Singapore Private Property Resale Process 2026: Step-by-Step Guide from OTP to Keys

Quick Answer: Buying a Private Resale Property in Singapore 2026

- The full resale process — from engaging a solicitor to receiving keys — typically takes 10–14 weeks.

- You pay an Option Fee (1% of price) to secure the OTP, then exercise it within 14 days by paying the balance 4%.

- Buyer’s Stamp Duty (BSD) must be paid within 14 days of exercising the OTP; ABSD is also due at exercise.

- CPF Ordinary Account can be used for private property purchases subject to the Valuation Limit and Withdrawal Limit.

- Foreigners and PRs face Additional Buyer’s Stamp Duty (ABSD) of 60% and 5–30% respectively.

- A licensed solicitor is legally required for conveyancing — buyers and sellers cannot use the same law firm.

- The Total Debt Servicing Ratio (TDSR) cap of 55% applies to all private property mortgage loans.

What Is the Private Property Resale Process in Singapore?

Purchasing a resale private property — whether a condominium, apartment, or landed house — in Singapore follows a structured legal and financial process regulated by the Urban Redevelopment Authority (URA), the Singapore Land Authority (SLA), and the Inland Revenue Authority of Singapore (IRAS). Unlike buying a new launch (where you deal with a developer over a preview and balloting exercise), a resale transaction involves a private seller, a binding Option to Purchase (OTP), and a conveyancing timeline governed by the Law Society Conditions of Sale.

The process is considerably more compressed than buying a new launch — you can move in within 12 weeks of the OTP being granted, compared to the 3–5 year construction wait for a new launch. This immediacy comes with its own demands: due diligence, financing pre-approval, and legal fees must all be lined up before the OTP is granted.

This guide walks through every step from identifying a property to receiving keys, and explains the stamp duties, CPF rules, and financing mechanics that determine how much cash you need to have ready.

