Jurong Lake District White Site 2026: Town Hall Link GLS Tender, 1,200 Homes and CRL CR19

Quick Answer: JLD Town Hall Link White Site at a Glance

- Site: Town Hall Link, Jurong Lake District (JLD), adjacent to the Jurong Town Hall national monument.

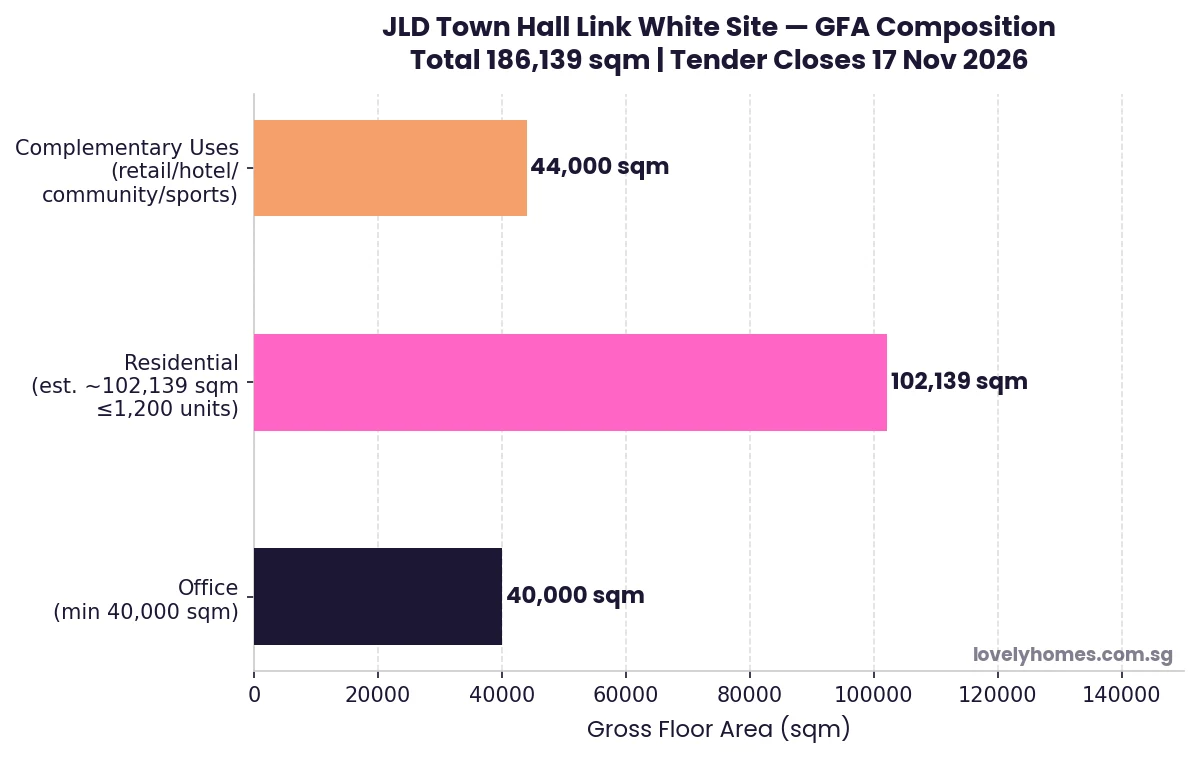

- Total GFA: 186,139 sqm — one of the largest mixed-use sites launched in Singapore in recent years.

- Residential: up to 1,200 private residential units.

- Office: minimum 40,000 sqm — anchoring JLD’s ambition as the largest business node outside the city centre.

- Complementary uses: up to 44,000 sqm for retail, serviced apartments, hotel, sports, community and medical facilities.

- Connectivity: integrated with Jurong East MRT interchange (EWL/NSL), future JRL JE5 station, and upcoming CRL CR19 station (planned 2032).

- Tender closes: 17 November 2026.

- Why it matters: the White site designation gives developers flexibility to configure uses — residential, commercial, or mixed — based on market conditions at launch, making it one of Singapore’s most strategically significant land sales of 2026.

URA Launches JLD White Site: Singapore’s Most Anticipated 2H 2026 GLS Tender

The Urban Redevelopment Authority (URA) launched the tender for a White site at Town Hall Link in the Jurong Lake District (JLD) on 3 July 2026, marking one of the most significant Government Land Sales (GLS) moves of the year. At 186,139 sqm of total potential Gross Floor Area (GFA) — comprising a minimum 40,000 sqm of office, up to 1,200 private residential units, and 44,000 sqm of complementary uses — this site has the potential to define the next chapter of Singapore’s western regional centre.

