Property decoupling is the restructuring of joint ownership between spouses so that one of them becomes the sole owner of the existing property, freeing the other to buy a second home at first-timer ABSD rates (0% for SCs, 5% for PRs). In 2026, with ABSD at 20% for SCs on a second property, the savings can be substantial — but HDB flats cannot be decoupled except in divorce, and IRAS scrutinises obviously tax-avoidance arrangements.

This guide walks through how decoupling works mechanically, the costs involved, a worked example, and when IRAS is likely to push back.

Quick Answer — Decoupling at a Glance

- Who: Joint owners of a private property (spouses typically).

- What: One party transfers their share to the other so that the other becomes sole owner.

- Why: The transferring party is now property-free and can buy a second home at first-timer ABSD rates.

- Cost: BSD on buy-over (~S$20–50k), legal fees (~S$4–6k), possibly CPF refund.

- HDB flats: Cannot be decoupled except under divorce court order.

- IRAS risk: If the arrangement is clearly contrived, IRAS can reassess as tax avoidance.

How Decoupling Works Mechanically

There are two legal pathways to decouple a property:

1. Part-purchase

One spouse buys the other spouse’s share via a sale and purchase agreement. The price must be at market value (to satisfy IRAS), and Buyer’s Stamp Duty is paid on the share being transferred. If there is a mortgage, the buying spouse typically refinances the loan in their sole name.

2. Transfer-of-ownership

Less common and typically used only in genuine gift scenarios or divorce. The share is transferred via a Deed of Transfer. Stamp duty still applies based on the market value of the share.

The common pathway is Part-purchase, because it creates a clear arms-length commercial record (helpful if IRAS later asks questions).

Costs of Decoupling

Decoupling a typical S$1.5m condo with joint ownership structured as 50:50:

| Component | Amount |

|---|---|

| Property value | S$1,500,000 |

| Share being transferred (50%) | S$750,000 |

| BSD on S$750,000 transfer | ~S$17,100 |

| Legal fees (2 parties, separate lawyers) | S$4,000–S$6,000 |

| Mortgage refinancing costs | S$1,000–S$3,000 |

| CPF refund (to transferring spouse’s CPF) | Full principal + accrued interest |

| Total cost (excluding CPF flows) | ~S$22,000–S$26,000 |

The CPF refund is a cash flow, not a cost — the transferring spouse’s CPF OA is topped up with their original contributions plus 2.5% annual accrued interest. They can then redeploy that CPF for the second property purchase.