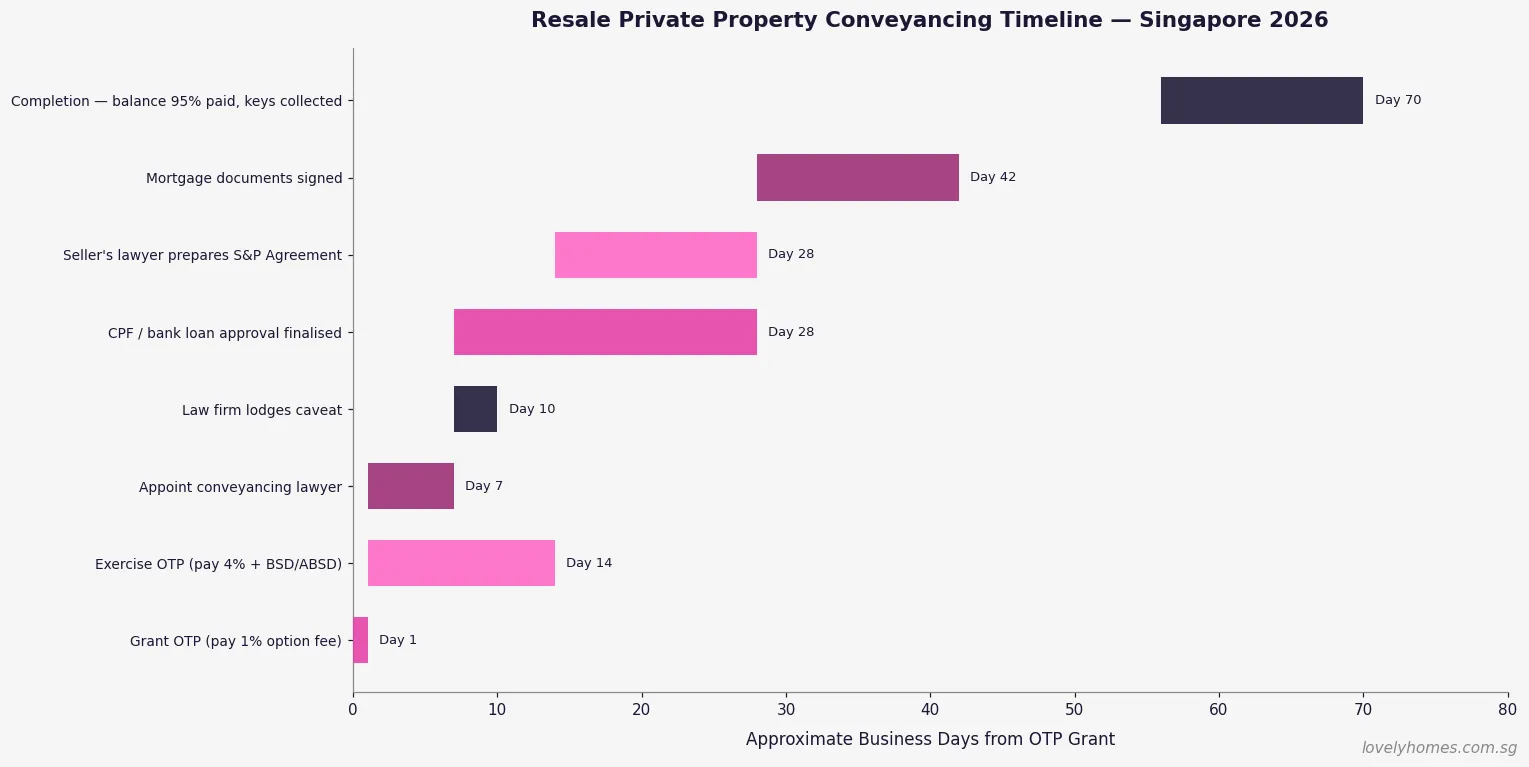

The 10-Step Private Resale Process: A Timeline Overview

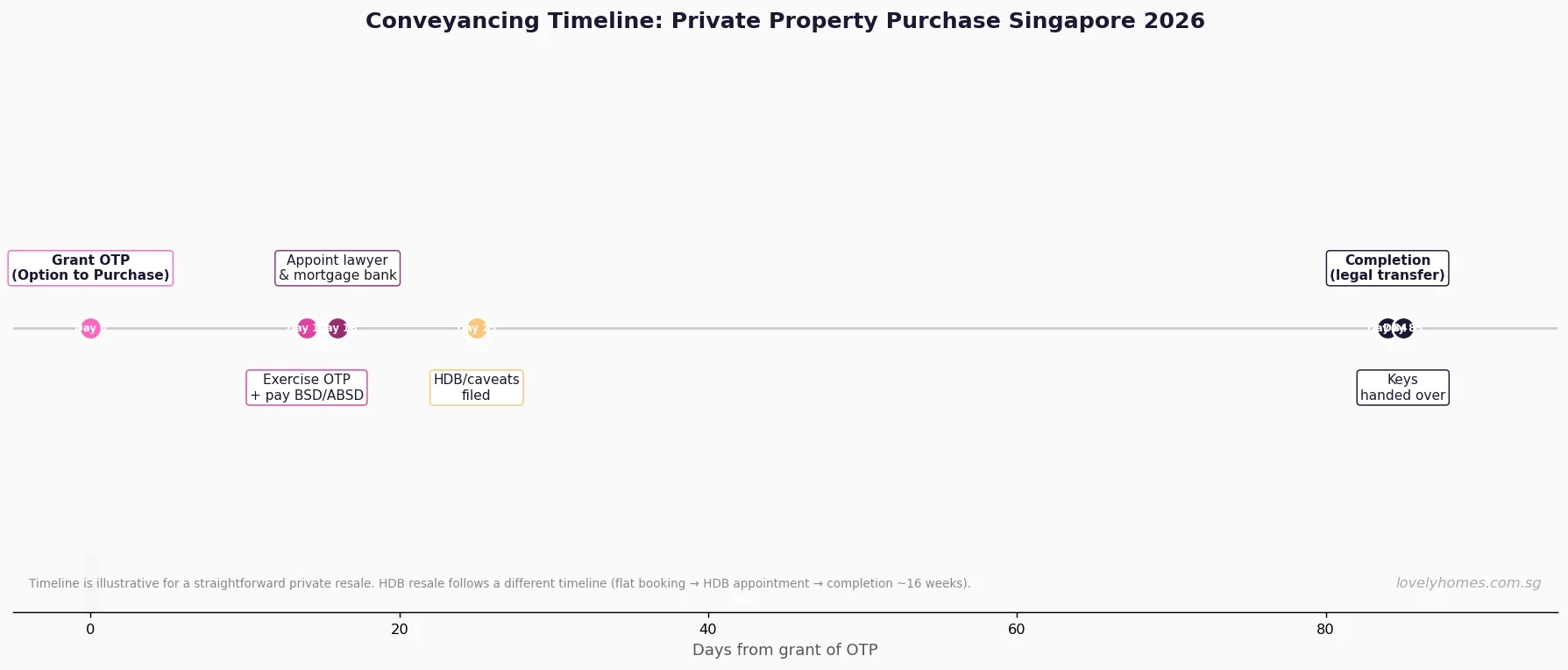

Figure 1 below shows the typical timeline across the ten stages of a private resale transaction. The entire process from engaging a solicitor to key collection typically spans 10 to 14 weeks (8 to 12 weeks for the legal completion period), though parties can agree to a shorter or longer completion period of up to 12 weeks by mutual consent.

Step 1: Engage a Solicitor (Before You Even Make an Offer)

The first step — one many buyers skip at their peril — is engaging a conveyancing solicitor before making any offer on a property. You