Kallang and Geylang East sit at one of Singapore’s most compelling property crossroads in 2026: an RCR location priced well below the regional average, a government masterplan injecting S$1 billion into a sports and lifestyle precinct, and a freshly awarded Government Land Sale (GLS) site that will deliver a new private residential project to the area by 2028. For investors and upgraders who missed the Queenstown and Toa Payoh price runs, Kallang offers a credible second chance — at a meaningful discount.

This guide covers everything property buyers and investors need to know about Kallang and the adjacent Geylang East cluster in 2026: location and subzones, price benchmarks, rental demand, the Kallang Alive Masterplan, the latest GLS award, worked investment examples, and the buyer strategies that make sense at current valuations.

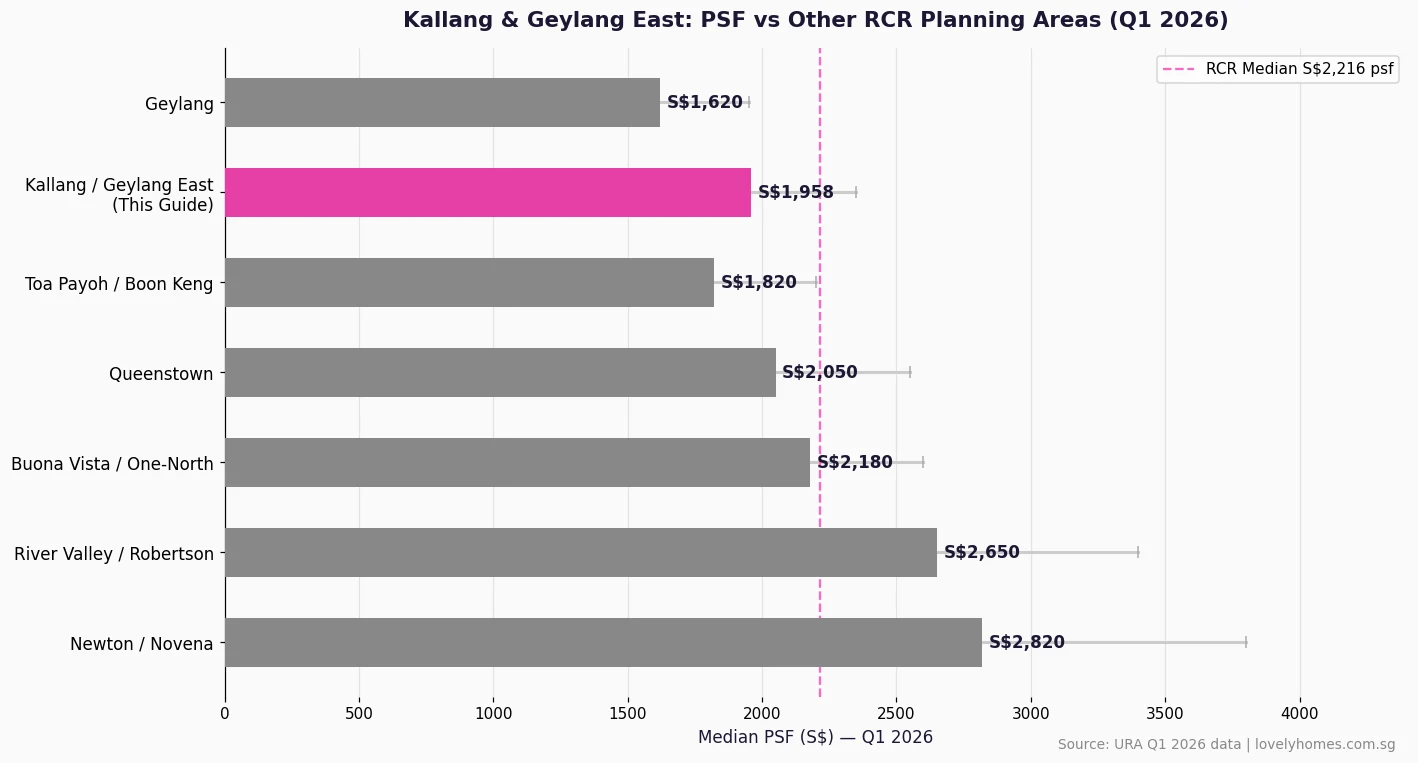

- Kallang sits in the Rest of Central Region (RCR) with a median PSF of S$1,958 in Q1 2026 — about S$258 below the RCR average of S$2,216, offering relative value.

