Singapore Property Inheritance Guide 2026: Wills, CPF Nominations, HDB Flats and Stamp Duty Explained

Inheriting property in Singapore is rarely straightforward. Whether you are the surviving spouse of an HDB flat owner, a child named in a parent’s will, or a beneficiary who just discovered their loved one died without any estate planning, the rules governing how Singapore residential property passes on death are layered, sometimes counterintuitive, and — if you get them wrong — expensive. This Singapore property inheritance guide 2026 consolidates everything you need to know: the Intestate Succession Act, making a valid will, CPF nomination rules that override your will, HDB flat transfer procedures, stamp duty obligations, the probate process, and the legitimate planning strategies every property owner in Singapore should consider.

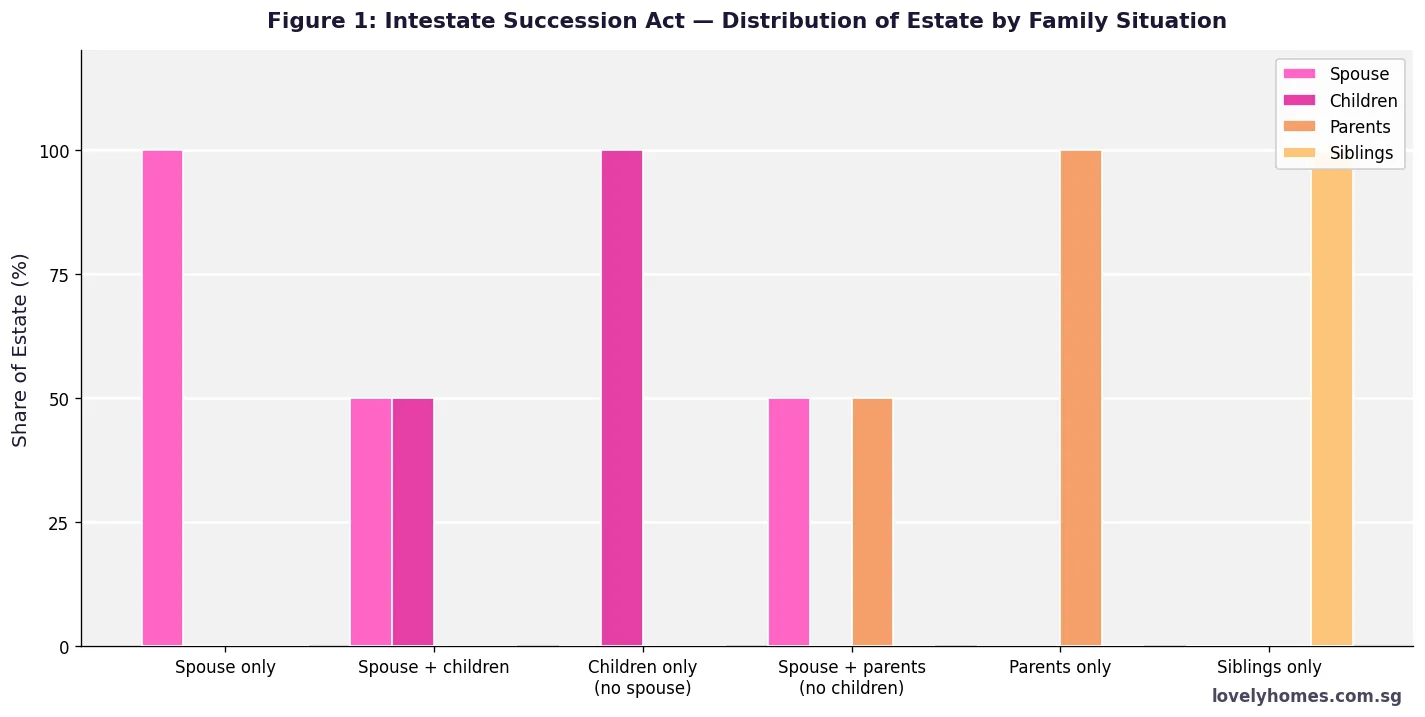

- Without a will, the Intestate Succession Act (Cap 146) governs distribution — your spouse gets 50%, your children share the other 50% (or spouse takes all if no children).

- CPF savings bypass your will entirely — they go to your CPF nominees, or to the Public Trustee if you have none.

- HDB flats may be retained by eligible family members under the Right of Occupancy Scheme; if no eligible occupier exists, HDB buys back the flat at market value.

- No estate duty applies in Singapore — abolished in February 2008. Inherited property itself is not subject to stamp duty on the death transfer.

- However, a subsequent gift or sale of inherited property to another person can trigger Buyer’s Stamp Duty (BSD) and, critically, ABSD based on the recipient’s property count and citizenship.

- A properly executed will, CPF nomination, and LPA can prevent months of delays, court applications, and avoidable costs.

- Probate in Singapore typically takes 4–9 months for a straightforward estate; more complex multi-property or overseas-asset estates may take 12–24 months.

The Intestate Succession Act — What Happens Without a Will

When a Singapore resident who is not a Muslim dies without a valid will, the Intestate Succession Act (Cap 146), administered by the Family Justice Courts, determines who inherits the estate. The Act follows a fixed hierarchy of beneficiaries and applies to both HDB flats and private residential property (subject to the special HDB rules discussed later).

The most important thing to understand is that the Act’s rules are inflexible — the court has no discretion to vary them based on your wishes or circumstances. If you want a different outcome, you need a will.

| Survivors at Death | Who Inherits (and Share) |

|---|---|

| Spouse only (no children, no parents) | Spouse — 100% |

| Spouse + children | Spouse 50% / Children share 50% equally |

| Children only (no spouse) | Children — 100% shared equally |

| Spouse + parents (no children) | Spouse 50% / Parents 50% |

| Parents only (no spouse, no children) | Parents — 100% equally |

| Siblings only | Siblings — 100% equally |

| No family at all | Government — bona vacantia |

Critically, the Intestate Succession Act does not apply to Muslims in Singapore — Muslim estates are governed by Islamic inheritance law (faraid) administered through the Syariah Court and Muslim Trust Fund (MUIS). If you are Muslim, consult a lawyer or MUIS directly.

