Quick Answer: Singapore Bridging Loan 2026 at a Glance

- What it is: A short-term loan that bridges the timing gap between buying a new property and receiving sale proceeds from your existing one. It covers the shortfall when both transactions overlap.

- Who needs it: Typically upgraders who sign an Option to Purchase (OTP) on a new property before completing the sale of their current HDB flat, condo, or landed home.

- Loan quantum: Usually up to 120% of the sale price of the property being sold, capped by the bank’s assessment. The amount typically covers the gap between the new purchase price and your available cash and CPF savings.

- Interest rate: Singapore banks typically price bridging loans at 5.0–6.5% per annum (as at Q1 2026), charged on the drawn-down amount on a daily rest basis. This is significantly higher than standard mortgage rates of 2.8–3.5%.

- Maximum term: Most banks limit bridging loans to 6 months, with some allowing up to 12 months by exception. They are designed to be short-term instruments, not medium-term financing.

- Repayment: The bridging loan is repaid in full from the sale proceeds of your existing property at completion. Interest may be capitalised (added to the loan balance) or paid monthly, depending on the bank’s product structure.

- TDSR applies: The bridging loan amount and interest must be included in the Total Debt Servicing Ratio (TDSR) calculation alongside your new home loan, which can affect the amount you are eligible to borrow for the new property.

- Alternative: Selling your current property first before buying the new one eliminates the need for a bridging loan entirely — but requires temporary accommodation and precise transaction timing.

What Is a Bridging Loan in Singapore Property?

A bridging loan (sometimes called a bridging facility) is a short-term credit instrument provided by Singapore banks to property buyers who need to complete the purchase of a new property before the sale of their existing one has been finalised. The loan “bridges” the financing gap — giving you access to the equity locked in your current property so that you can meet the payment obligations on your new home without waiting for completion of the sale.

In Singapore’s property market, bridging loans arise most commonly in the upgrader scenario: an owner-occupier who is selling their HDB flat or private condo and simultaneously buying a larger or more expensive replacement home. Because Singapore’s property transactions involve a sequence of deposits, Option exercises, and completion dates that cannot always be synchronised precisely, it is common for buyers to need short-term funds to plug the gap between “paying for the new place” and “receiving money from selling the old one”.

The Monetary Authority of Singapore (MAS) does not publish specific rules governing bridging loans as a product category, but banks are required to apply the Total Debt Servicing Ratio (TDSR) framework to all property-related credit facilities. This means the bridging loan reduces the amount you can borrow on your new home mortgage, and the combined debt burden must not exceed 55% of your gross monthly income.

When Do You Need a Bridging Loan?

The need for a bridging loan arises whenever you are committed to buying before you have received the proceeds from your sale. In practice, the scenarios that most commonly trigger a bridging loan in Singapore are:

Scenario 1 — HDB upgrader buying before HDB flat is sold. You find a private condo you want to buy. You grant the OTP, which starts the 21-day clock. Your HDB flat has not yet been sold. The CPF and proceeds you plan to use for the new downpayment are still tied up in your HDB flat. A bridging loan covers the downpayment shortfall until your HDB sale completes (typically 8–16 weeks after OTP exercise).

Scenario 2 — Private upgrader with overlapping completion dates. You are selling your existing condo (completion in Month 6) and buying a new condo (completion in Month 4). The two-month timing mismatch means you need bridging to cover the new home’s completion before your old one is sold.

Scenario 3 — New launch purchase with progressive payment. For some uncompleted private condominiums, the S&P stage payments fall due before the buyer’s existing property sale completes. Bridging covers the interim stage payments.

In each case, the bridging loan is a temporary instrument. It is never designed to be a permanent part of your capital structure — it should be repaid in full from sale proceeds as soon as they arrive.

How Does a Bridging Loan Work in Singapore?

Here is the typical process a buyer goes through when arranging a bridging loan alongside a new home purchase:

- Apply to your bank — usually the same bank providing your new home loan. Most banks will only offer a bridging loan if they are also lending you the mortgage on the new property. You will need to provide the signed OTP (or S&P Agreement) for both the property you are buying and the property you are selling.

