Buying or selling property in Singapore involves more than the purchase price and stamp duties. Every transaction — whether an HDB resale flat, a private condominium, or a landed house — requires a conveyancing lawyer to handle the legal transfer of ownership. These legal fees, plus the various disbursements that lawyers incur on your behalf, form part of the total transaction cost that every buyer and seller must budget for.

In Singapore, conveyancing is a regulated area of legal practice. The Law Society of Singapore previously prescribed a fixed fee scale, but that scale was abolished in 2009. Lawyers now charge based on the complexity of the transaction and market rates, though most firms price competitively within a fairly predictable band. This guide explains what conveyancing lawyers do, what you will pay, and how to manage the costs effectively in 2026.

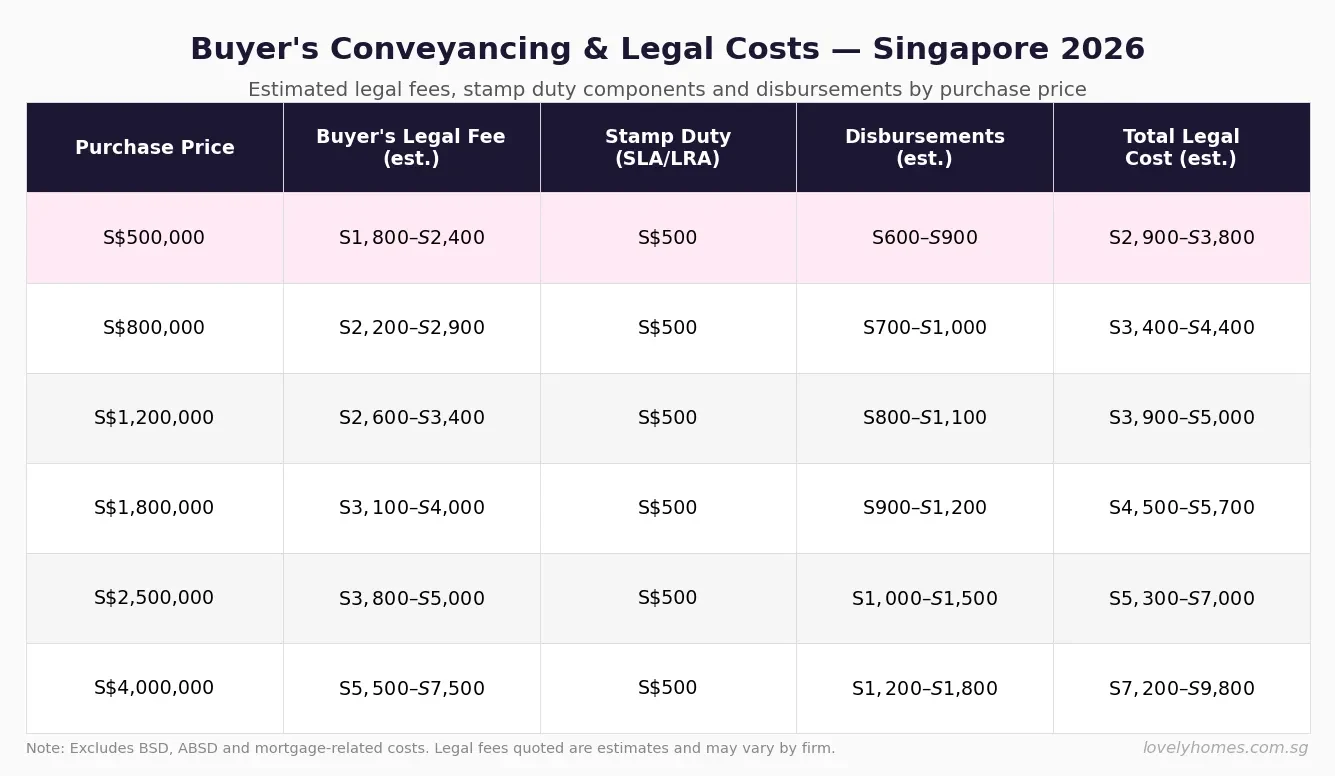

- Buyer’s conveyancing fees for a S$1.5M private property typically range from S$2,800 to S$4,500 (legal fee) plus S$800–S$1,200 in disbursements.

