Good Class Bungalow (GCB) Singapore 2026: Complete Guide to Eligibility, Areas, Prices and Acquisition Costs

Quick Answer: Good Class Bungalow (GCB) at a Glance

- Eligibility: Singapore Citizens only — Permanent Residents and foreigners cannot purchase GCBs

- Minimum Plot: 1,400 sqm (~15,069 sqft) as defined by URA; maximum site coverage 40%; height limit 2 storeys plus attic

- Price Range: S$15M–S$150M+ depending on area tier and plot size; median psf ~S$2,100 (2025)

- Number of GCBs: Approximately 2,700–2,800 units across 39 gazetted GCB areas in Singapore

- BSD (S$28M example): Approximately S$2.07M (8% marginal rate above S$6M)

- ABSD: Nil for SC buying first residential property; 20% for SC buying second; 35% for PR; 60% for foreigners

- Annual Transactions: ~90–190 transactions per year; 2021 peak of ~187 driven by low interest rates

- Key GCB Areas: Nassim Road/Hill (ultra-prime), Cluny Hill, Caldecott Hill, Leedon Road, Swiss Club Road

In the hierarchy of Singapore’s residential property market, the Good Class Bungalow (GCB) occupies a category of its own. Protected by strict URA planning parameters and restricted to Singapore Citizens only, GCBs are the most tightly regulated — and among the most coveted — properties in the country. With fewer than 2,800 units spread across 39 designated areas, the GCB market is defined by scarcity, exclusivity, and the kind of long-term value resilience that institutional investors typically associate with trophy assets.

This guide explains the planning rules, buyer eligibility, price tiers, transaction trends, and acquisition costs that define Singapore’s GCB market in 2026 — with a full worked example of what it costs a Singapore Citizen to purchase a S$28 million bungalow in a prime GCB area.

What Is a Good Class Bungalow? The URA Definition

A Good Class Bungalow is a detached dwelling house located within one of URA’s 39 gazetted GCB Areas. The planning parameters are set by URA’s Master Plan and are non-negotiable: the minimum land area is 1,400 sqm (approximately 15,069 sqft). Unlike standard landed property elsewhere in Singapore, GCBs cannot be subdivided below this threshold — a deliberate policy choice by URA to preserve the low-density, high-greenery character of these enclaves.

Additional development controls apply: site coverage is capped at 40% (meaning at most 560 sqm of a 1,400 sqm plot can be covered by the building footprint); building height is limited to two storeys plus an attic and a basement; and setback requirements ensure generous greenery between structures. The effect is a de facto exclusivity floor: even a plot at the minimum threshold costs between S$15 million and S$50 million depending on location, and the construction of a purpose-built bungalow adds a further S$3 million–S$8 million at current build costs.

Who Can Buy a GCB in Singapore?

Only Singapore Citizens may purchase landed residential property in gazetted GCB Areas. This restriction is absolute — Singapore Permanent Residents, foreigners, and companies (including Singapore-incorporated entities) are ineligible unless specific ministerial approval is obtained, which is rarely granted for private residential purposes. The restriction applies regardless of whether the buyer is a high-net-worth individual, a family office, or a foreign sovereign wealth fund — GCBs are citizen-only assets.

This legal restriction is administered under the Residential Property Act (RPA), overseen by the Singapore Land Authority (SLA). Any transaction involving a non-citizen buyer requires prior written approval from the Minister for Law, and approvals for GCBs are essentially never granted for purely residential purposes. Prospective foreign buyers wishing to invest in Singapore’s landed property market are directed to Sentosa Cove, which operates under a separate framework.