need your solicitor in place because: (a) the OTP’s 14-day exercise window moves fast; (b) your solicitor must review the OTP wording and raise any queries before you exercise; and (c) you need legal confirmation of the CPF rules, title status, encumbrances, and outstanding maintenance fees before committing.

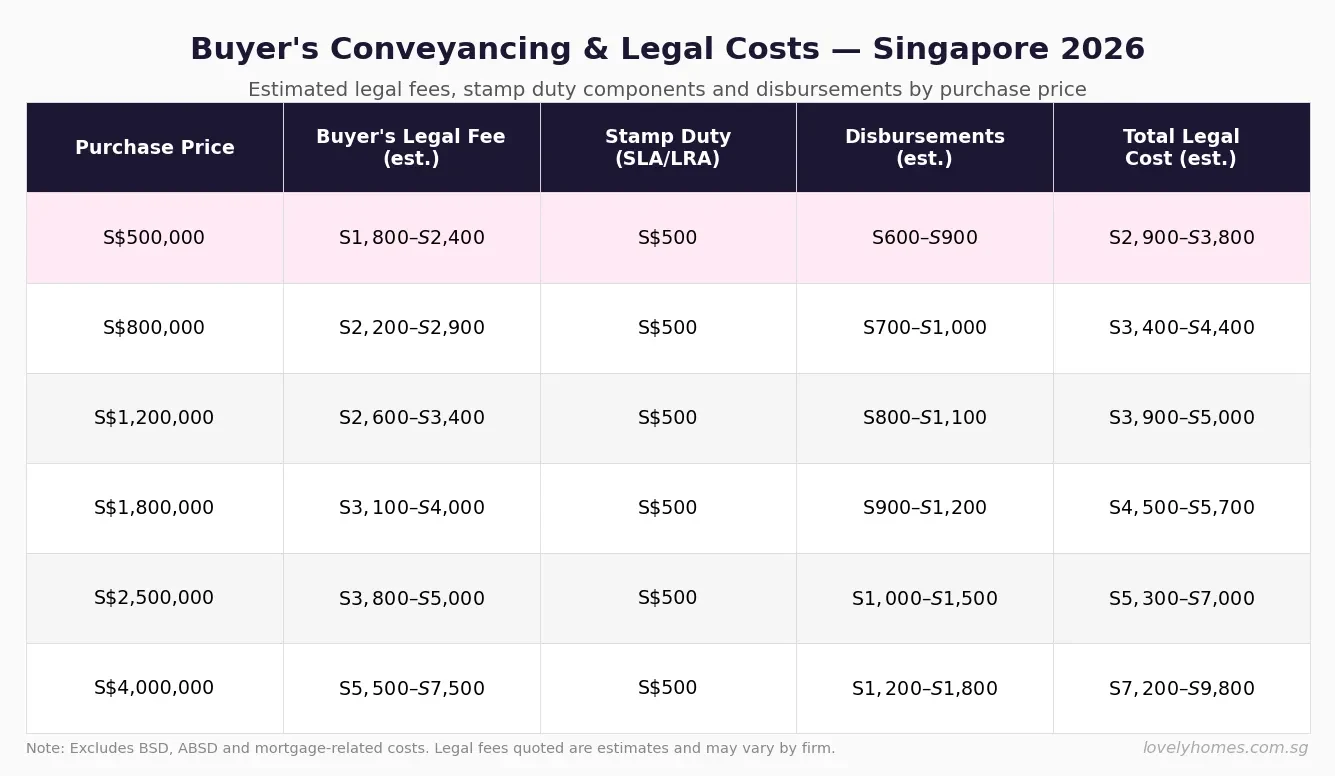

Buyer and seller cannot use the same law firm. Typical buyer legal fees for a S$1.5M condo range from S$3,500 to S$5,000 (inclusive of disbursements such as SLA caveat registration, title search, and stamp duty filing). Fees are broadly governed by the Law Society’s conveyancing fee guidelines but are now freely negotiable.