- Seller’s legal fees are generally lower — S$2,000 to S$3,500 plus disbursements of S$600–S$1,000.

- For HDB resale flats, both buyer and seller pay separately for their own lawyers; HDB sets a guide for solicitors’ fees.

- Disbursements are fixed government and third-party charges — Caveat filing, SLA searches, stamp duty lodgement — totalling S$400–S$1,000 for most transactions.

- The conveyancing process from Option to Purchase (OTP) exercise to legal completion typically takes 8–12 weeks for private property and 12–16 weeks for HDB resale.

- You may use the same law firm as the bank providing your mortgage loan (called an “acting for both” arrangement) to reduce total costs — though this is subject to the firm’s conflict-of-interest policies.

- Buyers must pay Buyer’s Stamp Duty (BSD) within 14 days of exercising the OTP; ABSD (if applicable) is due at the same time.

- GST at the prevailing rate (9% as at 2026) applies to lawyers’ professional fees but not to government disbursements.

What Is Conveyancing and Why Do You Need a Lawyer?

Conveyancing is the legal process by which ownership of a property is transferred from seller to buyer. In Singapore, this is a mandatory process overseen by qualified solicitors admitted to the Singapore Bar. Unlike some jurisdictions where buyers and sellers may self-represent, Singapore law requires a practising solicitor to execute the conveyancing documents, lodge the transfer with the Singapore Land Authority (SLA), and handle the settlement of funds.

For the buyer, the conveyancing lawyer: reviews the OTP and Sale and Purchase Agreement (SPA), conducts title searches to confirm ownership and encumbrances, lodges a caveat on the property title, handles stamp duty payment on your behalf, liaises with the bank (if you have a mortgage) to coordinate the mortgage documentation and drawdown, and oversees the completion — handing over the title in exchange for the purchase price.

For the seller, the conveyancing lawyer: reviews the OTP, liaises with the buyer’s solicitor, discharges any existing mortgage on the property, handles the discharge of the existing caveat, and receives and distributes the sale proceeds — repaying the outstanding loan to the bank and CPF (if CPF monies were used), and releasing the net balance to you.

How Conveyancing Fees Are Structured

Since the abolition of the prescribed scale in 2009, Singapore law firms price conveyancing work in one of three ways: a fixed fee (most common for straightforward residential transactions), an ad valorem fee (a percentage of the purchase price, typically 0.1–0.25%), or an hourly rate (rare for standard residential work). The legal fee is subject to 9% GST.

On top of the professional fee, the lawyer will charge disbursements — third-party costs incurred on your behalf. These are typically passed through at cost (no markup) and are not subject to GST. Common disbursements include: SLA title search fees, caveat registration, stamp duty lodgement fee, HDB resale levy search (if applicable), legal requisitions to various government bodies (URA, LTA, PUB, NEA, SLA, ACRA), and the Electronic Payment fee for the Legal Practitioners Fidelity Fund (LPFF).

| Fee Component | Typical Range | Chargeable? | GST? |

|---|---|---|---|

| Professional (legal) fee — buyer | S$1,800–S$7,500 (price-dependent) | Yes | Yes (9%) |

| Professional (legal) fee — seller | S$1,500–S$5,000 (price-dependent) | Yes | Yes (9%) |

| SLA title search | S$30–S$60 per search | Disbursement | No |

| Caveat lodgement | S$64.45 | Disbursement | No |

| Stamp duty lodgement / e-stamping | S$10–S$25 | Disbursement | No |

| Government requisitions (URA, LTA, etc.) | S$200–S$400 | Disbursement | No |

| LPFF contribution | S$100 (standard) | Disbursement | No |

| Mortgage documentation (if bank appoints same firm) | S$800–S$2,500 | Yes (bank-to-borrower) | Yes (9%) |