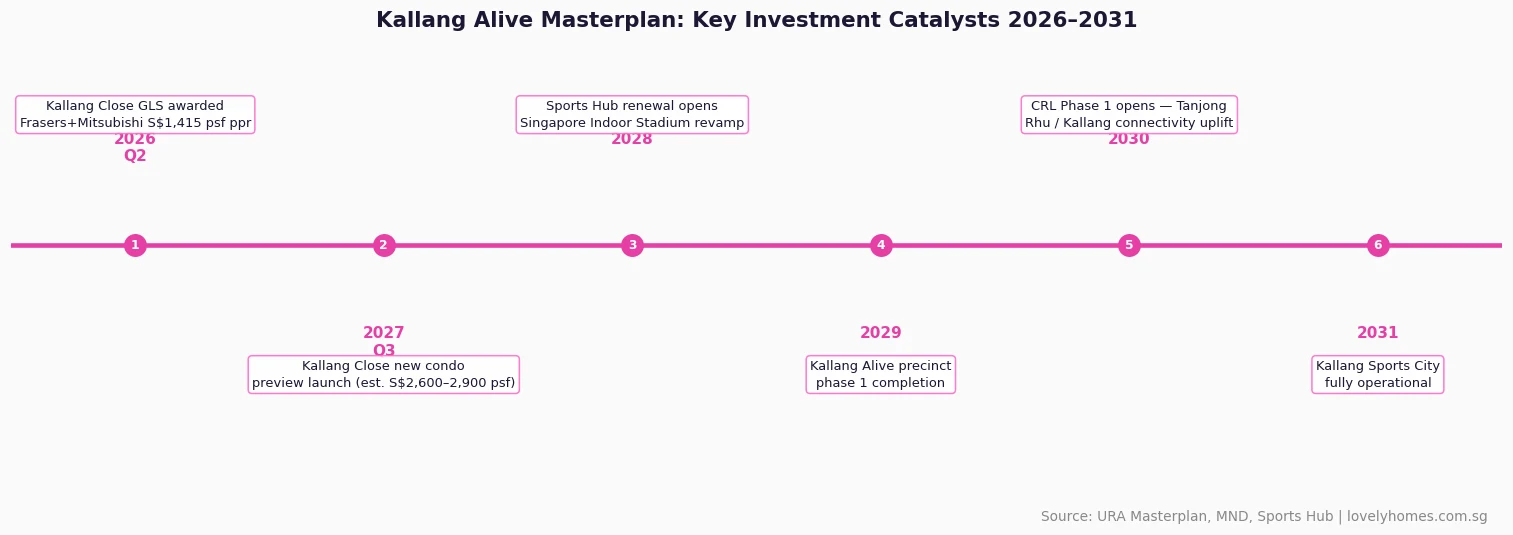

- The Kallang Alive Masterplan, led by MND and Sport Singapore, will redevelop the Sports Hub precinct into a vibrant leisure and residential district by 2031.

- In April 2026, Frasers Property and Mitsubishi Estate won the Kallang Close GLS site at S$1,415 psf ppr (S$610.8 million), signalling strong developer confidence.