- Bank assesses quantum and TDSR — the bank will confirm (a) the maximum bridging quantum (typically up to the lower of the expected sale proceeds or 120% of the existing property’s market value), and (b) whether the combined TDSR — new mortgage + bridging loan — passes the 55% cap. If the combined TDSR fails, the bank will reduce either the bridging quantum or the new home loan accordingly.

- Bridging loan is drawn down at the point when the funds are needed — usually at completion of the new purchase or at the OTP exercise stage requiring a cash deposit.

- Interest accrues daily on the outstanding bridging balance, typically at 5.0–6.5% per annum. Some banks allow interest to be capitalised (added to the loan balance and settled at repayment); others require monthly interest servicing.

- Bridging loan is repaid when the sale of the existing property completes and the proceeds are disbursed. The law firm acting in the sale will typically direct the net sale proceeds to discharge the bridging loan before releasing any balance to the seller.

Bridging Loan vs Selling First: Which Is Better?

The most important decision an upgrader makes is not “which bank to use for the bridging loan” — it is whether to use a bridging loan at all. The sell-first strategy eliminates the bridging cost entirely, but introduces its own set of trade-offs.

| Factor | Sell First, Then Buy | Buy First (Bridging Loan) |

|---|---|---|

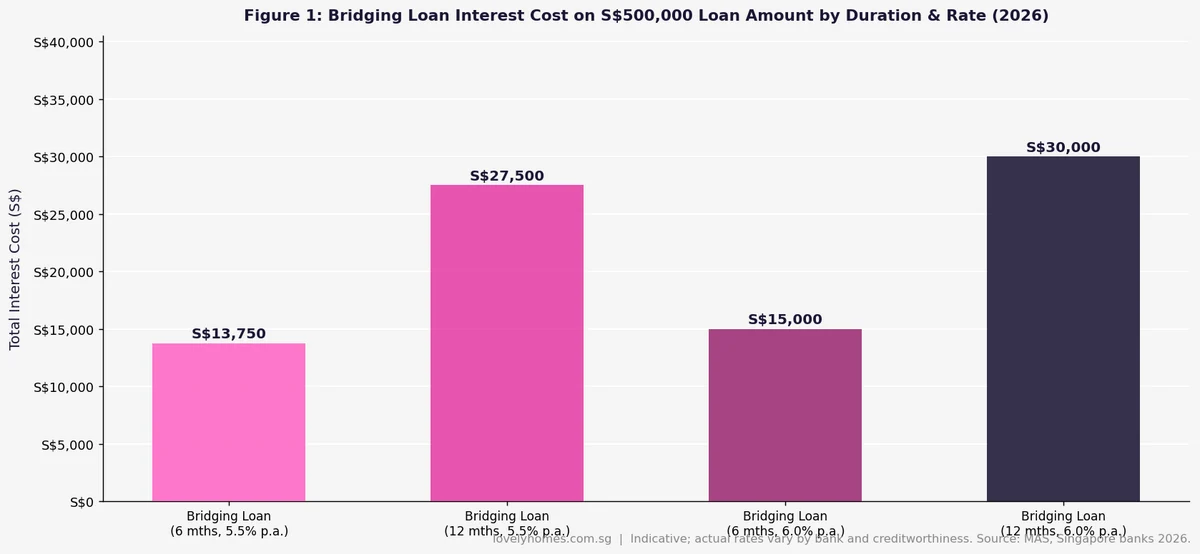

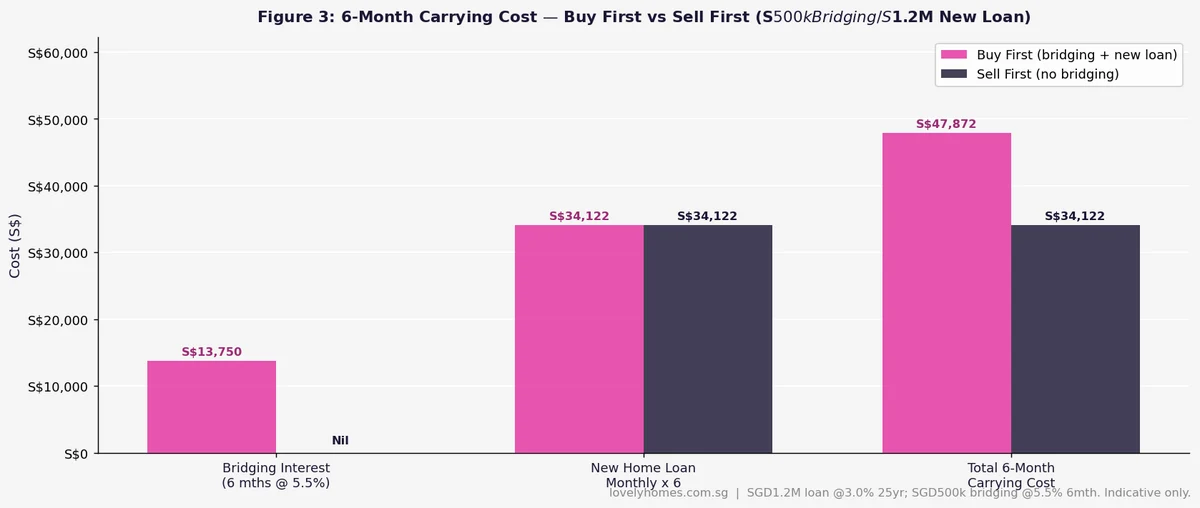

| Bridging interest cost | Nil | S$13,750–S$30,000 on S$500k for 6–12 mths |

| ABSD risk | None — only one property at OTP date | 20% ABSD if OTP on new home before HDB/condo sold |

| Negotiating position | Strong — you are a cash buyer with no chain | Weaker — subject to bridging approval and old sale completing |

| Temporary accommodation | Required (rent or stay with family during transition) | None needed — move from old to new directly |

| Market risk | New property price may rise while you wait to buy | New property secured; old property sold in current market |