The Full Picture: Transaction Costs Beyond Legal Fees

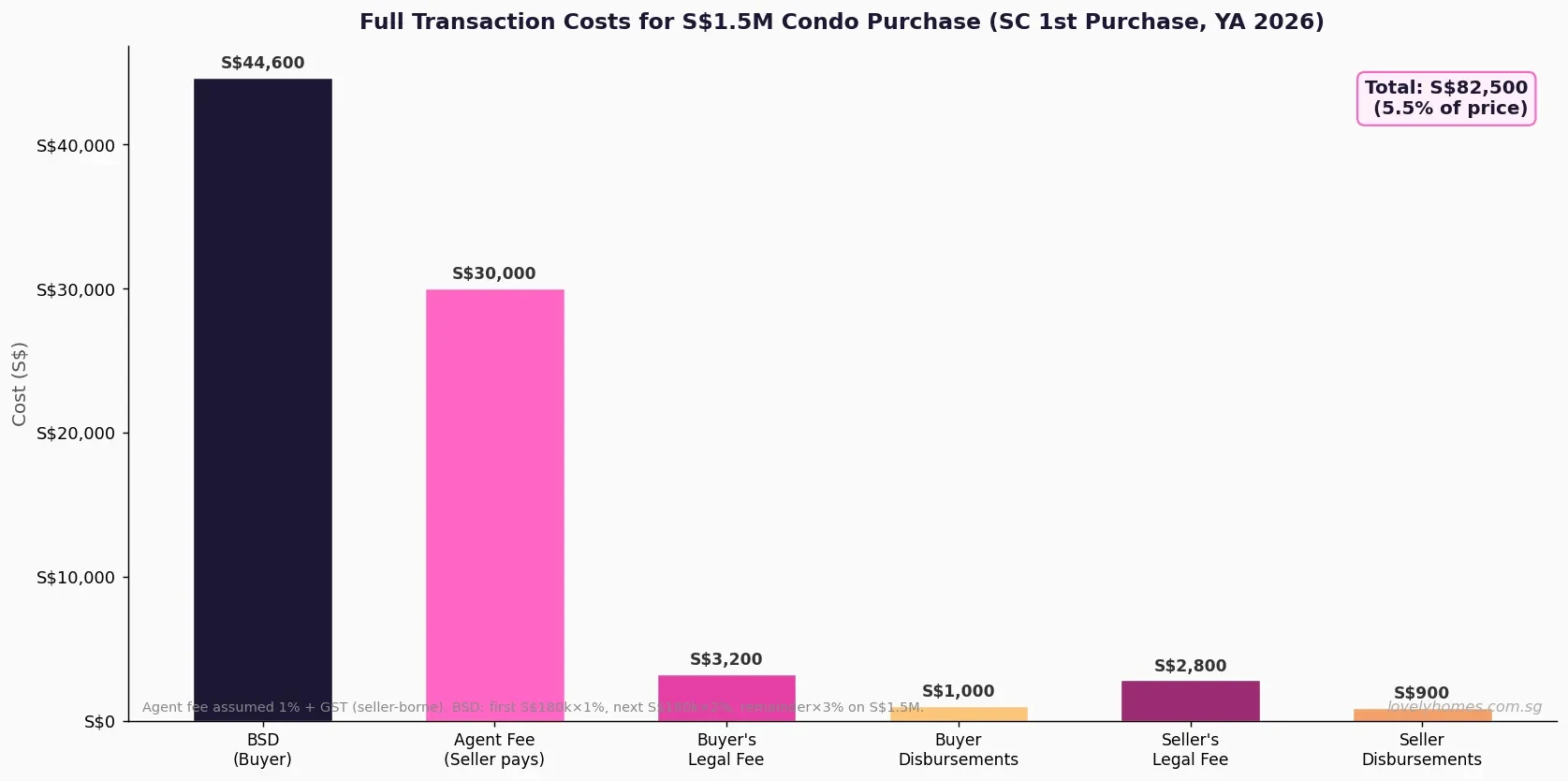

Legal fees are only one component of the total cost of buying or selling. The dominant costs for buyers are Buyer’s Stamp Duty (BSD) and, where applicable, Additional Buyer’s Stamp Duty (ABSD). Sellers bear the property agent’s commission (if an agent is engaged). Understanding the full transaction cost envelope is essential for accurate budgeting.