Making a Valid Will in Singapore

A will is the cornerstone of any estate plan. Under the Wills Act (Cap 352), a valid Singapore will must be:

- In writing (typed or handwritten).

- Signed by the testator (the person making the will) at the foot of the document.

- Witnessed by two independent witnesses — both present at the same time when the testator signs. Neither witness (nor their spouse) can be a beneficiary.

- Made by a person aged 21 or older (or a member of the armed forces on active service).

There is no requirement to register a will with any government body in Singapore, though many solicitors recommend lodging it with the Wills Registry at the Singapore Academy of Law for a small fee (~S$50). A will can be revoked at any time by making a new one or by destroying the original with the intention to revoke. Marriage automatically revokes a prior will in Singapore.

What your will can do: direct who receives your private residential property; name your executor; appoint guardians for minor children; specify funeral wishes; establish testamentary trusts for minors or dependants. What it cannot do: override CPF nominations, bypass HDB rules on flat ownership, or transfer assets held in joint tenancy (these pass automatically to the surviving joint tenant by operation of law).

CPF Nominations — The Rule That Overrides Your Will

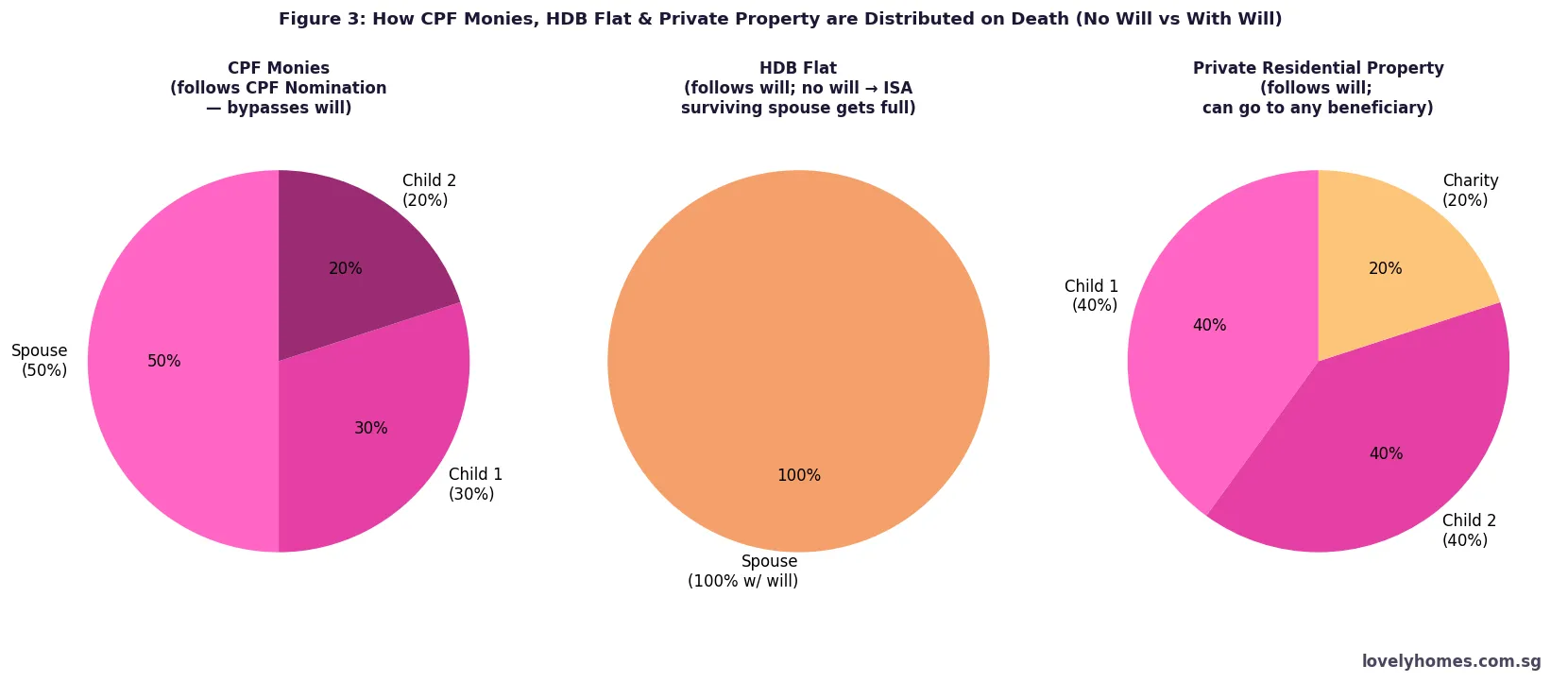

Many Singapore property owners are surprised to learn that their CPF Ordinary Account (OA) savings — which are frequently used to fund property purchases and monthly mortgage instalments — do not form part of their estate and cannot be distributed via a will. CPF monies are governed separately by the Central Provident Fund Act and paid out exclusively to CPF nominees upon death.

If you have not made a CPF nomination, your CPF savings (OA, SA, MediSave) will be transferred to the Public Trustee’s Office, which then distributes them according to the Intestate Succession Act — but charges an administration fee (0.75%–2.75% of the CPF balance, capped at S$6,000). This process can take 6–12 months. A CPF nomination is free, takes about 10 minutes via the CPF Board website, and can be updated any time.

Note also: if you bought your HDB flat using CPF, the CPF funds drawn plus accrued interest must be refunded to your CPF account on the sale or transfer of the flat. This affects the net cash proceeds available to your estate or your surviving family members.

HDB Flat Inheritance — Special Rules Apply

HDB flats come with a unique set of rules on death that do not apply to private residential property. The guiding principle is that an HDB flat should continue to be used as an owner-occupied home for a qualifying Singapore household — it is not freely tradeable inheritance that can be sold at will.

