TDSR and MSR are the two regulatory ratios the Monetary Authority of Singapore (MAS) uses to decide how much home loan any Singapore buyer can take. Get these wrong in your budgeting, and the pre-approval letter from the bank will come back smaller than the deposit you have already put down on a flat. This guide breaks down what each ratio means, how they stack, and exactly how to calculate your own limit for 2026.

For the official statements, refer to the MAS Notice 645 on TDSR and the HDB financing page.

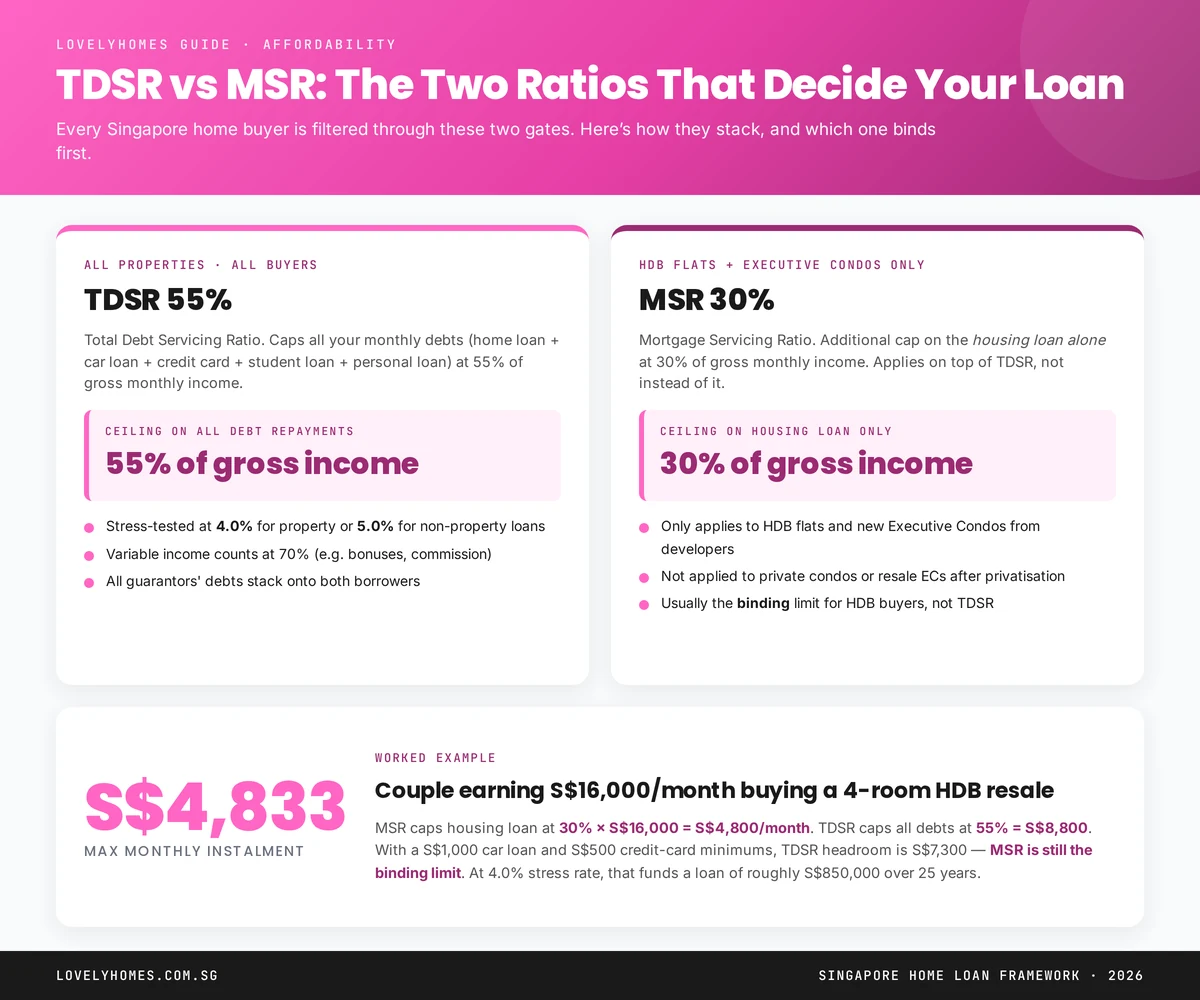

Quick Answer — TDSR & MSR at a glance

- TDSR 55%: All your monthly debts (home loan, car loan, credit card minimums, student loans, personal loans) must stay at or below 55% of your gross monthly income.