Your solicitor will conduct a title search via SLA to confirm the seller has clear, unencumbered title; check for any outstanding mortgage that must be discharged on completion; verify there is no Subsidiary Strata Land Act (SSLA) restriction or approved change of use that affects the property; and review the Management Corporation Strata Title (MCST) accounts for outstanding arrears and sinking fund adequacy. For a deeper primer on MCST issues, see our Singapore Condo MCST Guide 2026.

Step 2: Search and View Properties — Due Diligence Before the OTP

Before agreeing to any price, buyers should undertake thorough due diligence on the unit and the development. Key checks include: verifying the actual floor area against the strata title plan; confirming the remaining lease term (for leasehold developments); reviewing the MCST annual report for sinking fund balance and any pending special levies; checking for outstanding renovations bans or works on the common property; and reviewing recent comparable transactions in the development (available via URA REALIS or on the URA website’s Resale Transactions tool).

Buyers should also verify their eligibility. Singapore Citizens may purchase all private property types. Permanent Residents may purchase apartments, condominiums, and commercial property freely but require approval from the Land Dealings (Approval) Unit to purchase landed residential property. Foreigners may only purchase landed property in designated areas (Sentosa Cove) or with SLA approval, and face 60% ABSD on any residential purchase.

Step 3: Grant and Exercise of the Option to Purchase (OTP)

Once you have agreed on a price, the seller grants you an Option to Purchase in exchange for the Option Fee — typically 1% of the agreed purchase price paid in cash. The OTP gives you an exclusive right to purchase the property at the agreed price, typically for a 14-day option period (this period is agreed between parties and can be shorter or longer).

During the option period, your solicitor reviews the OTP. If you are satisfied, you exercise the OTP by signing it and paying the exercise fee — typically the balance 4% of the purchase price in cash or a combination of cash and CPF. On exercise, the OTP becomes a binding contract. The completion date is set for 8–12 weeks from the exercise date.

If you do not exercise the OTP within the period, the Option Fee is forfeited to the seller. There is no other penalty — the purchase simply does not proceed. This is why due diligence and financing must be in order before granting an OTP.

Step 4: Stamp Duties — BSD and ABSD (Due Within 14 Days)

