✔ Quick Answer — Singapore Property Buying Checklist 2026

- 12 steps from budget check to key collection, covering both HDB resale and private property transactions.

- OTP window: 21 days (private resale) or 14 days (HDB resale) to exercise after paying the option fee.

- BSD deadline: Buyer’s Stamp Duty must be paid within 14 days of exercising the OTP/SPA — late payment attracts penalties from IRAS.

- ABSD: SC first property = 0%; SC second = 20%; PR first = 5%; foreigner = 60%. Rates as of 2026.

- TDSR limit: 55% of gross monthly income (MAS ruling) for all property loans; MSR 30% applies additionally for HDB purchases.

- CPF OA can fund the downpayment and monthly instalments — but accrued interest must be returned to CPF on sale.

- Resale timeline: 8–14 weeks from OTP to key collection for private resale; 3–5 years for HDB BTO.

- Upfront costs at S$1.5M (SC first property, no HDB): BSD S$44,600 + 25% downpayment S$375,000 + legal ~S$3,200 ≈ S$423k total cash/CPF required.

Introduction: Why a Checklist Matters More Than Ever in 2026

Singapore’s property market in 2026 is defined by overlapping rules, deadlines and financial thresholds that interact in ways that can catch even experienced buyers off guard. Since the government introduced ABSD remission conditions for upgraders in 2023, revised the BSD progressive rates, extended the TDSR framework, and introduced new EC cooling measures in May 2026, the compliance landscape has become materially more complex than it was five years ago. Missing one deadline — such as the 14-day BSD payment window or the 21-day OTP exercise period — can result in financial penalties, forfeited deposits, or unexpected stamp duty liabilities running into tens of thousands of dollars.

This guide provides a structured, sequenced checklist for buying property in Singapore in 2026. It applies equally to Singapore Citizens (SC), Permanent Residents (PR) and foreigners purchasing private residential property, with specific callouts for HDB buyers. The checklist is administered by four principal government bodies: the Urban Redevelopment Authority (URA) for planning and private property matters; the Housing and Development Board (HDB) for public housing transactions; the Inland Revenue Authority of Singapore (IRAS) for stamp duty collection; and the Central Provident Fund Board (CPF) for CPF withdrawal approvals.