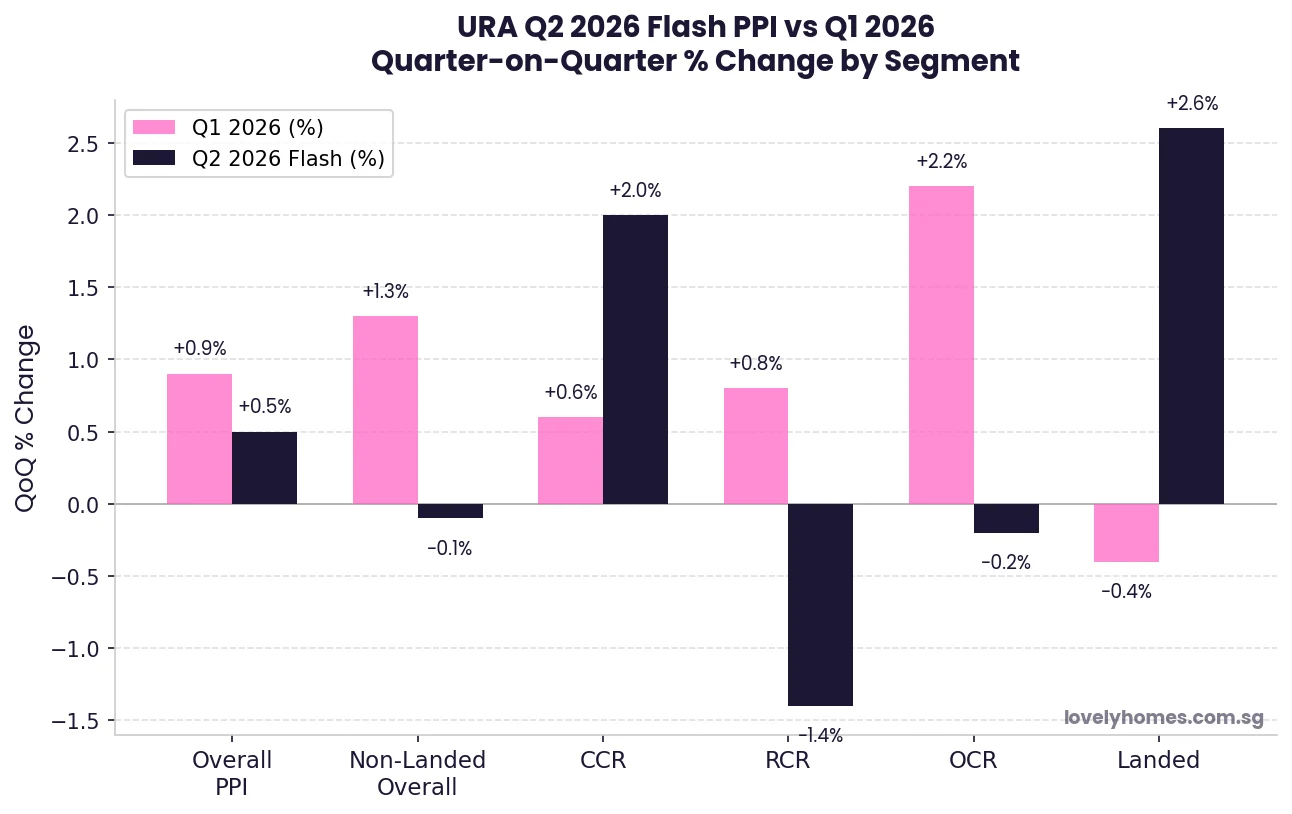

The tender forms part of the Confirmed List for the 2H 2026 GLS Programme and will close at 12 noon on 17 November 2026. It comes less than two weeks after URA released its Q2 2026 property price flash estimate showing the overall private residential PPI rising a modest 0.5% — a market context that is stable enough for developers to bid with confidence, but not so frothy as to suggest over-payment risk.

JLD is Singapore’s flagship decentralisation initiative: a vision to create a vibrant live-work-play precinct in the western part of Singapore that can absorb commercial, residential, and civic activity without adding further pressure on the already-congested central business district. The Town Hall Link site occupies a prime position within this vision — sited next to the Jurong Town Hall national monument, directly connected to the Jurong East MRT interchange, and in the future path of two new MRT lines.

What Is a White Site?

A White site in Singapore’s GLS framework is a land parcel that developers may develop for any combination of uses permitted under the Master Plan, subject to a minimum requirement for one or more specified uses. Unlike purpose-specific GLS sites (e.g., residential-only or commercial-only), a White site allows developers to calibrate the use mix based on their read of market conditions at the time of design and launch.

For the Town Hall Link site specifically, the conditions are: minimum 40,000 sqm office; up to 1,200 residential units; and up to 44,000 sqm for complementary uses. The developer awarded the site will have latitude to decide the precise mix of hotel, serviced apartments, retail, community facilities, and sports/recreation components — creating significant design flexibility in exchange for the commitment to deliver a meaningful commercial core.

