✔ Quick Answer — Paya Lebar Property Investment 2026

- Location: Planning Area of Geylang, District 14 (D14), classified as Rest of Central Region (RCR) by URA.

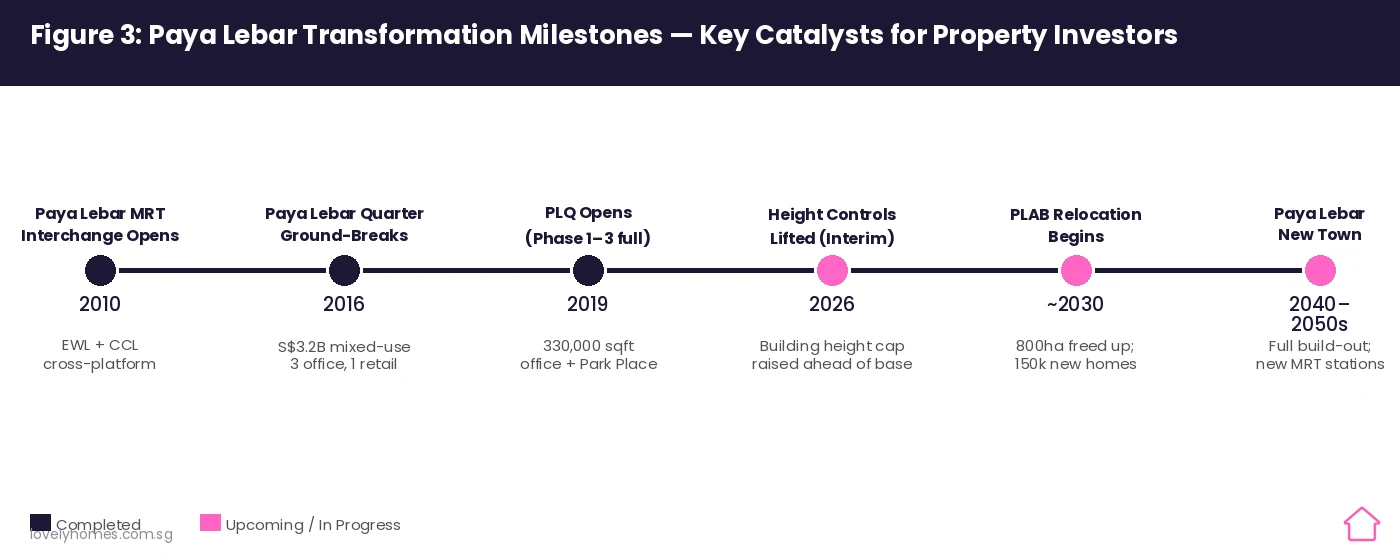

- Connectivity: Paya Lebar MRT is the only EWL-CCL interchange outside the city centre — 5 stops to City Hall (Raffles Place).

- HDB Resale Prices: S$430,000–S$980,000 depending on flat type and floor; median 4-room transacted at S$693,000 in Q1 2026.

- Private Condo Prices: S$1,100–S$2,200 psf for RCR condominiums near the MRT interchange; Park Place Residences averages S$2,245 psf.

- Gross Rental Yield: 3.2%–3.8% for HDB subletting; 3.4%–3.8% for private condos — among the stronger RCR yields.

- 5-Year Capital Growth: Private RCR condos in D14 have appreciated approximately 14%–19% over five years (2021–2026), driven by PLQ and the upcoming airbase uplift.

- Major Catalyst: Paya Lebar Airbase (PLAB) relocation from ~2030 will free 800 hectares — bigger than Bishan — for a new town with up to 150,000 new homes, and allows taller buildings in surrounding estates now.

- ABSD 2026: Singapore Citizens purchasing a first property pay 0% ABSD; second property 20%. Permanent Residents: 5% first, 30% second. Foreigners: 60%.

Introduction: Why Paya Lebar Stands Apart in Singapore’s Property Market

Paya Lebar occupies a rare position in the Singapore property landscape: it is simultaneously a mature estate with affordable HDB resale options, a thriving commercial node anchored by Paya Lebar Quarter (PLQ), and the ground-zero beneficiary of one of the most consequential land-release decisions the government has ever made — the scheduled relocation of Paya Lebar Airbase from approximately 2030 onwards. Few Singapore locations combine near-term rental demand, established transport infrastructure, and a decade-long uplift story quite so neatly.