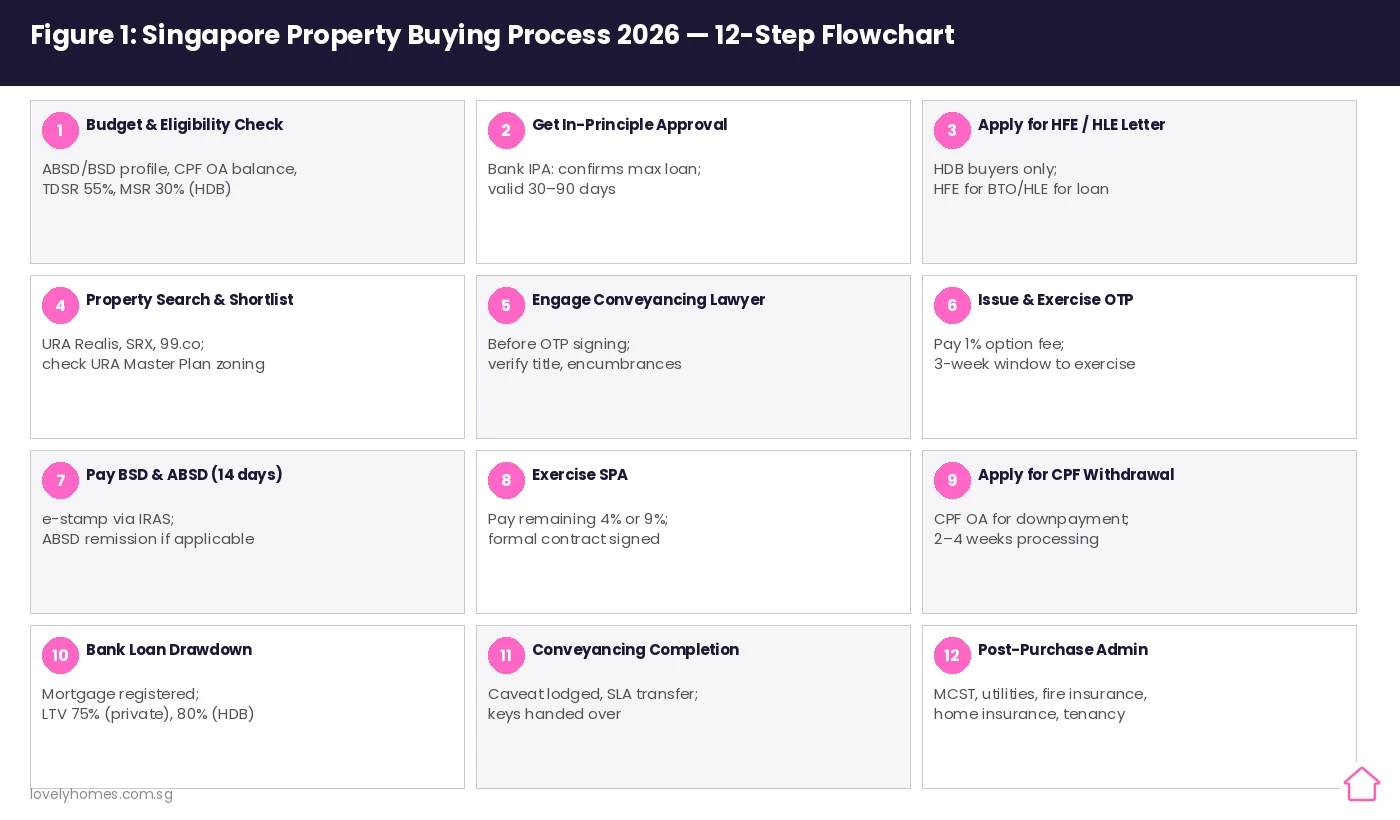

Figure 1: Singapore Property Buying Process 2026 — 12-Step Flowchart from Budget Check to Post-Purchase Admin. Applies to both private resale and HDB resale transactions with noted differences.

The 12-Step Singapore Property Buying Checklist

Phase 1: Pre-Purchase Preparation (Steps 1–5)

Budget and Eligibility Check

Determine your ABSD profile (SC / PR / foreigner; first, second or subsequent property) and calculate your maximum purchase price. Run a TDSR calculation: your total monthly debt obligations — mortgage plus any outstanding car loan, personal loan or credit card minimum — must not exceed 55% of gross monthly income. For HDB purchases, the MSR 30% cap applies to the mortgage alone. Check your CPF OA balance at my.cpf.gov.sg. Confirm your legal eligibility: foreigners may only buy private non-landed property (or Sentosa Cove landed); PRs may buy HDB resale flats but not new BTOs.

Obtain an In-Principle Approval (IPA) from a Bank

Before viewing properties seriously, apply for an IPA (sometimes called AIP — Approval-In-Principle) from at least two banks. The IPA tells you the maximum loan quantum, the indicative interest rate, and the loan tenure available to you. Most banks honour the IPA for 30–90 days. For HDB purchases using the HDB Concessionary Loan, apply for a HDB Loan Eligibility (HLE) letter instead — this has a validity of 6 months and is mandatory before HDB will process your flat application.

HDB Buyers: Apply for HFE Letter

Since May 2023, all HDB flat purchasers (BTO and resale) must obtain a HDB Flat Eligibility (HFE) letter before an OTP can be issued. The HFE confirms your eligibility to buy, the grants you qualify for (EHG, PHG, Step-Up Grant), and the HDB loan amount if applicable. Processing takes approximately 3–4 weeks. Apply at the HDB Flat Portal early in your property search to avoid delays at the OTP stage.

Property Search and Due Diligence

Use URA Realis for verified transaction data (S$2.50 per search or bulk subscription), SRX Property for market trend analysis, and the HDB Resale Flat Prices portal for HDB-specific data. When you shortlist a property, check the URA Master Plan 2019 (or its 2025 revision) to confirm the surrounding land use zoning and any future development plans. Request from the seller or listing agent the Maintenance and Sinking Fund arrears status, the MCST minutes (for strata property), and any outstanding charges on the land title.

Engage a Conveyancing Lawyer Before OTP Signing

Do not sign the OTP without first engaging a conveyancing lawyer. The lawyer’s role is to review the OTP terms, check for encumbrances on the title, liaise with CPF Board and the mortgagee bank, and manage all legal milestones including caveat lodgement. Legal fees for a private resale at S$1–2 million are typically S$2,800–S$4,500 inclusive of disbursements. For HDB resale, fees are lower (S$1,500–S$2,500). Many law firms offer a fixed-fee quote — get at least two quotes before committing.

