress. The first condition has held for less than 24 months in the past decade. The second condition is what trips upgrading households who refinanced in 2020–21 and now see their bank rate above 3.5 per cent.

The 7.5 Per Cent Late-Payment Rule

HDB charges 7.5 per cent per annum on arrears, simple interest, computed daily. The penalty is moderate by Singapore lending standards — bank late charges typically run from 8 to 12 per cent per annum on arrears, with some products applying compounded daily charges and minimum monthly fee floors. HDB also has a more flexible posture toward genuine hardship: the borrower can apply for instalment deferment, term extension or partial-payment arrangement directly through the HDB Mortgage Servicing portal, and the back-office tends to accept reasonable hardship documentation without escalation.

This is one of the under-appreciated qualitative differences between HDB and bank financing. HDB does not chase its borrowers into the courts the way an unsecured creditor does; it has a structural mandate to retain the household in the flat. Default and forced sale are very rare outcomes — the system works through deferment and reschedule, not through repossession.

Summary Table — HDB Concessionary Loan 2026

| Parameter | Rule (2026) | Source |

|---|---|---|

| Interest rate | 2.6% p.a. (CPF OA + 0.1 pp) | CPF Board, HDB |

| Rate review | Quarterly (Jan, Apr, Jul, Oct) | CPF Act |

| First-loan LTV | Up to 80% of valuation | HDB |

| Down-payment cash leg | 10% of valuation in cash; 10% from CPF OA permitted | HDB |

| Tenure ceiling | 25 years for resale; 25 years for BTO | HDB |

| Income ceiling — family | S$14,000 gross household monthly | HDB |

| Income ceiling — Singles Scheme | S$7,000 single Singapore Citizen aged 35+ | HDB |

| Income ceiling — Extended/Multi-Gen | Up to S$21,000 | HDB |

| Lifetime loan cap | Two HDB Concessionary Loans per adult | HDB |

| MSR cap | 30% of gross monthly income (HDB and EC purchases) | MAS Notice 632 |

| TDSR cap | 55% of gross monthly income (all property loans) | MAS Notice 645 |

| Late-payment penalty | 7.5% p.a. simple interest on arrears | HDB |

| Refinancing | HDB to bank: yes; bank to HDB: no | HDB |

What This Means for You

The HDB Concessionary Loan is the most heavily subsidised housing finance instrument any Singapore Citizen household will ever access. The combination of a 2.6 per cent fixed-by-policy rate, an 80 per cent LTV cap, a friendly late-payment regime, and the option to layer EHG on top makes it the default starting point for any buyer who can qualify. The strategic question is therefore not whether to take the HDB Loan, but how to preserve access to it across the household’s life cycle.

Three rules of thumb follow. First, do not refinance from HDB to bank unless the bank rate is at least 50 basis points below 2.6 per cent for the duration of the fix, and the household can withstand a return to 4.0 per cent. Second, if a household holds two unused HDB Loan slots between the two adults, treat the second slot as the upgrade slot — preserve it for the move from the BTO into the resale flat or into the EC at the point of family expansion. Third, before any private property purchase, model the 30-month disqualification window: the moment the household sells a private home, the 30-month clock starts ticking on HDB Loan re-eligibility for the next HDB purchase.

What Might Come Next

The HDB Concessionary Loan rate has been pinned at 2.6 per cent since 1999, which is to say through every rate-up cycle of the past 26 years. The most likely vector of change is not the rate itself but the eligibility envelope. The income ceiling has stepped up over the last decade in tandem with median household income, and may continue to creep up in subsequent National Day Rally announcements. The Multi-Generation income ceiling has shown the most sensitivity to policy adjustment.

The two-loan lifetime cap and the citizenship gate are unlikely to change. They are deliberate rationing levers — the Government wants concessional finance flowing to first-time and upgrading citizen households rather than to the third-time mover or to PR-only households. The 30-month no-private-property rule could, in theory, be tightened or loosened depending on private-market dynamics, but the direction of change in recent cooling-measure cycles has been to lengthen lookback periods, not shorten them. A buyer who relies on the HDB Loan to make their housing maths work should plan around the rules as they stand and treat liberalisation as an upside surprise rather than a base case.

