Every property buyer in Singapore pays Buyer’s Stamp Duty (BSD) — a transaction tax levied on the purchase price or market value (whichever is higher) of any residential, commercial, or industrial property. Unlike the Additional Buyer’s Stamp Duty (ABSD), which applies only to second and subsequent property purchases by residents and all properties purchased by foreigners, BSD is the baseline duty that every single buyer must pay, regardless of citizenship, residency status, or how many properties they already own.

Whether you are buying your first HDB flat, upgrading to a private condo, or acquiring commercial premises, understanding how BSD is calculated, when it must be paid, and how it differs from ABSD is essential to budgeting correctly for your purchase. Get BSD wrong, and it can consume tens of thousands of dollars in unexpected costs.

This guide walks you through the exact BSD rates in force in 2026, provides step-by-step calculation examples across multiple property types and price points, explains how CPF reimbursement works, and clarifies how BSD stacks with ABSD. All figures reflect the latest IRAS guidance.

Quick Answer — BSD at a glance

- Applies to: Every property purchase (residential, commercial, industrial, land)

- Basis: Higher of purchase price or market valuation

- Payment timeline: Within 14 days of signing OTP/SPA

- CPF: Cannot be paid directly from CPF; reimbursement available after stamping

- Top residential rate: 6% on amounts above S$3,000,000

- Top non-residential rate: 5% (raised 15 February 2023)

What is Buyer’s Stamp Duty (BSD)?

Buyer’s Stamp Duty is a progressive transaction tax imposed by the Inland Revenue Authority of Singapore (IRAS) on the acquisition of any property in Singapore. The term “stamp duty” originates from the historical practice of stamping documents as proof that tax had been paid; today, the duty is administered entirely through the Stamp Duty system managed by IRAS and supporting conveyancers.

BSD is:

- Progressive: The rate increases in tiers as the property price rises

- Compulsory: It applies to every buyer, without exception

- Upfront: It must be paid within 14 days of executing the Option to Purchase (OTP) for resale, or the Sale & Purchase Agreement (SPA) for new launches

