For most Singaporeans buying an HDB flat, the choice between an HDB concessionary loan and a bank loan is one of the most consequential financial decisions in the entire purchase — yet it is frequently made on incomplete information or based on advice that was accurate five years ago but may not reflect today’s rate environment. In 2026, with bank floating rates hovering near 1.59%–1.80% and the HDB loan rate remaining at 2.6% since November 2022, the interest cost differential is material. On a S$500,000 loan over 25 years, the total interest difference between the two options exceeds S$90,000.

At the same time, the HDB loan offers structural advantages — no minimum cash downpayment, no lock-in period, the stability of a fixed spread above the CPF Ordinary Account rate, and the safety of not being subject to bank repricing risk — that a purely interest-rate-driven comparison misses. This guide gives you the complete picture for 2026 so you can make the right decision for your specific financial situation.

- The HDB concessionary loan rate is 2.6% per annum (CPF OA rate + 0.1%), unchanged since November 2022. It is reviewed quarterly and can change if the CPF OA rate moves.

- Bank fixed rates for HDB flat purchases start from approximately 1.55%–1.85% (2-year fixed, as at May 2026). Floating rates on 3-month SORA + margin run at approximately 1.59%–1.80%.

- HDB loan: maximum LTV of 80%, no minimum cash downpayment (full 20% can come from CPF). Bank loan: maximum LTV 75%, minimum 5% cash downpayment required.

- Once you switch from an HDB loan to a bank loan, you can never switch back to an HDB loan. This is irreversible.

- Bank loans carry a lock-in period (typically 2 years) during which early repayment or refinancing triggers a penalty, usually 1.5% of the loan outstanding.

- Both loans are subject to the Total Debt Servicing Ratio (TDSR) cap of 55% and the Mortgage Servicing Ratio (MSR) cap of 30% for HDB flats and Executive Condominiums.