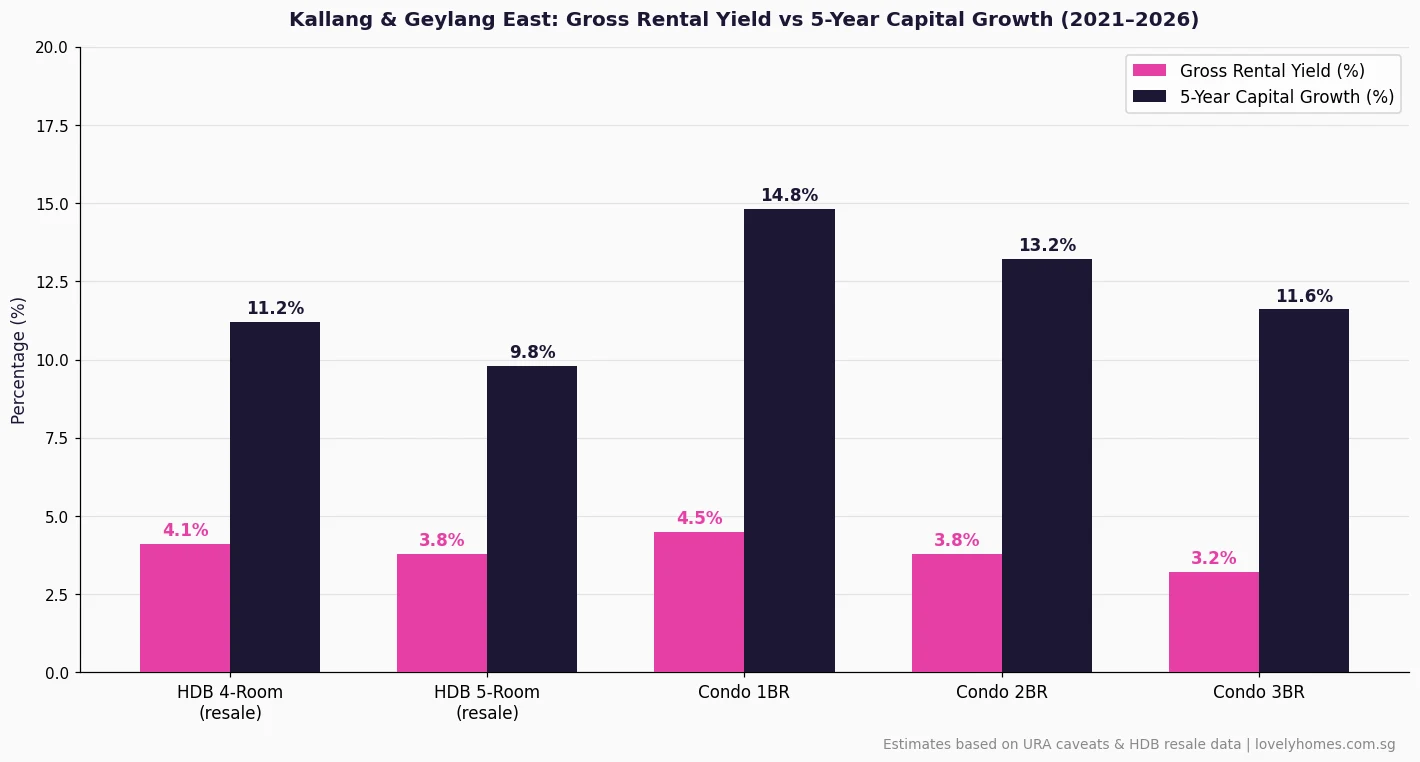

- Gross rental yields in Kallang range from 3.2% (3BR condos) to 4.5% (1BR units), driven by expat demand, Lavender/Kallang basin employment clusters, and MRT access.

- Geylang East forms the HDB-dominant southern flank: 4-room resale prices run S$570,000–S$720,000, with gross yields of 4.1%+ and strong tenant demand from PLQ workers.

- From 2030, the Cross Island Line Phase 1 will deliver a Tanjong Rhu station, improving Kallang’s waterfront connectivity to the CBD and Changi.

- Singapore Citizens buying their first property pay zero ABSD; PRs pay 5%; foreigners face 65%, making this primarily a local investor and upgrader market.

- The indicative new launch price for the Kallang Close GLS project is S$2,600–S$2,900 psf — setting the reference ceiling for resale values in the area.