Administered by the Urban Redevelopment Authority (URA) under the Geylang Planning Area, Paya Lebar sits in District 14 (D14) and is classified as the Rest of Central Region (RCR) — the city-fringe band that historically delivers stronger capital growth than the Outer Central Region (OCR) while remaining meaningfully more affordable than the Core Central Region (CCR). Buyers who purchased in the RCR a decade ago have seen private residential prices rise approximately 49% from 2016 to Q1 2026, compared with 40% for the CCR and 73% for the OCR, according to URA Property Price Index data.

This guide analyses Paya Lebar’s property market as of Q1 2026: current prices across all property types, rental yields, the five key catalysts driving value, a worked buyer analysis, and a realistic forward outlook.

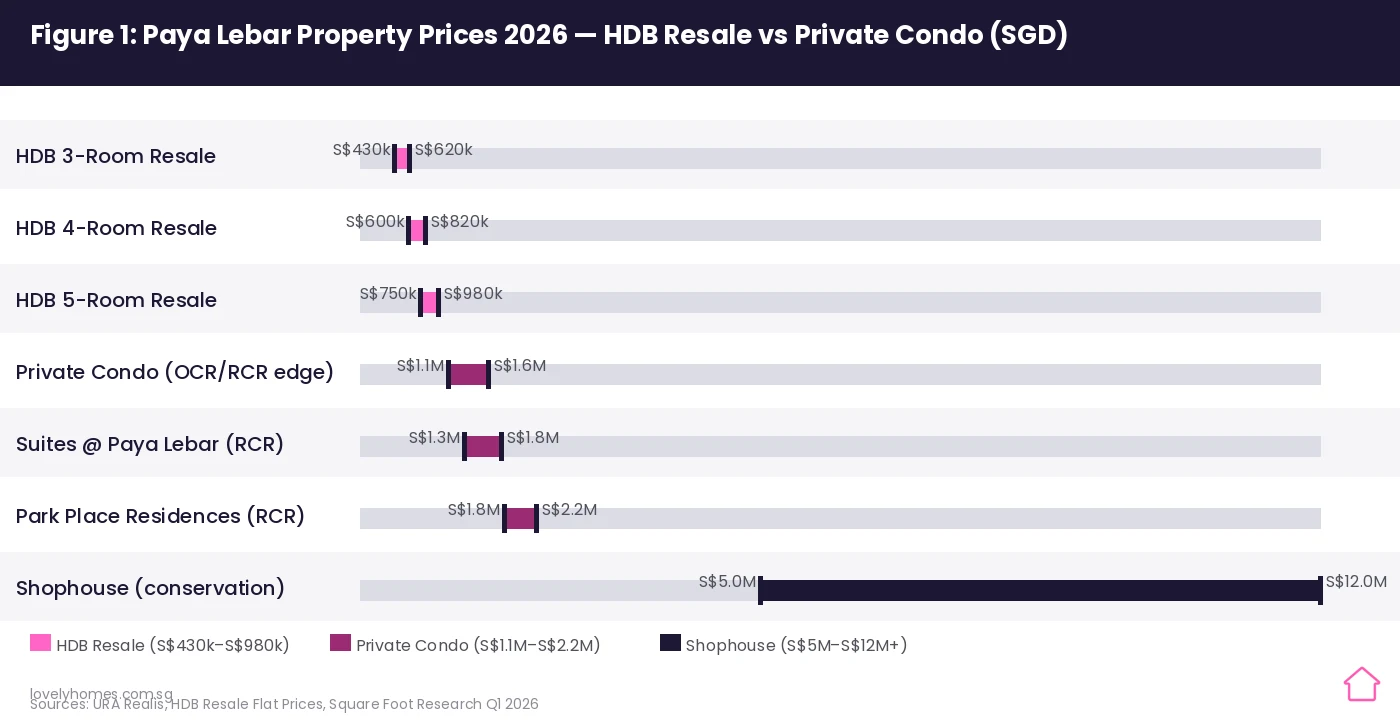

Figure 1: Paya Lebar Property Prices 2026 — HDB Resale vs Private Condo vs Shophouse (SGD range by property type). Source: URA Realis, HDB Resale Flat Prices, Square Foot Research Q1 2026.

