- Valuation Limit (VL): The lower of the purchase price or the property’s market valuation. CPF usage is capped at 100% of the VL for down-payments and loan instalments combined.

- Withdrawal Limit (WL): 120% of the VL — the absolute maximum CPF that may be drawn for a property (for leases with ≥ 60 years remaining when the youngest buyer turns 55).

- Accrued interest: CPF Board charges 2.5% p.a. on all CPF Ordinary Account (OA) monies used for property. On sale, you must refund the principal plus accrued interest to your CPF account.

- Age 55 rule: After age 55, you must first set aside the Basic Retirement Sum (BRS) or Full Retirement Sum (FRS) in your Retirement Account before further CPF OA can be used for property.

- Lease adequacy: CPF OA cannot be used if the remaining lease is under 20 years; for shorter leases (20–59 years), a pro-rated WL applies. The lease must cover the youngest buyer to age 95 for unrestricted use.

- HDB loans: Up to 80% LTV from HDB; CPF OA can cover the full 20% cash/CPF downpayment. Bank loans: 75% LTV with 5% mandatory cash; CPF can cover the remaining 20% downpayment.

- Refund on sale: Net sale proceeds first repay the bank/HDB loan; remaining cash replenishes CPF up to the refund amount before you receive any cash proceeds.

What Is the CPF Ordinary Account and How Is It Used for Property?

The Central Provident Fund (CPF) is Singapore’s mandatory social security savings system, administered by the CPF Board. Every employed Singapore Citizen and Permanent Resident contributes a percentage of their monthly wages into three CPF accounts: the Ordinary Account (OA), the Special Account (SA), and the MediSave Account (MA). The OA earns a guaranteed 2.5% per annum (p.a.) interest, currently with a floor rate maintained by the CPF Board. It is the OA that may be used for housing — specifically for the purchase or construction of HDB flats, Executive Condominiums (ECs), and private residential property, as well as for home protection insurance premiums and property tax.

The CPF framework for property withdrawals is governed by the CPF Act (Cap. 36) and the CPF Housing Schemes administered by the CPF Board. Two concepts sit at the heart of the framework: the Valuation Limit (VL) and the Withdrawal Limit (WL). Understanding both — and their interaction with accrued interest, lease adequacy rules, and the post-55 retirement sum requirements — is essential for every property buyer in Singapore.