Scenario A: Joint tenancy — surviving joint tenant takes all

Most married couples own their HDB flat as joint tenants. On the death of one owner, the surviving joint tenant automatically becomes the sole owner by right of survivorship — no probate is required, and no will can override this. The surviving owner needs only to lodge a Notice of Death with HDB and the Singapore Land Authority (SLA) to update the title.

Scenario B: Tenancy-in-common — estate share passes via will or ISA

If the flat was held as tenancy-in-common, the deceased’s share passes to the estate and is then distributed via the will or the Intestate Succession Act. The beneficiary of the share must be an eligible person under HDB’s policies — meaning they must form a family nucleus with the remaining flat owner(s), be a Singapore Citizen or PR, and meet the HDB eligibility criteria. If the beneficiary is not eligible (e.g. a foreigner child), HDB will require the flat to be sold.

Scenario C: Sole owner dies — HDB’s Retention Scheme

If the deceased was the sole owner, HDB allows eligible occupiers (family members currently living in the flat who meet eligibility criteria) to apply to retain the flat under the Right of Occupancy Scheme. If no eligible occupier exists, HDB will buy back the flat at market value, and the proceeds go to the estate.

Importantly, the Minimum Occupation Period (MOP) for the inherited flat is assessed separately. An inheriting family member does not automatically “reset” the MOP clock — HDB’s rules on this have specific carve-outs. Always check with HDB directly at the time of inheritance.

Private Residential Property — Inheritance and Stamp Duty

Private condominiums, landed houses, and freehold/leasehold private apartments follow a different set of rules from HDB flats. There is no HDB eligibility requirement — foreigners can inherit private property — but stamp duty implications arise when the property is subsequently transferred or sold.

No stamp duty on the death transfer itself

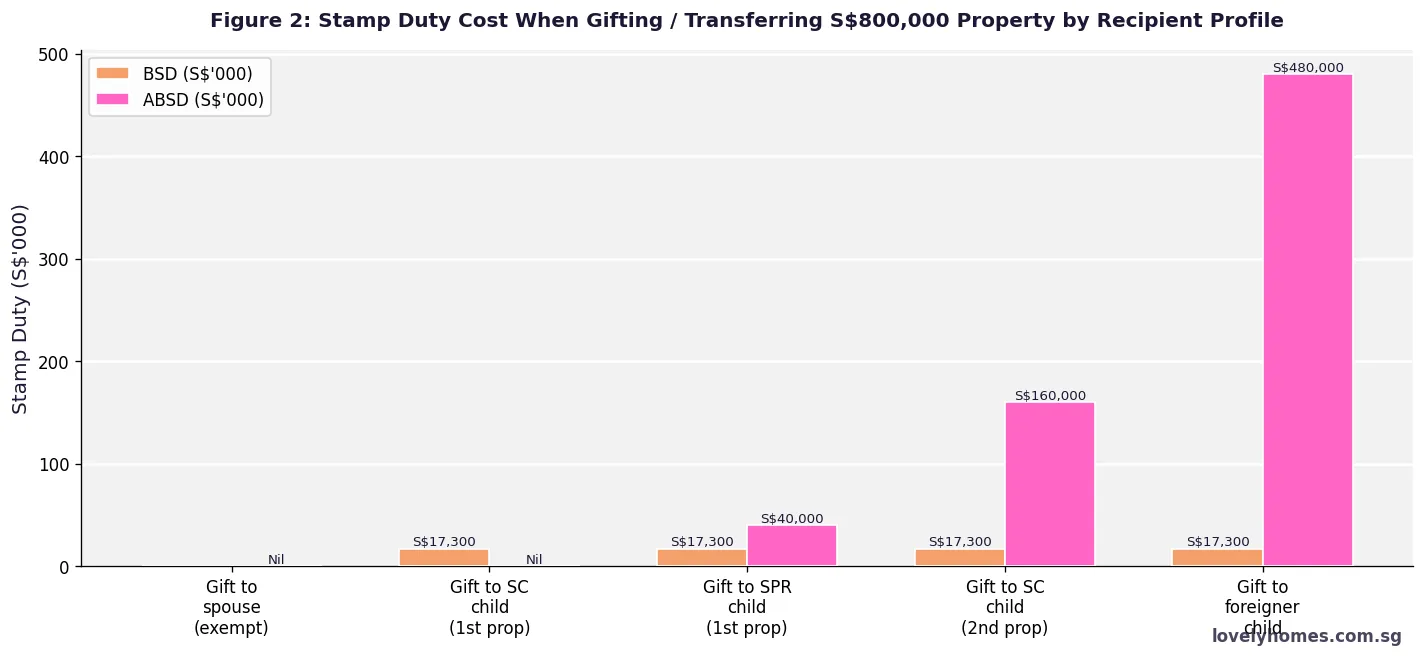

The transfer of property to a beneficiary via a will or intestacy is treated as a transmission on death. Under the Stamp Duties Act, such transmissions are exempt from Buyer’s Stamp Duty and ABSD. No duty is payable when the executor or administrator assents the property to the beneficiary. Singapore also abolished estate duty in February 2008, so there is no inheritance tax on the total value of the estate.

ABSD when you inherit a second or third property

However, the inherited property is counted toward your property count for future purchases. This is a critical but frequently misunderstood rule. If you are a Singapore Citizen who already owns one condominium and then inherb a second private property from a deceased parent, your property count becomes two. If you subsequently buy a third property, ABSD of 30% (SC rate for 3rd property) applies. Plan accordingly.

Gifting property inter vivos (lifetime transfers)

If you choose to gift a property to a family member during your lifetime (rather than leaving it via will), BSD is triggered on the market value of the property at the time of transfer. ABSD also applies based on the recipient’s citizenship and property count. A gift to your Singapore Citizen child who already owns one property would attract 20% ABSD on the market value — potentially hundreds of thousands of dollars.