Paya Lebar’s Five Value Catalysts in 2026

Investment theses for Singapore property typically rest on one or two structural drivers. Paya Lebar currently offers five simultaneously active catalysts — an unusually concentrated set for a single planning area.

1. The MRT Interchange Advantage

Paya Lebar MRT station is one of only a handful of interchange stations outside the city centre where two different MRT lines converge on the same platform. Commuters can board the East-West Line (EWL) and reach Raffles Place in approximately nine minutes, or switch to the Circle Line (CCL) and access Dhoby Ghaut or Harbourfront without a bus connection. This dual-line access raises the effective connectivity score for both residents and business tenants, supporting rental demand from professionals working across multiple corporate corridors.

2. Paya Lebar Quarter and the Commercial Hub Effect

The S$3.2 billion Paya Lebar Quarter, developed by Lendlease, opened progressively between 2018 and 2020. It comprises three Grade-A office towers (totalling approximately 840,000 sq ft of NLA), PLQ Mall (340,000 sq ft retail), and the Park Place Residences condo, all connected to the MRT concourse. PLQ has repositioned Paya Lebar from a light-industrial estate into a fully-fledged decentralised business hub — attracting financial services, technology and media tenants who previously gravitated exclusively to the CBD or one-north. The presence of multinational office tenants directly underpins rental demand for nearby residential units.

3. Airbase Relocation: Singapore’s Most Significant Land-Release Event

The Ministry of Defence confirmed that Paya Lebar Airbase will begin relocating from approximately 2030. The airbase and surrounding industrial buffer zones occupy more than 800 hectares — an area larger than Bishan or Ang Mo Kio new town. URA has indicated that the freed land will accommodate up to 150,000 new homes and allow for new MRT stations. Critically, URA has already lifted the height restrictions that existed in surrounding estates as a safety buffer for aircraft approaches. Buyers in Paya Lebar and Geylang today are acquiring before this transformation is priced in.

4. Height Restriction Relaxation (Interim, from 2024–2025)

Ahead of the formal airbase departure, URA has progressively relaxed the building height caps that previously constrained development in D14. This makes remaining land parcels more developable, increases the plot ratio potential of future GLS sites in the area, and signals to the market that taller, denser residential development is coming. Every new height-approved project adds to the estate’s skyline and reinforces its transition from industrial fringe to urban node.

5. Shophouse Scarcity and Conservation Premiums

Paya Lebar Road and the surrounding conservation areas contain a cluster of two- and three-storey pre-war shophouses listed on the URA Conservation Map. With only a finite number of these buildings in existence and rising demand from food-and-beverage operators, boutique offices, and high-net-worth collectors, conservation shophouse transactions in D14 have reached S$5,000,000–S$12,000,000+ depending on lot size and street frontage. This is not a mass-market play, but for investors seeking inflation-resistant assets with unique character, Paya Lebar shophouses command a meaningful scarcity premium.