Phase 2: Option to Purchase and Contract (Steps 6–8)

Issue and Exercise the OTP

The seller issues you an Option to Purchase upon receipt of the option fee (1% of purchase price for private; S$1 for HDB resale). You then have 21 calendar days (private resale) or 14 calendar days (HDB resale) to exercise the OTP by paying the exercise fee (typically 4% for private, making a 5% total deposit; or the agreed sum for HDB). During this window, your lawyer will conduct title searches and CPF checks. Do not let the OTP expire unexercised — the option fee (1%) is forfeited. The OTP is the most time-pressured stage in the entire process.

Pay BSD and ABSD Within 14 Days

Once you exercise the OTP (i.e., sign the Sale and Purchase Agreement or equivalent HDB resale application), both BSD and ABSD must be e-stamped and paid to IRAS within 14 calendar days of signing. Late payment attracts a surcharge of up to S$25 or 4× the unpaid duty, whichever is higher. BSD and ABSD cannot be paid directly from your CPF at this stage — you must first pay in cash, cheque or bank transfer, and may later claim reimbursement from CPF if eligible. Use IRAS’s e-Stamp portal to calculate and pay online.

Execute the Sale and Purchase Agreement

The SPA (or HDB Resale Agreement) is the binding contract that transfers the property. Your lawyer will review the SPA draft before signing. Key items to verify: the correct unit number, floor level, car park lot allocation (if any), existing tenancy (for investment purchases), completion date, and any furniture or fittings being sold with the property. The SPA typically requires payment of the balance of the deposit (if not already paid with the OTP exercise fee) and sets out the completion timeline — usually 8–12 weeks from OTP for resale.

Phase 3: Financing and Completion (Steps 9–12)

Apply for CPF Withdrawal

After the SPA is executed, your lawyer will submit a CPF withdrawal application to the CPF Board on your behalf. Processing typically takes 2–4 weeks. CPF OA funds can be used for: the downpayment (above the 5% minimum cash), legal fees, and monthly mortgage instalments. For private property, the Valuation Limit (VL) and Withdrawal Limit (WL — capped at 120% of VL) govern how much CPF can be used over the life of the property. Plan your CPF usage carefully if you anticipate needing OA funds for retirement.

Bank Loan Drawdown and Mortgage Registration

Your bank will disburse the loan (drawdown) on or before the completion date. The mortgage is registered with the Singapore Land Authority (SLA), and a caveat is lodged to protect your interest in the property. For new launch condominiums, the drawdown is typically progressive (tied to construction milestones under the Normal Payment Scheme) or deferred (no longer an option for EC sites tendered from May 2026, when DPS was abolished for new EC GLS sites). Ensure your fire insurance is in place before drawdown — most banks require this as a condition of the mortgage.

Completion — Key Collection

Completion is the day the ownership transfers to you. Your lawyer will attend the completion appointment, where the balance of the purchase price is paid to the seller’s lawyers (net of any CPF retention and existing mortgage redemption). The SLA updates the land register, and you collect the keys. For resale properties, inspect the property thoroughly on the day of completion — check all fittings and appliances against the SPA schedule, and document any defects in writing to the seller immediately.

Post-Purchase Administration

After key collection: register with the Management Corporation Strata Title (MCST) for strata properties and pay any outstanding Maintenance and Sinking Fund contributions. Activate utilities (SP Group, NTUC FairPrice Gas). Set up a home contents insurance policy. If you are renting out the property, register the tenancy with HDB (for HDB subletting) or comply with URA’s short-term rental rules (minimum 3-month tenancy for private residential). Inform IRAS of rental income for the relevant Year of Assessment — failure to declare rental income is an offence under the Income Tax Act.

Key Deadlines and Cost Summary

| Milestone | Deadline from OTP | Amount / Action | Payable To |

|---|---|---|---|

| OTP Exercise (Private) | Within 21 calendar days | 4% exercise fee (total 5% deposit) | Seller (via lawyer) |

| OTP Exercise (HDB Resale) | Within 14 calendar days | As agreed in OTP | HDB Resale Portal |

| BSD & ABSD Payment | Within 14 days of SPA signing | BSD 1%–6% progressive; ABSD 0%–60% | IRAS (e-Stamp Portal) |

| CPF Withdrawal Application | After SPA execution | 2–4 weeks processing | CPF Board (via lawyer) |

| Completion (Private Resale) | 8–12 weeks from OTP | Balance purchase price | Seller (via lawyer) |

| Completion (HDB Resale) | 8–10 weeks from HDB approval | Balance purchase price | HDB |

| Fire Insurance | Before loan drawdown | ~S$150–S$400/yr depending on sum insured | Licensed insurer |

| Rental Income Declaration | By 18 April each YA | Declare via myTax Portal to IRAS | IRAS |

Worked Example: Ms Lim, SC First-Time Buyer — OCR Condo at S$1.1M

📊 Case Study — Ms Lim, Singapore Citizen, Single, Income S$8,000/mth

Property: 1-bedroom resale condo in Tampines (OCR), 560 sq ft at S$1,930 psf = S$1,080,800 (rounded to S$1.08M).