The 39 GCB Areas: Location, Tier, and Character

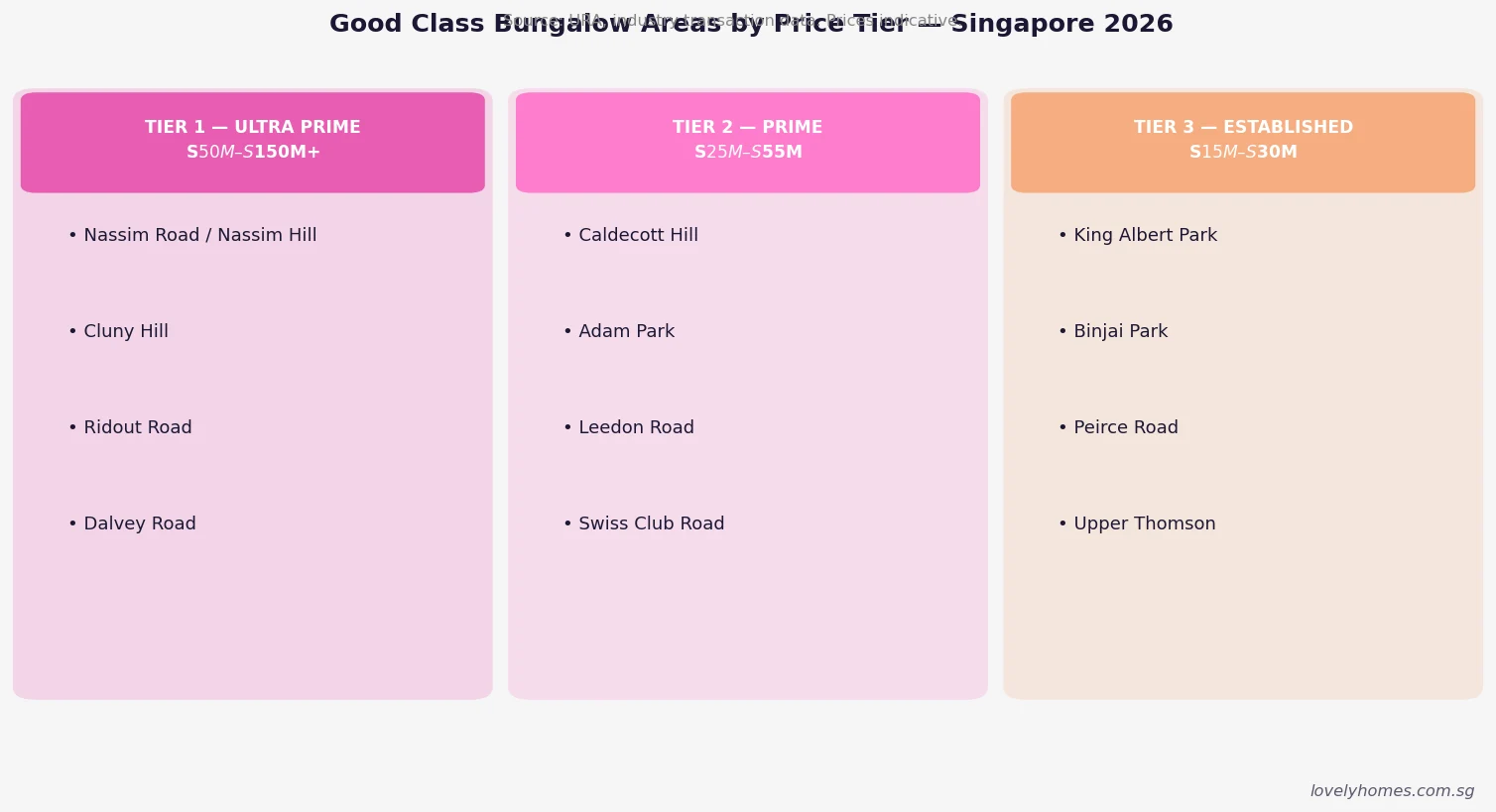

URA has gazetted 39 GCB Areas across Singapore, concentrated primarily in the central-west corridor between Bukit Timah, Tanglin, and Holland. The areas range from ultra-prime enclaves — where plots on Nassim Road have traded at record prices exceeding S$4,000 psf of land — to more established residential pockets in Peirce Road or Binjai Park where values are more accessible.

