Quick Answer — Key Takeaways

- Seller’s Stamp Duty (SSD) of 12%, 8%, or 4% applies if you sell within 3 years of purchase (private residential properties)

- Agent commission is typically 1–2% of sale price — negotiable; CEA-registered agents only

- CPF funds used must be refunded to CPF OA with Accrued Interest (compounded at 2.5% p.a.) upon sale

- The sale process from OTP to legal completion typically takes 10–12 weeks for private property; 8–12 weeks for HDB

- Outstanding mortgage must be discharged from sale proceeds; early repayment penalty may apply (lock-in period)

- No Capital Gains Tax in Singapore — profits from property sales are generally not taxed unless you are classified as a property trader by IRAS

- Decoupling a property before sale may reduce ABSD on a subsequent purchase but requires careful legal structuring to avoid Section 33A anti-avoidance provisions

Selling Property in Singapore — Overview

Singapore’s property market has no Capital Gains Tax — meaning that profits from the sale of residential property are generally not subject to income tax, provided IRAS does not classify you as conducting a property trading business. However, selling a property in Singapore does involve a web of stamp duties, CPF refund obligations, agent fees, legal costs, and outstanding loan discharges. Understanding these costs upfront prevents unpleasant surprises at the point of sale.

The Seller’s Stamp Duty (SSD) — introduced in January 2011 and most recently recalibrated in April 2023 — is the most significant policy lever for sellers. At 12% for properties sold within the first year of purchase, SSD is designed to deter speculative flipping. This guide covers every major cost and step for selling a private residential property (condo, landed, or HDB) in Singapore in 2026.

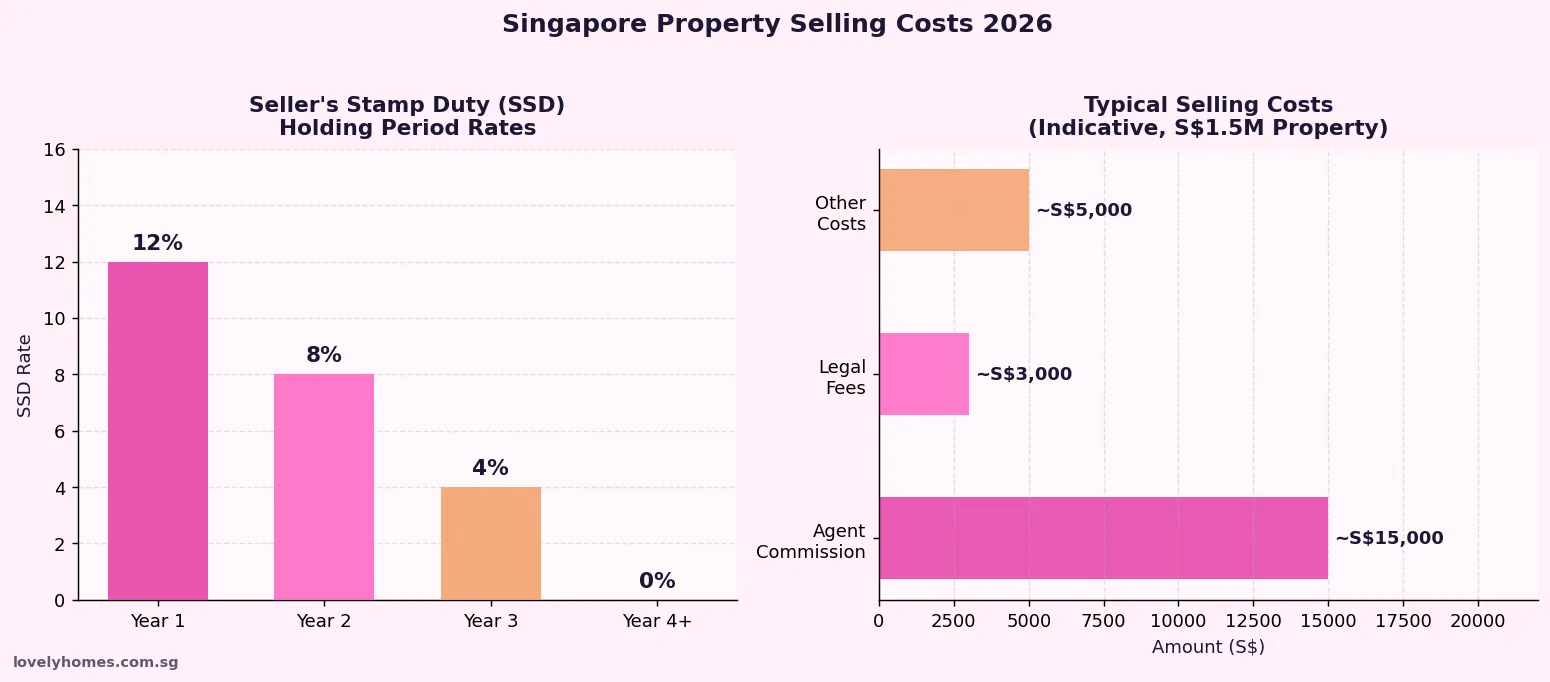

Seller’s Stamp Duty (SSD) — Rates and Rules

Seller’s Stamp Duty is payable by the seller if a residential property is sold within 3 years of its purchase date (for private properties). The rates are based on the higher of the sale price or market value:

| Holding Period | SSD Rate (Current, from Apr 2023) | SSD on S$1.5M Sale |

|---|---|---|

| Up to 1 year | 12% | S$180,000 |

| More than 1, up to 2 years | 8% | S$120,000 |

| More than 2, up to 3 years | 4% | S$60,000 |

| More than 3 years | 0% | Nil |

HDB flats are not subject to SSD, but have their own MOP (Minimum Occupation Period) of 5 years — during which the flat cannot be sold on the resale market at all.