ABSD: S$0 — SC purchasing first residential property. No ABSD applies.

BSD Calculation:

- First S$180,000 × 1% = S$1,800

- Next S$180,000 × 2% = S$3,600

- Next S$640,000 × 3% = S$19,200

- Remaining S$80,000 × 4% = S$3,200

- Total BSD: S$27,800

Financing: Bank loan at LTV 75% = S$810,000. At 3.0% p.a. over 30 years: approximately S$3,413/month. TDSR: S$3,413 ÷ S$8,000 = 42.7% — within the 55% TDSR limit. Ms Lim qualifies without a joint borrower.

Downpayment: 25% = S$270,000. Minimum 5% cash = S$54,000. Balance S$216,000 from CPF OA.

Legal Fees (Buyer): approximately S$3,000 including disbursements (caveat, SLA searches, CPF liaison).

Total Upfront Cash/CPF Required: BSD S$27,800 (cash) + Downpayment S$270,000 (S$54k cash + S$216k CPF) + Legal S$3,000 ≈ S$300,800 (including minimum S$81,800 in cash).

Checklist Critical Date: OTP issued Day 0. Ms Lim must exercise by Day 21, pay BSD within 14 days of SPA signing, and complete within ~10 weeks of OTP. Her lawyer sets a calendar reminder for Day 18 to ensure OTP exercise happens before the deadline.