As the chart illustrates, BSD at S$44,600 dwarfs all other transaction costs for a first-time SC buyer at S$1.5M. BSD is calculated on the graduated scale: 1% on the first S$180,000, 2% on the next S$180,000, 3% on the next S$640,000, and 4% on the remainder. Total BSD on S$1.5M: S$180,000×1% + S$180,000×2% + S$640,000×3% + S$500,000×4% = S$1,800 + S$3,600 + S$19,200 + S$20,000 = S$44,600.

HDB Resale Flat — Conveyancing Fees

For HDB resale flat transactions, both buyer and seller must appoint their own lawyers. HDB no longer acts as the conveyancing party (it did so for many decades for straightforward HDB transactions, but now all HDB resale transactions go through private solicitors). The HDB sets a guide fee scale, though individual firms may charge within or beyond that band.

| Purchase Price / Flat Type | Buyer’s Legal Fee (Estimate) | Seller’s Legal Fee (Estimate) |

|---|---|---|

| 1- and 2-room flats (below S$300k) | S$1,200–S$1,800 | S$900–S$1,500 |

| 3-room flats (S$300k–S$450k) | S$1,500–S$2,200 | S$1,200–S$1,800 |

| 4-room flats (S$450k–S$650k) | S$1,800–S$2,600 | S$1,500–S$2,200 |

| 5-room / Executive flats (S$650k–S$900k) | S$2,200–S$3,200 | S$1,800–S$2,800 |

| Maisonette / DBSS (above S$900k) | S$2,800–S$4,000 | S$2,200–S$3,500 |

HDB resale disbursements are broadly similar to private property: title searches, caveat registration (S$64.45), government requisitions (approximately S$150–S$250 for HDB-specific searches), and the LPFF contribution. The total HDB resale legal cost for buyer or seller is usually S$1,500–S$4,500 all-in, depending on flat value and firm.

Under HDB rules, a buyer using an HDB loan may use their lawyer to handle both the HDB loan documentation and the conveyancing — consolidating into one engagement. Buyers using a bank loan will need a separate mortgage solicitor engagement (often the same firm, as many firms act for both).

