HDB Resale Market Q1 2026: Prices Fall 0.6% in First Decline Since 2019

Quick Answer

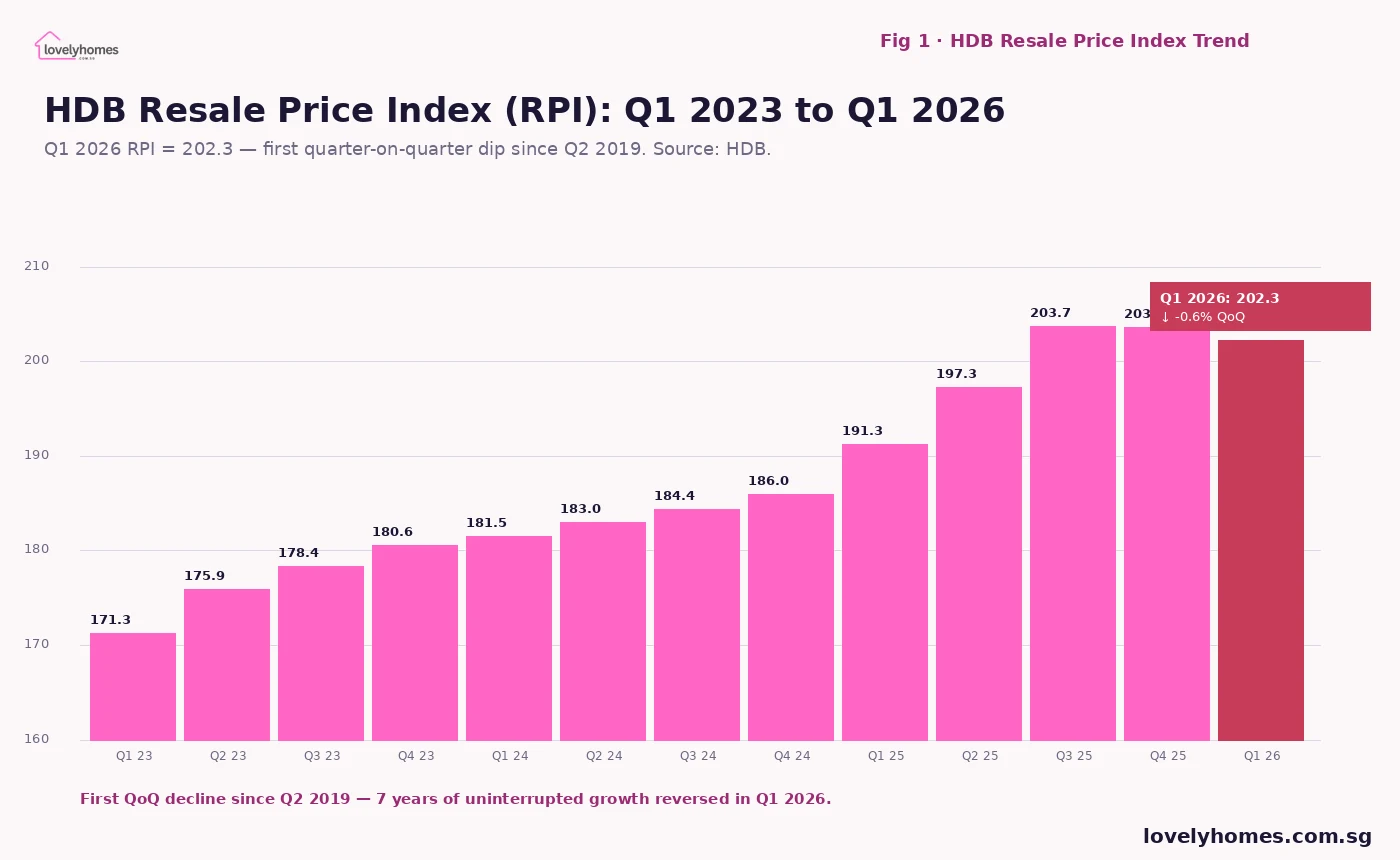

- The HDB Resale Price Index (RPI) fell 0.6% quarter-on-quarter in Q1 2026, from 203.6 in Q4 2025 to 202.3 — the first decline since Q2 2019.

- The dip breaks a 27-quarter streak of flat or rising resale prices, signalling early-stage market cooling after years of post-pandemic appreciation.

- Transaction volumes were 6,107 resale flats in Q1 2026, broadly in line with Q4 2025 levels — the price softening is driven by supply rather than a demand collapse.

- The MOP supply wave — 13,480 HDB flats reaching their 5-year Minimum Occupation Period in 2026 — is the structural factor adding resale supply.