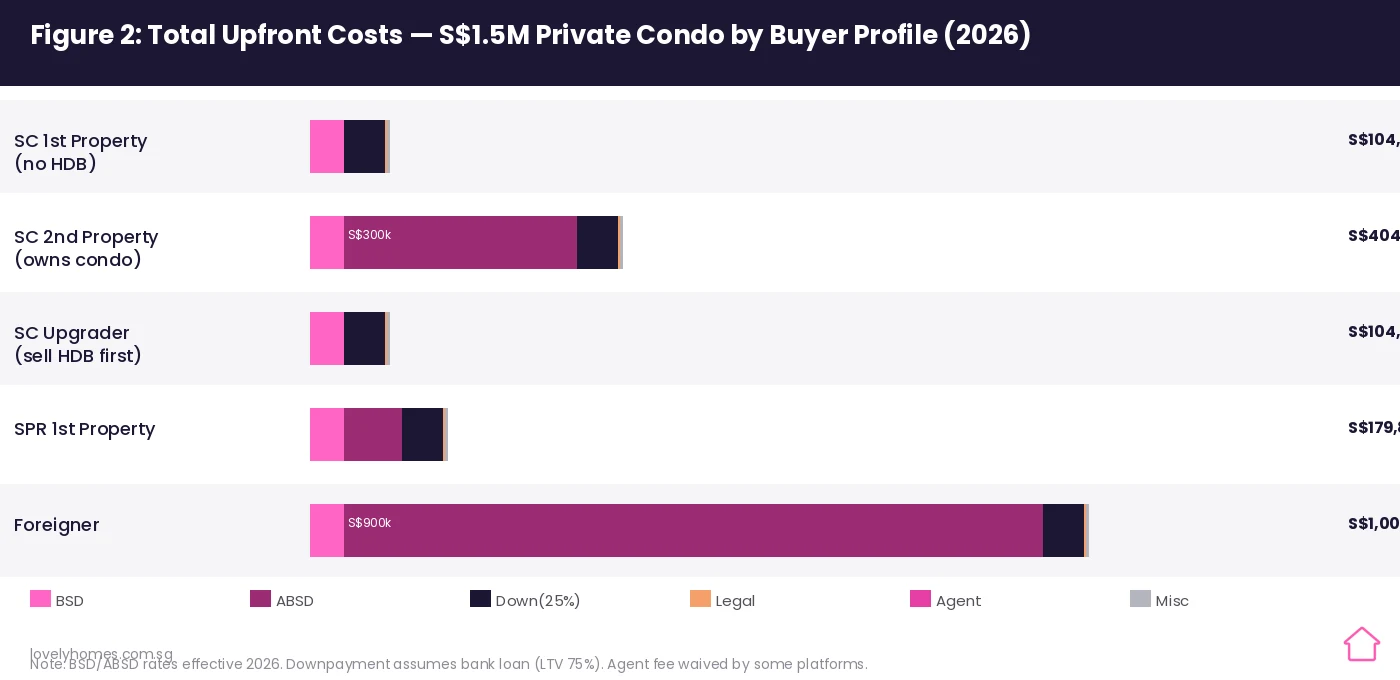

Figure 2: Total Upfront Costs at S$1.5M — BSD, ABSD, Downpayment and Legal by Buyer Profile 2026. Note: ABSD of S$900,000 for foreigners makes the effective total cost S$1.45M above and beyond the purchase price — a near-doubling of the upfront outlay.

Why the 2026 Regulatory Landscape Demands Extra Care

The Singapore property market has accumulated layer upon layer of regulatory measures since the first cooling round in 2009. As of 2026, a buyer simultaneously navigates BSD (four-tier progressive, administered by IRAS), ABSD (five-tier by residency and ownership count, administered by IRAS), TDSR (MAS-mandated income test, enforced by banks), MSR (HDB/EC purchases only, administered by HDB and banks), CPF Withdrawal Limits (CPF Board), ABSD remission conditions for upgraders (IRAS), EC cooling measures (MND/HDB, revised May 2026), and rental restriction rules (URA, SLA). None of these systems talk to each other automatically — the buyer’s lawyer is the only party who checks the full suite in one place.

This is precisely why engaging a conveyancing lawyer before signing the OTP is not optional. Singapore Law Society guidelines permit a lawyer to act for both buyer and mortgagee bank in the same transaction, but the lawyer’s primary duty is to the client. First-time buyers should ensure they understand each cost line before OTP day, not the morning they are asked to sign.

What Might Come Next: Tech-Enabled Property Transactions

URA and HDB are actively developing digital streamlining tools that may, in future, consolidate several of the 12 steps above. The HFE letter introduced in May 2023 already replaced three separate application processes. Industry participants have proposed that BSD and ABSD e-stamping be integrated directly into the OTP workflow so that buyers receive a real-time stamp-duty estimate at the point of OTP issuance. CPF Board’s e-conveyancing integration has progressively reduced the time for CPF withdrawal approvals from six weeks (pre-2020) to the current two-to-four weeks. It is reasonable to expect that a future iteration of the conveyancing process reduces total timeline from the current 8–14 weeks to under 6 weeks for straightforward resale transactions.