- MSR 30%: For HDB flats and new Executive Condos only — your monthly home loan alone must stay at or below 30% of gross monthly income. MSR sits on top of TDSR.

- Stress rate: Both ratios are calculated using a 4.0% stress interest rate, not the actual package rate you are quoted.

- Variable income: Bonuses, commission and rental income count at only 70% of their face value.

- MSR is usually binding for HDB and EC buyers; TDSR is usually binding for private condo buyers.

What is TDSR and Why Does It Matter?

TDSR — Total Debt Servicing Ratio — was introduced in June 2013 as the backbone of Singapore’s sustainable-lending framework. It forces banks to look beyond your home loan and consider every monthly debt commitment you carry. If the sum of all those instalments exceeds 55% of your gross monthly income, the bank cannot extend you any further credit.

In practice, TDSR means that two borrowers on identical salaries can qualify for very different loan sizes if one of them also carries a car loan, a renovation loan, or a large outstanding credit-card balance. Because the ratio is regulatory rather than bank-specific, shopping around will not get you past it.

What counts in the 55% ceiling?

- Housing loans (existing and the new one being applied for)

- Car loans, motorcycle loans, and hire-purchase instalments

- Renovation loans, education loans, personal loans

- Minimum monthly payments on credit cards and overdraft facilities

- Guarantor obligations on another party’s loan — even if you are not the primary borrower

What is MSR and When Does It Apply?

MSR — Mortgage Servicing Ratio — is a narrower, tougher cap that applies only when you are buying:

- An HDB flat (BTO, Sale of Balance Flat, Open Booking, or resale), or

- A new Executive Condominium (EC) directly from a developer, still within its minimum occupation period scheme.

MSR says that your monthly housing loan instalment alone must not exceed 30% of gross monthly income. Unlike TDSR, MSR does not let you compensate by showing you have no other debt — the housing instalment itself cannot breach the 30% line.

Private condos, landed property, and resale ECs after their 10-year privatisation milestone are not subject to MSR. Only TDSR applies. This is one of several reasons why private-property buyers on the same income can often borrow more than HDB buyers.

How Banks Actually Calculate Your Limit

Here is the sequence every MAS-regulated bank follows when you submit a loan application:

- Gross monthly income is totalled. Salary contributes 100%; variable income (bonus, commission, rent, freelance earnings) is haircut to 70%. For rental income, the bank also deducts a vacancy allowance.

- Other monthly debts are added up. This includes a 3% notional minimum on your total credit-card outstandings if you do not pay in full.

- Housing loan instalment is calculated at 4.0% stress rate, over your requested tenure (capped at 30 years for HDB, 35 for private). This is the rate used for ratio maths — not the 2.6% or 2.8% your package may quote.

- Apply TDSR: (All debts + new housing loan at 4.0%) ÷ gross income must be ≤ 55%.

- If HDB/new EC, apply MSR: New housing loan at 4.0% ÷ gross income must be ≤ 30%.

- The loan is sized to the tighter of the two ceilings.

Worked example: couple earning S$16,000 a month

Consider a married couple with combined gross income of S$16,000, a car loan costing S$1,000 a month, and credit-card minimums of S$500 a month. They want to buy a 4-room resale HDB flat.

- TDSR ceiling: 55% × S$16,000 = S$8,800. Existing debts eat S$1,500, leaving S$7,300 of housing-loan headroom.

- MSR ceiling: 30% × S$16,000 = S$4,800.

- Binding limit: MSR, at S$4,800.