- Non-recoverable: Unlike GST or certain taxes, BSD is not refundable

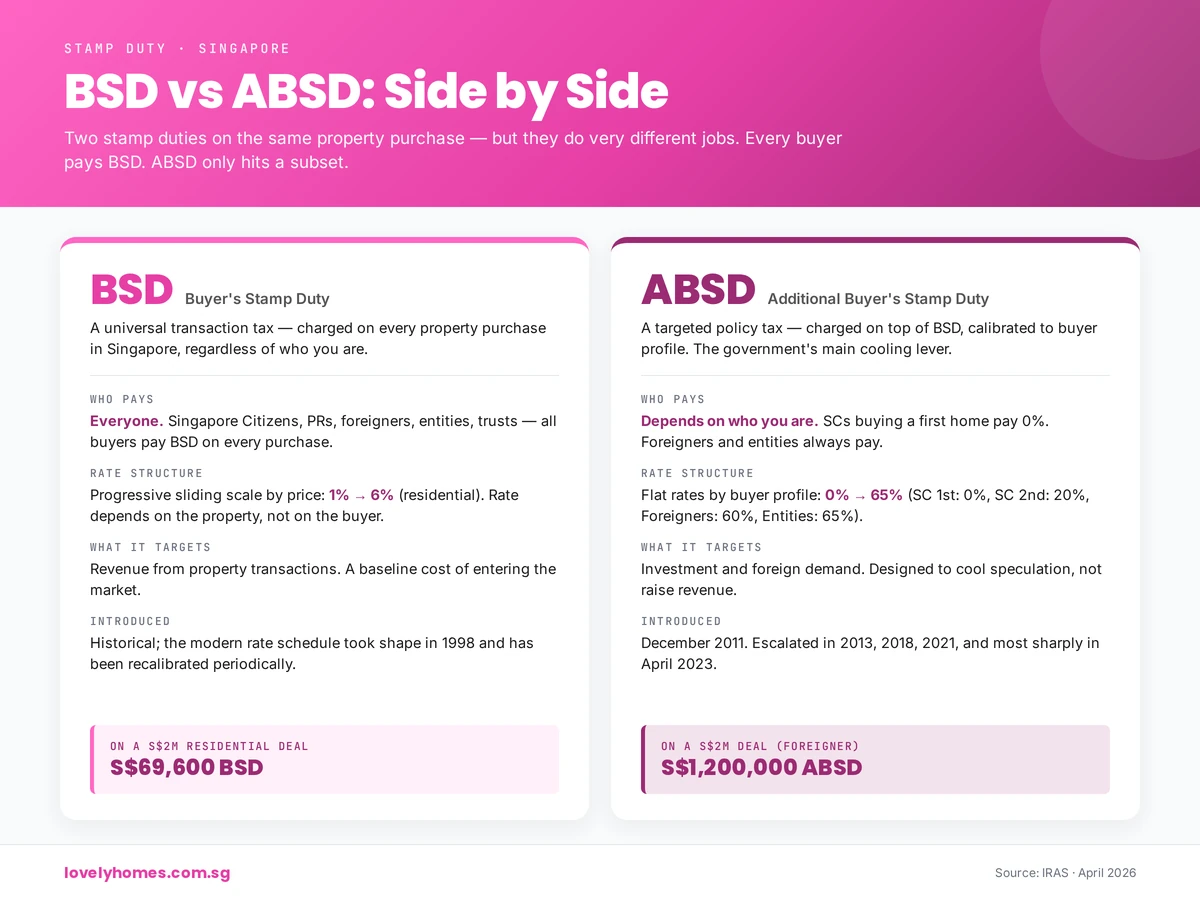

How BSD Differs From ABSD

The key difference between BSD and ABSD often confuses first-time buyers. Here is the distinction in plain terms:

| Feature | BSD (Buyer’s Stamp Duty) | ABSD (Additional Buyer’s Stamp Duty) |

|---|---|---|

| Who pays | Every buyer | Only 2nd+ residential buyers; all foreigners buying residential |

| Rate structure | Progressive (1–6% for residential) | Flat (0–60% depending on profile) |

| Applied to | Residential, commercial, industrial, land | Residential properties only |

| Purpose | Government revenue; general property transaction tax | Cooling measure; discourages speculation and foreign ownership |

| Remission available | No | Yes (married couple, developer, etc.) |

Example to clarify: A Singapore Citizen buying their first residential property pays BSD but zero ABSD. A Singapore Citizen buying their second residential property pays BSD plus 20% ABSD on top.