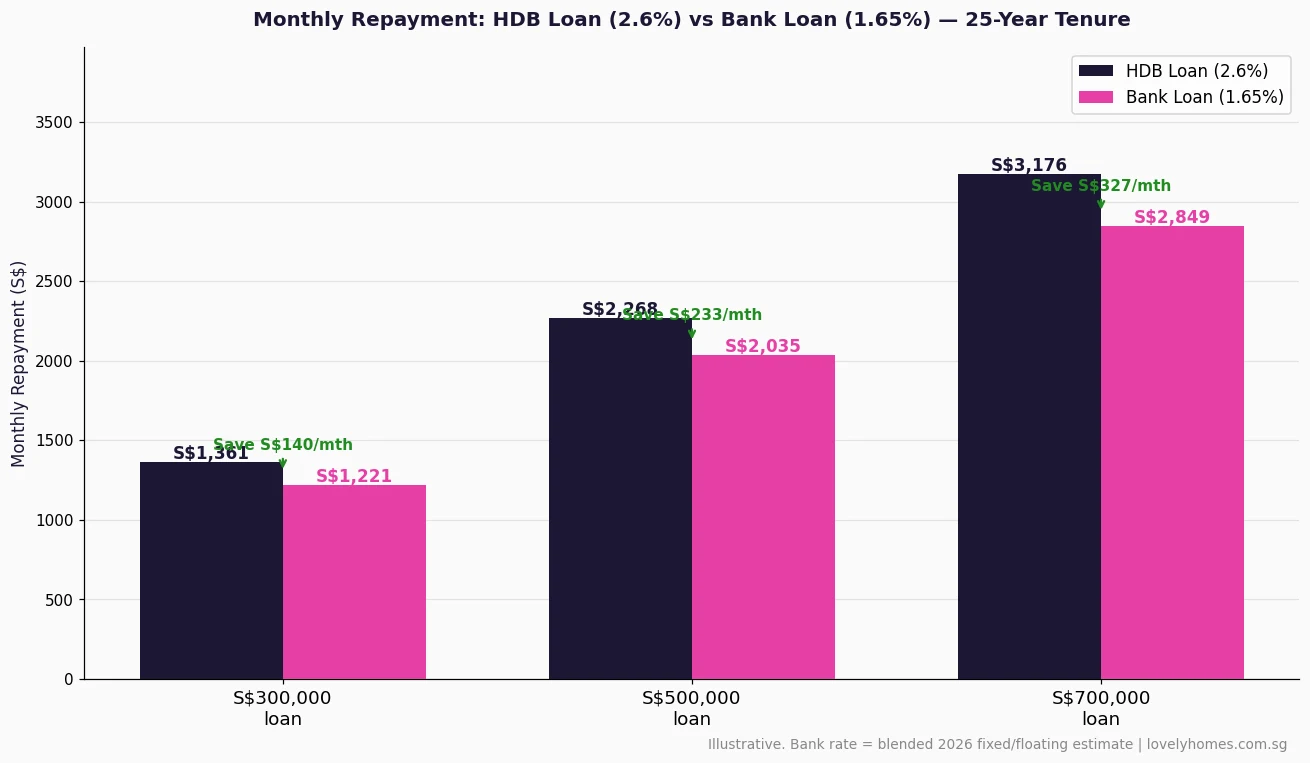

- On a S$500,000 loan over 25 years, a bank fixed rate of 1.65% saves approximately S$92,000 in total interest compared with the HDB rate of 2.6%.

- HDB loan eligibility for resale flats has no income ceiling (removed in February 2024). For BTO flats, the household income ceiling of S$14,000/month still applies.

How the HDB Concessionary Loan Works in 2026

The HDB concessionary loan is a housing loan issued directly by the Housing and Development Board. It is available only for the purchase of HDB flats — BTO and resale — and is not available for Executive Condominiums or private property. The interest rate is set at 0.1% above the prevailing CPF Ordinary Account (OA) interest rate, which has been 2.5% since 1999, placing the HDB loan rate at 2.6%. The CPF Board reviews the CPF OA rate quarterly; if it changes, the HDB loan rate adjusts accordingly at the next quarterly interval (January, April, July, or October).

To qualify for the HDB loan on a resale flat, at least one buyer must be a Singapore Citizen (Permanent Residents alone cannot take an HDB loan). There is no household income ceiling for resale flats since February 2024. The loan covers up to 80% of the flat’s purchase price or valuation (whichever is lower), meaning the buyer needs to fund only 20% as a downpayment — and the entire 20% can come from CPF savings with no minimum cash requirement.

Crucially, the HDB loan has no lock-in period. Borrowers may make partial prepayments or full redemption at any time without penalty. This flexibility is valuable for buyers who anticipate selling or refinancing within the near term, or who expect to receive a CPF top-up or windfall that they wish to put toward the mortgage.

How Bank Loans Work for HDB Flat Purchases in 2026

Any bank licensed by the Monetary Authority of Singapore (MAS) can offer mortgage financing for HDB flat purchases, subject to HDB’s co-approval. Unlike the HDB loan, bank loans offer a choice between fixed-rate packages (where the rate is locked for an initial 2- or 3-year period before repricing) and floating-rate packages pegged to the Singapore Overnight Rate Average (SORA). As at May 2026, the most competitive rates from DBS, OCBC, and UOB for HDB flat purchases are:

- Fixed 2-year: 1.55%–1.85% per annum (varies by loan quantum and bank package)

- Floating (3M SORA + margin): approximately 1.59%–1.80% at current SORA of ~1.34%

The maximum LTV for a bank loan on an HDB flat is 75% of the purchase price or valuation (lower), meaning the buyer must fund a 25% downpayment, of which at least 5% must be cash — the remainder can come from CPF. This cash requirement is the most significant structural difference for buyers who have limited cash savings.

Bank loans for HDB flats typically come with a lock-in period of 2 years. If you refinance or make a lump-sum prepayment above a certain threshold during the lock-in, the bank charges a redemption fee of approximately 1.5% of the loan outstanding — which on a S$500,000 loan is S$7,500. After the lock-in, you may refinance freely, but you cannot switch back to the HDB concessionary loan under any circumstances.

Monthly Repayment Comparison: Where the Numbers Land

The most immediate financial difference between the two options is the monthly repayment. Using a 25-year tenure and a blended bank rate of 1.65% (representing a fixed-to-floating journey), the comparison across three common loan sizes is as follows:

Summary Comparison Table: HDB Loan vs Bank Loan (2026)

| Parameter | HDB Concessionary Loan | Bank Loan |

|---|---|---|

| Interest Rate (May 2026) | 2.6% p.a. (CPF OA + 0.1%) | Fixed: 1.55%–1.85% / Float: ~1.59%–1.80% |

| Maximum LTV | 80% | 75% |

| Minimum Cash Downpayment | 0% cash (full 20% can be CPF) | 5% cash (remaining 20% can be CPF) |

| Lock-In Period | None | Typically 2 years (~1.5% penalty) |

| Property Eligibility | HDB flats only (BTO + resale) | HDB, EC, and private property |