White sites have historically attracted strong bidding interest in Singapore because they reduce the development risk associated with committing entirely to a single use in a market that can shift between residential launch and commercial occupation. The last major White site in JLD — the site that became J Gateway and the surrounding cluster — generated keen bidding when it was first introduced.

Figure 1: Town Hall Link White Site — indicative GFA breakdown by use. Total 186,139 sqm. Source: URA pr26-53, 3 July 2026.

The JLD Masterplan: Context for This Site

JLD’s transformation has been driven by two decades of sustained government investment in infrastructure and planning. The revitalised Jurong Lake Gardens (90 hectares) provides the greenery spine at the district’s heart. Two new MRT lines are changing the connectivity calculus dramatically:

- Jurong Region Line (JRL): JE5 station at Jurong East and JE6 station at International Business Park (planned to open 2028).

- Cross Island Line (CRL): CR19 station at the heart of the new JLD precinct (planned to open 2032).

The addition of CRL is particularly significant: it will provide a direct east-west connection from JLD to Ang Mo Kio, Pasir Ris, and eventually Changi — transforming what has historically been perceived as a “western” destination into a genuinely cross-island node. For the Town Hall Link site, the multi-level pedestrian connections to Jurong East MRT interchange and the upcoming CR19 station mean that residents and office workers at this development will enjoy arguably the best public transport connectivity of any mixed-use site currently on the GLS market.

The site sits next to the Jurong Town Hall, a gazetted national monument. This adjacency imposes design constraints — any development will need to respect the monument’s visual and physical setting — but also provides a distinctive civic character that differentiates the JLD precinct from purely commercial developments elsewhere.

Development Mix Analysis

| Use Component | GFA (sqm) | Status | Commentary |

|---|---|---|---|

| Office | 40,000 minimum | Mandatory | Anchors JLD’s role as business node; positions site as corporate headquarters address |

| Private Residential | Up to ~102,139 (est.), max 1,200 units | Optional (developer discretion) | 1,200 units at typical 80–90 sqm average ≈ 102,000 sqm; adds residential critical mass to district |

| Complementary Uses | Up to 44,000 | Optional (developer discretion) | Can include: retail, hotel, serviced apartments, sports/recreation, medical clinics, community facilities, visitor attractions |

| Total GFA | 186,139 | One of Singapore’s largest mixed-use GLS sites |

At 1,200 residential units, this would represent one of Singapore’s larger single-site condominium developments — comparable in scale to recent developments like Canninghill Piers (696 units) and Lentor Modern (605 units), but notably larger. The scale is appropriate for JLD’s ambition to create residential density that sustains the commercial base.

Key Catalysts and Infrastructure Timeline

The development that occupies this site will benefit from a series of planned catalysts over the 2026–2035 horizon:

| Catalyst | Timeline | Impact on Site |

|---|---|---|

| JRL JE5 (Jurong East) and JE6 (International Business Park) | Phased opening, 2027–2028 | Improved east-west connectivity within JLD; connects IBP to Jurong East interchange |

| New Science Centre at JLD | Expected by 2027 | Adds visitor attraction and civic anchor to the precinct; drives weekend footfall |

| Jurong Gateway Hub (bus interchange + office + retail + community club + library + sports) | Expected by 2028 | Integrated civic hub immediately adjacent; dramatically increases JLD’s daytime and evening population |

| CRL CR19 station at JLD | Planned 2032 | Cross-island connectivity; potential 15% to 20% capital value uplift for residential units at this site based on historical TEL/MRT proximity premiums |

Residential Investment Angle: 1,200 Units in JLD

If the awarded developer proceeds with the full 1,200-unit residential allocation, this will be among the more significant new private residential supply additions to JLD since the area last saw major development activity in the 2013–2017 era (J Gateway, Westwood Residences, Lake Grande, Twin Vew). JLD has historically commanded a premium relative to other OCR locations — driven by the live-work-play narrative, the lake setting, and the Jurong East MRT interchange’s accessibility to both the western industrial belt and the central business district via the East-West Line.

A new-launch condo at this site, post-CRL connectivity, could plausibly target $2,000–$2,400 psf based on the trajectory of comparable new launches in OCR/RCR boundary locations in 2025–2026. The tender price paid by the developer will be the key determinant of eventual launch pricing — a high land bid will translate into a premium launch price, while a competitive-but-measured bid could allow the developer to price attractively and generate strong take-up. The tender close date of 17 November 2026 gives the market approximately four and a half months to assess these dynamics.

What This Means for the Broader Market

The JLD White Site launch is a policy signal as well as a commercial opportunity. URA’s decision to include a major White site in the 2H 2026 Confirmed List — rather than deferring it to the Reserve List — indicates confidence that developer demand is sufficient to support a committed bid within the current market cycle. The White site mechanism also signals flexibility: if the residential market softens before design completion, the developer can weight the mix toward commercial and serviced apartment uses.