The three broad pricing tiers (illustrated in Figure 1) reflect differences in land scarcity, proximity to Orchard Road and the CBD, plot sizes, and the historic prestige of each enclave. Tier 1 (Ultra-Prime) covers Nassim Road/Hill, Cluny Hill, Ridout Road, and Dalvey Road — areas where transaction prices typically start at S$50 million and have reached S$148 million (Nassim Road, 2021) for landmark plots. Tier 2 (Prime) encompasses Caldecott Hill, Adam Park, Leedon Road, and Swiss Club Road — where a mid-sized plot at S$25 million–S$55 million represents reasonable market value. Tier 3 (Established) includes King Albert Park, Binjai Park, Peirce Road, and Upper Thomson, where the GCB premium is significant but entry-level plots can be found in the S$15 million–S$30 million range.

GCB Transaction Trends: Volume and Pricing 2019–2025

Despite representing a tiny slice of Singapore’s overall residential property market, GCB transactions attract disproportionate attention from analysts and media because they serve as a barometer of ultra-high-net-worth (UHNW) confidence in Singapore as a wealth hub.

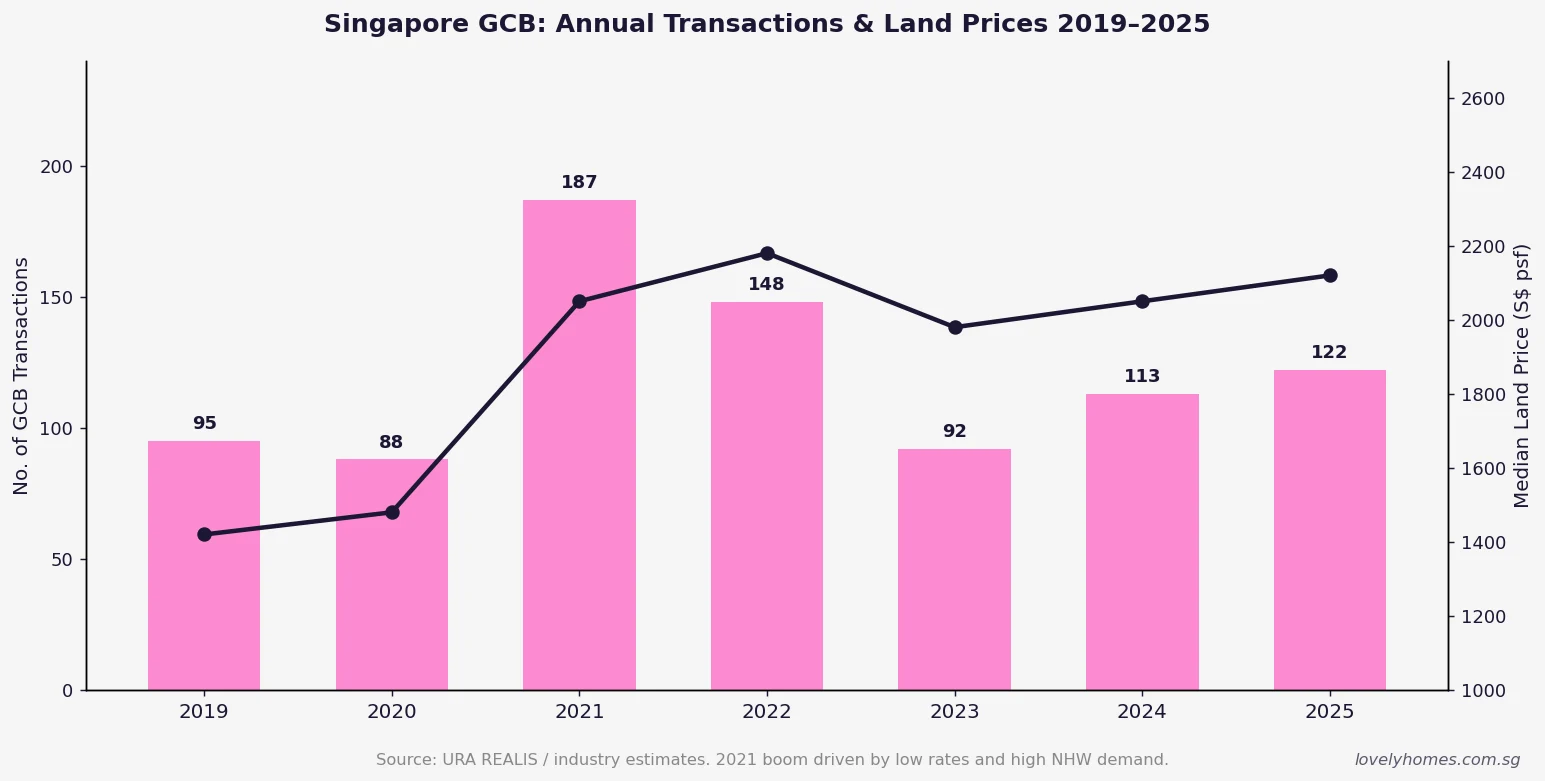

The 2021 boom — when GCB transactions surged to approximately 187 — was driven by a confluence of factors: historically low global interest rates, Singapore’s successful management of COVID-19 relative to peer cities, and an influx of ultra-high-net-worth families relocating their base to Singapore. Median land prices peaked around S$2,180 psf in 2022 before softening modestly as global interest rates rose. By 2025, transaction volumes had stabilised at approximately 120 per year and median land prices had recovered to roughly S$2,120 psf — demonstrating the market’s characteristic price resilience even as volumes remained well below the 2021 peak.

The long-run story is one of consistent appreciation: GCB land values have risen from approximately S$1,420 psf in 2019 to S$2,120 psf in 2025 — a compound annual growth rate of approximately 6.9% over six years, outpacing Singapore’s Private Residential Property Price Index over the same period.

Buying Costs: BSD, ABSD, and Total Acquisition Outlay

Acquiring a GCB involves several layers of transaction cost. The most significant are Buyer’s Stamp Duty (BSD) and, where applicable, Additional Buyer’s Stamp Duty (ABSD). Both are administered by the Inland Revenue Authority of Singapore (IRAS).