| Switch Back to HDB? | N/A | NO — irreversible once bank loan taken |

| TDSR / MSR | Both apply (55% TDSR, 30% MSR) | Both apply (55% TDSR, 30% MSR) |

| CPF Usage | Yes — for downpayment and monthly repayment | Yes — for downpayment and monthly repayment |

| Income Ceiling (Resale) | None (removed Feb 2024) | None |

| Total Interest (S$500k, 25yr) | ~S$215,700 | ~S$123,200 (at 1.65%) |

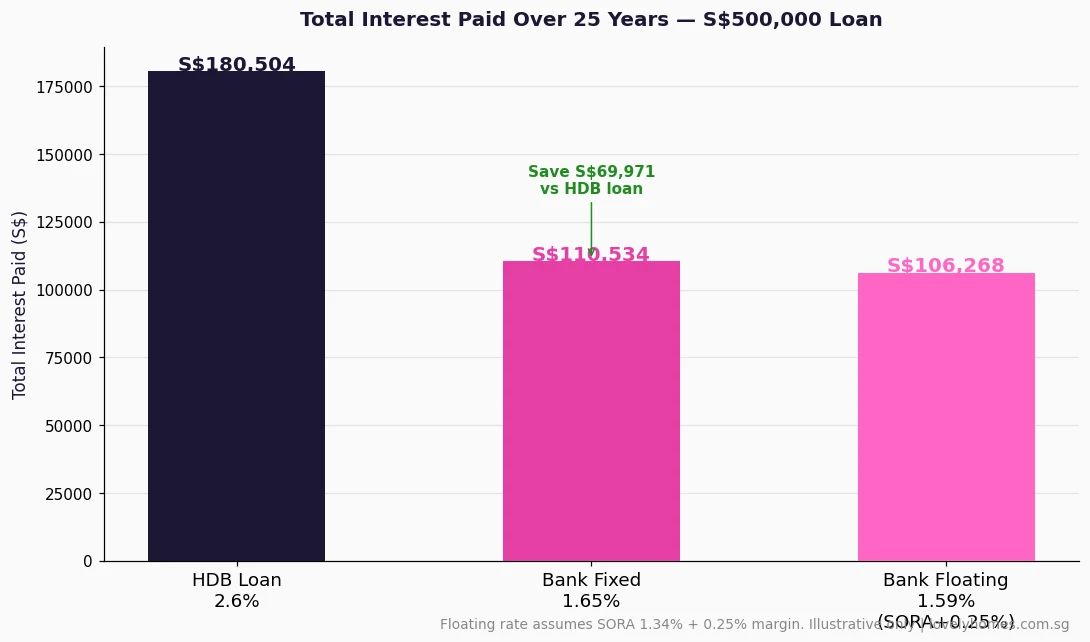

Total Interest Over 25 Years: The Full Cost Picture

The total interest difference is stark. At 1.65% (illustrative blended bank rate), a S$500,000 loan over 25 years costs approximately S$123,200 in interest — against S$215,700 at the HDB rate of 2.6%. The saving of approximately S$92,500 over the loan tenure is meaningful, though it must be weighed against the higher cash outlay (additional 5% minimum cash downpayment) and loss of the flexibility to switch back to an HDB loan.

It is also important to note that bank rates are not guaranteed to remain low. The floating rate in Figure 3 uses a static SORA assumption; if the Singapore interbank rate rises — as it did sharply between 2022 and 2023, peaking at 3.68% in July 2023 — the actual total interest on a floating-rate bank loan could exceed the HDB loan total. Fixed-rate borrowers are protected during their 2-year lock-in but face repricing risk at the end of each fixed period.

Worked Example: Buying a 4-Room Resale HDB Flat in Clementi at S$750,000

Mr and Mrs Lim are Singapore Citizens with a combined monthly income of S$9,500. They plan to purchase a 4-room HDB resale flat in Clementi for S$750,000. Their CPF OA balances total S$180,000 between them. They have S$60,000 in accessible cash savings.

Option A — HDB Loan (2.6%): Maximum loan S$600,000 (80% LTV). Downpayment S$150,000 — fully payable from their combined CPF (S$180,000 balance more than sufficient, leaving S$30,000 for BSD and legal). Monthly repayment at 2.6% over 25 years: S$2,720. MSR: S$2,720 / S$9,500 = 28.6% (within 30% cap). Total interest over 25 years: approximately S$216,000. Cash outlay: effectively S$0 (BSD and legal fees, approximately S$19,100 total, are payable from CPF or cash). No lock-in, can make penalty-free prepayments from future CPF inflows.