🏠 Worked Example: The Tan Family Estate

Situation: Mr Tan (Singapore Citizen) passed away on 15 March 2026, leaving a 4-bedroom condominium in Bishan worth S$2,100,000 and a 5-room HDB flat in Ang Mo Kio worth S$780,000. Mr Tan had a valid will leaving both properties to his wife (Mrs Tan, SC) and two adult children (both SC, each with their own private condominiums). The HDB flat was held in joint tenancy with Mrs Tan; the condo was held in Mr Tan’s sole name.

HDB flat (joint tenancy):

- Passes automatically to Mrs Tan by right of survivorship — no probate required for HDB.

- Mrs Tan lodges a Notice of Death with HDB and SLA. Title updated in her sole name.

- No stamp duty on this transmission. Mrs Tan now holds the HDB as sole owner.

Bishan condominium (sole name, covered by will):

- Executor obtains Grant of Probate from the Family Justice Courts — estimated 4–6 months.

- Will bequeaths the condo 50% to Mrs Tan and 25% each to Child 1 and Child 2.

- Transmission to all three beneficiaries: BSD = Nil; ABSD = Nil (transmission on death exempt).

- Mrs Tan’s property count: now HDB flat + 50% share in Bishan condo = 2 properties held.

- Each child’s property count: now their existing condo + 25% Bishan share = 2 properties each.

- If any of them buys another property, ABSD will be charged at the 3rd-property SC rate (30%).

BSD + Legal costs for probate:

- Probate solicitor fees (estimated): S$3,500–S$6,000 for a clean estate

- Court filing fee (estimated): S$750–S$1,500

- Assent (Conveyancing for condo transfer): S$1,500–S$2,500 legal fees + SLA registration ~S$165

- Total estate settlement cost: approximately S$6,500–S$10,000

Key lesson: Having a valid will allowed Mr Tan’s estate to be distributed efficiently. Without a will, the ISA would have given Mrs Tan 50% and split the other 50% equally between the two children — a similar result here, but in more complex family structures the ISA’s rigid hierarchy can produce very different outcomes from what the deceased intended.

The Probate Process in Singapore

When a person dies leaving a will, the executor named in the will applies to the Family Justice Courts for a Grant of Probate, which authorises the executor to administer the estate. If there is no will, the next-of-kin applies for Letters of Administration — a broadly equivalent process but typically requiring two sureties (guarantors).

Key steps in the process:

- Death registration — the attending doctor issues a Cause of Death certificate; the Registrar of Deaths (ICA) issues the Death Certificate, usually within a few days.

- Identify and value assets — bank accounts, CPF balances, property title searches (SLA), shareholdings, insurance policies, foreign assets.

- Engage a probate solicitor — unless the estate is very simple (below S$50,000 with no immovable property), legal representation is strongly recommended.

- File for Grant of Probate / Letters of Administration at the Family Justice Courts — fees are payable on a sliding scale based on the estate value.

- Advertise for creditors — in a local newspaper, to flush out any outstanding liabilities.

- Pay outstanding debts and liabilities — including any outstanding mortgage (the estate must redeem the mortgage or service it until the property is transferred or sold).

- Transfer or sell the property — the executor assents (transfers title) to the beneficiary or conducts a sale, remitting proceeds to the estate.

- Distribute balance to beneficiaries — with a proper estate account and receipts.

A straightforward Singapore estate with no overseas assets, no disputes, and a valid will typically takes 4–9 months from death to final distribution. Estates with overseas property can take significantly longer due to separate probate requirements in each jurisdiction.

Estate Planning — What Every Singapore Property Owner Should Do

Singapore’s property market is one of the most valuable asset classes for most families. Leaving the transmission of that wealth to chance — or to the rigidities of the Intestate Succession Act — is a risk that is easily and cheaply avoided. A comprehensive estate plan for a property-owning Singapore family typically involves four instruments:

| Instrument | What it Covers | Who Administers | Cost (Approx.) |

|---|---|---|---|

| Will | Private property, bank accounts, personal effects, guardianship of minor children | Family Justice Courts (probate) | S$300–S$1,200 (straightforward) |

| CPF Nomination | CPF OA, SA, MediSave balances | CPF Board (direct payment) | Free |

| HDB Nomination (if applicable) | Share in HDB flat (for tenancy-in-common owners) | HDB | Free |

| Lasting Power of Attorney (LPA) | Decision-making if you lose mental capacity (not on death) | Office of the Public Guardian | S$75 (standard); free if certified by legal aid |

Why Singapore Property Inheritance Matters in 2026

Singapore is in the midst of a significant intergenerational wealth transfer. According to industry estimates, the cohort of HDB flat owners who purchased under SERS and other early schemes in the 1970s–1990s are now in their 70s and 80s. Hundreds of thousands of HDB flats — many now in the S$600,000–S$1,100,000+ resale range — will change hands via inheritance over the next decade. Add private condominiums and landed property to the mix, and the scale of property wealth being inherited is unprecedented in Singapore’s history.

At the same time, the 2023 ABSD increase to 60% for foreigners and 20%/30% for Singapore Citizens on 2nd/3rd properties has made the counting of inherited properties a material financial issue. An unexpected inheritance that tips a SC buyer from “first property” to “second property” status can turn a planned purchase into an ABSD liability of 20% — potentially S$400,000+ on a typical CCR condominium.

What Might Come Next

This section contains editorial speculation and is clearly labelled as such.

Singapore’s government has occasionally reviewed the rules around HDB flat inheritance, particularly in the context of ageing lease profiles and the VERS (Voluntary Early Redevelopment Scheme) pipeline. There is some industry discussion about whether the Right of Occupancy Scheme might be tightened as Singapore’s HDB stock ages and more flats with shorter remaining leases pass between generations — since family members inheriting a flat with 30 or 40 years of lease remaining face a very different investment proposition from those inheriting a newer flat.