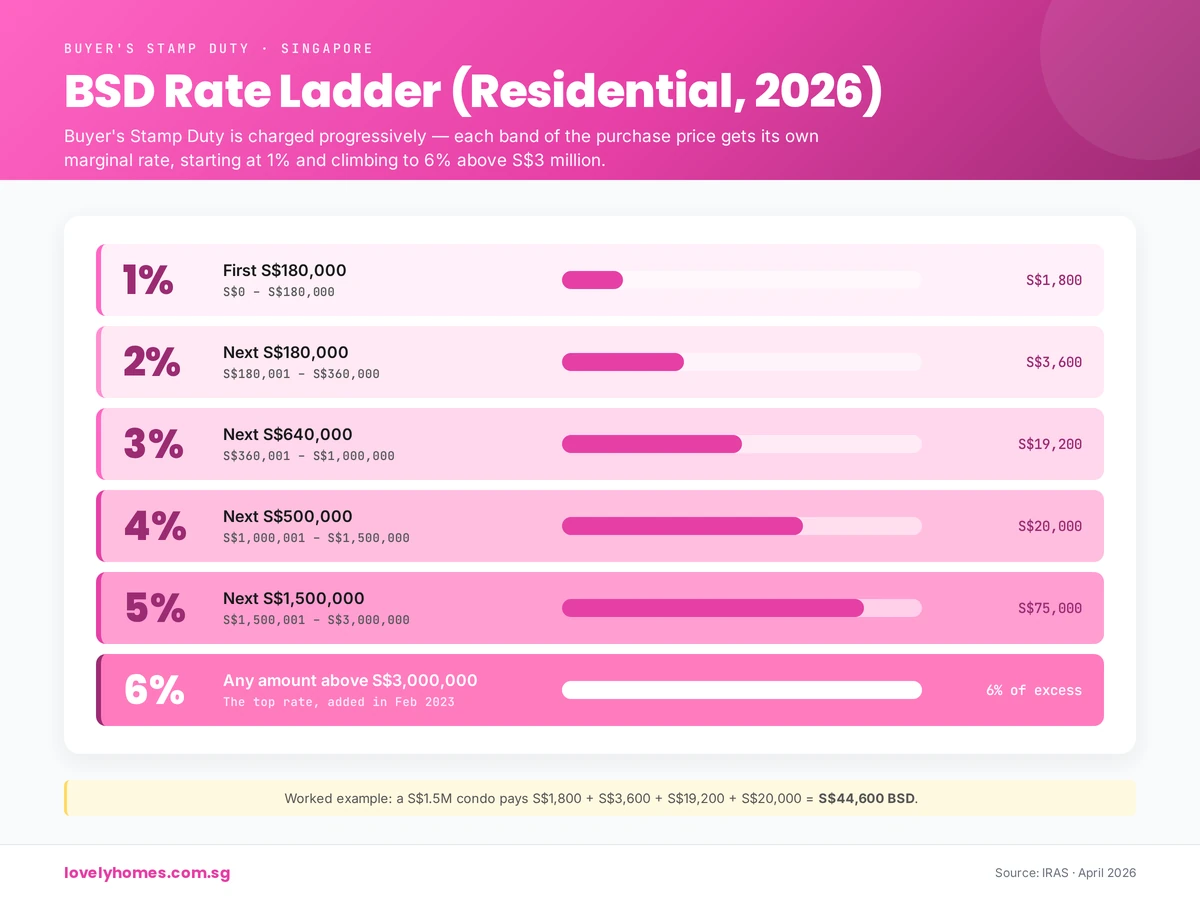

BSD Rates for Residential Properties (2026)

As of 15 February 2023, the residential BSD rates are:

| Property Price Bracket | BSD Rate | Cumulative Duty (Example) |

|---|---|---|

| First S$180,000 | 1% | S$1,800 |

| S$180,001 to S$360,000 | 2% | S$3,600 |

| S$360,001 to S$1,000,000 | 3% | S$19,200 |

| S$1,000,001 to S$1,500,000 | 4% | S$20,000 |

| S$1,500,001 to S$3,000,000 | 5% | S$75,000 |

| Above S$3,000,000 | 6% | 6% on excess |

Note: The 6% top rate for residential properties was introduced in July 2018. The 5% top rate for non-residential properties was raised from 4% on 15 February 2023.

BSD Rates for Non-Residential Properties (2026)

Non-residential properties (commercial, industrial, land for non-residential use) follow a similar progressive structure but max out at 5%:

| Property Price Bracket | Non-Residential Rate |

|---|---|

| First S$180,000 | 1% |

| S$180,001 to S$360,000 | 2% |

| S$360,001 to S$1,000,000 | 3% |

| S$1,000,001 to S$1,500,000 | 4% |

| Above S$1,500,000 | 5% |

How BSD is Calculated: Step by Step

BSD is calculated on the higher of the purchase price or the market value of the property at the time of acquisition. This is a critical point: if the market value (as assessed by IRAS or an independent valuer) exceeds your negotiated purchase price, you pay BSD on the higher figure.