Option B — Bank Loan (1.65% fixed for 2 years): Maximum loan S$562,500 (75% LTV). Downpayment S$187,500 — minimum 5% cash S$37,500 required, remaining S$150,000 from CPF. Monthly repayment at 1.65% over 25 years: S$2,292. MSR: S$2,292 / S$9,500 = 24.1%. Total interest over 25 years at 1.65%: approximately S$125,100. Monthly savings vs HDB: S$428. After 2-year lock-in, can refinance. Cash outlay: S$37,500 (downpayment cash) + BSD/legal (~S$19,100 from CPF or cash) = minimum S$37,500 cash on day one.

Analysis: With S$60,000 in accessible cash, the Lims can comfortably meet the bank loan’s S$37,500 cash downpayment. The bank loan saves S$428/month and approximately S$91,000 over the full 25-year term. However, they permanently give up the right to return to the HDB concessionary loan. If SORA rises materially after their fixed period ends in 2028, their repriced rate could approach or exceed 2.6%. Given their stable income and adequate cash buffer, the bank loan is the financially superior choice if they are confident about staying in the property long-term and can manage the rate risk at repricing.

When to Choose the HDB Loan vs When to Choose a Bank Loan

There is no universal answer — the right choice depends on your specific cash position, risk appetite, tenure horizon, and income stability. As a guide: choose the HDB loan if you have minimal cash savings and cannot meet the 5% cash downpayment for a bank loan, if your income is variable and you value the certainty of the 2.6% rate not rising during a SORA spike, or if you plan to sell within 2–3 years and want flexibility without lock-in penalties. Choose a bank loan if you have sufficient cash for the 5% downpayment, can lock in a fixed rate below 2.0% for the first 2 years, plan to hold the flat for 5 or more years (recovering the rate advantage over the HDB loan), and are comfortable refinancing actively at each lock-in expiry to maintain a competitive rate.

A middle path, used by many financially sophisticated buyers, is to take the HDB loan initially (preserving the option to switch later) and then refinance to a bank loan when the interest rate environment is favourable — typically when fixed rates are below 2.0% and there is no imminent sale or major financial change on the horizon. Once you make that switch, however, you must manage your future mortgage relationship entirely within the private banking market.

What Might Change: HDB Loan Rate Outlook for 2026–2028

Forward-looking analysis — speculative. The CPF OA rate of 2.5% has been unchanged since 1999, making it an unusually stable anchor for the HDB loan rate. The CPF Advisory Panel recommended maintaining the OA rate at 2.5% through the near term, citing the need to balance retirement adequacy with sustainability for CPF’s investment returns. A reduction is theoretically possible if the Monetary Authority of Singapore engineers materially lower interest rates, but is unlikely in the current global rate environment where major central banks maintain rates above historical lows. Buyers who lock in a bank fixed rate in 2026 are effectively betting that the bank rate will remain below 2.6% for most of the next 25 years — a reasonable bet given Singapore’s monetary policy framework, but not a certainty.

Frequently Asked Questions

Can I use CPF to pay my bank loan monthly instalment?

If I take a bank loan now, can I switch back to HDB later?

Does the MSR apply to bank loans for HDB flats?

What happens to my bank loan rate after the 2-year fixed period ends?

Can Permanent Residents take an HDB loan?

Is the HDB Housing Loan Eligibility (HLE) letter still required in 2026?

Related Articles

- Mortgage Refinancing vs Repricing Singapore 2026: When to Switch Banks and When to Stay

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Stamp Duty Calculator Singapore 2026: Complete BSD and ABSD Guide

- CPF Housing Grant for Resale Singapore 2026: Complete Guide to EHG, PHG and Step-Up Grant

- Conveyancing Fees Singapore 2026: Legal Costs for Buying and Selling Property

- First-Time Property Buyer Checklist Singapore 2026

Disclaimer

This article is for informational purposes only and does not constitute financial, mortgage, legal or property advice. Interest rates, CPF rules, HDB loan eligibility criteria, and government policies are subject to change. Worked examples use illustrative rates and figures — actual loan costs, repayments and CPF entitlements will vary. Always verify current HDB loan rates and eligibility conditions directly with HDB. Bank loan rates should be confirmed with individual banks or a licensed mortgage broker. CPF housing withdrawal limits are governed by the CPF Board. Seek independent advice from a licensed financial adviser before committing to any mortgage product.

Click anywhere or press Esc to close

0 Comments