On the stamp-duty side, there is no indication that Singapore intends to reintroduce estate duty (abolished 2008). The MND and MOF have historically viewed the abolition as positive for Singapore’s competitiveness as a wealth hub. For now, the transmission-on-death BSD/ABSD exemption also appears stable. Changes to ABSD for inherited properties — e.g. a grace period or exemption from the property count for inherited shares — have been discussed in industry circles but have not been signalled by the Government.

Frequently Asked Questions

Does inheriting a property count toward my ABSD property count?

Yes. Once a property is transmitted to you as a beneficiary and you are registered as owner (or part-owner) at the Singapore Land Authority, it counts toward your residential property count for ABSD purposes. This means that if you already own one private property and you inherit a second one, you are considered a second-property owner. A subsequent purchase would attract the SC third-property ABSD rate of 30%. There is currently no grace period or inherited-property exemption from this counting rule. If you are planning a purchase and know an inheritance is likely, speak to a lawyer about the timing and sequencing.

My parent passed away and left an HDB flat in their sole name. What happens?

If the deceased was the sole HDB owner and there is a valid will, the executor will apply for Grant of Probate. HDB will then assess whether any of the occupiers listed in the flat (or beneficiaries named in the will) qualify to retain it under their eligibility criteria — they must be a Singapore Citizen or PR, form a proper family nucleus, and satisfy income/property ownership requirements. If an eligible person exists, the flat can be transferred to them (subject to HDB’s approval). If no eligible occupier or beneficiary qualifies, HDB has the right to buy back the flat at market value, and the proceeds form part of the estate. Contact HDB’s Branch directly early in the probate process to understand your options.