Valuation Limit (VL) and Withdrawal Limit (WL) Explained

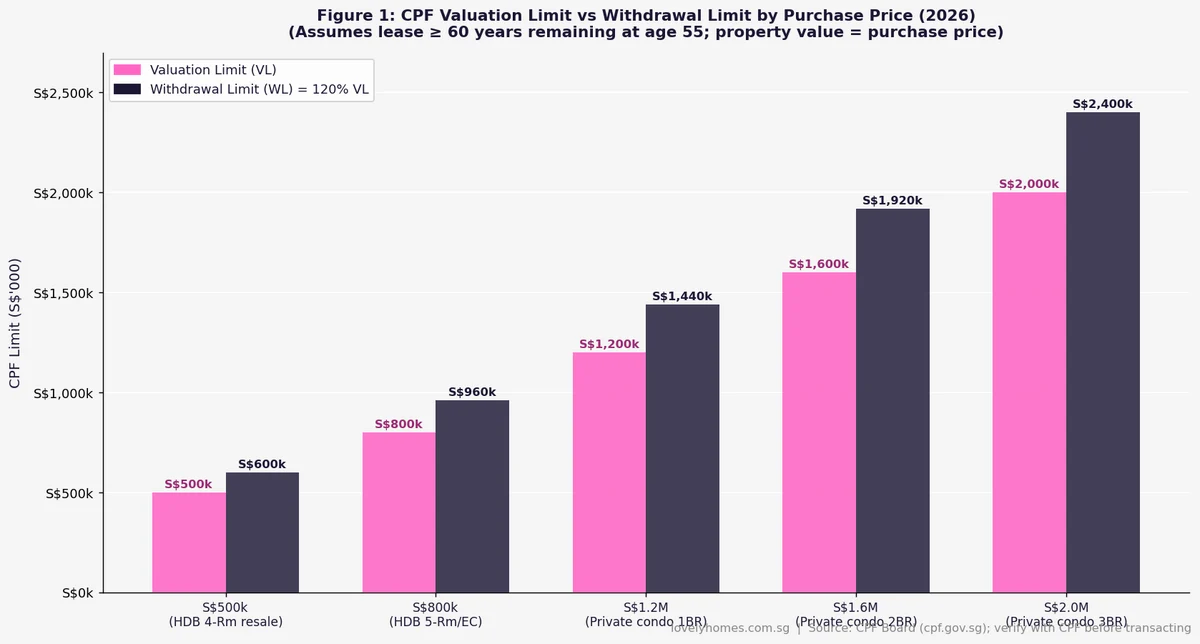

The Valuation Limit (VL) is defined as the lower of the purchase price or the Chief Valuer’s assessed market value of the property at the time of purchase. For most buyers transacting at or near market price, the VL will equal the purchase price. For buyers paying a significant premium above valuation — common in competitive en-bloc or collective-sale situations — the VL will be capped at the lower valuation figure. CPF OA monies used for the downpayment and all subsequent monthly mortgage instalments together cannot exceed the VL.

The Withdrawal Limit (WL) is set at 120% of the VL. This is the absolute ceiling on the total amount of CPF OA that may be used for a single property across the entire ownership period. The WL is higher than the VL to accommodate the progressive drawdown of CPF for monthly instalments: even after the full VL is exhausted for the principal portion, buyers may continue using CPF for instalments up to the WL threshold. Figure 1 visualises the VL and WL across five representative purchase price scenarios.

Lease Adequacy: How Property Lease Length Affects CPF Usage

The CPF Board applies lease adequacy rules to protect CPF members from over-investing their retirement savings in depreciating assets. For a buyer to enjoy unrestricted CPF usage up to the full WL (120% of VL), the property’s remaining lease must cover the youngest buyer from the date of purchase to at least age 95. In practice, this means a 30-year-old buying a property with an 80-year remaining lease has no CPF restriction (80 years covers them to age 110 well above 95). However, a 45-year-old buying a 99-year flat built in 1985 — meaning approximately 58 years of lease remain — would face a pro-rated WL calculation, since the lease does not cover them to age 95 (45 + 58 = 103: marginal case; check CPF Board calculator for exact figure).

If a property’s remaining lease at the time of purchase is under 30 years, CPF OA cannot be used at all. Properties with remaining leases between 30 and 59 years at the time the youngest buyer turns 55 are subject to a reduced pro-rated WL — the CPF Board will provide an exact figure through its online calculator. This lease adequacy framework was substantially tightened in a series of regulatory updates in 2019 and 2021 and is particularly relevant for older HDB resale flats and ageing freehold private properties on a 99-year lease nearing expiry.

| Remaining Lease (at purchase) | CPF Usage Permitted? | WL Cap | Notes |

|---|---|---|---|

| ≥ 60 years AND covers youngest buyer to 95 | Yes — full WL | 120% of VL | Standard case for most new and resale purchases |

| 30–59 years | Yes — pro-rated WL | Reduced (CPF Board calculator) | Common for older HDB flats built pre-1985 |

| 20–29 years | Restricted use only | Significantly reduced | CPF Board approval required |