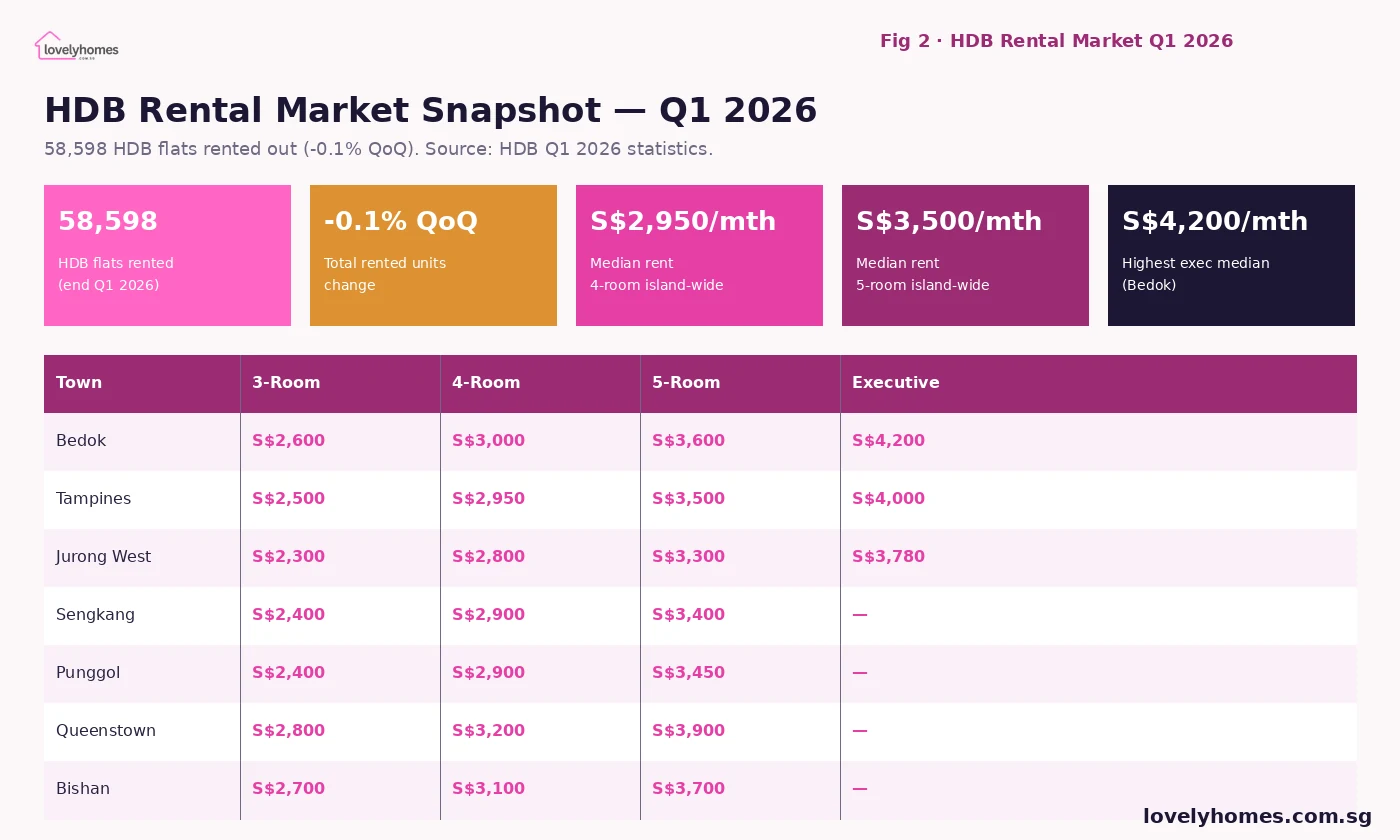

- HDB rents held relatively steady: 58,598 flats rented at end-Q1, with median rents ranging from S$2,300 (3-room Jurong West) to S$4,200/mth (executive Bedok).

- Million-dollar resale transactions continued to feature, with a new record of S$1.728M at City Vue @ Henderson (Henderson Road, April 2026).

- Analysts describe the trajectory as a “soft landing” — the price dip is small and unlikely to accelerate sharply unless interest rates rise again or unemployment climbs.