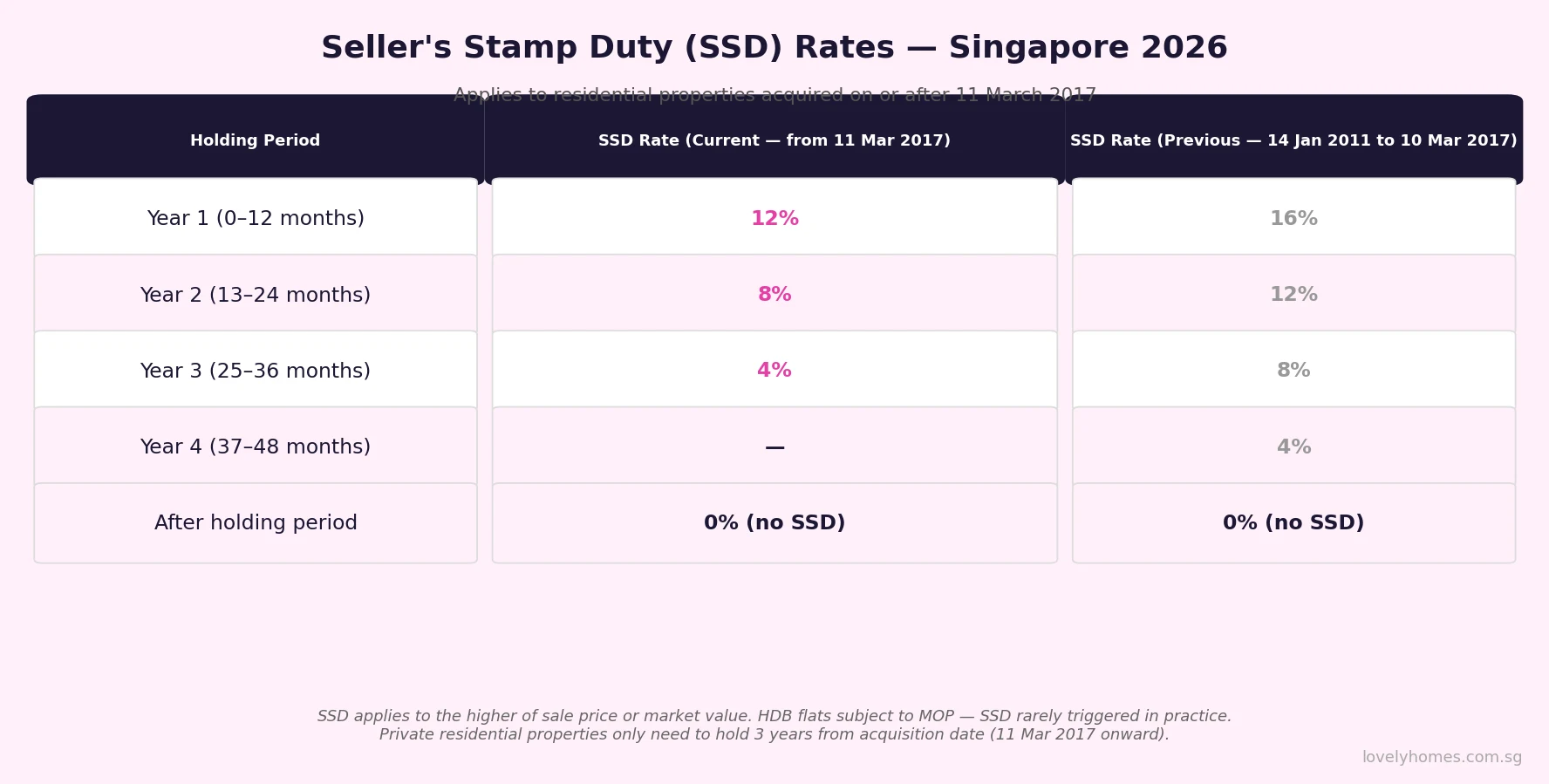

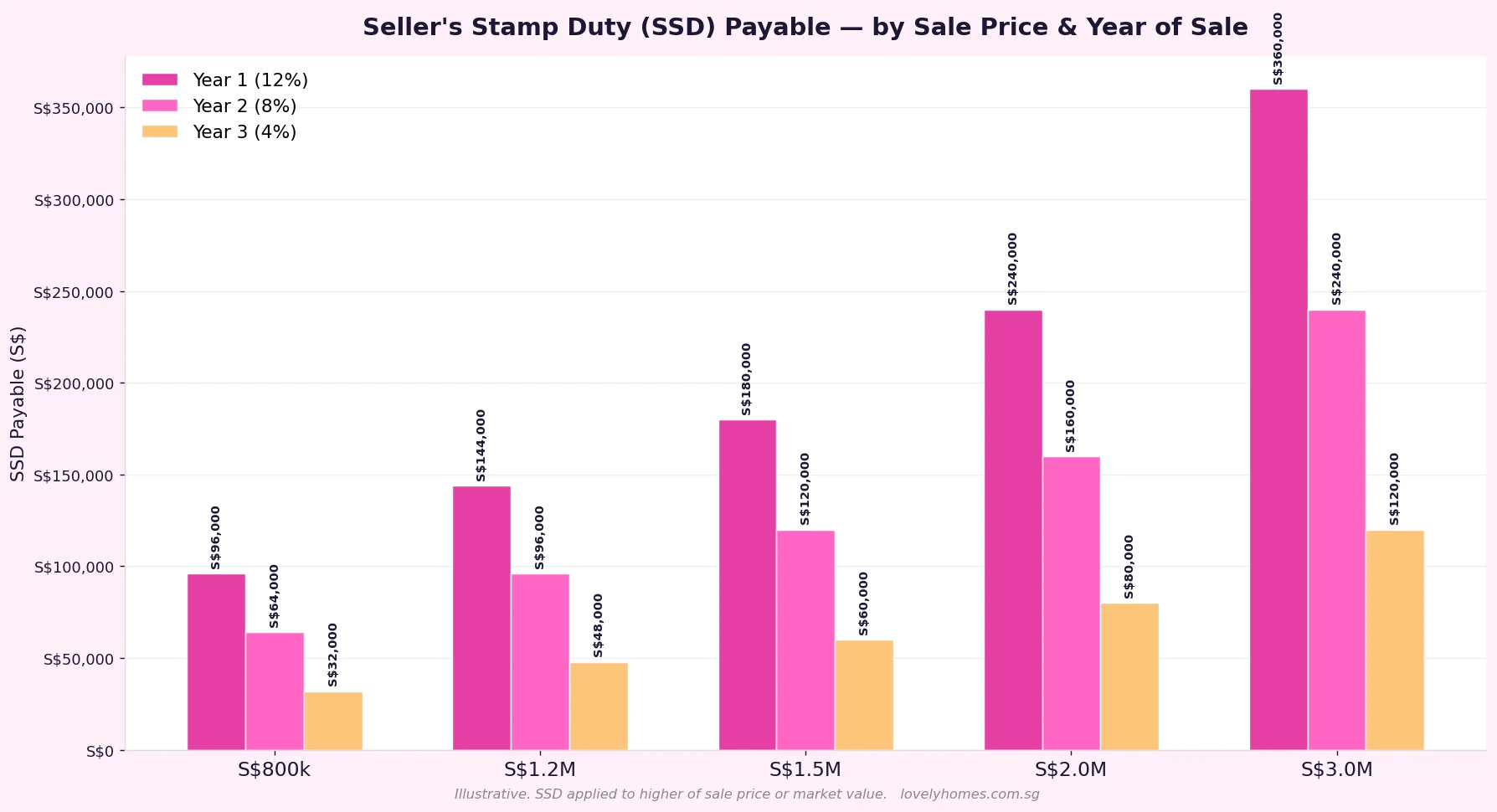

Can I sell an inherited private property immediately, or do I need to wait?