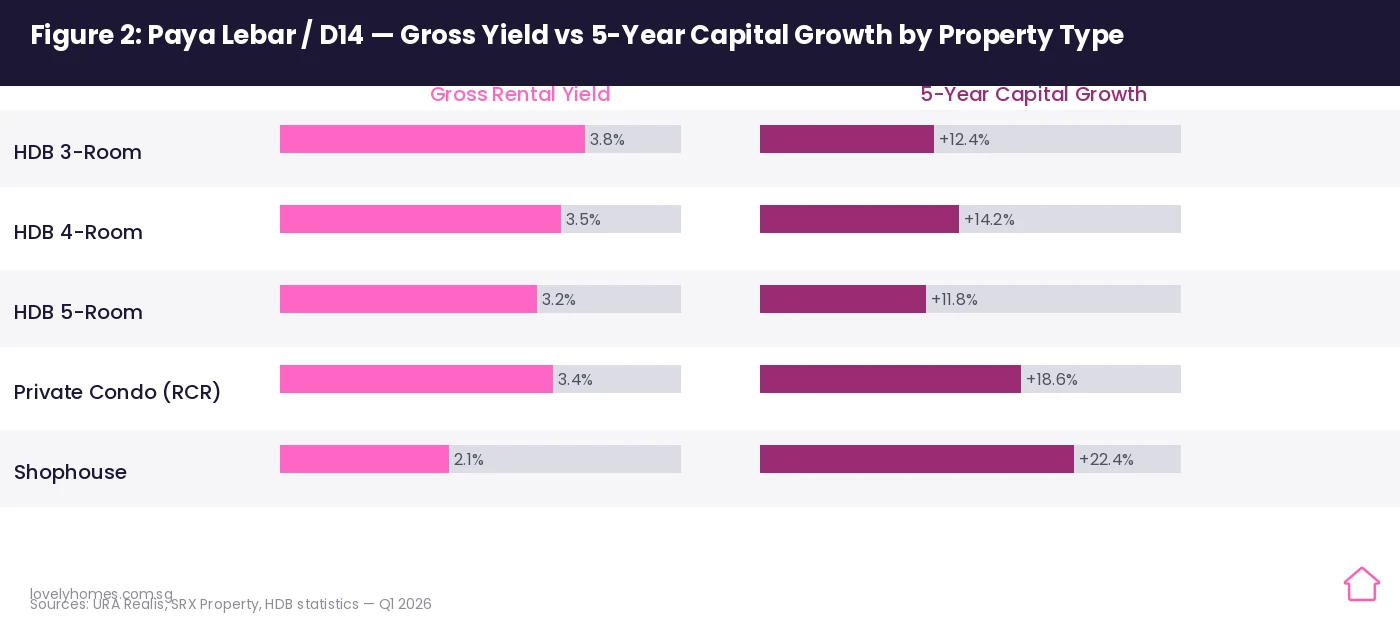

Figure 2: Paya Lebar / D14 — Gross Rental Yield vs 5-Year Capital Growth by Property Type. Source: URA Realis, SRX Property, HDB Statistics Q1 2026.

Current Market Prices and Rental Data (Q1 2026)

Property prices in Paya Lebar span an exceptionally wide range depending on property type, allowing investors with different capital levels to participate in the same location story.

HDB Resale Prices

HDB resale transactions in the Paya Lebar and surrounding Geylang/Kampong Ubi subzones reflect a mature, liquid market. Based on Q1 2026 HDB Resale Flat Prices data, 3-room flats typically change hands at S$430,000–S$620,000; 4-room flats at S$600,000–S$820,000; and 5-room flats at S$750,000–S$980,000. These represent meaningful value relative to comparable RCR-adjacent neighbourhoods. No HDB BTO supply is being launched in the Geylang planning area in 2025–2026, which keeps resale demand firm against a constrained new supply.

Private Condominium Prices (PSF)

Private condominiums in D14 / RCR Paya Lebar operate in a clearly delineated price band. Older strata developments such as Suites @ Paya Lebar have transacted at an average of approximately S$1,492 psf, with units ranging from S$969 to S$1,769 psf depending on level and facing. Park Place Residences, part of PLQ and the area’s premium address, has seen transactions at S$2,245–S$2,600 psf. For a typical two-bedroom unit of approximately 700 sq ft in the S$1,400–S$1,600 psf range, this translates to an all-in purchase price of S$980,000–S$1,120,000 — placing Paya Lebar well within reach of HDB upgraders.