Where is Kallang? Location, Subzones and District Classification

Kallang is a planning area in the Central Region of Singapore, classified as part of the Rest of Central Region (RCR) for property purposes. The planning area spans from the Kallang River basin in the west to Tanjong Rhu and the Marina Reservoir shoreline in the east. It is divided into eight subzones: Boon Keng, Whampoa, Lavender, Crawford, Kampong Arang, Kallang, Geylang East, and Tanjong Rhu. The area is designated District 12 (D12) in the postal district system.

Geylang East, while administratively a Kallang subzone, functions as a distinct micro-market. It borders the wider Geylang planning area (D14) and draws price comparisons from both districts. The Paya Lebar Quarters (PLQ) commercial hub — with some 3.2 million square feet of Grade-A office space — abuts Geylang East’s northern edge, providing a large pool of white-collar tenants within walking distance.

MRT connectivity is excellent. Kallang station (East West Line), Boon Keng (North East Line), Bendemeer (Downtown Line), and Aljunied (East West Line) all serve the precinct. By 2030, the Cross Island Line Phase 1 will add a Tanjong Rhu station on Kallang’s waterfront, providing direct access to Pasir Ris and Jurong Lake District without changing trains.

Kallang Property Prices in 2026: How the Numbers Stack Up

Kallang’s median PSF for non-landed private residential transactions in Q1 2026 stood at S$1,958 per square foot — representing a meaningful discount to the RCR median of S$2,216 psf. This gap exists primarily because the area has seen no major new private launches since the mid-2010s, leaving resale stock priced below the new-launch reference level that drives neighbouring districts upward. The Kallang Close GLS award in April 2026, and the expected launch of that project at S$2,600–S$2,900 psf in 2027–2028, will reset the price ceiling for the entire Kallang micro-market.

For HDB buyers, Geylang East offers 4-room resale flats in the S$570,000–S$720,000 range (Q1 2026) depending on floor level, remaining lease, and proximity to PLQ. Five-room resales command S$720,000–S$870,000. These prices remain below equivalent stock in Queenstown, Bishan, or Toa Payoh, making Geylang East one of the last affordable RCR-adjacent HDB markets for first-time buyers.

The Kallang Alive Masterplan: A S$1 Billion Catalyst

The Kallang Alive Masterplan is the government’s plan to transform the Sports Hub precinct — currently dominated by the Singapore National Stadium and the Singapore Indoor Stadium — into a vibrant mixed-use sports, leisure, and residential district. Overseen by the Ministry of National Development and Sport Singapore, the masterplan involves renewing the Sports Hub under a new long-term agreement, adding commercial and F&B activations along the Kallang basin waterfront, and integrating housing into a “Singapore Sports City” concept.

The first physical catalyst is already under way: the Sports Hub management agreement was retendered in 2024, with the new operator tasked with higher utilisation, more community programming, and upgrades to the Indoor Stadium and surrounding retail. The Kallang Close GLS site — adjacent to the stadium precinct — will deliver approximately 430 private residential units, adding permanent residents to the area and sustaining retail and F&B demand.

By analogy, the Jurong Lake District masterplan announcement in the mid-2010s preceded a sustained 15–20% PSF premium for JLD-proximate properties over the following decade. Kallang’s masterplan is smaller in scale but more advanced in execution — the infrastructure is already in place; the question is activation quality and speed.

The Kallang Close GLS Award: What S$1,415 psf ppr Means for Buyers

On 7 April 2026, URA awarded the Kallang Close GLS tender to a joint venture of Frasers Property and Mitsubishi Estate JR Investment (MJR Investment) at S$610.8 million — S$1,415 psf per plot ratio. The site attracted four bids, with the winning offer 8.6% above the next-highest bid, reflecting strong developer conviction in the Kallang Alive thesis.

At S$1,415 psf ppr, the developer’s blended cost stack (land + construction ~S$650 psf + professional fees ~S$180 psf + overheads ~S$120 psf + 12–15% margin) implies a breakeven in the S$2,500–S$2,700 psf range, and an expected launch price of S$2,600–S$2,900 psf. At that level, a 700 sf 2-bedroom unit would carry a launch price of approximately S$1.82M–S$2.03M.