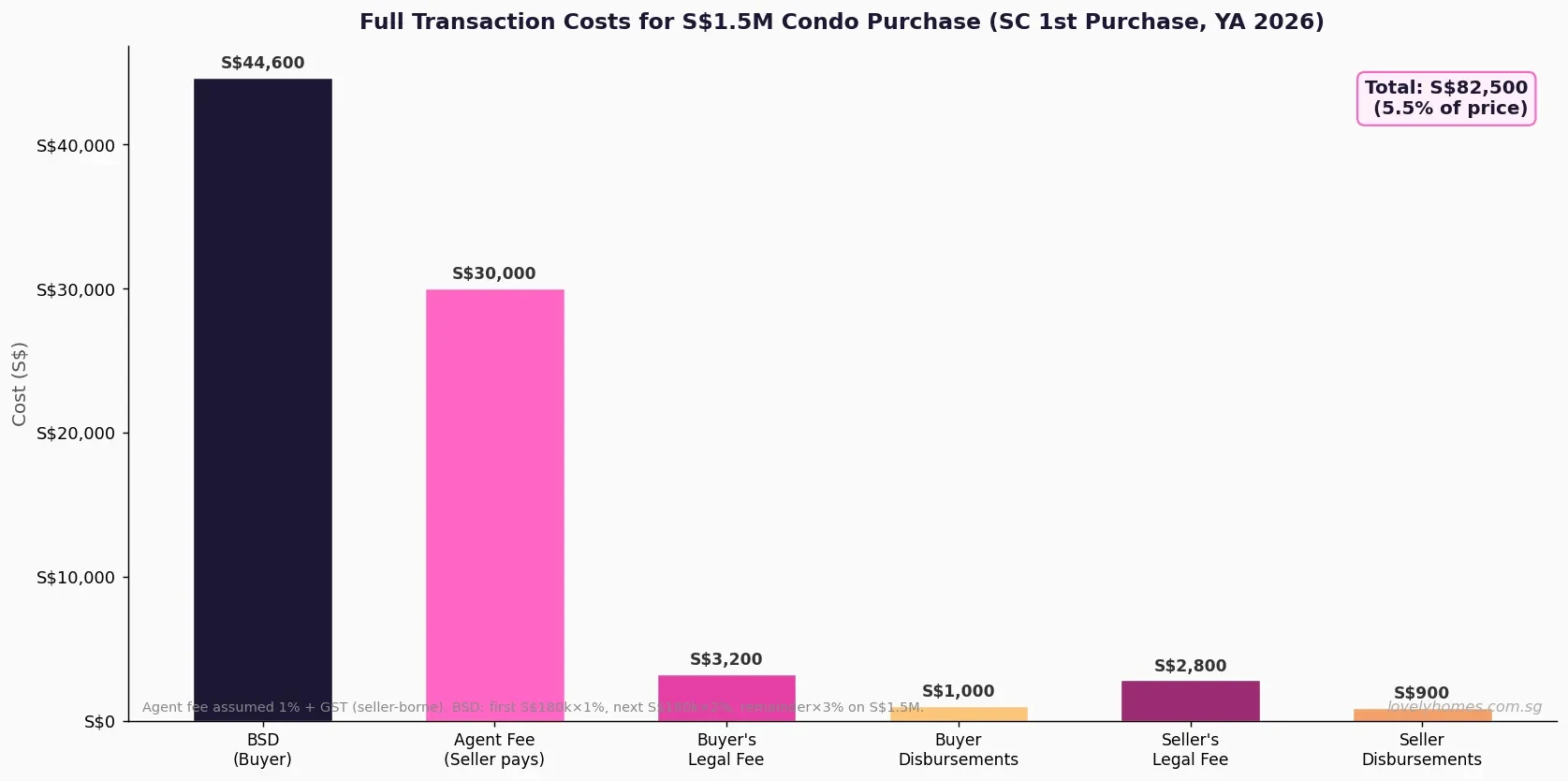

Buyer’s Stamp Duty (BSD) is payable on all property purchases. It is calculated on a graduated scale on the purchase price or market value, whichever is higher. On a S$1.5M purchase, BSD is S$44,600 (effective rate approximately 2.97%). BSD must be paid via IRAS e-Stamping within 14 days of the date of the OTP exercise.

Additional Buyer’s Stamp Duty (ABSD) applies to SC buyers purchasing a second or subsequent residential property, and to all PR and foreigner buyers. ABSD rates in 2026 are: SC 2nd property 20%, SC 3rd+ 30%, SPR 1st property 5%, SPR 2nd+ 30%, foreigners 60%. For a full ABSD breakdown, see our ABSD Singapore 2026 Complete Guide. ABSD is also due within 14 days of exercise.

Both BSD and ABSD can be paid from CPF Ordinary Account (for residential property). However, ABSD amounts for second properties are substantial — for example, a SC buying a S$1.5M second property pays S$300,000 in ABSD alone, which would exhaust most CPF balances. The ABSD remission scheme allows SC couples who are upgraders to claim a refund of the ABSD if they sell their existing residential property within 6 months of purchasing the new one. See our Stamp Duty Remission Guide for details.

Upfront Stamp Duty and Legal Costs by Buyer Profile (S$1.5M)

Figure 2 illustrates the total upfront stamp duties and legal costs at a S$1.5M purchase price across five buyer profiles. The disparity between a SC first-time buyer (S$49,100) and a foreigner (S$944,600) underlines why Singapore’s ABSD is one of the world’s most aggressive foreign-buyer deterrents.

Step 5: Arranging the Mortgage

Private property purchases must comply with the Monetary Authority of Singapore’s Total Debt Servicing Ratio (TDSR) framework. Under the TDSR, monthly debt obligations — including the new mortgage plus any existing credit facilities — cannot exceed 55% of gross monthly income. Unlike HDB loans (which have a 30% Mortgage Servicing Ratio cap), private property loans use TDSR only.

The Loan-to-Value (LTV) ratio for a first private property mortgage is up to 75%, requiring a minimum 25% downpayment (of which 5% must be in cash). For a buyer with an existing outstanding mortgage, the LTV drops to 45% (first subsequent loan). See the prior reference in our Property Downpayment Guide 2026.