Key rules:

- BSD is rounded down to the nearest dollar, subject to a minimum of S$1

- The calculation is tiered and progressive — you do not pay the top rate on the entire property price, only on the portion that falls into that bracket

- BSD is computed using the property price or market value at the time the OTP is granted (for resale) or the SPA is signed (for new launches)

Worked Example 1: HDB Resale at S$650,000

A Singapore Citizen couple purchases a 4-room HDB resale flat in Yung Ho for S$650,000. This is their first joint property purchase.

Calculation:

- First S$180,000 @ 1% = S$1,800

- Next S$180,000 (S$180,001–S$360,000) @ 2% = S$3,600

- Remaining S$290,000 (S$360,001–S$650,000) @ 3% = S$8,700

- Total BSD = S$1,800 + S$3,600 + S$8,700 = S$14,100

They also pay 0% ABSD (first residential property for a Singapore Citizen). Total stamp duty = S$14,100.

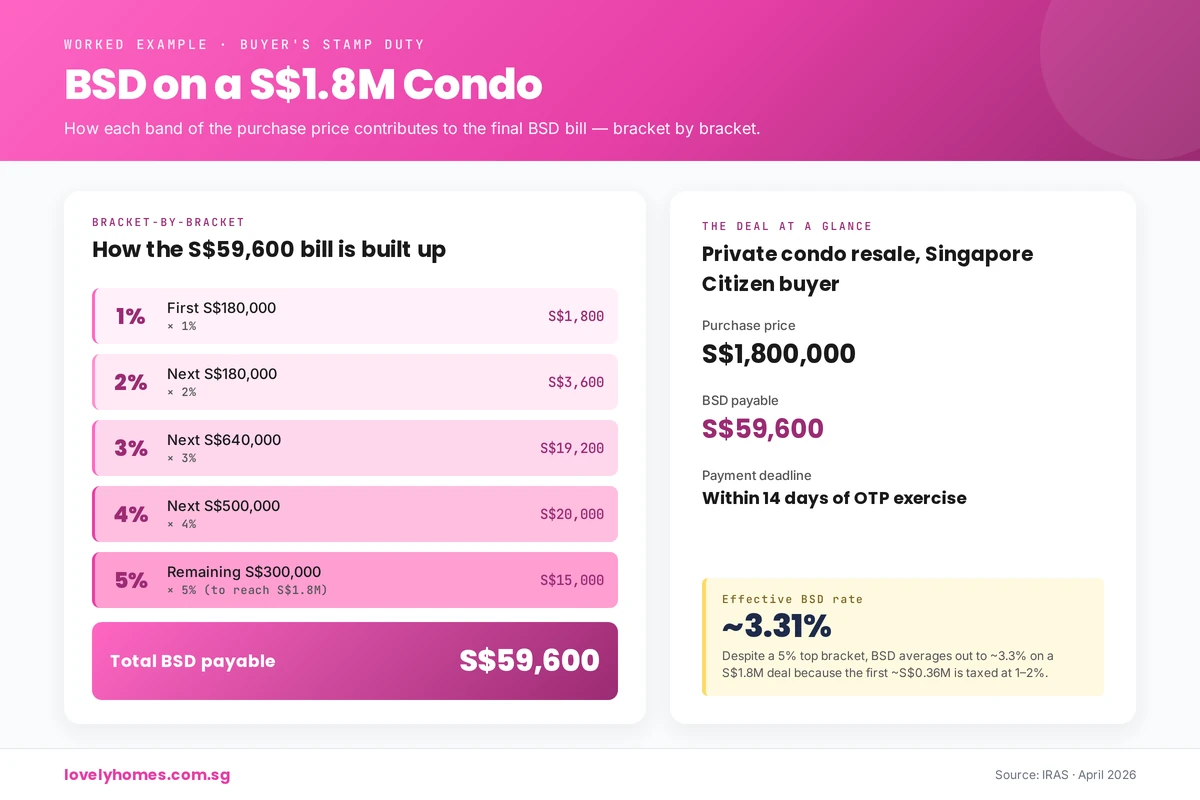

Worked Example 2: Private Condo Resale at S$1,800,000

A Singapore Citizen already owns one residential property and purchases a 3-bedroom condo resale in the central business district for S$1,800,000. This is their second residential property.