The direct implication for existing Kallang resale buyers: the GLS launch will establish a new market benchmark that resale pricing in the area will begin converging upward toward — a pattern clearly visible after every major new launch in established RCR districts. Buyers who acquire resale Kallang condos at current S$1,800–S$2,200 psf stand to benefit from this re-rating over the 2027–2029 window.

Rental Yields and Investment Returns in Kallang and Geylang East

Kallang’s rental market is anchored by several demand pillars: proximity to the CBD (15–20 minutes by MRT), the Lavender/Kallang employment cluster (F&B trade, SME light industry, creative sector), the expat community in the Bendemeer/Boon Keng corridor, and increasing demand from PLQ office workers spilling south into Geylang East. According to URA rental caveat data for Q1 2026, median monthly rents in Kallang private condos range from S$3,100–S$3,800 for a 1-bedroom to S$4,200–S$5,500 for a 3-bedroom, depending on project age and specification.

For HDB investors (subletting approved units), Geylang East 4-room flats grossing S$3,500–S$4,200/month at current resale prices of S$570,000–S$720,000 produce gross yields of 4.1%–5.0% — among the highest in any RCR-adjacent HDB market. Five-year capital growth for 4-room HDB flats in the Geylang East subzone ran at approximately 11.2% between 2021 and Q1 2026, supported by the MOP wave from earlier Dawson and Geylang East BTO launches and sustained demand from PLQ workers.

Summary: Kallang and Geylang East at a Glance (2026)

| Parameter | Kallang Private Condo | Geylang East HDB (resale) |

|---|---|---|

| Median PSF (Q1 2026) | S$1,958 psf | S$550–S$720 psf (HDB resale basis) |

| Typical Price (2BR / 4-room) | S$1.35M–S$1.75M | S$570,000–S$720,000 |

| Gross Rental Yield | 3.2%–4.5% | 4.1%–5.0% |

| 5-Year Capital Growth (2021–26) | 11.6%–14.8% | 9.8%–11.2% |

| RCR Classification | RCR (Rest of Central Region) | Geylang Planning Area / D14 adjacent |

| Key MRT Stations | Kallang (EWL), Boon Keng (NEL), Bendemeer (DTL) | Aljunied (EWL), Paya Lebar (EWL+CCL) |

| Major Catalysts | Kallang Alive Masterplan, GLS launch 2027–28, CRL 2030 | PLQ employment growth, Geylang East regeneration |

| ABSD (SC 1st Property) | Nil | Nil |

Worked Example: Buying a Kallang 2BR Condo as a First Property

Mr and Mrs Chen are Singapore Citizens in their mid-30s with a combined monthly income of S$12,000. They are looking to purchase their first private property — a 2-bedroom resale condominium in Kallang at S$1.45 million, with plans to rent it out and eventually move in when their current HDB flat reaches MOP.

Step 1 — Stamp Duties: As Singapore Citizens buying their first property, ABSD is nil. Buyer’s Stamp Duty (BSD) is S$1,800 (first S$180,000 × 1%) + S$3,600 (next S$180,000 × 2%) + S$19,200 (next S$640,000 × 3%) + S$18,000 (remaining S$450,000 × 4%) = S$42,600. BSD can be paid from CPF Ordinary Account.

Step 2 — Financing: Bank loan LTV 75% = S$1,087,500. Down payment 25% = S$362,500 (minimum cash 5% = S$72,500; the rest S$290,000 from CPF). At 1.65% fixed for 2 years over 25 years, the monthly repayment is approximately S$4,430. TDSR at this income level: S$4,430 / S$12,000 = 36.9% — well within the 55% TDSR cap.

Step 3 — Rental yield and break-even: A 2BR in Kallang at current market rates fetches S$4,200–S$4,800/month. At S$4,500/month (annualised S$54,000), the gross yield on S$1.45M is 3.72%. After property tax (~S$3,500/yr), maintenance (~S$3,600/yr) and estimated rental income tax (~S$5,500/yr on net rental profit), annual net income is approximately S$41,400 — a net yield of 2.86%.