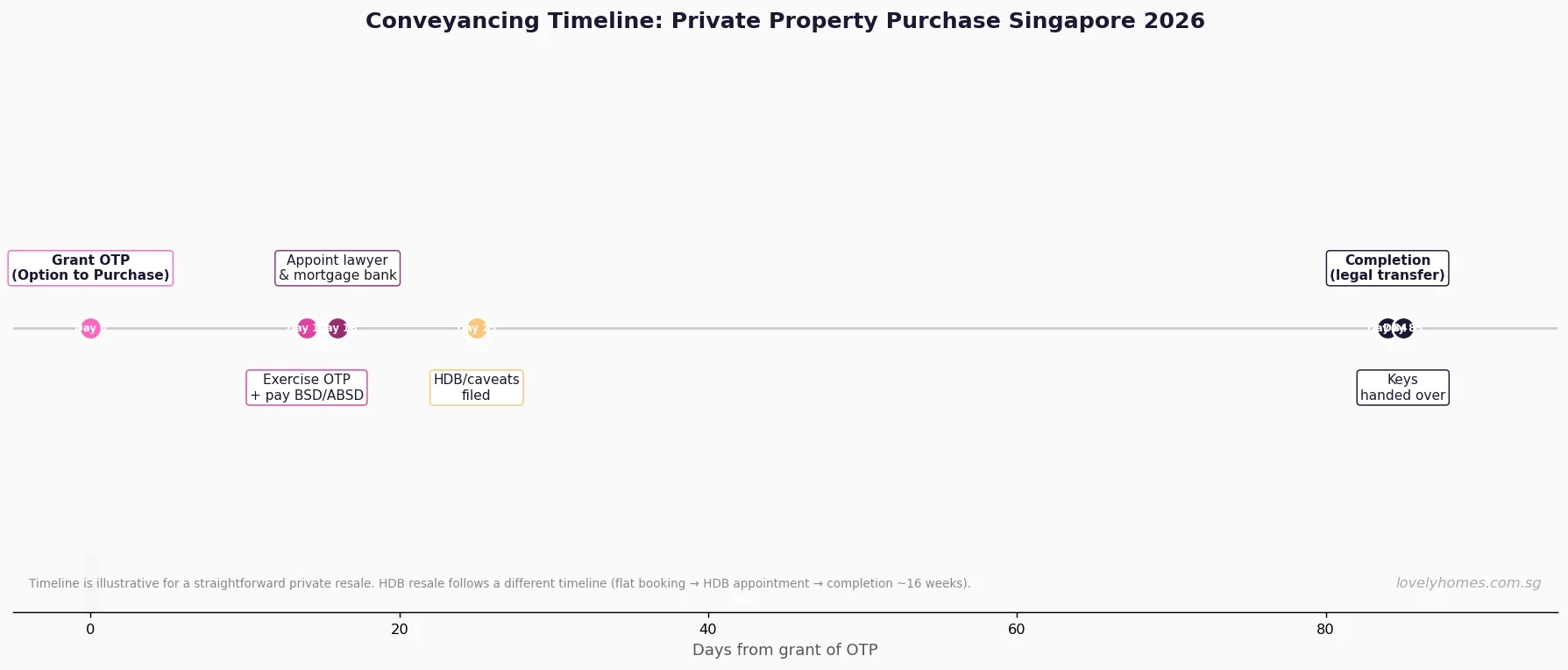

The Conveyancing Timeline: From OTP to Keys

The timeline above reflects a standard, uncomplicated private resale transaction. Key milestones and deadlines:

- Day 0 — OTP granted: The seller grants the buyer an Option to Purchase, typically with a 1% option fee. The buyer has 14 days (negotiable; commonly 14 days for private property) to exercise the OTP by paying the exercise fee (usually 4–9%, completing the 5–10% deposit).

- Day 14 — OTP exercised and stamp duty due: BSD (and ABSD if applicable) must be paid to IRAS within 14 days of exercising the OTP, via e-Stamping or through your lawyer. BSD payment late by even one day attracts a 5–15% penalty.

- Day 16 — Lawyer and bank formally appointed: Your lawyer receives the OTP, confirms instructions, and begins the legal due diligence — ordering title searches, government requisitions, and liaising with the seller’s solicitors to receive the draft SPA.

- Day 25 — Caveat lodged: Your lawyer lodges a caveat on the property title with SLA, protecting your interest as buyer against any competing claims or encumbrances registered after this date.

- Day 84 (approx.) — Legal completion: The seller’s lawyers hand over the property title documents; your lawyer simultaneously releases the purchase funds (mortgage drawdown + CPF withdrawal + cash) to the seller. The title is transferred.

- Day 85 — Keys handed over: Typically the same day as legal completion or the following business day.

Worked Example: Total Legal Costs for Mr and Mrs Lee’s Condo Purchase

Property: 3-bedroom condominium in Buona Vista, purchase price S$1.9M. Singapore Citizens, first purchase — BSD applies, no ABSD. Bank loan of S$1.425M (75% LTV).

BSD calculation:

- First S$180,000 × 1% = S$1,800

- Next S$180,000 × 2% = S$3,600

- Next S$640,000 × 3% = S$19,200

- Remaining S$900,000 × 4% = S$36,000

- BSD Total: S$60,600

Buyer’s legal costs (estimate):

- Conveyancing professional fee: S$3,800 + 9% GST = S$4,142

- Mortgage documentation fee (bank): S$1,800 + 9% GST = S$1,962

- Disbursements (searches, caveat, requisitions, LPFF): S$980

- Total buyer’s legal cost: S$7,084

Total upfront outlay by buyer:

- Initial option fee (1%): S$19,000

- Exercise fee (4%, completing 5% deposit): S$76,000

- BSD: S$60,600

- Legal fees + disbursements: S$7,084

- Remaining cash portion at completion (25% – 5% deposit already paid): S$380,000 – S$95,000 = S$285,000 (if 25% down)

- Total cash before completion: S$162,684 (option + BSD + legal)

Key insight: Legal fees account for approximately 4.4% of the total non-price transaction cost. BSD is the dominant cost at 37.3%. For planning purposes, budget at least S$165,000 in upfront costs (above the 5% deposit) for a S$1.9M purchase as a first-time SC buyer.