Summary: Paya Lebar Property at a Glance

| Property Type | Price Range | Typical PSF | Gross Yield | 5-Yr Capital Growth |

|---|---|---|---|---|

| HDB 3-Room Resale | S$430k–S$620k | S$520–S$680 | 3.8% | +12.4% |

| HDB 4-Room Resale | S$600k–S$820k | S$480–S$640 | 3.5% | +14.2% |

| HDB 5-Room Resale | S$750k–S$980k | S$470–S$580 | 3.2% | +11.8% |

| Private Condo (RCR) | S$1.1M–S$2.2M | S$1,492–S$2,600 | 3.4%–3.8% | +14%–+19% |

| Shophouse (Conservation) | S$5M–S$12M+ | varies | 2.1%–2.8% | +18%–+22% |

Worked Example: Buying a Resale Condo in Paya Lebar 2026

📊 Case Study — Mr & Mrs Ng, Singapore Citizens, Joint Income S$11,000/mth

Property: 2-bedroom resale condo near Paya Lebar interchange, 850 sq ft at S$1,550 psf = S$1,317,500 (rounded to S$1.32M for this example).

ABSD: S$0 — SC purchasing their first private property after selling their HDB flat within the 3-year remission window. ABSD remission applies if HDB is sold within 3 years of the new private property purchase.

BSD Calculation:

- First S$180,000 × 1% = S$1,800

- Next S$180,000 × 2% = S$3,600

- Next S$640,000 × 3% = S$19,200

- Remaining S$320,000 × 4% = S$12,800

- Total BSD: S$37,400

Financing: Bank loan at LTV 75% = S$990,000. At 3.0% p.a. over 25 years: approximately S$4,689/month. TDSR check: S$4,689 ÷ S$11,000 = 42.6% — comfortably within the 55% TDSR limit.

Downpayment: 25% = S$330,000 (minimum 5% cash = S$66,000; remainder from CPF OA).

Estimated Gross Rental Income: S$4,200–S$4,800/mth for a 2-bedroom near PLQ (based on SRX Q1 2026 data).

Net Yield: Using mid-point rental S$4,500/mth and assuming 92% occupancy: (S$4,500 × 12 × 0.92 – S$3,600 maintenance – S$1,200 property tax) ÷ S$1,320,000 ≈ 3.4% gross yield.

5-Year Capital Gain Scenario: At historical RCR growth of 3% p.a., the property appreciates to ~S$1.53M — a capital gain of ~S$210,000 before selling costs.

Why Paya Lebar Matters for the Singapore Property Market

The Paya Lebar investment case is not merely a local neighbourhood story — it is a preview of what Singapore’s urban transformation looks like in practice. The government’s approach follows a consistent playbook: anchor commercial infrastructure (PLQ), improve transport connectivity (MRT interchange), then announce a major catalyst (airbase relocation) while managing price expectations by releasing sufficient supply. Investors who understand this sequencing — commercial before residential, infrastructure before announcement — can position themselves ahead of the formal re-rating.

By regional comparison, Singapore’s RCR yields of 3.4%–3.8% compare favourably with equivalent city-fringe assets in Sydney (2.5%–3.0%), London (2.8%–3.3%), and Tokyo (3.0%–3.5%), while Singapore’s political stability, rule of law, and lack of capital gains tax on property remain structural advantages for long-term holders.

What Might Come Next: The 10-Year Paya Lebar Outlook

The forward-looking case rests heavily on the airbase relocation timeline. Should PLAB vacate on schedule from 2030, URA’s masterplan for the freed land is expected to include new MRT stations on a future transit line, a new town-centre precinct, and a mix of public and private housing. Based on precedents such as the Bidadari transformation (former Bidadari cemetery, now a mature estate with strong price appreciation), land-release events of this scale typically generate 20%–35% above-market appreciation in immediately surrounding estates within a decade of the announcement crystallising into visible construction. That uplift potential has not yet been fully priced into Paya Lebar property values.

Disclaimer: This is speculation based on public information. Actual timelines depend on Ministry of Defence operational decisions and URA planning processes, both of which are subject to change.

Figure 3: Paya Lebar Transformation Milestones — From MRT Interchange (2010) to Airbase New Town (2040s). Source: URA, MND, Lendlease public filings.

Frequently Asked Questions

Is Paya Lebar a good area to buy property in 2026?

Paya Lebar offers a compelling combination of mature-estate stability and long-term uplift potential that is rare in the Singapore market. The Paya Lebar Airbase relocation, scheduled to begin from approximately 2030, will free 800 hectares for a new town — an event with no parallel in recent Singapore history. However, buyers should note that the uplift is a decade-long play, not an immediate re-rating. In the near term, Paya Lebar benefits from strong rental demand driven by PLQ office tenants, excellent dual-line MRT connectivity, and no new HDB BTO supply in the immediate area, all of which support occupancy and resale liquidity.