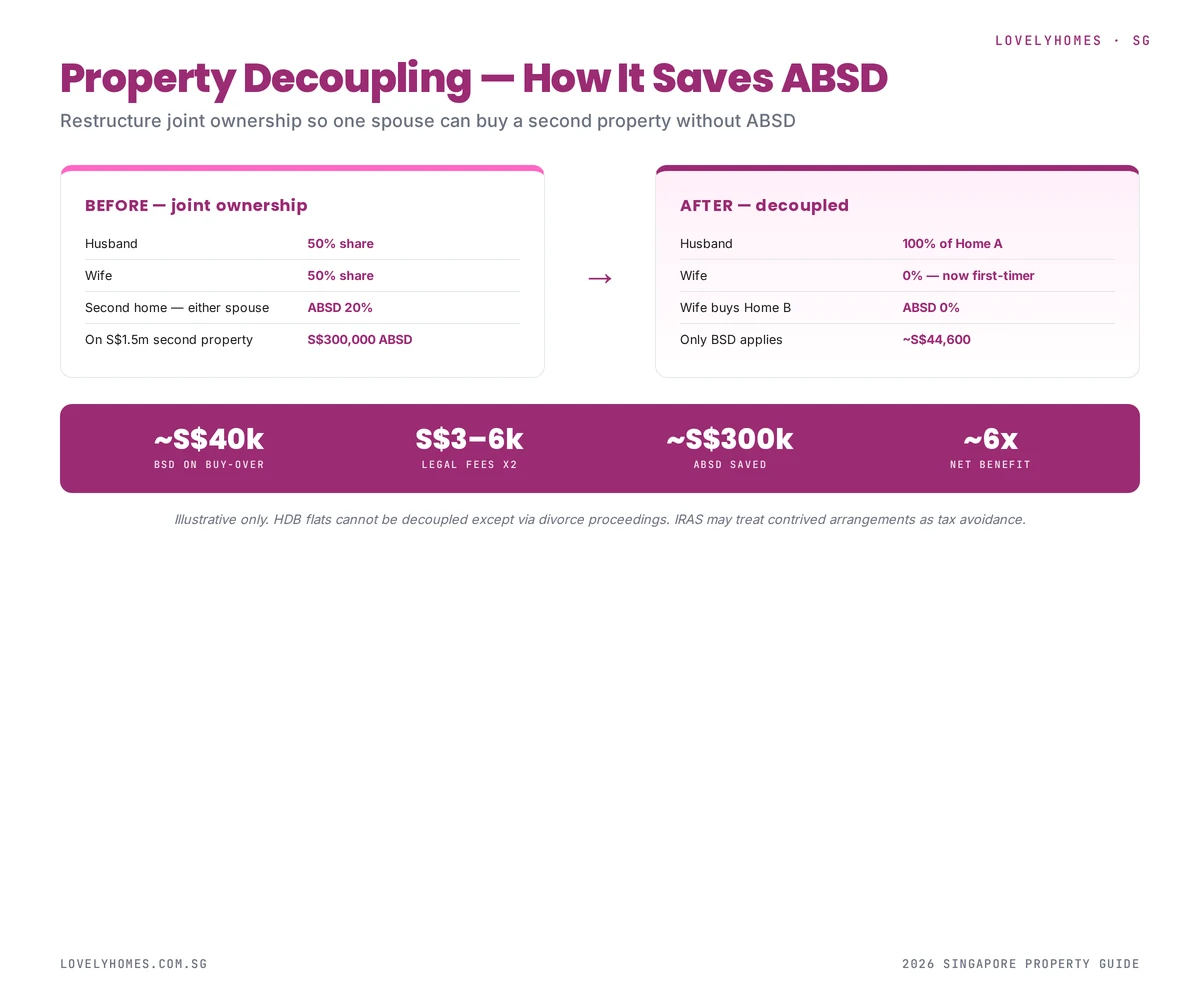

Worked Example: Buying a S$1.5m Second Property

A married couple owns a S$2.5m Orchard-area condo jointly. They want to buy a S$1.5m investment unit.

Without decoupling

- Both already own property → ABSD 20% applies to the second purchase

- ABSD on S$1.5m = S$300,000

- Plus BSD on S$1.5m = S$44,600

- Total stamp duty: S$344,600

With decoupling

- Husband buys out wife’s 50% share of the Orchard condo → BSD on S$1.25m = ~S$35,600

- Plus legal fees and refinancing: ~S$6,000

- Wife now has zero property → first-timer status

- Wife buys the S$1.5m second property → ABSD 0%, BSD only

- BSD on S$1.5m = S$44,600

- Total stamp duty + decoupling costs: S$86,200

Net saving

S$344,600 – S$86,200 = S$258,400 saved.

HDB Flats Cannot Be Decoupled

Since 2016, HDB explicitly prohibits decoupling of HDB flats except under court order (usually in the context of divorce). The rule was introduced specifically to close the ABSD-avoidance loophole that decoupling had opened for HDB flat owners looking to buy private property.

If you own an HDB flat and want to buy a private unit without paying ABSD, the only legitimate paths are:

- Sell the HDB first, buy the private unit as a first-timer (subject to MOP being fulfilled)

- Dispose of HDB within 6 months of buying the private unit — the ABSD Remission Scheme refunds the ABSD you initially paid

IRAS Scrutiny: When Decoupling Becomes Tax Avoidance

Decoupling is legitimate when it reflects a genuine change in ownership. IRAS begins asking questions when the arrangement is obviously contrived for tax savings alone. Red flags include:

- Back-to-back decoupling and second purchase — decouple today, OTP tomorrow

- The transferring spouse had no means to be a genuine buyer (income too low to have qualified for the original loan alone)

- Multiple decouplings in sequence — decouple to buy property A, decouple again to buy property B

- Artificial “loan” structures where the buying spouse’s share payment is obviously funded by the transferring spouse

Under the Stamp Duties Act and the general anti-avoidance provision, IRAS can reassess the arrangement as tax avoidance and claw back the saved ABSD with a surcharge. The 99-to-1 arrangement scrutinised in 2023–2024 was a related pattern — see our 99-to-1 guide.

Is Decoupling Still Worth It in 2026?

For genuine cases — where one spouse actually wants to become a sole owner, and the other actually has the income and savings to buy a second property independently — yes. The ABSD savings on a mid-market second property (S$1m–S$2m) typically far exceed the cost of decoupling by a factor of 6 to 10.

For arrangements that are transparently tax-motivated — where the transferring spouse has no genuine interest in becoming a sole property owner — the risk calculus has changed. IRAS has shown a real willingness to reassess such arrangements, and the 1.5x clawback means a failed attempt costs more than just paying the ABSD upfront.

Practical Considerations

- Timing: Complete the decoupling fully before the second property’s OTP. Back-to-back transactions draw IRAS attention.

- Separate legal counsel: Each spouse should use a different lawyer. Joint counsel can be a red flag.

- Market-value pricing: The share must be sold at market value, supported by a professional valuation.

- Mortgage servicing: The buying spouse must independently qualify for the refinanced loan in their sole name.

- CPF flows: The transferring spouse’s CPF must be refunded in the correct amount, including accrued interest.

FAQ — Decoupling 2026

Can I decouple a condo I own with my parent?

Yes, the same mechanisms apply (Part-purchase or Transfer-of-ownership). The stamp duty rates depend on the parent’s relationship, and IRAS may look more closely if the decoupling pattern is unusual.

Does decoupling affect the existing bank loan?

Yes. The bank will need to refinance the loan in the sole name of the buying spouse. If the buying spouse cannot service the full loan independently, decoupling is not viable.

How long does decoupling take?

Typically 8–12 weeks from engagement to completion. Both lawyers, the bank, and CPF must all coordinate.

Can unmarried partners decouple?

They can, but the original joint ownership would need to have had a clear commercial basis (co-investors, for instance). IRAS is more likely to scrutinise an unmarried joint ownership that decouples immediately before a second purchase.

What if IRAS does reassess?

Expect the original ABSD saved plus a 50% surcharge (1.5x clawback). On our S$300k ABSD example, that would be S$450k payable — plus interest and legal costs.

Disclaimer: This is general guidance, not legal or tax advice. Decoupling has significant tax, legal and CPF consequences specific to your household. Always engage a qualified conveyancing lawyer and a tax advisor before proceeding.

0 Comments