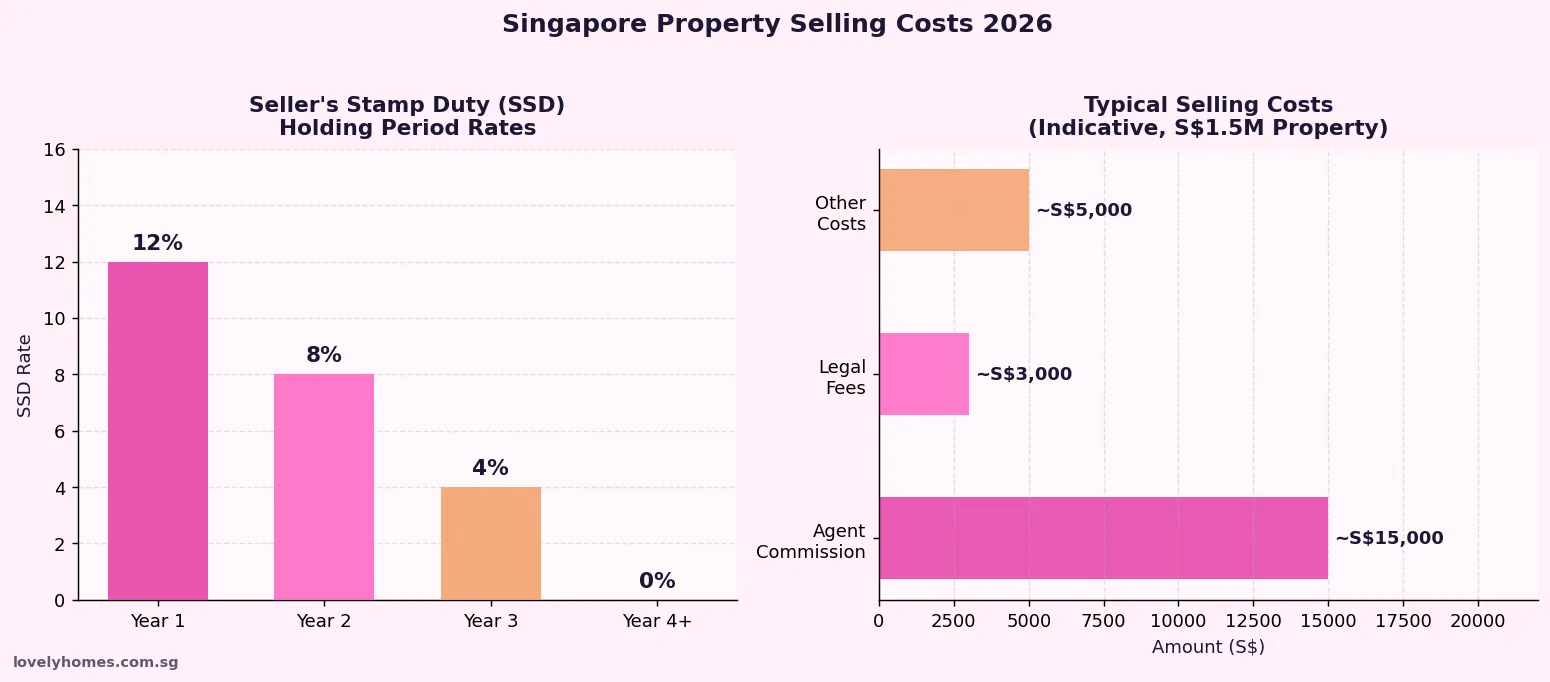

BSD applies to all property purchases in Singapore and is computed on the purchase price or market value (whichever is higher) at progressive rates. For a GCB purchase at S$28 million, the BSD calculation is: 1% on the first S$180,000 (S$1,800) + 2% on the next S$180,000 (S$3,600) + 3% on the next S$640,000 (S$19,200) + 4% on the next S$500,000 (S$20,000) + 5% on the next S$1,500,000 (S$75,000) + 6% on the next S$1,500,000 (S$90,000) + 7% on the next S$1,500,000 (S$105,000) + 8% on the remaining S$22,000,000 (S$1,760,000). Total BSD: approximately S$2,074,600.

ABSD is determined by the buyer’s residency status and the number of residential properties already owned. Singapore Citizens buying their first residential property pay nil ABSD; buying a second, 20%; buying a third or subsequent, 30%. PRs pay 5% on first, 30% on second. Foreigners pay 60% flat.

GCB Key Facts: Summary Table

| Parameter | Detail | Governing Body |

|---|---|---|

| Minimum plot size | 1,400 sqm (~15,069 sqft) | URA Master Plan |

| Maximum site coverage | 40% of plot area | URA |

| Maximum height | 2 storeys + attic + basement | URA |

| Buyer eligibility | Singapore Citizens only | SLA / Residential Property Act |

| No. of gazetted GCB areas | 39 | URA |

| Estimated GCB stock | ~2,700–2,800 units | URA / industry |

| Annual transactions (2025 est.) | ~120 | URA REALIS |

| Median land price (2025 est.) | ~S$2,100–S$2,200 psf | URA REALIS |

| BSD (at S$28M) | ~S$2,074,600 (~7.4% of price) | IRAS |

| ABSD (SC, 1st property) | Nil | IRAS |

Worked Example: Buying a S$28M GCB (SC, First Property)

Mr Tan Wei Ming is a Singapore Citizen entrepreneur, aged 52, with no existing residential properties. He wishes to acquire a freehold GCB plot in the Caldecott Hill area (Tier 2 prime) measuring 1,650 sqm at a price of S$28,000,000 — approximately S$1,697 psf of land.