| Under 20 years | No CPF usage | Nil | Full cash purchase only |

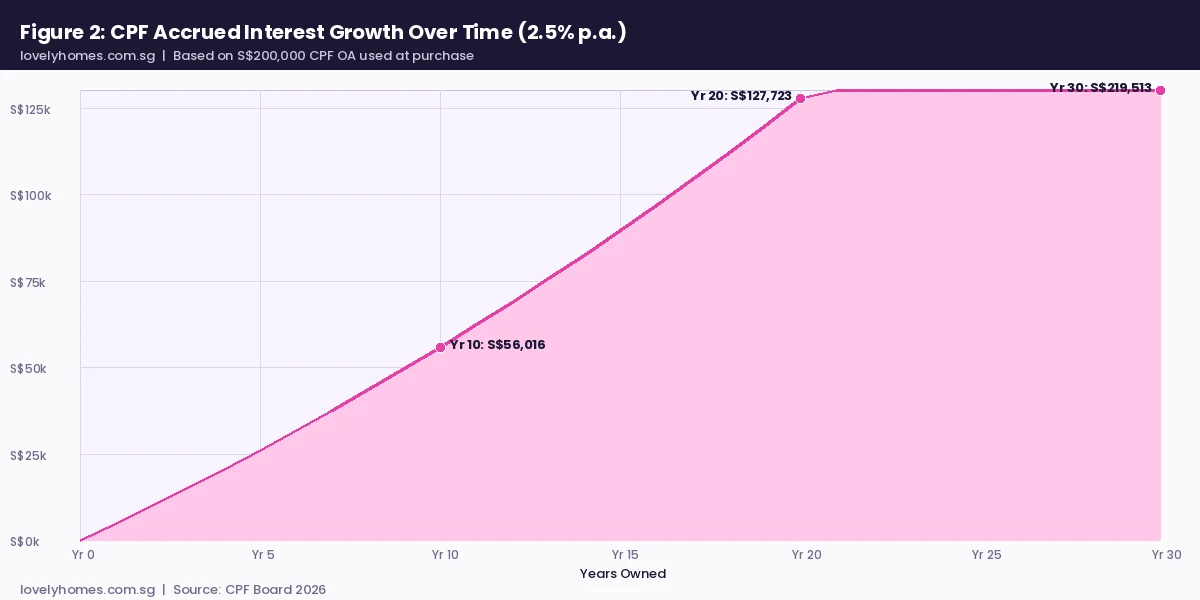

Accrued Interest: The Hidden Cost of Using CPF for Property

One of the most frequently misunderstood aspects of CPF housing withdrawals is the concept of accrued interest. When you use CPF OA monies for your property, the CPF Board does not treat those funds as a gift — they are treated as a loan from your retirement account. The 2.5% p.a. interest that your OA would have earned had the money not been used for property continues to accumulate as a notional debt against your CPF housing account. This means that when you sell your property, you must refund both the principal amount withdrawn and all the accrued interest to your CPF OA (or Retirement Account if you are over 55). You do not pay this interest out of pocket while you own the property — it accrues notionally — but it becomes payable at the point of sale from your net sale proceeds.

Figure 2 illustrates the compounding effect: on a S$200,000 CPF withdrawal at the 2.5% p.a. OA rate, the accrued interest reaches approximately S$28,000 by Year 5, S$62,000 by Year 10, and S$219,000 by Year 30. The total CPF refund required after 30 years of ownership is thus approximately S$419,000 — more than double the original withdrawal. This is not a cash loss if property prices appreciate sufficiently, but it means that the net cash proceeds from a property sale are significantly lower than buyers sometimes expect. For HDB upgraders who use maximum CPF for their flat purchase, this accrued interest obligation can materially affect the cash available for a subsequent private property purchase.

CPF Usage After Age 55: Retirement Sum Rules

Once a CPF member turns 55, the CPF Board creates a Retirement Account (RA) by sweeping funds from the Special Account (SA) and then OA into the RA up to the applicable Full Retirement Sum (FRS). For 2026, the FRS is S$213,000 and the Basic Retirement Sum (BRS) is S$106,500. The Enhanced Retirement Sum (ERS) is S$319,500 (150% of FRS).