BSD calculation:

- First S$180,000 @ 1% = S$1,800

- Next S$180,000 (S$180,001–S$360,000) @ 2% = S$3,600

- Next S$640,000 (S$360,001–S$1,000,000) @ 3% = S$19,200

- Next S$500,000 (S$1,000,001–S$1,500,000) @ 4% = S$20,000

- Remaining S$300,000 (S$1,500,001–S$1,800,000) @ 5% = S$15,000

- Total BSD = S$1,800 + S$3,600 + S$19,200 + S$20,000 + S$15,000 = S$59,600

ABSD calculation:

- S$1,800,000 @ 20% (second property, Singapore Citizen) = S$360,000

Total stamp duty payable = S$59,600 + S$360,000 = S$419,600

This is why many upgraders choose to sell their first property before purchasing the second — it allows them to avoid the 20% ABSD entirely.

Worked Example 3: Luxury Landed Property at S$4,500,000

A Singapore Citizen couple purchasing a luxury landed property in Bukit Timah for S$4,500,000. This is their first residential property.

BSD calculation:

- First S$180,000 @ 1% = S$1,800

- Next S$180,000 (S$180,001–S$360,000) @ 2% = S$3,600

- Next S$640,000 (S$360,001–S$1,000,000) @ 3% = S$19,200

- Next S$500,000 (S$1,000,001–S$1,500,000) @ 4% = S$20,000

- Next S$1,500,000 (S$1,500,001–S$3,000,000) @ 5% = S$75,000

- Remaining S$1,500,000 (above S$3,000,000) @ 6% = S$90,000

- Total BSD = S$1,800 + S$3,600 + S$19,200 + S$20,000 + S$75,000 + S$90,000 = S$209,600

ABSD calculation:

- 0% ABSD (first residential property for a Singapore Citizen)

Total stamp duty payable = S$209,600

Note how the 6% band kicks in at S$3,000,000 and above — on luxury properties, BSD becomes a significant cost.

Who Pays BSD? Property Types and Exemptions

BSD applies to the acquisition of any property in Singapore — residential, commercial, industrial, or undeveloped land — regardless of the buyer’s citizenship or residency status. However, certain transactions are exempt or treated differently:

Properties Subject to BSD

- HDB flats (public housing)

- Executive Condominiums (ECs) — during MOP and after privatisation

- Private condominiums and apartments

- Landed houses (terrace, semi-detached, detached)

- Commercial properties (shophouses, offices, retail units)

- Industrial properties (factories, warehouses)

- Land (whether for residential or non-residential development)

Transactions Not Attracting BSD

- Transfers within families: If a property is transferred from one spouse to another (with no consideration), no BSD is triggered

- Transmissions on death: When a property is transmitted via a will or intestacy, no stamp duty is payable on the transmission itself (though a later sale would trigger BSD)

- Gifts: A gift of property attracts a nominal stamp duty (10 cents) but not the full BSD rate

- Leasehold renewals: Renewing a lease on the same property does not trigger BSD

When Must BSD Be Paid?

BSD (together with ABSD, if applicable) must be paid within 14 days of the date the property transaction is formally documented:

- For resale properties: Within 14 days of signing the Option to Purchase (OTP)

- For new launch properties: Within 14 days of signing the Sale & Purchase Agreement (SPA)

- For contracts executed overseas: Within 30 days of the contract being received in Singapore

Late payment penalty: If BSD is not paid within the prescribed timeframe, IRAS charges a penalty. For delays of up to three months, the penalty is typically 5% of the duty; beyond three months, it escalates to 10%. Interest also accrues.