BSD: Computed per IRAS progressive rates as detailed above. Total BSD: approximately S$2,074,600 (7.4% of purchase price).

ABSD: Nil — Mr Tan is a Singapore Citizen buying his first residential property.

Financing: Maximum Loan-to-Value (LTV) for a non-HDB property purchase by an individual with no existing mortgage is 75% from a bank. Loan quantum = S$21,000,000. At an indicative 3.0% per annum over a 25-year tenure, the estimated monthly instalment is approximately S$99,600/month (indicative; subject to TDSR compliance and bank assessment). Cash downpayment (25%) = S$7,000,000.

Total upfront cash outlay: S$7,000,000 (downpayment) + S$2,074,600 (BSD) + approximately S$18,000 (legal/disbursements) = approximately S$9,092,600.

TDSR: At a monthly income of S$300,000 (indicative for this profile), monthly mortgage of S$99,600 equates to a TDSR of 33.2% — within MAS’s 55% TDSR cap. UHNW buyers with predominantly investment or dividend income should note that banks apply haircuts to variable income streams in TDSR assessment; structuring advice from a private bank relationship manager is advisable before committing.

Why GCBs Matter: The Investment Perspective

GCBs are among the few truly scarce assets in Singapore’s property market. The total GCB stock is essentially fixed — URA’s planning framework prevents new GCB areas from being gazetted, and the subdivision rules prevent existing plots from being broken up. This structural supply ceiling, combined with Singapore’s political stability, rule of law, and its role as a global wealth management hub, creates a long-run demand and supply dynamic that has supported price appreciation even through global financial crises and pandemic disruptions.

Compared with trophy residential property in peer cities — Hong Kong, London, Sydney — Singapore’s GCB market offers a relatively transparent transaction environment (URA REALIS provides full transaction history), robust title security (Torrens system administered by SLA), and no capital gains tax on property disposal. The absence of estate duty (abolished in 2008) further enhances GCBs as intergenerational wealth transfer vehicles for Singapore Citizens.

What Might Come Next in the GCB Market

Several macro factors are worth monitoring. Singapore’s Family Office (FO) sector has grown to over 1,500 registered single-family offices as at 2025, and while GCB purchases require Singapore Citizenship, FO principals who have naturalised as Citizens represent a growing pool of qualified buyers. This gradual structural demand increment — as wealth migration matures into citizenship — is a medium-term tailwind for GCB values, all else equal.

On the supply side, there is occasional discussion of whether URA might ever revise GCB area boundaries or minimum plot sizes. No such revisions have been announced or signalled as at writing. Any regulatory tightening (e.g. raising the minimum plot threshold) would, if anything, reduce future supply and could be price-supportive for existing GCBs. Conversely, a sustained period of high global interest rates constraining UHNW liquidity could suppress transaction volumes further, though historical evidence suggests GCB prices are relatively price-inelastic because they are purchased largely without leverage stress.

Frequently Asked Questions

Can a Singapore Permanent Resident buy a GCB?

No. Only Singapore Citizens may purchase Good Class Bungalows or any landed residential property within gazetted GCB Areas. This restriction is legislated under the Residential Property Act (RPA) and is administered by the Singapore Land Authority (SLA). PRs who wish to purchase landed property in Singapore are limited to non-GCB landed homes (e.g. terrace houses, semi-detached, detached outside GCB Areas), subject to ministerial approval on a case-by-case basis. Even for non-GCB landed, PR buyers must satisfy SLA’s criteria, which are not routinely granted.

How many GCB areas are there in Singapore?

URA has gazetted 39 GCB Areas across Singapore, concentrated primarily in the central-west region (Bukit Timah, Tanglin, Holland, and Caldecott corridors). The total estimated GCB stock is approximately 2,700–2,800 individual bungalows across all 39 areas, making GCBs one of the most limited housing categories in the country. The 39 areas range from the ultra-prime Nassim Road enclave to more accessible established areas such as King Albert Park and Binjai Park.