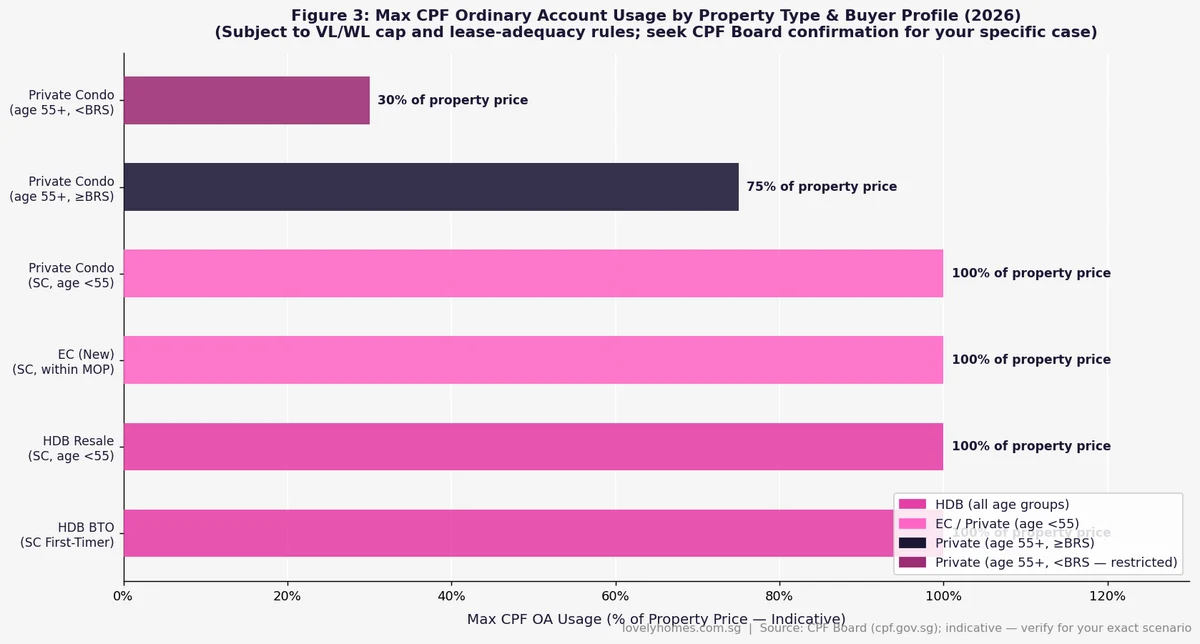

After age 55, you may continue using your remaining OA for property only after setting aside the BRS in your RA — and only if you have pledged your property to cover the BRS shortfall up to the FRS. In practical terms: if your RA balance after the SA and OA sweep equals or exceeds the FRS, you retain full flexibility to use the remaining OA for property instalments. If your RA is below the FRS but above the BRS and you have pledged your property, you may also continue using OA. However, if your RA is below the BRS, no further CPF OA can be used for property until the BRS shortfall is resolved. Figure 3 summarises the maximum CPF OA usage across different buyer profiles.

CPF for HDB Flats: HDB Loan vs Bank Loan Rules

Singapore Citizens (SCs) purchasing an HDB flat have the option of a concessionary HDB loan (administered by HDB, funded by the government) or a bank loan from a commercial lender. The loan type significantly affects how CPF may be deployed. Under an HDB loan (LTV up to 80%, interest rate currently 2.6% p.a.), buyers may use CPF OA to cover the full downpayment — there is no mandatory cash component for the 20% downpayment, and CPF can cover 100% of the downpayment. Under a bank loan (LTV 75%), buyers must pay a minimum of 5% of the purchase price in cash, but the remaining 20% downpayment (and monthly instalments within the WL) can come from CPF OA. For first-timer SC couples purchasing an HDB flat, the Enhanced CPF Housing Grant (EHG) and Proximity Housing Grant (PHG) supplements, administered by HDB, reduce the effective purchase price and therefore the total CPF required, making home ownership more accessible.

CPF for Private Property and Executive Condominiums

For private residential property (and ECs, which are treated as private property for CPF purposes after their five-year Minimum Occupation Period), the CPF OA may be used for: the downpayment (above the mandatory 5% cash for bank loans); monthly loan instalments to the bank; and stamp duties. The VL and WL rules apply as described above. It is important to note that for private property, CPF usage for the downpayment is capped at the difference between the purchase price and the bank loan amount (i.e. the cash/CPF portion of the downpayment). CPF cannot be used to pay the mandatory 5% cash downpayment — that must always come from cash. Stamp duties (BSD and ABSD) may be paid from the CPF OA in some circumstances, but most buyers pay these from cash to preserve CPF for loan servicing.