Can You Pay BSD Using CPF?

No, BSD (like ABSD) cannot be paid directly from your CPF Ordinary Account at the point of purchase. You must pay in cash or by cheque/bank transfer to IRAS.

However, CPF reimbursement is available after the property is stamped:

- Once IRAS has stamped your property document, you may apply for CPF reimbursement of BSD (and the purchase price) from your Ordinary Account

- The reimbursement claim is typically submitted via the conveyancing lawyer and approved by the CPF Board within 1–2 months

- Your CPF funds are refunded to your OA once your legal title to the property has been registered with the Land Authority

This two-step process — pay upfront, then reimburse from CPF — is a key budgeting consideration for many first-time HDB and condo buyers. Ensure you have sufficient cash reserves to bridge the gap between the OTP date and the CPF reimbursement.

BSD vs ABSD: Side-by-Side Comparison

To solidify understanding, here is a comprehensive comparison:

| Aspect | BSD | ABSD |

|---|---|---|

| Full name | Buyer’s Stamp Duty | Additional Buyer’s Stamp Duty |

| Who pays | Every buyer | Second/third+ residential buyers; all foreigners (residential) |

| Payment basis | Higher of purchase price or market value | Higher of purchase price or market value |

| Rate type | Progressive (1%–6% residential) | Flat rate (0%–65% depending on buyer profile) |

| Applies to | Residential, commercial, industrial, land | Residential only |

| Example (SC, 2nd property, S$1.8M) | S$59,600 | S$360,000 |

| Payment deadline | 14 days of OTP/SPA | 14 days of OTP/SPA |

| CPF reimbursement | Yes (post-stamping) | No (non-refundable) |

| Remission/deferral schemes | No | Yes (married couple, developer, etc.) |

The History of BSD in Singapore (2011–2026)

Understanding how BSD has evolved helps explain why the rates stand where they do today:

- July 2018: The top residential rate was raised from 5% to 6% on amounts above S$3,000,000 — designed to moderate price growth in the luxury segment

- 15 February 2023: The top non-residential rate was raised from 4% to 5% in line with a broader cooling-measures update — reflecting rising commercial property prices in Singapore’s business core

The progressive structure itself has remained relatively stable, with the tier brackets unchanged since their introduction. This consistency allows developers and conveyancers to model costs with confidence.

Frequently Asked Questions (FAQ)

Is BSD the same as ABSD?

No. BSD is the baseline stamp duty every buyer pays. ABSD is an additional layer that only applies to second-and-subsequent residential purchases and purchases by foreigners. A first-time buyer pays BSD but zero ABSD; a second-time buyer pays both BSD and ABSD.

Can I pay BSD from my CPF Ordinary Account?

No, not directly at the point of purchase. You must pay BSD in cash. After the property document is stamped and registered, you can apply for CPF reimbursement of the purchase price and stamp duty from your CPF Ordinary Account.

What if the valuation is higher than my purchase price?

BSD is calculated on the higher of the purchase price or the market value. If IRAS or an independent valuer assesses the market value above your negotiated price, you pay stamp duty on the higher figure. This is common in the resale HDB market where transaction prices may lag official valuations. Always budget for this possibility.

Do I pay BSD on inherited property?

No. When property is inherited via a will or intestacy, the transmission to the heirs does not attract stamp duty. However, if you later sell that inherited property, the buyer (not the inheritor) pays BSD based on the sale price.

Is BSD payable on commercial property?

Yes. Commercial and industrial properties are subject to BSD. The rates are the same as residential up to S$1,500,000, then cap at 5% above S$1,500,000 (rather than 6% for residential).

How do I file and pay BSD?

Your conveyancing lawyer handles the submission and payment to IRAS. Upon signing the OTP/SPA, the lawyer prepares the stamped property document and submits it to IRAS for assessment and stamping. Payment is made on behalf of the buyer, typically before the completion date. The stamped document is then lodged with the Singapore Land Authority for registration.