What are the restrictions on foreigners buying Paya Lebar property?

Foreigners may purchase private condominium units in Paya Lebar without restriction, subject to the 60% Additional Buyer’s Stamp Duty (ABSD) effective from 27 April 2023. Foreigners cannot purchase HDB flats or landed property (with very limited exceptions for Sentosa Cove). For a S$1.5 million condo, a foreign buyer would pay BSD of approximately S$44,600 plus ABSD of S$900,000, making the total tax impost S$944,600 before legal fees — a substantial barrier that effectively prices out most foreign retail investors at current levels.

How does Paya Lebar compare to Geylang as an investment location?

Paya Lebar and Geylang are part of the same URA Planning Area but serve distinct investment profiles. Paya Lebar is focused on the PLQ commercial hub, MRT interchange, and the airbase redevelopment story — it is a structural, multi-decade investment case. Geylang proper (particularly Districts 7 and 14 east) has historically attracted investors for its very high gross rental yields (4.0%–5.0%) driven by the area’s unique occupancy mix, but has seen more modest capital appreciation. For buyers prioritising long-term capital growth over immediate yield, Paya Lebar’s positioning near PLQ is generally considered the stronger play. LovelyHomes has published a detailed Geylang Neighbourhood Guide and a Geylang East & Kallang Investment Guide for comparative reference.

Can I use CPF to buy a Paya Lebar condo?

Yes. Singapore Citizens and Permanent Residents may use their CPF Ordinary Account (OA) savings to fund the downpayment and monthly mortgage instalments on private property purchases, subject to the Valuation Limit (VL) and Withdrawal Limit (WL). For a property purchased below the VL, CPF can be used without restriction; above the VL, cumulative CPF withdrawals are capped at 120% of the VL. Interest accrued on the CPF used must be returned to the CPF account upon sale, which reduces the net cash proceeds received at exit. Buyers should model this CPF accrual carefully, especially if they intend to hold the property for fewer than ten years.

What is the minimum income needed to buy a Paya Lebar condo in 2026?

For a two-bedroom resale condo at approximately S$1.2 million, the bank loan at 75% LTV is S$900,000. At a 25-year loan at 3.0% per annum, the monthly instalment is approximately S$4,271. Under the 55% Total Debt Servicing Ratio (TDSR) set by MAS, the minimum gross monthly income required (assuming no other debt obligations) is approximately S$7,766 per month for a single borrower, or a lower threshold achievable jointly. In practice, banks typically look for a comfortable buffer, so a gross monthly income of S$9,000–S$10,000 (single) or S$14,000–S$16,000 (joint) is more realistic when factoring credit card obligations and car loans.

Will the airbase relocation happen on time, and what if it is delayed?

The Ministry of Defence has confirmed the relocation is on track to begin “around 2030 or beyond,” but has not committed to a specific completion date for the military move. Partial relocation — freeing some of the 800 hectares while the rest continues operating — is a realistic scenario that would allow URA to commence planning and early rezoning without waiting for a full departure. Even a partial or phased relocation is likely to be a significant catalyst. The risk of delay is real, and buyers pricing in a 2030 event should assess whether their investment thesis holds without it, given that Paya Lebar already generates credible standalone yields of 3.4%–3.8%.

Are there any HDB upgrader pitfalls specific to Paya Lebar?

The primary pitfall for HDB upgraders purchasing a private Paya Lebar condo is the ABSD trap: if you purchase the private property before selling your HDB flat, you will be liable for 20% ABSD on the new purchase (on top of BSD). For a S$1.3 million condo, that ABSD is S$260,000. You can apply for an ABSD remission as a Singapore Citizen couple, but you must sell the HDB within three years and the refund only comes after the sale is confirmed. Always ensure your HDB sale is completed, or at least the OTP exercised and sale unconditional, before committing to a private property purchase — or plan the timing very carefully with your conveyancing lawyer.

0 Comments