Frequently Asked Questions

Can a Permanent Resident take an HDB Concessionary Loan?

No. At least one buyer (or proposed occupier, depending on the scheme) must be a Singapore Citizen for the household to qualify. A PR may co-apply with a Singapore Citizen, but a PR-only household must take a bank loan even if it is buying an HDB resale flat.

What happens if my income exceeds the ceiling between application and key collection?

The income check is taken at the point of HLE application and re-verified at key collection. A modest increase that still leaves the household within the ceiling is fine. Crossing the ceiling between HLE issuance and key collection — for example because of a job change or promotion — does not retroactively cancel the HLE if the loan was already booked, but a new HLE for a fresh purchase would have to satisfy the new income at the time of application.

Does my CPF Special Account or Medisave count toward HDB Loan affordability?

No. Only CPF Ordinary Account (OA) balances can be used to fund the down-payment, monthly instalments, BSD and legal fees on an HDB flat. Special Account, Medisave and Retirement Account balances are not available for housing — the OA is the dedicated housing pocket within the CPF system.

Can the loan tenure go beyond 25 years?

For HDB-purchased flats, no — 25 years is the maximum. A bank loan can extend to 30 years (or 35 for some private property), but extending tenure on a bank loan beyond 30 years (or beyond age 65 at end of loan) triggers a step-down in the LTV cap from 75 per cent to 55 per cent. The HDB Loan does not offer a comparable extended-tenure option.

If I take an HDB Loan and later get a windfall, can I make a partial prepayment without penalty?

Yes. HDB does not impose a prepayment penalty on partial or full early redemption of the Concessionary Loan. The flexibility is one of the under-appreciated benefits versus a fixed-rate bank loan, where partial prepayment during the lock-in period typically attracts a 1.5 per cent fee on the redeemed amount.

Can I use the HDB Loan to buy an Executive Condominium (EC)?

No. The HDB Concessionary Loan funds only HDB flats — BTO and resale. ECs are sold by private developers under a hybrid scheme and must be financed through a bank loan from the developer launch onward. The MSR 30 per cent rule still applies for the first 10 years of an EC’s life (until full privatisation), but the bank rates apply.

What is the cost of switching from an HDB Loan to a bank loan?

Legal fees of approximately S$1,800 to S$2,500 (depending on the bank’s panel solicitor), valuation fee of around S$300, and the bank’s processing or admin fee (typically S$300 to S$500). Some banks subsidise the legal and valuation fees as part of their loan offer; verify the small print. There is no clawback from HDB on grants used at original purchase, provided the Minimum Occupation Period has been served.

Disclaimer

This article provides general guidance for Singapore Citizen households considering the HDB Concessionary Loan and is not financial, tax or legal advice. The 2.6 per cent rate, 80 per cent LTV cap, MSR threshold, eligibility ceilings and lifetime two-loan rule reflect rules administered by the Housing & Development Board, the CPF Board and the Monetary Authority of Singapore in force as at the publication date. For the rule that applies to your specific transaction, consult HDB Mortgage Servicing, the CPF Board, the Monetary Authority of Singapore, the Inland Revenue Authority of Singapore and a licensed Singapore mortgage adviser or solicitor. Always rely on official sources — HDB, CPF, MAS, IRAS — for the latest position before transacting.

Related Articles

- TDSR Singapore 2026: How the 55% Cap and 4.0% Stress Test Decide Your Home Loan

- LTV Limits Singapore 2026: How Much You Can Borrow for Your Home or Investment Property

- CPF for Property Purchase Singapore 2026

- CPF Accrued Interest Singapore 2026

- Buyer’s Stamp Duty Singapore 2026

- Conveyancing Process Singapore 2026

- Executive Condominium Singapore 2026

0 Comments