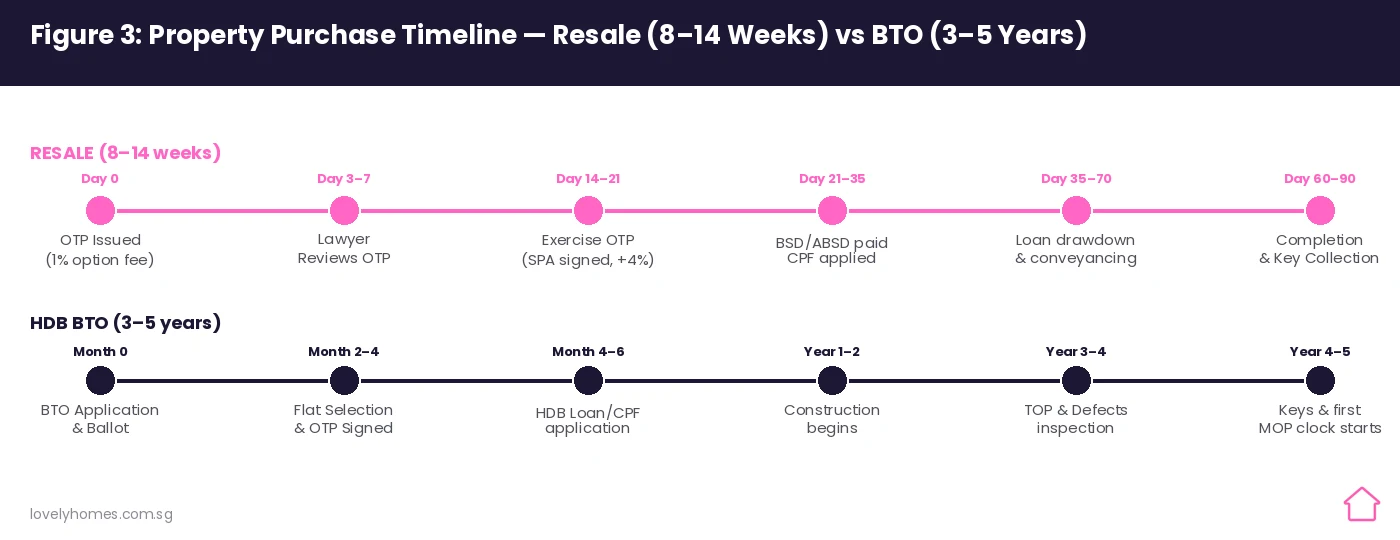

Figure 3: Purchase Timeline Comparison — Resale (8–14 weeks) vs HDB BTO (3–5 years). BTO buyers must manage cash flow, CPF accrual and bank loan conditions across a multi-year period before receiving keys.

Frequently Asked Questions

What happens if I miss the 21-day OTP exercise window?

If you do not exercise the OTP within the prescribed period (21 calendar days for most private resale transactions), the OTP lapses automatically. The seller retains your option fee (typically 1% of the purchase price) as a forfeiture. There is no legal recourse unless the seller agreed in writing to extend the option period. Given the financial stakes — 1% of S$1.5 million is S$15,000 — always ensure your lawyer, bank and CPF paperwork are already in progress before the OTP is issued, not after.

Can I use CPF to pay BSD or ABSD?

No — not directly at the point of payment. BSD and ABSD must be paid to IRAS within 14 days of signing the SPA, and IRAS does not accept CPF funds directly. You must pay in cash (bank transfer, FAST, cheque). However, once the property is legally stamped and the CPF withdrawal is approved, you may use CPF OA funds to reimburse yourself for the BSD paid (subject to the property’s Valuation Limit and your remaining CPF balance). ABSD, by contrast, is generally not reimbursable from CPF in this manner — it must be funded from personal cash.

What is the ABSD remission for Singapore Citizen couples upgrading from HDB?

Singapore Citizen married couples who own an HDB flat and purchase a second residential property (typically a private condo) are liable for 20% ABSD on the new purchase. However, they may apply to IRAS for an ABSD remission under the Married Couple Remission, provided they sell their existing HDB flat within 3 years of the private property’s stamp duty date (for resale) or 3 years from the property’s TOP date (for new launch). The ABSD is paid upfront in full, and the refund is processed after the HDB sale is confirmed. The refund does not include the interest cost of funding the ABSD during the interim period — a real but often-overlooked carrying cost.

How much cash do I need on hand to buy a S$1.5M private condo as a first-time SC buyer?

The minimum cash requirement (amounts that cannot be funded from CPF) is: (1) at least 5% of the purchase price as downpayment cash = S$75,000; (2) BSD S$44,600 paid in cash upfront (reimbursable from CPF later); (3) legal fees approximately S$3,200 (usually payable from CPF for private property). So the hard minimum cash outflow is approximately S$75,000 + S$44,600 = S$119,600, plus any miscellaneous costs. In practice, buyers should have S$130,000–S$150,000 in cash for comfortable headroom, with the remaining S$225,000–S$300,000 (balance downpayment) coming from CPF OA.

What is TDSR and how does the bank calculate it?

The Total Debt Servicing Ratio (TDSR) framework, mandated by MAS since 2013 and revised in 2022, caps your total monthly debt obligations at 55% of gross monthly income. “Debt obligations” include: the new property mortgage instalment, any existing home loan instalments, car loan instalments, and the minimum monthly repayment on credit cards (calculated at 5% of outstanding balance under MAS rules). The bank stress-tests your mortgage at a medium-term interest rate (typically 4.0%–4.5% for TDSR calculation purposes, regardless of the actual rate offered) to ensure affordability even in a rising-rate environment. Exceeding 55% TDSR means the bank cannot approve the loan; reducing outstanding credit card debt or settling the car loan before applying can meaningfully improve your TDSR headroom.

Does the checklist apply to buying a HDB BTO flat?

The BTO process differs significantly from resale in timing but not in regulatory obligations. BTO buyers apply during the sales exercise (quarterly or otherwise), ballot for a flat, select a unit, sign the Agreement for Lease (not an OTP), and make progress payments over the construction period — which can span 3–5 years. BSD applies and must be paid within 14 days of signing the Agreement for Lease. ABSD applies at the point of signing. CPF can be used from the point of agreement signing, subject to HFE confirmation. The HDB Loan (2.6% pegged to CPF OA + 0.1%) is available for BTO buyers who meet income and eligibility criteria; bank loans are also permitted.

0 Comments