For existing JLD residential owners — in projects like J Gateway, Lake Grande, Twin Vew, and the upcoming The LakeGarden Residences — the Town Hall Link development represents both an opportunity (improved amenity and connectivity as the precinct builds out) and a risk (increased residential supply within the immediate catchment). On balance, the infrastructure and amenity uplift from the New Science Centre, Jurong Gateway Hub, and CRL CR19 is likely to outweigh the supply effect, particularly for well-located existing units.

What Might Come Next

The following is editorial commentary — not official guidance.

Bidding for the Town Hall Link site is expected to attract Singapore’s larger developers and possibly joint ventures. The scale of the site (186,139 sqm) requires significant capital — a land price in the S$1.5–S$2.5 billion range would not be surprising, depending on the assumed residential launch pricing and the developer’s commercial income projections. International developers with Asian regional headquarters-in-a-hub ambitions could also consider the mandatory 40,000 sqm office component as a corporate campus opportunity.

The CRL CR19 station opening in 2032 is a known future catalyst — developers will model this into their land bid assumptions. A project that launches residential units in 2028–2029 (assuming a 2027 tender award, 1-year design/approval, and early 2028 launch) would be telling buyers that their units will be CRL-connected by the time they reach the 5-year mark of ownership.

Frequently Asked Questions

What does “White site” mean for buyers of the eventual development?

A White site designation affects the developer’s design choices, not individual buyers’ rights. When the eventual development is launched for sale, buyers will purchase units in a standard private condominium development. They will benefit from the mixed-use amenities — retail, food and beverage, possibly a hotel or serviced apartment building within the same development — that result from the White site configuration. The White site label itself conveys no special lease conditions or restrictions on buyers beyond the standard conditions of a freehold or 99-year leasehold private condominium.

When will the residential units at Town Hall Link be available for sale?

The tender closes 17 November 2026. Assuming the tender is awarded in Q1 2027, and accounting for design, planning approval, and construction timelines, the earliest a residential launch could realistically occur is late 2027 or 2028. Physical completion (Temporary Occupation Permit) would likely follow in 2030–2032. Prospective buyers interested in this development should monitor URA and the awarded developer’s announcements in 2027.

How does the JLD CRL station affect property values nearby?

Historical evidence from Singapore MRT openings — most recently the Thomson-East Coast Line (TEL) stages 1–4 and the Downtown Line — suggests that residential properties within 500 metres of a new MRT station tend to appreciate by 8–15% relative to comparable properties further away in the 3–5 years following station opening. The effect is partially priced in ahead of the opening as buyers and investors anticipate the connectivity uplift. For CR19 (planned 2032), properties in the immediate JLD precinct likely already incorporate some forward-looking CRL premium in 2026. The full premium crystallises as the opening date approaches and actual connectivity is confirmed.

Is the Town Hall Link site freehold or leasehold?

GLS sites in Singapore are typically sold on 99-year leasehold terms. The Town Hall Link site is expected to follow this standard. Buyers of units in the eventual development will hold 99-year leasehold titles, with the lease commencement date tied to the date of the land award. Leasehold tenure is the norm for new GLS-sourced developments in Singapore; the premium-location attributes of the site — MRT connectivity, JLD masterplan, CRL uplift — are expected to sustain long-term value notwithstanding the leasehold structure.

What other major GLS sites were launched in 2H 2026?

The 2H 2026 GLS Confirmed List provides a total of 4,745 private residential units. In addition to the Town Hall Link White site, URA also launched sites at Lorong Puntong/Sin Ming Avenue (~140 units, TEL Bright Hill MRT, tender closes 15 September 2026) and Kitchener Link (~145 units, Reserve List, Farrer Park MRT NEL). The full 2H 2026 GLS programme — including industrial and commercial sites — is available on the URA website at ura.gov.sg/land-sales.

Related Articles

- Jurong East Neighbourhood Guide Singapore 2026: JLD, JRL and Investment Outlook

- URA GLS: Lorong Puntong/Sin Ming Avenue and Kitchener Link Sites (June 2026)

- URA Q2 2026 Singapore Property Price Index: Market Softens as CCR Rebounds

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Property Cooling Measures Timeline 2009–2026

Disclaimer

This article is for general informational purposes only and does not constitute financial or investment advice. Details of the Town Hall Link White site are sourced from URA press release pr26-53 (3 July 2026) and the URA website. Developer bidding, design outcomes, launch pricing, and project timelines are speculative editorial commentary and do not represent commitments by URA or any developer. For authoritative site details and tender conditions, refer to ura.gov.sg. Consult a licensed financial adviser before making any property investment decision.