Step 4 — Capital appreciation scenario: If Kallang condos re-rate to S$2,200 psf by 2030 following the Kallang Close GLS launch (from current S$1,958 median), the Chens’ 750 sf unit would be worth approximately S$1.65M — a paper gain of S$200,000 in four years. Combined with S$41,400/yr net rental income over four years, the total return before tax exceeds S$365,000 on an initial outlay of approximately S$115,000 in cash and S$290,000 in CPF.

What This Means for Property Buyers and Investors

Kallang represents one of the clearest “buy before the catalyst” opportunities in Singapore’s private residential market in 2026. The combination of below-average RCR PSF, a government masterplan that is already funded and in progress, a freshly awarded GLS site that will set a new price benchmark, and impending CRL connectivity creates a layered investment thesis that is difficult to replicate in more mature RCR districts like Queenstown or Toa Payoh.

For HDB upgraders specifically, Kallang and Geylang East offer a unique dual-market entry: begin with a resale HDB flat in Geylang East (strong yield, lower entry price) while the MOP clock runs, then upgrade into a private condo — potentially the Kallang Close new launch — within five to seven years. This sequencing maximises grant eligibility, CPF accumulation, and ABSD remission windows.

The main risk is execution: Kallang Alive’s eventual vibrancy depends on the Sports Hub operator’s programme quality and tenant mix. If activations are muted, the waterfront precinct premium may take longer to materialise than the optimistic 2028–2030 timeline suggests. Investors should stress-test their numbers at a flat PSF of S$1,958 (no re-rating scenario) and ensure yield coverage even without capital appreciation.

What Might Come Next: Forward Outlook for Kallang Property (2027–2032)

The following is forward-looking analysis and should be treated as informed speculation rather than certainty. Industry observers expect the Frasers/MJR Kallang Close development to preview in Q3 2027 at S$2,600–S$2,900 psf. A successful launch weekend absorption above 70% within two weeks — similar to TGR at One-North and Vela Bay at Jurong — would likely pull Kallang resale values up by 8–12% in the subsequent 12 months as the new reference price sets in. The CRL Tanjong Rhu station, expected by 2030, would add a further connectivity premium to Tanjong Rhu waterfront condos specifically.

For Geylang East HDB, the key risk is lease decay on older blocks (built 1970s–1980s) approaching the 60-year mark. Buyers should study remaining lease tenure carefully: HDB blocks with fewer than 60 years remaining face reduced CPF usage and bank financing constraints, which depress resale values and liquidity. New BTO supply in the Geylang East subzone is unlikely given the precinct’s predominantly mature and commercial character.

Frequently Asked Questions

Is Kallang a good area to buy property in 2026?

What price will the Kallang Close new launch sell at?

Can foreigners buy property in Kallang?

What are the best condominiums to look at in Kallang?

How does Kallang compare to Queenstown and Toa Payoh for investment?

What is the HDB situation in Geylang East — should I be worried about lease decay?

Related Articles

- Geylang Neighbourhood Guide Singapore 2026: Property Prices, Schools and Investment Outlook

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Holland Plain GLS 2026: D10 CCR Pricing, Investment Outlook and Buyer Analysis

- Jurong Lake District Property Outlook 2026: Prices, Investment Potential and What Is Coming

- Stamp Duty Calculator Singapore 2026: Complete BSD and ABSD Guide

- Private Condo Buying Process Singapore 2026: Complete Step-by-Step Guide

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, legal, or property advice. Property values, rental yields, stamp duty rates, CPF rules, and government policies are subject to change. Worked examples are illustrative only — actual costs will vary. Before making any property purchase or investment decision, readers should seek independent advice from a licensed financial adviser, solicitor, and/or HDB/URA directly. Stamp duty calculations should be verified via the IRAS website. GLS information sourced from URA. CPF usage rules are governed by the CPF Board.

Click anywhere or press Esc to close

0 Comments