The CPF Refund Calculation: What You Owe on Sale

When you sell a property, the sequence of repayments from the net sale proceeds is: (1) outstanding bank or HDB loan; (2) seller’s legal fees and agent commissions; (3) CPF refund (principal withdrawn + accrued interest) to CPF OA; (4) any remaining cash to the seller. If the net sale proceeds after paying off the loan are insufficient to cover the full CPF refund, you are not required to top up the shortfall in cash — you simply refund what is available. However, this shortfall means your CPF OA and retirement savings are permanently reduced, which can affect your CPF LIFE monthly payout in retirement and your ability to make future CPF-funded property purchases.

Worked Example: HDB Resale Flat Purchase and Sale

Mr and Mrs Lim are Singapore Citizens, both aged 34. They purchase a Bishan 4-room HDB resale flat for S$750,000 in January 2021. They take an HDB concessionary loan of S$600,000 (80% LTV, 2.6% p.a.) and use S$150,000 from their combined CPF OA for the downpayment. Over five years of ownership, they make monthly CPF OA contributions totalling an additional S$120,000 towards mortgage instalments, bringing total CPF drawn to S$270,000.

Valuation Limit: S$750,000 (purchase price = valuation). Withdrawal Limit: S$900,000 (120% × S$750,000).

CPF drawn by January 2026 (5 years): S$270,000 principal. At 2.5% p.a. compounding, accrued interest over 5 years ≈ S$270,000 × ((1.025)^5 – 1) = S$270,000 × 0.1314 = approximately S$35,500. Total CPF refund required: S$270,000 + S$35,500 = S$305,500.

Sale in January 2026: Market price S$950,000. Outstanding HDB loan balance ≈ S$540,000. Legal and agent fees ≈ S$16,000. Net proceeds after loan repayment and fees: S$950,000 – S$540,000 – S$16,000 = S$394,000. CPF refund of S$305,500 is repaid to CPF OA; remaining cash proceeds to Mr and Mrs Lim: S$394,000 – S$305,500 = S$88,500. This S$88,500 in cash, combined with the S$305,500 refunded to CPF OA (now available for a new purchase), provides the platform for their next HDB or private property purchase.

What This Means for You: Planning Around CPF Limits

The CPF housing framework is designed to strike a balance between enabling Singaporeans to purchase homes and preserving retirement adequacy. The 2.5% p.a. accrued interest rule and the post-55 retirement sum requirements are both policy tools to prevent CPF members from depleting their retirement savings on property speculation. For long-term owner-occupiers who purchase well-located property and hold through full loan tenure, the accrued interest is offset by capital appreciation — but buyers who purchase at the top of a cycle or sell in a down market may find that the CPF refund obligation leaves them with less cash than expected.

Key planning implications: First, preserve CPF OA capacity for property by minimising voluntary CPF top-ups or top-ups to Special Account (SA) if you anticipate a large property purchase within three to five years — money in SA cannot be used for housing. Second, understand the WL ceiling: once you have used 120% of the VL for a property, no further CPF OA can be drawn for that property regardless of your remaining OA balance. Third, for buyers approaching age 55, model the post-55 retirement sum scenario carefully with a CPF planner — the retirement sum set-aside requirement can significantly reduce the CPF available for property instalments precisely at the point when income typically peaks.

What Might Come Next: CPF Housing Framework Changes to Watch

The CPF Board reviews the housing withdrawal framework periodically, typically in conjunction with the HDB Loan-to-Value (LTV) and MAS TDSR policy cycles. Key forward-looking considerations for 2026–2028 include: the annual upward revision of the BRS and FRS (typically 3%–5% per year), which progressively tightens the CPF available for property after age 55; potential further tightening of the lease adequacy rules for older HDB flats as more pre-1990s stock enters the 30–40-year remaining lease window; and the long-run policy direction on whether CPF should be used more restrictively for investment properties (currently allowed within the same VL/WL framework as owner-occupied units). Buyers should check cpf.gov.sg for the most current BRS/FRS figures, WL calculators and policy updates before transacting.

Frequently Asked Questions: CPF Property Withdrawal Limits Singapore 2026

How much CPF can I use to buy a private condo?

