Every January, analysts publish a property outlook for the year ahead. Most read more like agent talking-points than analysis. This one tries to do the opposite — state the numbers as they stand at Q1 2026, name the forces that will move them, and flag where consensus is most likely to be wrong.

This is a general-market view, not a valuation of any specific district. For district-level granularity, watch our forthcoming Area Guide series. For the tax and cooling-measure context that underpins all of the below, start with our cooling measures timeline.

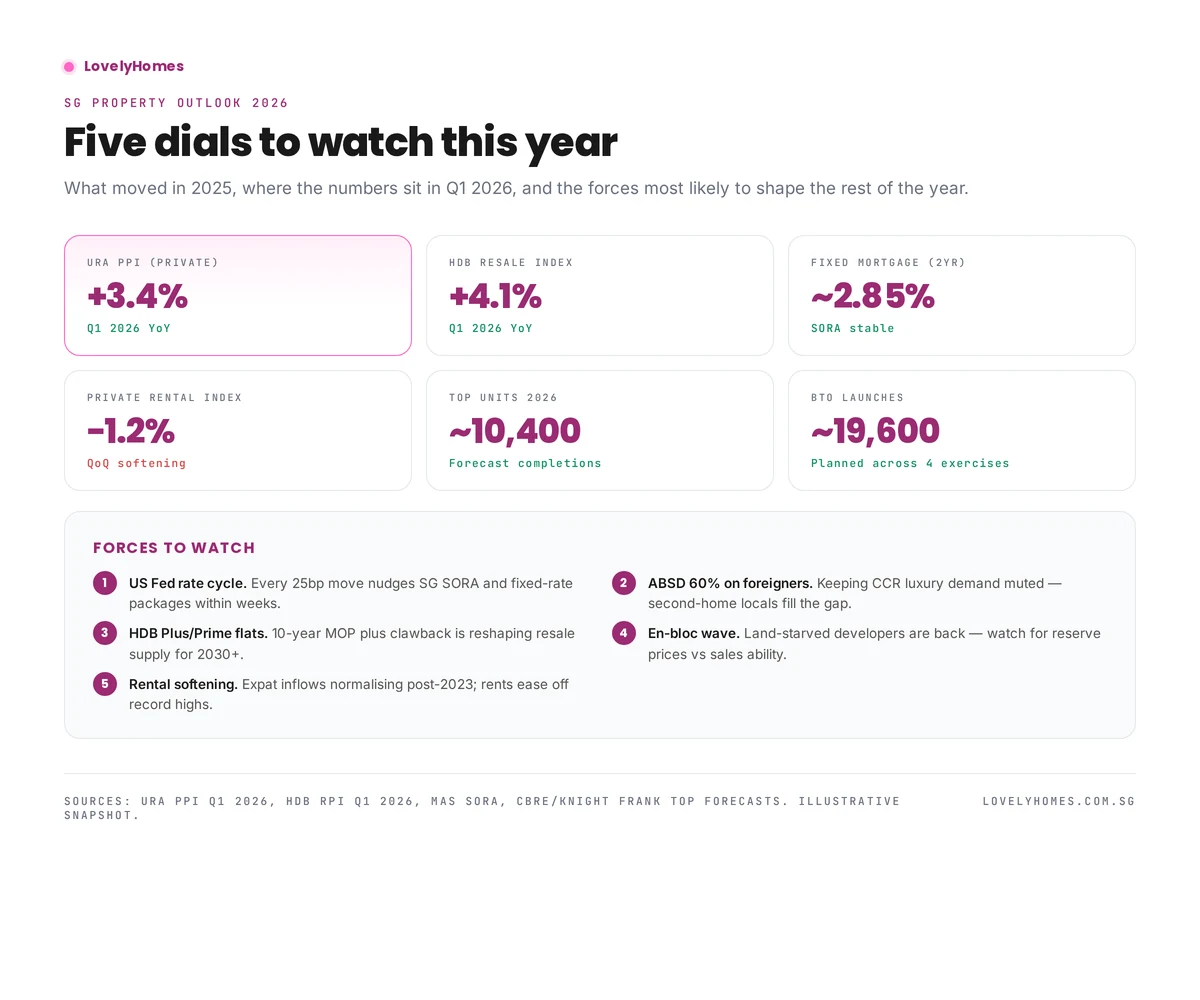

Prices — private and public

URA Private Residential Price Index

URA PPI closed 2025 at record highs. The Q1 2026 flash estimate is +3.4% YoY, with the RCR (city fringe) band leading at roughly +4.6% and CCR lagging at +2.1%. OCR sits in between at +3.9%.

HDB Resale Price Index

HDB RPI is tracking +4.1% YoY — the eighth consecutive quarter of gains, but the pace has decelerated from the double-digit 2022 run. Million-dollar HDB transactions have broadened from central flats into Bishan, Bukit Merah, Queenstown and, increasingly, mature Bidadari and Kallang Whampoa.

Interest rates and financing

3-month compounded SORA has drifted into the 2.5–2.9% range. Fixed packages from local banks are quoting around 2.85% for two-year tenors. That is well below the 2023 peak (~4%) but still meaningfully higher than the 2020–2021 sub-2% era.

Two upshots:

- Refinancing activity is picking up for loans originated at the 2023 peak. See our refinancing guide.

- TDSR bites harder than it did pre-2022. Affordability constraints more than prices are now the dominant buying-decision driver. Our TDSR & MSR guide explains the maths.

Supply coming through

| Segment | Units landing 2026 | Impact |

|---|---|---|

| Private residential TOP | ~10,400 | Keeps rental supply refreshed |

| EC TOP | ~3,800 | HDB upgraders hand back resale flats |

| BTO launches (planned) | ~19,600 flats | Large Plus/Prime share |

Rental market

After the extraordinary 2022–2023 surge (+25% to +30% YoY at the peak), rents are normalising. Q4 2025 URA rental index was down 1.2% QoQ. Expect a sideways-to-softer 2026, especially for older non-integrated condos as expat renters rotate into newer stock.

Five forces shaping the rest of 2026

- US Fed rate path. Every 25bp shift flows through SORA and fixed packages in weeks.

- The 60% foreigner ABSD. Kept CCR luxury flat. Any softening would re-ignite CCR transaction volumes.

- HDB Plus / Prime supply. 10-year MOP plus subsidy clawback is reshaping the 2030+ resale pool.

- En-bloc cycle. Developers are land-starved; reserve prices that reflect cooling measures may finally clear.

- Rental compression. Yields moderate as wages normalise; investor maths re-anchors on capital appreciation, not cash flow.

Frequently asked questions

Will prices fall in 2026?

Base case: no. Prices grind higher at low single digits. Downside case: if the Fed holds rates longer than expected and supply lands faster, a flattish 2H 2026 is plausible.

Is now a good time to buy?

Depends on your horizon and cash flow. Owner-occupier with stable income: time in market beats timing the market. Investor leveraging up: TDSR-constrained — stress-test your affordability at a 4% rate.

Which segment looks strongest?

City-fringe RCR continues to be the sweet spot for owner-occupiers. OCR near MRT interchanges wins on yield.

This guide is for general information only and is accurate as of April 2026. Singapore property rules, taxes and cooling measures change frequently — always verify current figures with URA, IRAS, HDB or a licensed professional before committing. LovelyHomes is not a financial, legal or tax advisor.

0 Comments