All Costs When Selling Your Property

| Cost | Typical Amount | Paid by / When |

|---|---|---|

| Agent Commission | 1–2% of sale price | Seller; at completion |

| Legal Fees (conveyancing) | ~S$2,500–S$4,000 | Seller; at completion |

| Seller’s Stamp Duty (SSD) | 0–12% of sale price (if <3 years) | Seller; within 14 days of OTP exercise |

| Mortgage Early Repayment Penalty | 0.75–1.5% of outstanding loan (if in lock-in) | Seller; upon full redemption at completion |

| CPF Refund (OA + Accrued Interest) | All CPF used + 2.5% p.a. compound interest | Mandatory; deducted from proceeds at completion |

| Property Tax (prorated to sale date) | Varies by AV; prorated to completion date | Seller; adjusted at completion |

| HDB Admin Fee (HDB resale only) | S$40–S$80 | Seller; to HDB |

Worked Example: Selling a S$1.5M Condo Purchased 2 Years Ago

Scenario: SC seller, selling a condo purchased in April 2024 for S$1.4M, now selling in April 2026 at S$1.5M. Outstanding bank loan: S$900,000. CPF used: S$200,000 OA + S$10,000 accrued interest.

- Gross Sale Price: S$1,500,000

- Less SSD (8% × S$1.5M, sold in year 2): −S$120,000

- Less Agent Commission (1.5%): −S$22,500

- Less Legal Fees: −S$3,000

- Less Outstanding Loan Redemption: −S$900,000

- Less CPF Refund (S$200K + S$10K interest): −S$210,000

- Net Cash Proceeds to Seller: S$1,500,000 − S$120,000 − S$22,500 − S$3,000 − S$900,000 − S$210,000 = S$244,500

- Of which cash in hand (after CPF returned to CPF, not to pocket): ~S$244,500 (cash) + S$210,000 returned to CPF OA

Note: This example excludes any early repayment penalty on the bank loan. Verify with your bank and a property consultant. IRAS may treat profits as income if you are assessed as a property trader — consult a tax professional if you have sold multiple properties in recent years.

The Private Property Sale Process — Step by Step

For a private residential property (condominium or landed), the sale process broadly follows these stages over 10–12 weeks:

- Appoint a CEA-licensed agent (or sell directly). Agent markets the property, manages viewings, and facilitates negotiations.

- Accept an offer and grant an OTP. The buyer pays an Option Fee (typically 1% of agreed price). The OTP is valid for 14 days (standard) — extendable to 21 days by agreement.

- Buyer exercises OTP — pays the balance 4–9% deposit within the OTP period. Both buyer and seller appoint conveyancing solicitors.

- Solicitors conduct due diligence — title search, CPF charge check, Inland Revenue caveats, mortgagee consent if applicable.

- Completion — typically 8–10 weeks after OTP exercise. Sale proceeds are disbursed, mortgage is redeemed, CPF is refunded, and keys are handed over.

Frequently Asked Questions

Is there Capital Gains Tax on property sales in Singapore?

No. Singapore does not impose a Capital Gains Tax on property sales by individuals. Profits from property sales are not taxable — provided IRAS does not classify you as a property trader (i.e. someone who buys and sells properties as a business, subject to income tax on profits). If you have sold multiple properties in a short period, consult a tax professional to confirm your IRAS classification. The Inland Revenue Authority of Singapore (IRAS) administers all property tax matters.

How is the CPF refund calculated when I sell my property?

Upon selling your property, you must refund to your CPF OA: (1) all CPF funds withdrawn for the property (down payment, monthly instalments, BSD, legal fees funded by CPF), plus (2) accrued interest at 2.5% per annum, compounded annually, on those withdrawn amounts. This refund goes back into your CPF OA — it is not a tax, but it reduces the cash proceeds you receive. The CPF Board calculates the exact refund amount at completion. For long-held properties with large CPF withdrawals, accrued interest can be significant.

What if the sale price is less than the outstanding loan and CPF refund?

If the sale proceeds are insufficient to fully redeem the outstanding mortgage and refund all CPF funds with accrued interest, you would face a shortfall. In this scenario, you would need to top up the difference in cash. This is sometimes called a “negative sale.” To avoid this situation, sellers should always compute their minimum viable sale price before listing — accounting for loan balance, CPF refund, SSD, agent fees, and legal costs.

Can I avoid SSD by transferring the property to a family member?

No. SSD applies to all legal transfers of residential property within the holding period — including transfers to family members, whether by sale, gift, or trust arrangement. IRAS treats these as disposals subject to SSD. Section 33A of the Stamp Duties Act also provides anti-avoidance powers allowing IRAS to look through artificial arrangements designed to circumvent stamp duty obligations. Seek advice from a qualified stamp duty lawyer before attempting any form of property restructuring.

What happens if I have an HDB bank loan and sell before 3 years?

Unlike private property, HDB flats carry no SSD on their own — however, HDB resale flats cannot be sold during the 5-year MOP. If you have a bank loan (not an HDB concessionary loan) on a private property, an early redemption penalty (clawback) of 0.75%–1.5% of the outstanding loan may apply if you sell during the loan’s lock-in period (typically 1–3 years). Check your bank’s loan terms carefully before committing to sell. HDB concessionary loans do not carry lock-in penalties.

Related Articles

Full SSD rates, holding periods, and remissions

ABSD Singapore 2026

ABSD rates when buying your next property

CPF for Property Purchase

CPF accrued interest and refund rules explained

Decoupling Guide 2026

60% ABSD reality, anti-avoidance, and Section 33A

Property Tax Singapore 2026

Owner-occupier vs investor rates and AV assessment

0 Comments