Banks will commission an independent valuation of the property. If the valuation comes in below the agreed price, the bank will lend only against the valuation — meaning the buyer must fund the shortfall in cash. For example, if you agreed to pay S$1,550,000 but the valuation is S$1,500,000, the bank’s 75% LTV is based on S$1,500,000, so the buyer must fund the additional S$50,000 from cash.

For CPF usage: CPF Ordinary Account can be used for the downpayment and monthly instalments for private property up to the property’s Valuation Limit (the lower of purchase price or valuation). Beyond the Valuation Limit, the Withdrawal Limit (120% of the property value for properties with sufficient lease) applies. See our CPF for Private Property Guide 2026 for the full mechanics.

Step 6: Lodge a Caveat with the Singapore Land Authority (SLA)

Once the OTP is exercised, your solicitor should promptly lodge a Caveat with the SLA. A caveat protects your interest in the property by registering your claim against the title. It prevents the seller from selling to a third party or granting another mortgage on the same property. The caveat fee is approximately S$150–S$200. Caveats are registered via the SLA’s e-Conveyancing system.

Step 7: Completion of the Sale and Purchase

Completion is the legal transfer of title from seller to buyer. On the completion date (typically 8–12 weeks from OTP exercise), all parties’ solicitors meet (or exchange completion documents electronically via e-Conveyancing). The buyer’s solicitor pays the balance purchase price from the mortgage loan drawdown and any remaining CPF/cash. The seller’s solicitor receives the funds and transfers title.

At completion, the seller’s outstanding mortgage is discharged from the sale proceeds. The SLA registers the transfer of title and the buyer’s new mortgage. The buyer’s solicitor registers the mortgage instrument. Typically, keys are handed over on the completion date or shortly thereafter.

Singapore Resale Condo Price Ranges by Region and Unit Type (Q1 2026)

Figure 3 illustrates indicative resale condo price ranges by unit size and region. The Core Central Region (CCR — Districts 9, 10, 11, and the Downtown Core) commands the highest prices, particularly for larger units. The Outside Central Region (OCR) offers the widest value range for buyers seeking more affordable entry points.

Private Resale Process at a Glance: Key Facts Table

| Stage | Who Acts | Key Deadline | Typical Cost |

|---|---|---|---|

| Engage solicitor | Buyer | Before OTP | S$3,500–S$5,000 |

| Grant OTP / Option Fee (1%) | Seller grants, Buyer pays | At agreement | 1% of price (cash) |

| Exercise OTP (4%) | Buyer | Within 14 days | 4% of price (cash/CPF) |

| BSD + ABSD payment | Buyer via solicitor | 14 days from exercise | Varies (BSD + any ABSD) |

| Lodge caveat (SLA) | Buyer’s solicitor | Promptly after exercise | ~S$150–S$200 |

| Mortgage drawdown | Buyer / Bank | Before completion | Bank valuation fee S$300–S$700 |

| Completion / Key collection | Both solicitors | 8–12 weeks from exercise | Balance purchase price |

Worked Example: The Kumar Family Buying a Resale 3-Bedroom in the RCR

Scenario: SC Couple, First Private Property, Selling Their HDB

Mr Kumar (38, SC) earns S$9,500/month; Mrs Kumar (36, SC) earns S$8,800/month. Joint income: S$18,300/month. They currently own an HDB flat (5-room, Tampines) with no outstanding mortgage. They wish to upgrade to a private resale 3-bedroom condo in the RCR.

- Target unit: 3-bedroom resale condo, RCR (District 3), 1,000 sqft, freehold.

- Agreed price: S$2,100,000

- Bank valuation: S$2,050,000 (shortfall S$50,000 — must fund in cash)

- BSD: S$74,600 (progressive on S$2,100,000: 1% × S$180K + 2% × S$180K + 3% × S$640K + 4% × S$500K + 5% × S$600K = S$74,600)

- ABSD: 20% × S$2,100,000 = S$420,000 (SC 2nd property — HDB still owned at time of purchase)

- ABSD remission plan: The Kumars plan to sell their HDB flat within 6 months of completion. If sold within 6 months, ABSD S$420,000 is refunded by IRAS. They pay ABSD upfront and claim the remission later.