| Stress and timing | Can negotiate purchase at leisure | Time pressure from both transaction deadlines simultaneously |

| Suitable for | Buyers with flexible accommodation options; rising market | Buyers wanting seamless move; found specific property they want |

The ABSD trap is the most important consideration in the buy-first scenario. If you are a Singapore Citizen and you sign an OTP on a new property while still owning your HDB flat or condo, you technically hold two properties at the OTP date. This triggers 20% ABSD on the new purchase for SCs (30% for SPRs on a second property). You can claim back the ABSD under the Married Couple Remission — but only if you complete the sale of the existing property within six months of the new purchase completion (or TOP/CSC date for uncompleted units). Miss the six-month window, and the ABSD is forfeited. Our full ABSD Singapore 2026 guide covers the remission conditions in detail.

Worked Example: The Tans — HDB Upgraders Using a Bridging Loan

Profile: Mr & Mrs Tan, Singapore Citizens, joint gross income S$14,500/month. They own a fully paid-up Tampines 5-room HDB flat (est. market value S$920,000, no outstanding HDB loan, CPF accrued interest to refund approx. S$180,000). They wish to buy a 3-bedroom 99-year leasehold condo in Bedok for S$1,650,000.

Transaction plan: They sign an OTP for the new Bedok condo first (grants on 1 June 2026). They intend to sell the HDB flat, estimated completion 15 August 2026. The bridging period is approximately 2.5 months.

ABSD: The Tans hold two residential properties at the OTP date for the Bedok condo. ABSD of 20% on S$1,650,000 = S$330,000 is payable within 14 days. They apply for the SC Married Couple Remission, planning to complete the HDB sale within 6 months of Bedok condo completion (expected December 2026). If remission is granted, S$330,000 is returned; if the HDB sale slips past the 6-month window, the S$330,000 is forfeited.

BSD on new condo: 1%×S$180k + 2%×S$180k + 3%×S$640k + 4%×S$500k + 5%×S$150k = S$1,800 + S$3,600 + S$19,200 + S$20,000 + S$7,500 = S$52,100.

New condo bank loan (LTV 75%): Maximum S$1,237,500. Minimum 5% cash = S$82,500; remaining 20% (S$330,000) via CPF OA.