Practical Tips for Managing Conveyancing Costs

Get multiple quotes early. Contact two or three law firms before committing. Many reputable Singapore conveyancing firms provide free quotes via email or WhatsApp. The range across firms is usually S$400–S$800, which is worth shopping around for.

Use a panel firm for your mortgage bank. Banks maintain a panel of approved law firms for mortgage work. If your chosen conveyancing firm is also on your bank’s panel, the firm can act for both you and the bank in the same transaction, eliminating a duplicated engagement — saving S$1,500–S$3,000 in mortgage documentation fees. Ask your firm explicitly whether they are on your bank’s panel.

Understand what is included. When comparing quotes, check whether the stated fee includes disbursements or excludes them. A headline figure of S$1,800 that excludes all disbursements may end up costing more than a S$2,400 all-inclusive quote.

Keep records for rental income tax. If you are purchasing an investment property that you will rent out, your conveyancing fee is not itself deductible against rental income (it is capital expenditure). However, maintaining all records of your acquisition costs is important for computing any eventual capital gain or loss for income tax purposes if you sell (and for the base cost in any future en bloc or collective sale scenario).

Why Legal Costs Matter: Singapore vs Other Markets

Singapore’s conveyancing system is efficient and highly digitalised. The SLA’s integrated land registry means that title searches, caveats, and transfers are processed electronically and within days rather than weeks. Compared to the United Kingdom (where conveyancing often takes four to six months and legal fees on a comparable property can reach 0.5–1.0% of the purchase price), Singapore’s 8–12 week timeline and 0.15–0.25% legal fee benchmark represent a relatively streamlined and cost-effective system.

The most significant friction in Singapore’s property transaction costs remains stamp duty — BSD plus ABSD — which can amount to 5–40% of the purchase price depending on the buyer profile and property count. Legal fees are modest in comparison. For buyers focused on reducing transaction costs, understanding and minimising ABSD exposure (through careful timing, entity structure analysis, and buyer profile planning) yields far greater savings than shopping for the cheapest conveyancing quote.

What Might Change: Conveyancing Regulatory Outlook

This section is speculative. No major changes to the Singapore conveyancing framework are expected in 2026. The Ministry of Law has been examining ways to further digitalise the end-to-end property transaction process — including potential e-OTP frameworks and automated stamp duty computation — that could reduce reliance on solicitors for routine documentation in future years. However, the core requirement for a qualified Singapore solicitor to execute the transfer instrument and lodge with SLA is likely to remain in place for the foreseeable future. Any move toward a fully self-service model would require significant statutory amendment.

Summary: Conveyancing Fees at a Glance

| Transaction Type | Who Pays | Legal Fee (est.) | Disbursements (est.) | Total (est.) |

|---|---|---|---|---|

| Private property purchase (S$1M–S$2M) | Buyer | S$2,600–S$4,200 + GST | S$700–S$1,100 | S$3,600–S$5,700 |

| Private property purchase (S$2M–S$4M) | Buyer | S$3,800–S$6,500 + GST | S$900–S$1,400 | S$5,100–S$8,500 |

| Private property sale | Seller | S$2,000–S$4,500 + GST | S$600–S$900 | S$2,800–S$5,800 |

| HDB resale purchase (4-room, S$500k–S$650k) | Buyer | S$1,800–S$2,600 + GST | S$400–S$700 | S$2,400–S$3,500 |

| HDB resale sale (4-room) | Seller | S$1,500–S$2,200 + GST | S$350–S$600 | S$1,985–S$3,000 |

| Mortgage documentation (bank panel) | Borrower | S$800–S$2,500 + GST | S$100–S$300 | S$972–S$3,025 |

Frequently Asked Questions

Can I use one lawyer for both the buyer and the seller in the same transaction?

Generally, no. Under the Legal Profession (Professional Conduct) Rules, the same solicitor or firm cannot act for both buyer and seller in a property transaction, as the interests of the two parties are inherently conflicting. Each party must appoint their own lawyer. The exception applies to certain intra-family transfers or specific corporate restructurings — if in doubt, seek guidance from the Law Society of Singapore.