- At 4.0% stress rate over 25 years, S$4,800/month supports a loan of approximately S$910,000. At the actual package rate of 2.6%, the real payment on that loan would be around S$4,127/month — giving the couple a S$673 monthly buffer once they move in.

Take away the car loan and the maths does not change — MSR still binds at S$4,800. Take away MSR (i.e. if they were buying a private condo instead), and the binding number becomes S$7,300 of TDSR headroom, translating to roughly a S$1,380,000 loan. Same couple, same income, different rule set, S$470k of extra purchasing power.

Stress Rate: The 4.0% That Quietly Decides Everything

MAS introduced the 4.0% medium-term interest rate floor (officially the “medium-term rate benchmark” or MTRB) in 2022, raising it from 3.5%. The stress rate is higher than virtually any home loan package in the market, which is the point — it builds in resilience against future rate rises.

Because the maths compounds, every 1% of stress-rate uplift cuts affordability by roughly 10%. That is why a package teaser rate of 2.5% does not actually buy you more house than a teaser of 3.0% — both are calculated at 4.0% for TDSR/MSR. What the lower package rate does buy you is cash-flow during the package term.

Variable Income: The 70% Haircut

If you earn a significant bonus, commission or rental income, the 30% haircut matters. Take a relationship manager earning S$10,000 base plus an average S$4,000 a month in commission. Gross looks like S$14,000. TDSR-countable gross is S$10,000 + (0.70 × S$4,000) = S$12,800.

To “grossed-up” income, banks typically require 24 months of commission history (12 for the more flexible ones). First-year hires with fat bonuses but short tenure often cannot count that income at all.

Three Levers to Increase Your Loan Ceiling

- Extend the loan tenure (within the 30/35-year cap) — a longer tenure reduces the monthly instalment under the 4.0% stress calculation, freeing headroom under both ratios.

- Retire consumer debt. Every S$1,000 of car-loan instalment taken off releases exactly S$1,000 of TDSR headroom. For HDB buyers, note this only helps if TDSR (not MSR) is the binding constraint.

- Add a younger co-borrower. Tenure is capped at the weighted average age of all borrowers — bringing in a younger, income-earning co-borrower lifts the tenure ceiling and, by extension, your qualifying loan amount. Be deliberate about the legal and ownership implications before doing this.

Frequently Asked Questions

Does TDSR apply to refinancing?

For owner-occupied residential property, TDSR does not apply to refinancing of an existing loan (this is the “owner-occupier refinancing exemption”). For investment property, TDSR does apply on refinancing, with a debt-reduction plan over three years if you exceed the 55% cap.

Is rental income counted towards TDSR?

Yes. Rental income is haircut to 70% of face value, and banks further deduct a vacancy allowance. A 12-month tenancy agreement is usually required as evidence.

Does my existing home loan count if the property is rented out?

Yes, always. Every housing loan you are servicing — owner-occupied or rented — enters the TDSR calculation on the debt side, regardless of whether the rental income covers it.

Can I get a higher loan if I pay down my credit card before applying?

Yes, provided the payment clears before your bank pulls the credit bureau report. Banks calculate TDSR based on bureau-reported outstandings — pay down early enough for the next monthly report cycle.

What happens if my income drops after I take the loan?

TDSR is tested only at origination and on refinancing of investment property. A mid-loan income drop does not trigger a call on your loan — you simply need to keep paying the contracted instalment.

What to Do Next

TDSR and MSR are the first conversation with any bank, but they are not the only one. Your Loan-to-Value ratio and cash-on-hand position matter just as much. Your logical next reads on LovelyHomes:

- HDB Loan vs Bank Loan: Which Should You Choose? — the choice that comes immediately after knowing your ceiling.

- ABSD Singapore 2026: Complete Guide — the single largest cash cost if this is not your first property.

- Home Loans & Mortgages — all our rate-comparison and refinancing guides in one place.

Disclaimer: This guide is for general information and does not constitute financial advice. TDSR and MSR rules are set and periodically revised by MAS. Always verify current rules at mas.gov.sg and consult a licensed mortgage broker or bank before committing to any property purchase.

0 Comments