CPF available: After CPF accrued interest refund of S$180,000, the Tans expect approximately S$310,000 in CPF OA from the HDB sale — but this only arrives at HDB completion in August. For the June new purchase, their current CPF OA balance is S$95,000. Shortfall for 20% cash-or-CPF at June completion = S$330,000 – S$95,000 = S$235,000 bridging required.

Bridging loan: S$235,000 at 5.5% per annum for approximately 2.5 months = S$235,000 × 5.5% × (2.5/12) ≈ S$2,698 interest. This is the cost of the bridging loan — relatively modest at this quantum and short duration.

New home loan monthly repayment: S$1,237,500 at 3.0% over 25 years ≈ S$5,868/month. TDSR = S$5,868 ÷ S$14,500 = 40.5% — well within the 55% cap. The bridging loan itself adds minimal TDSR impact given its short remaining term at the time of the new home loan drawdown.

HDB sale net proceeds: S$920,000 – CPF accrued interest refund S$180,000 = est. S$740,000 (before conveyancing costs, agent commission and any CPF OA refund offset). The net cash/CPF from the HDB sale repays the bridging loan and tops up the Tans’ CPF OA for the new condo.

This example is illustrative. CPF calculations depend on actual contribution history; ABSD remission requires strict compliance with timelines; engage a conveyancing lawyer before signing any OTP.

Interest Rates and Fees: What Singapore Banks Charge in 2026

Bridging loan interest rates are not regulated individually — each bank sets its own pricing, typically benchmarked against the prime lending rate or a fixed spread. As at Q1 2026, the indicative rates from major Singapore banks are:

- DBS / POSB: Approximately 5.5% per annum, daily rest, on the drawn-down outstanding balance.

- OCBC: Approximately 5.75–6.0% per annum, depending on loan quantum and customer relationship tier.

- UOB: Approximately 5.5–6.0% per annum.

- Standard Chartered, HSBC, Maybank: Typically 5.5–6.5% per annum for bridging, priced on a case-by-case basis.

In addition to the interest, some banks charge a processing or commitment fee of 0.5–1.0% of the bridging quantum, though this is waived by some banks as part of a combined new home loan package. There is no early repayment penalty on bridging loans — redeeming early as soon as sale proceeds arrive is standard practice and incurs no penalty.

Always compare the all-in cost (interest + fees) rather than the headline rate, and clarify whether interest is capitalised or must be serviced monthly. Monthly interest servicing on a S$500,000 bridging loan at 5.5% per annum = S$500,000 × 5.5% ÷ 12 ≈ S$2,292 per month — a significant additional monthly cash outflow on top of the new mortgage.

TDSR Implications: How Bridging Loans Affect Your Borrowing Capacity

This is the most frequently misunderstood aspect of bridging loans. Under the MAS TDSR framework, all outstanding debt obligations must be counted when calculating your maximum new home loan. This includes the bridging loan.

In practice, most banks assess TDSR at the point of new home loan approval by considering the bridging loan as a temporary debt that will be retired at the old property’s sale completion. Banks typically apply a “stressed” annualised interest rate (usually at or slightly above the actual bridging rate) to the bridging outstanding balance to calculate a monthly debt equivalent. This monthly equivalent is added to your projected new home mortgage payment, and the combined total must be below 55% of gross income.

The practical impact: if you are borrowing close to the TDSR limit on your new mortgage, a bridging loan may push you over the threshold. In such cases, the bank will either reduce the new home loan quantum or decline the bridging facility. This is a key reason why property lawyers and mortgage brokers recommend getting in-principle approval for the combined new home loan and bridging loan before signing any OTP on the new property.

What Might Change: Bridging Loan Policy Outlook 2026

This section represents forward-looking analysis only and should not be taken as advice.

The MAS has not signalled any specific changes to bridging loan regulation in 2026. However, the broader property cooling measure landscape — particularly the 20% ABSD for SC second-property purchases and the six-month remission window — creates ongoing policy interaction with bridging loans. Any extension of the ABSD remission window (currently six months) would reduce the timing risk for upgraders using bridging loans and might marginally increase demand for such facilities.

Conversely, if MAS tightens the TDSR methodology to apply higher stress rates to bridging loan obligations, the maximum new home loan quantum for borrowers using bridging would fall further. This is speculative at this stage but worth monitoring if you are planning a mid-2026 transaction.