- Loan (75% LTV on valuation S$2,050,000): S$1,537,500 at 3.1% p.a., 30 years → S$6,567/month

- TDSR check: S$6,567 ÷ S$18,300 = 35.9% (below 55% cap — PASS)

- Downpayment (25% of S$2,050,000): S$512,500 (5% cash = S$102,500 + 20% CPF = S$410,000)

- Price shortfall (purchase price above valuation): S$50,000 (cash)

- Total cash at exercise and completion: Option fee S$21,000 (1%) + exercise S$84,000 (4%) + BSD S$74,600 + ABSD S$420,000 + valuation shortfall S$50,000 + legal S$5,200 + CPF mortgage arrangement S$0 = S$654,800 gross cash outlay (S$234,800 net after ABSD remission assuming HDB sold within 6 months)

Key takeaway: The Kumars’ biggest cash item is the upfront ABSD of S$420,000 — which they recover after selling the HDB. The net out-of-pocket (excluding ABSD) is approximately S$234,800. Planning the HDB sale timeline to remain within the 6-month remission window is critical.

Why the Private Resale Market Has Structural Depth

Unlike new launches, where pricing is controlled by the developer and buyers often face limited negotiation leverage, the resale market allows genuine price discovery between informed parties. This creates opportunities for buyers who do thorough research — understanding block-level transaction data, comparable lease terms, and development-specific factors like upcoming en-bloc potential, MCST financial health, and facilities.

The resale market also offers a distinct advantage: immediate occupation. For families with school enrolment timelines, existing rental commitments, or home sale proceeds that need to be redeployed promptly, the 10–14 week completion window is a significant operational benefit over a 3–5 year new-launch wait.

Resale buyers are also protected by a more mature legal framework. The Law Society Conditions of Sale provide standardised terms. The conveyancing system is transparent, title searches are reliable, and disputes are resolvable via the High Court or the Small Claims Tribunal (for deposits and agent disputes).

What Might Come Next for Singapore’s Private Resale Market?

This section reflects editorial analysis and forward-looking opinion, not a guarantee of future market performance.

The private resale market in 2026 is characterised by moderate volumes and selective price growth. OCR resale condos have held up well due to strong HDB upgrader demand — particularly from families exiting their MOP-completed BTO flats and entering the private market for the first time. CCR volumes remain relatively subdued as the 60% ABSD on foreign buyers has largely eliminated the speculative froth that characterised 2010–2013.

Looking ahead, the GLS tender pipeline — including sites at River Valley Green Parcel C (tendered June 2026), Town Hall Link white site (July 2026), and several OCR sites — will deliver new supply from 2028 onwards. This supply pipeline, while healthy, is not expected to flood the market given construction cost inflation and developer pricing discipline. The 2H2026 GLS Confirmed List of nine sites yielding approximately 4,745 residential units is broadly consistent with household formation rates and replacement demand.

For resale buyers, the near-term window before new-launch supply hits the market in volume (2027–2028) may represent a relative opportunity for well-priced resale units in established OCR and RCR estates.

Frequently Asked Questions: Buying Private Resale Property in Singapore

Can buyer and seller use the same solicitor?

No. Buyer and seller in a private property transaction must each engage their own separate law firm. This is a professional conduct requirement under the Legal Profession (Professional Conduct) Rules. Having the same solicitor act for both parties creates a conflict of interest — the solicitor cannot independently advise each party on a transaction where interests may diverge. In practice, buyers sometimes attempt to share a solicitor to save costs; this is not permitted for private property transactions (though an exception exists for certain straightforward HDB transactions under specific conditions).

What happens if my bank valuation comes in below the agreed price?

If the bank’s independent valuation of the property is lower than the agreed purchase price, the bank will only lend based on the lower valuation. The buyer must fund the difference (the shortfall between valuation and price) entirely in cash. CPF cannot be used for amounts above the valuation, and the ABSD is still calculated on the actual purchase price (the higher amount). For example, if you paid S$1,600,000 for a unit valued at S$1,550,000, you fund the S$50,000 shortfall in cash; BSD and ABSD are calculated on S$1,600,000. Buyers can seek a second valuation from a different valuer if they believe the first is too conservative, but banks are not obliged to accept it.

What is a Diplomatic Clause and should I request one?