What the Q1 2026 HDB Resale Data Shows

HDB released its 1st Quarter 2026 Public Housing Statistics on 25 April 2026, revealing that the Resale Price Index — the primary measure of HDB resale flat price movements — dipped 0.6% quarter-on-quarter to 202.3. This ends a remarkable run: from Q3 2019 through Q4 2025, the RPI rose or held flat in every single quarter, a 27-quarter streak fuelled first by the pandemic-era demand surge (2020–2022), then by the post-pandemic upgrader wave and tight resale supply (2023–2024), then by continued above-median-income household demand (2025).

The 0.6% dip is modest in absolute terms — the RPI remains 18% above its Q1 2023 level — but its direction is significant. It confirms what market practitioners have been observing since late 2025: sellers are taking longer to find buyers, price gaps between asking and transacted prices have widened, and the buyer pool is showing greater selectivity.

Why Prices Dipped: The MOP Supply Effect

The primary explanation for the price softening is straightforward: supply. As LovelyHomes reported in May 2026, approximately 13,480 HDB flats are reaching their 5-year Minimum Occupation Period (MOP) in 2026, up 93% year-on-year from the approximately 6,980 that crossed MOP in 2025. This is partly a consequence of the BTO surge years of 2016–2018, when HDB completed large volumes of units in towns including Punggol (est. 3,200 MOP units), Sengkang (est. 2,400), Tengah (est. 1,900), and Bidadari (est. 1,800).

As these flat owners become eligible to sell on the open market, many are choosing to do so — either to capture appreciation gains, to upgrade to private property, or to rightsize. The resulting increase in resale listings gives buyers more choice and more negotiating room, which compresses prices at the margin.

A structural supply increase of this magnitude does not typically reverse quickly. The MOP pipeline into 2027 remains elevated, meaning the resale supply overhang is likely to persist through much of 2026 and into 2027. This is not a liquidity crisis or a demand collapse — transaction volumes remain healthy — but it is a period where sellers who need to move quickly will likely accept modest discounts to achieve a timely sale.

Transaction Volume: Stable, Not Falling

Notably, the price dip in Q1 2026 was not accompanied by a volume collapse. HDB reported approximately 6,107 resale transactions in Q1 2026, broadly in line with the approximately 6,200 recorded in Q4 2025. This is an important distinction: a falling price index alongside stable volume suggests a price-discovery adjustment driven by supply rather than a demand retreat. When markets fall on low volume, it often signals more serious stress; when they adjust modestly on normal volume, it is more consistent with a soft landing.

Million-dollar resale flats continued to transact. There were 165 million-dollar HDB transactions in Q1 2026, slightly below the 188 recorded in Q4 2025 but still historically elevated. The most expensive transaction in recent months was a 5-room flat at City Vue @ Henderson (Henderson Road) that transacted at S$1,728,000 in April 2026 — a new island-wide record, surpassing the previous S$1.7M record at SkyTerrace @ Dawson (February 2026).

The Rental Market: Holding Steady

HDB’s Q1 2026 data also covered the rental sub-market. As at end of March 2026, there were 58,598 HDB flats rented out on the open market — down marginally (-0.1%) from the 58,775 rented at end of Q4 2025. The occupancy rental market has broadly plateaued after the 2022–2023 surge, reflecting a more balanced supply-demand dynamic at current rent levels.

Median monthly rents by flat type as at Q1 2026:

| Flat Type | Median Rent (Island-wide) | Highest Town (Est.) | Lowest Town (Est.) |

|---|---|---|---|

| 3-Room | S$2,450/mth | Queenstown ~S$2,800 | Jurong West ~S$2,300 |

| 4-Room | S$2,950/mth | Queenstown ~S$3,200 | Jurong West ~S$2,800 |

| 5-Room | S$3,500/mth | Bishan ~S$3,700 | Jurong West ~S$3,300 |

| Executive | S$3,900/mth | Bedok ~S$4,200 | Jurong West ~S$3,780 |

Worked Example: Seller Navigating the Q1 2026 Market

Consider Ms Chen, a 48-year-old SC who bought a 5-room flat in Punggol in 2021 at S$640,000. Her flat crossed MOP in March 2026. She lists it at S$820,000 based on comparable transaction data from late 2025. By April 2026, the market has softened: similar units in her block are closing at S$795,000–S$805,000. After 6 weeks on market, she accepts S$800,000 — S$20,000 below her initial ask.

At S$800,000, her net proceeds (after clearing the HDB loan balance of S$180,000, CPF refund of S$195,000 including accrued interest, agent commission of S$16,000 at 2%, and legal fees of S$2,500) amount to approximately S$406,500 in cash. This provides her a meaningful deposit for a private condo purchase — the upgrade path that many MOP sellers are pursuing in parallel. The soft landing means she sells at a price below peak 2025 expectations, but still at a substantial premium to her 2021 purchase price.