Frequently Asked Questions

Can I use CPF to repay a bridging loan?

No. CPF Ordinary Account (OA) funds can only be used for specific approved purposes: purchasing a residential property, servicing the monthly mortgage instalment on that property, or paying stamp duties. Repaying a bridging loan directly from CPF is not an approved use. However, when your existing property (the one being sold) completes its sale, your solicitors will refund any CPF OA amounts you previously drew from that property back to your CPF OA, with accrued interest at 2.5% per annum. Those refunded CPF funds can then be applied toward the new property’s mortgage or downpayment, which indirectly allows you to reduce the amount of cash needed from your bank loan or bridging facility. For the detailed CPF rules on property purchases, see the CPF Board’s official guidelines.

What happens if my existing property sale falls through while I have an outstanding bridging loan?

This is the primary risk of the buy-first strategy. If your sale falls through after the new purchase has completed, you are left holding two properties with no sale proceeds to repay the bridging loan. In that scenario, the bridging loan continues to accrue interest at 5.0–6.5% per annum until a new buyer is found and the sale completes. Additionally, you may be holding two properties simultaneously — triggering 20% ABSD on the newer purchase (for SCs) unless you already paid it and are waiting for remission. You would need to refinance the bridging loan as a longer-term mortgage, which requires bank approval and may not be granted at favourable rates. This scenario underlines why most financial advisers recommend the sell-first sequence for buyers who do not have strong cash reserves to cover an extended bridging period if plans go awry.

How long does it take to get a bridging loan approved in Singapore?

Most major Singapore banks can approve a bridging loan in principle within 2–5 business days, provided you submit complete documentation: income documents (latest 3 months’ payslips or 2 years’ NOA for self-employed), the signed OTP or S&P Agreement for both the purchase and sale properties, and the latest CPF Statement showing your OA balance. Some banks require the new home loan approval to be finalised in parallel with the bridging approval. In practice, most upgraders apply for the combined facility (new home loan + bridging) at the same time, which can take 1–2 weeks for formal approval. Always apply at least 3 weeks before the payment obligation falls due.

Do HDB sellers qualify for a bridging loan?

Yes, if they are simultaneously buying a private property. HDB sellers who are selling their flat and purchasing a private residential property can apply for a bridging loan from a bank, provided the bank also approves the new private property mortgage. Note that HDB resale transactions involving the Central Provident Fund Board typically have a completion timeline of around 8–16 weeks after exercising the OTP, which determines how long the bridging facility needs to remain outstanding. HDB sellers cannot use an HDB Concessionary Loan for a private property purchase — only bank loans apply to private residential transactions.

Is a bridging loan the same as a renovation loan or a personal loan?

No. A bridging loan is a property-secured short-term credit facility specifically designed to cover the timing gap in a simultaneous sale-and-purchase transaction. A renovation loan is an unsecured or property-secured loan used to fund home improvements, typically capped at S$30,000–S$200,000 and repaid over 1–5 years. A personal loan is unsecured, typically carries a higher effective interest rate (6–12% per annum), and is not tied to a specific property transaction. Of the three, only the bridging loan and the renovation loan (if secured) fall within the MAS TDSR framework as property-related credit; a personal loan is counted separately under the broader all-debt-obligation test. Never use a personal loan as a substitute for a bridging loan on a property transaction — the higher cost and the TDSR double-counting will almost always make your financial position worse.

Can I use a bridging loan to buy an investment property I do not intend to sell my current home for?

A bridging loan is specifically designed for the scenario where an existing property is being sold and the proceeds are needed to fund a replacement purchase. Banks will not issue a bridging loan simply because a buyer wants short-term leverage on a second investment property without an underlying sale. For buyers seeking to fund an investment property purchase while retaining their existing home, the standard instruments are a standard bank mortgage (subject to LTV and TDSR) or, for short-term portfolio financing, specialist property investor loans. The 20% ABSD (for SCs) and 30% ABSD (for SPRs) on second properties make leveraged second-property investment a high-bar exercise in Singapore regardless of the loan type.

Click anywhere outside to close

0 Comments