What happens if BSD or ABSD is paid late?

BSD and ABSD are due within 14 days of executing the Sale and Purchase Agreement (or exercising the OTP — whichever is the relevant instrument). If payment is late by up to three months, a 5% penalty surcharge applies on the outstanding stamp duty. For delays of three to six months, the penalty increases to 10%; beyond six months, 15%. In practice, your conveyancing lawyer will ensure stamp duty is paid on time — one of the core reasons why appointing a lawyer promptly after OTP exercise is important.

Do I need a separate lawyer for my mortgage, or can it be the same firm?

In most cases, the same law firm can handle both your conveyancing (title transfer) and the mortgage documentation for your bank — provided that firm is on your bank’s approved panel. This “acting for both” arrangement is standard practice in Singapore and reduces duplication. The mortgage documentation fee is a separate charge from the conveyancing fee, but using one firm is significantly cheaper than appointing two. Confirm with your chosen firm and your bank whether this arrangement is available for your specific loan product.

When should I appoint a conveyancing lawyer — before or after the OTP?

Ideally before, or at the very latest on the day the OTP is granted to you. Once you hold an OTP, you have a hard deadline (typically 14 days) to exercise it and pay BSD within another 14 days of exercise. If you appoint your lawyer only after exercising the OTP, you may lose time for the due diligence steps your lawyer needs to complete before recommending whether to proceed. For a first property purchase, most experienced buyers appoint a lawyer at the same time as they make their In-Principle Approval (IPA) application to the bank — months before finding a property.

What is a caveat, and why does my lawyer file one?

A caveat is a notice lodged on the land register with the Singapore Land Authority, alerting any third party who searches the title that you (the buyer) have an interest in the property. Once lodged, the caveat prevents the seller from transferring the property to anyone else, creating further encumbrances, or disposing of the property without your knowledge. The caveat costs S$64.45 to lodge and is typically filed within days of the SPA being signed. Your lawyer lodges it on your behalf as a standard step in every transaction.

Are conveyancing fees negotiable?

Yes, within limits. Since the prescribed scale was removed in 2009, law firms set their own fees. For straightforward transactions, fees are fairly competitive across firms and there is limited room to negotiate a significantly lower price without risking service quality. However, if you are transacting in multiple properties simultaneously (e.g., selling one and buying another), or if you are a repeat client of the firm, it is entirely reasonable to ask for a bundle discount. Always compare fee quotes from at least two firms before deciding.

What is the difference between the OTP and the Sale and Purchase Agreement (SPA)?

The Option to Purchase (OTP) is a short document — typically one to two pages — granted by the seller to the buyer for a consideration (the option fee, usually 1%). The OTP gives the buyer the exclusive right to purchase the property at an agreed price within the option period. The Sale and Purchase Agreement (SPA) is the full, binding contract that comes into force when the buyer exercises the OTP. For private properties, the SPA is a detailed document (often 20–50 pages) prepared by the seller’s solicitors and reviewed by the buyer’s solicitors. For HDB resale, a standard HDB Resale Agreement is used. Your conveyancing lawyer’s role includes reviewing both the OTP (before exercise) and the SPA (before and after execution).

Related Articles

- ABSD Singapore 2026 — Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Stamp Duty Guide 2026 — BSD, ABSD, SSD Calculator

- Private Property Buying Process Singapore 2026 — Step-by-Step Guide

- Option to Purchase Singapore 2026 — OTP Explained

- Using CPF to Buy Property in Singapore 2026

- HDB Resale Procedure Singapore 2026 — Full Timeline

- Rental Income Tax Singapore 2026 — IRAS Guide for Landlords

Disclaimer

This article is for general informational purposes only and does not constitute legal, tax, or financial advice. Fee estimates are based on market research as at May 2026 and will vary by law firm, transaction complexity, and individual circumstances. Always obtain a formal written fee quote from a qualified Singapore solicitor before instructing them. For official guidance on stamp duties, consult the Inland Revenue Authority of Singapore (IRAS). For land registration and title matters, refer to the Singapore Land Authority (SLA). For lawyer referrals or complaints, contact the Law Society of Singapore.

Click anywhere or press Esc to close

0 Comments