What Analysts Expect Next

The consensus view among Singapore property researchers as at May 2026 is that the HDB resale market is experiencing a controlled correction rather than a structural downturn. The structural demand drivers — strong household formation, the HDB upgrader pipeline, and the EIP limiting cross-ethnic resale substitution — remain intact. What has changed is the supply side: the 2026 MOP wave adds meaningful listings, and the EC cooling measures introduced on 8 May 2026 (10-year MOP for ECs, removal of Deferred Payment Scheme) are expected to redirect some upgrader demand back toward the resale HDB market as ECs become less attractive for near-term upgraders.

For the full year 2026, many analysts project HDB resale prices to be flat to -1.5% year-on-year — a modest correction rather than a collapse. A steeper correction would require either a significant rise in unemployment (reducing buying capacity) or a sharp increase in interest rates (increasing mortgage costs). Neither scenario appears imminent as at May 2026.

Frequently Asked Questions

Does the 0.6% price dip mean it’s a buyer’s market?

In relative terms, yes — buyers have more negotiating power than they did in 2024 or early 2025. Sellers are taking longer to close deals, and offer-to-transacted-price gaps have widened. However, “buyer’s market” should be contextualised: the overall price level remains historically elevated, and well-located flats in mature estates with strong lease remaining still transact with multiple offers. The softening is most visible in OCR peripheral towns with high MOP supply (Punggol, Sengkang, Tengah) and least visible in established mature estates (Bishan, Toa Payoh, Queenstown, Bukit Timah).

Should I sell my MOP flat now or wait?

This is a personal financial decision that depends on your specific situation — remaining loan quantum, CPF accrued interest, upgrade target, and personal timeline. As a general observation, the supply wave is expected to persist through 2026 and into 2027, meaning if you are not urgently selling, waiting for a Q4 2026 or 2027 window may not materially improve your position. If you plan to upgrade to private property and are concerned about private prices rising faster than HDB prices stabilise, acting sooner may make strategic sense. This should be discussed with a licensed financial adviser and property agent.

How does the MOP supply wave affect HDB rental demand?

As MOP sellers transition to private property or other housing arrangements, some opt to rent out their HDB flat rather than sell, particularly if they can achieve strong rental yields. This adds to the HDB rental supply pool. Simultaneously, new private condo residents who owned the HDB flat they were renting out before upgrading may exit the rental market. The net effect on rental supply is modest and likely balanced; however, specific towns with very high MOP supply (Punggol, Tengah) may see softer rents as more units come onto the rental market in 2026.

Are million-dollar HDB flats still transacting?

Yes. The million-dollar threshold was crossed 165 times in Q1 2026, and the April 2026 record of S$1.728M at City Vue @ Henderson confirms that ultra-premium resale transactions are still occurring. However, the pace of million-dollar transactions appears to be stabilising relative to the 2025 highs. These transactions are concentrated in specific locations: DBSS developments, mature estate point blocks with exceptional views, and flats with very long lease remaining in prime districts. They are the exception rather than the norm.

What is the HDB resale market outlook for H2 2026?

The outlook is cautiously stable with a soft-landing bias. The MOP supply wave will continue adding listings through the year. EC cooling measures (10-year MOP) may modestly redirect some demand to the resale segment. Interest rates, while elevated versus pre-2022 levels, have stabilised. Private-to-HDB downgraders remain limited in number. Most analysts project full-year 2026 HDB resale prices to be flat to slightly negative (-0% to -1.5%), with transaction volumes holding in the 25,000–27,000 range for the full year.

Related Articles

- HDB Million-Dollar Flats Singapore 2026: Where, Why, and Whether One Is Worth Buying

- S$1.728M HDB Resale Record: City Vue @ Henderson, April 2026

- HDB MOP Supply Bumper 2026: How 13,484 Newly-Eligible Flats Are Reshaping Resale

- HDB Resale Procedure Singapore 2026: Step-by-Step from HFE to Key Collection

- Upgrading from HDB to Private Property Singapore 2026: The Complete Roadmap

- Singapore EC Cooling Measures May 2026: 10-Year MOP and What It Means for Buyers

Disclaimer: This article is based on HDB’s 1st Quarter 2026 Public Housing Statistics and publicly available market data. All figures are for general informational purposes only. Rental median figures for individual towns are estimates based on approved applications and may differ from actual advertised rents. This is not financial or investment advice. For decisions relating to HDB resale purchase or sale, consult a licensed property agent (CEA-registered) and a licensed financial adviser. Official data is available at hdb.gov.sg and ura.gov.sg.

0 Comments