A Diplomatic Clause is a lease termination right inserted into a tenancy agreement (not a purchase OTP). It allows a tenant to terminate an ongoing tenancy early if they are required to relocate due to work reasons (typically due to a transfer or job loss). It typically kicks in after a minimum period (commonly 12–14 months) with 2 months’ notice. It is relevant for buyers who intend to rent out the unit before moving in or while relocating — they would negotiate a Diplomatic Clause into the tenancy they offer to their tenant, not into the OTP for the purchase. It is standard practice for developments popular with expatriate tenants in CCR and RCR.

Does ABSD apply if I buy a private property with my spouse for the first time?

If both you and your spouse are Singapore Citizens purchasing your first residential property together, no ABSD applies. SC buyers (individually or jointly) are exempt from ABSD on their first residential property. If one spouse already owns property (including overseas property counts for ABSD purposes), ABSD will apply based on the higher-count buyer’s profile. For example, if you own an HDB flat (first property) and your spouse does not, joint purchase of a private condo is treated as a second property for ABSD purposes — the 20% SC 2nd-property ABSD applies on the entire purchase price. Decoupling strategies (where one party transfers their share to the other) may be considered to reset the count; see our Joint Property Ownership Guide for the decoupling mechanics and costs.

What are the key differences between buying a new launch condo and a resale condo?

There are several material differences. New launches are purchased from a developer during a preview/balloting period using the standard Sale and Purchase Agreement (SPA) under the Housing Developers (Control and Licensing) Act, with a progressive payment schedule as construction milestones are met. Resale purchases use an OTP and a Law Society SPA, with full payment at completion. New launches typically offer developer discounts and stamp duty absorption deals near launch, but buyers wait 3–5 years for completion. Resale condos allow immediate occupation and give you a complete picture of the actual unit, renovation condition, view, and development quality before committing. Resale buyers can also inspect the MCST accounts in detail before purchase, something impossible for a new launch. Price transparency also favours resale — URA publishes every resale transaction, whereas new-launch prices require asking agents or checking URA REALIS.

Can I negotiate below the seller’s asking price?

Yes — negotiation is standard in the private resale market. Reference points for your offer include: recent comparable transactions in the same development (from URA Resale Transactions data), the property’s age and condition, any pending special levies or MCST deficits, how long the unit has been listed, and the seller’s motivation (e.g., upgrading, emigrating, financial pressure). In a buyers’ market (higher inventory, slower volume), 3–8% below asking is not unusual for motivated sellers. In a tight market (low inventory, fast absorption), properties can transact at or above asking. Always let the bank’s independent valuation inform your offer ceiling — paying significantly above valuation means funding the excess in cash without CPF or loan coverage.

Do I need a property agent to buy a resale condo?

No — there is no legal requirement to engage a buyer’s agent for a private resale transaction. However, a buyer’s agent provides value through: identifying suitable listings and arranging viewings; interpreting transaction data to assess fair market value; negotiating the OTP price and conditions; and coordinating between the solicitors and seller’s agent. Buyer’s commission for private resale is typically not charged to buyers directly — it is paid by the seller via a co-broking arrangement with the seller’s agent. Effectively, you get buyer’s representation at no direct cost in most resale transactions. For those who proceed without an agent, ensure your solicitor reviews the OTP carefully before exercise, and do your own comparable transaction research via URA REALIS.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Buyer’s Stamp Duty (BSD) 2026: Rates, Calculations and Worked Examples

- Buying a Condo in Singapore 2026: Complete Guide to Costs, Eligibility and Process

- Singapore Stamp Duty Remission Guide 2026: ABSD Upgrader Refunds Explained

- Using CPF to Buy Private Property in Singapore 2026: Valuation Limit and Withdrawal Limit

- Singapore Joint Property Ownership Guide 2026: Joint Tenancy, ABSD and Decoupling

- Singapore Condo MCST Guide 2026: Maintenance Fees, AGM and Your Rights

- Singapore Property Conveyancing Guide 2026: OTP, S&P Agreement and Legal Fees

Disclaimer: The information in this article is for general educational purposes only and does not constitute financial, investment, or legal advice. Stamp duty rates, CPF rules, LTV limits, and property market conditions are subject to change by the relevant Singapore government bodies. Verify current rates and rules with IRAS (iras.gov.sg), HDB (hdb.gov.sg), CPF Board (cpf.gov.sg), URA (ura.gov.sg), and the Monetary Authority of Singapore (mas.gov.sg). All property transactions should be conducted through a licensed solicitor for conveyancing. Engage a Council for Estate Agencies (CEA)-licensed property agent if you require professional property advisory services.

Click anywhere to close