What is the penalty for late BSD payment?

If BSD is not paid within 14 days of the OTP/SPA, IRAS charges a penalty of 5% for delays up to three months, escalating to 10% thereafter. Interest also accrues on the unpaid amount. Late payment can delay the registration of your legal title, so it is critical to meet the deadline.

Can BSD be remitted or waived in any circumstance?

No. Unlike ABSD, which has remission schemes for married couples and property developers, BSD is a fixed tax with no remission or deferral schemes. It must be paid in full within the prescribed timeframe.

What if I buy as a company or trust?

A property acquired by a company, trust, or other entity (not a natural person) is subject to the same BSD rates as a residential or non-residential property. However, such purchases often also trigger higher ABSD rates (65% for entities on residential property, depending on the nature and structure of the entity).

Key Takeaways: How to Manage Your BSD Bill

To wrap up, here are the core points to lock in as you plan a property purchase:

- BSD is compulsory. Every buyer, on every property, pays it. There is no avoiding it, and no remission schemes apply.

- It is progressive. The more expensive the property, the higher your effective rate, but you only pay the tier rate on each bracket of the purchase price.

- Budget for both BSD and ABSD. If you are a second-plus buyer or a foreigner buying residential, both apply. Your total stamp-duty bill can easily exceed S$300,000–S$400,000 on a S$2 million upgrade.

- Timing and staging matter. For upgraders, selling your existing property before buying your next one avoids the 20% ABSD entirely — potentially saving six figures.

- The payment deadline is strict. 14 days from OTP/SPA signature. Delay incurs penalties and can freeze your legal-title registration.

- CPF reimbursement is post-stamping. You must have cash at hand to pay BSD upfront; CPF refund follows weeks or months later.

- Always verify with IRAS. This guide reflects the rates as of April 2026, but the Government can change BSD or introduce new cooling measures. Check the IRAS Stamp Duty page before signing an OTP.

What to Do Next

If you are in active purchase planning, we recommend three next steps:

- Calculate your true cost of entry. Use our BSD calculator (if available) or work through the examples above with your target property price to see how much stamp duty you’ll owe. Don’t forget ABSD if applicable.

- Review your CPF position. Check your CPF Ordinary Account balance via myGov.sg, and confirm that post-reimbursement, you’ll still have sufficient balance for housing withdrawal limits. Our Home Loans & Mortgages guide walks through the interaction between stamp duty, mortgage eligibility (TDSR, MSR, LTV), and CPF withdrawal rules.

- If you’re upgrading, model the ‘sell-first’ scenario. Many upgraders can save tens of thousands by selling their existing property before buying the next. See our Upgrader Guide for detailed sequencing advice.

Unsure which property type is right for you? Our detailed property guides — HDB Buying Guide, Condo Buying Guide, Landed Buying Guide — break down the stamp-duty implications alongside financing and market comparison for each property class.

Related Articles and Resources

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty — Deep dive into the Additional Buyer’s Stamp Duty, remission schemes, and cooling-measure context

- Property Finance — Guides on mortgages, loan eligibility, CPF, and other financial aspects of property ownership

- Stamp Duties & Taxes — All stamp-duty articles, property taxes, and related regulatory updates

- Buying Guides by Property Type — First-time buyers, upgraders, HDB, condo, landed, and foreign-buyer guides

- Laws, Regulations & Policies — Property law, cooling measures, and regulatory guidance

Disclaimer

This guide is for general information only and does not constitute legal, tax, financial, or conveyancing advice. Buyer’s Stamp Duty rates, calculation rules, and remission schemes can change. Always verify the current position on the IRAS Stamp Duty page and consult a licensed conveyancing lawyer or tax specialist before committing to any property transaction. The worked examples in this guide are illustrative and assume no market valuation adjustments; your actual BSD may differ if IRAS determines a market value higher than the purchase price.

0 Comments