What is the minimum plot size for a GCB?

The minimum land area for a Good Class Bungalow is 1,400 square metres (approximately 15,069 sqft), as defined in URA’s Master Plan and the Residential Property Act. Plots below this threshold cannot be classified as GCBs. Site coverage is capped at 40%, meaning the building footprint may not exceed 560 sqm on a minimum-sized plot. The height limit is two storeys above ground, with an attic and one basement storey permitted. These controls are enforced by URA as part of Singapore’s statutory development approval process.

What is the BSD on a S$28M GCB purchase?

Buyer’s Stamp Duty (BSD) is calculated at IRAS’s progressive rates: 1% on the first S$180,000 (S$1,800); 2% on the next S$180,000 (S$3,600); 3% on the next S$640,000 (S$19,200); 4% on the next S$500,000 (S$20,000); 5% on the next S$1,500,000 (S$75,000); 6% on the next S$1,500,000 (S$90,000); 7% on the next S$1,500,000 (S$105,000); and 8% on the remaining S$22,000,000 (S$1,760,000). The total BSD is approximately S$2,074,600, equal to about 7.4% of the purchase price. ABSD is nil for a Singapore Citizen purchasing their first residential property.

Are there capital gains taxes when selling a GCB?

Singapore does not levy a capital gains tax on the disposal of property, including GCBs. However, the Seller’s Stamp Duty (SSD) may apply if the property is disposed of within three years of purchase: 12% if sold in the first year, 8% in the second year, and 4% in the third year. SSD does not apply to disposals after the three-year holding period. Property tax — an annual charge based on Annual Value computed by IRAS — continues to apply during ownership at non-owner-occupier rates if the property is tenanted, or owner-occupier rates if it is the owner’s primary residence.

Can a GCB be rented out?

Yes. GCBs may be rented out subject to URA’s rental regulations, which require a minimum tenancy of three consecutive months for the entire dwelling (whole-unit rental). Short-term rentals (less than three months) are not permitted for any private residential property in Singapore. Rental income from a GCB is treated as taxable income for the owner and must be declared to IRAS, though allowable deductions (mortgage interest, property tax, insurance, maintenance) can offset the taxable rental amount. Overseas owners should note that rental income may also trigger tax reporting obligations in their country of tax residence.

How liquid is the GCB market?

The GCB market is characterised by low liquidity relative to the mass-market residential sector. With only 90–190 transactions per year across all 39 areas, average time-on-market for a GCB can range from several months to over a year depending on the specific area, asking price, and macro conditions. This illiquidity is a key risk consideration for buyers who may need to exit within a short timeframe. On the other hand, the market’s depth of UHNW demand — particularly in ultra-prime areas — means that correctly priced GCBs in Tier 1 areas rarely trade at distressed prices even in down-cycles.

Related Articles

- Singapore Landed Property Buying Guide 2026

- Singapore Shophouse Investment Guide 2026

- ABSD Singapore 2026: Complete Guide

- Seller’s Stamp Duty (SSD) Singapore 2026

- Foreigners Buying Property in Singapore 2026

- Singapore Property Tax Guide 2026

- Singapore Prime District Property Guide 2026

- Rental Yield vs Capital Gain Singapore 2026

Disclaimer: All GCB prices, transaction volumes, and land price figures cited in this article are estimates based on publicly available data from URA REALIS, industry research, and secondary sources as at Q1 2026. They are for general information purposes only and do not constitute financial, investment, legal, or tax advice. GCB transactions involve substantial sums and complex regulatory requirements. Prospective buyers should engage a Singapore-qualified solicitor, consult the Singapore Land Authority (sla.gov.sg), verify BSD and ABSD liabilities directly with IRAS (iras.gov.sg), and obtain independent property valuations before making any commitment. This article does not constitute an offer to sell or a solicitation to purchase any property.