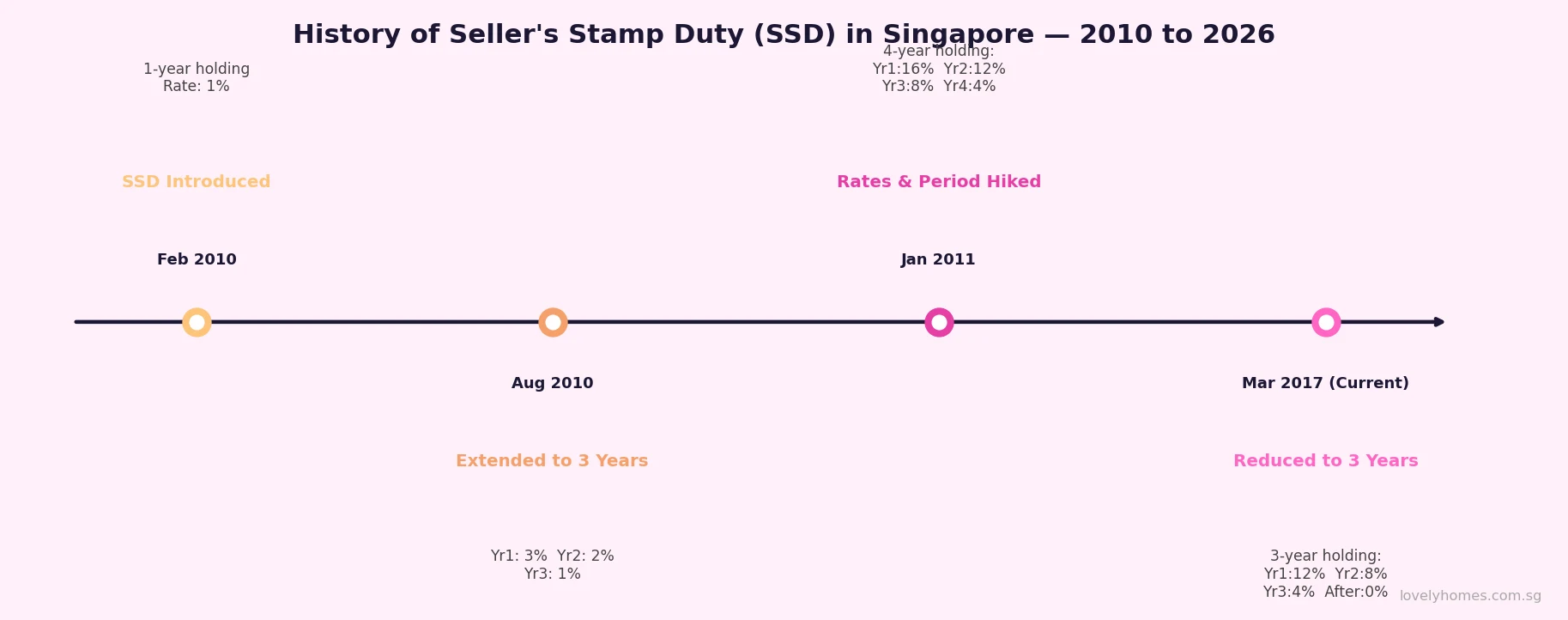

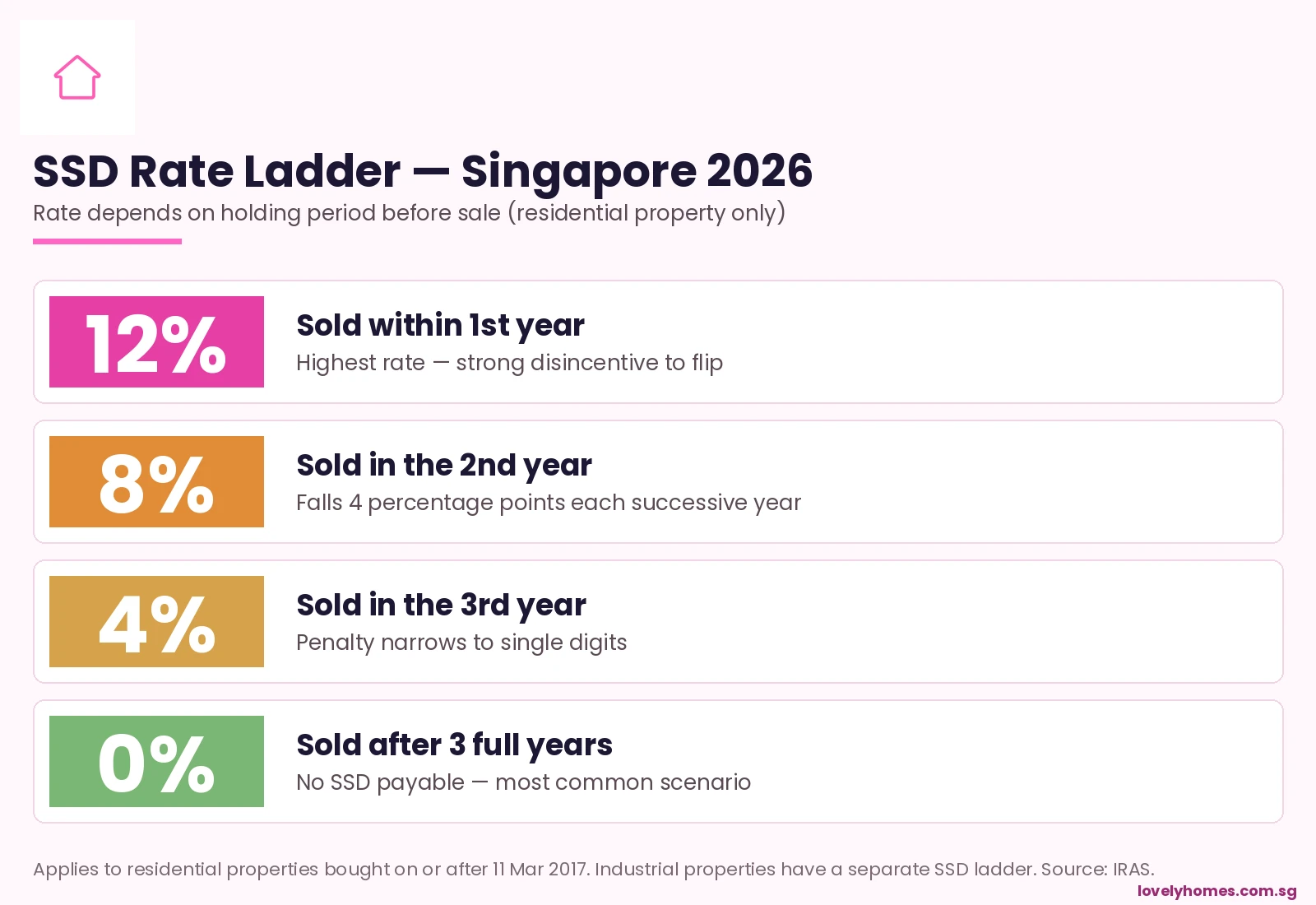

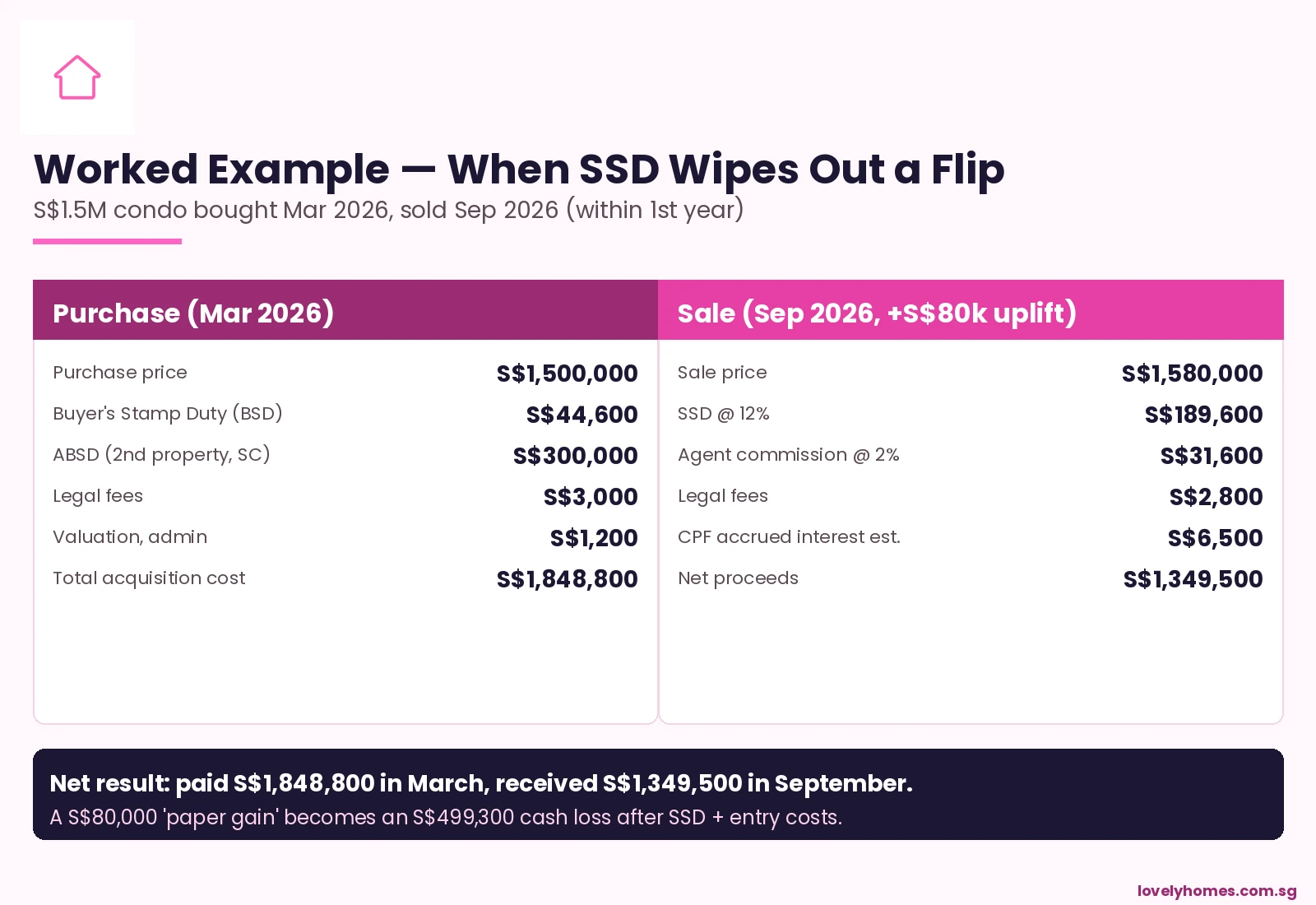

There is no mandatory holding period for private property inherited via an estate. Once the Grant of Probate or Letters of Administration is obtained and the title is assented to you, you can sell the property. However, Seller’s Stamp Duty (SSD) applies if the property is sold within 3 years of the deceased’s purchase date — not from the date you inherited it. SSD is 12%/8%/4% for disposals in the 1st/2nd/3rd year respectively. Check the original purchase date on the title register before deciding to sell quickly after inheritance. For HDB flats, the 5-year MOP from the original flat purchase date must also be observed before the flat can be sold on the open market.

What is the difference between a CPF nomination and a will for property?

A CPF nomination governs your CPF savings only (OA, SA, MediSave balances) and completely overrides your will for those assets. The CPF Board pays out directly to your nominees without going through probate. A will governs your private property, bank accounts, personal assets, and other estate assets — but not CPF savings. If you have bought your property using CPF funds and there is an outstanding CPF accrued interest amount, that is refunded to the CPF account on sale or transfer of the property, and then distributed to your CPF nominees. You should make both a valid will and a CPF nomination to ensure all assets are covered.

Is there any tax payable on inherited property in Singapore?

Singapore abolished estate duty in February 2008. No estate duty or inheritance tax is levied on the value of an estate. The transmission of a property to a beneficiary via will or intestacy is also exempt from Buyer’s Stamp Duty (BSD) and Additional Buyer’s Stamp Duty (ABSD) at the point of transfer. However, once you are registered as the owner of an inherited property, normal property tax (administered by IRAS) applies going forward at the prevailing rates — owner-occupied or non-owner-occupied depending on whether you live in the property. Annual property tax on a S$800,000 private condominium (non-owner-occupied) is approximately S$3,200–S$6,400 depending on the Annual Value assessed by IRAS.

What happens to an inherited HDB flat if none of the beneficiaries are eligible to own it?

If none of the will’s beneficiaries (or ISA-entitled family members) meet HDB’s eligibility criteria to retain the flat — for instance, all of them are foreigners, or they each already own private property — HDB will issue a directive requiring the estate to sell the flat on the open market or surrender it to HDB. If sold on the open market, any SC or PR eligible buyer can purchase it as a resale HDB flat in the normal manner. The net proceeds (after mortgage redemption and CPF refund obligations) are distributed to the estate’s beneficiaries. HDB typically allows up to 12 months for the estate to resolve the flat’s status before taking further action.

How long does probate take in Singapore and how much does it cost?

A straightforward Singapore estate with a valid will, no overseas assets, and no disputes typically takes 4–9 months from death to final distribution. An estate requiring Letters of Administration (no will) adds 1–3 months for additional surety and advertising requirements. Complex estates with foreign property, trust structures, or contested claims can take 12–36 months or more. Professional costs typically include: probate lawyer fees (S$3,500–S$8,000 for a clean estate, higher for complexity), Court filing fees on a sliding scale based on estate value, property assent legal fees (S$1,500–S$3,000 per property), and SLA registration fees (~S$165 per property). The Public Trustee’s Office also charges a fee of 0.75%–2.75% of CPF monies distributed where there is no CPF nomination.

Click anywhere outside the image to close