For a private condominium, you can use CPF OA up to the Withdrawal Limit (WL), which is 120% of the Valuation Limit (VL). The VL is the lower of the purchase price or the property’s valuation. For example, on a S$1,500,000 private condo with a valuation of S$1,500,000, the VL is S$1,500,000 and the WL is S$1,800,000. You cannot use more than S$1,800,000 in total CPF OA for that property across its entire ownership period. In practice, most buyers will not reach the WL because the bank will only lend 75% LTV (S$1,125,000 on a S$1,500,000 purchase), leaving S$375,000 for cash/CPF downpayment (of which S$75,000 — 5% — must be cash). The CPF OA portion for the downpayment is thus up to S$300,000, and subsequent instalments continue to draw down against the WL.

Do I have to pay back accrued interest when I sell my property?

Yes. When you sell your property, you must refund the total CPF used (principal + accrued interest at 2.5% p.a. for OA) back to your CPF OA. This refund is automatic — it is deducted from your sale proceeds before you receive any cash. If the net sale proceeds after the mortgage repayment are insufficient to cover the full CPF refund, you repay only what is available; there is no obligation to top up the shortfall in cash. However, this will reduce your CPF OA and retirement savings balance. The accrued interest rate is 2.5% p.a. compounded on OA monies. It is important to note that this is not a cash expense while you own the property — it accrues notionally and becomes payable only at the point of sale or transfer.

Can I use CPF after age 55 to pay for property?

Yes, but with restrictions. After age 55, the CPF Board creates a Retirement Account (RA) and sweeps funds from your Special Account (SA) and, if needed, Ordinary Account (OA) to meet the Full Retirement Sum (FRS) — S$213,000 for 2026. You may continue to use your remaining OA for property instalments only after setting aside the Basic Retirement Sum (BRS, S$106,500 for 2026) in the RA, provided you have pledged your property to cover the BRS-to-FRS gap. If your RA exceeds the FRS, you retain full OA flexibility for property. In all cases, the VL/WL cap continues to apply — you cannot use OA beyond the WL for any single property regardless of age. The BRS and FRS are revised upwards annually, so check cpf.gov.sg for the current year’s figures.

What happens to CPF if the remaining lease on my flat is less than 60 years?

If the remaining lease on an HDB flat or private property is between 30 and 59 years at the time the youngest buyer turns 55, CPF usage is subject to a pro-rated Withdrawal Limit — the CPF Board will calculate a reduced WL based on how much of the lease remains relative to the CPF member’s projected lifespan to age 95. If the remaining lease is under 30 years, CPF OA usage is even more restricted. If it is under 20 years, no CPF OA may be used at all. This rule primarily affects older HDB resale flats built in the 1970s and 1980s, particularly those in mature estates like Toa Payoh, Queenstown and Ang Mo Kio where some units now have fewer than 60 years of lease remaining. Buyers should use the CPF Housing Usage calculator at cpf.gov.sg to check the exact WL for any specific unit before committing to a purchase.

Can CPF be used to pay Additional Buyer’s Stamp Duty (ABSD)?

In principle, CPF OA can be used to pay Buyer’s Stamp Duty (BSD) and Additional Buyer’s Stamp Duty (ABSD) for property purchases under the CPF Approved Housing Schemes. However, given that stamp duties must typically be paid within 14 days of signing the Option to Purchase (OTP) — and CPF disbursements can take several working days — most buyers pay BSD and ABSD from cash to avoid timing risk. For large ABSD bills (e.g. 20% on a second SC purchase, or 60% for a foreign buyer), the quantum involved often far exceeds the buyer’s CPF OA balance, making cash payment the only viable option. Always verify the CPF withdrawal conditions with the CPF Board and your conveyancing lawyer before the OTP exercise.

What is CPF pledging, and how does it affect my property purchase?

CPF pledging is a mechanism that allows property owners over age 55 who have not met the Full Retirement Sum (FRS) in their Retirement Account to pledge their property as security against the shortfall between the Basic Retirement Sum (BRS) and the FRS. By pledging, the member demonstrates to the CPF Board that the eventual sale proceeds of the property will fund the retirement sum gap, and the CPF Board then permits continued use of the OA for mortgage instalments. Pledging does not restrict the owner’s ability to sell or refinance the property — it simply records the CPF Board’s interest in a portion of future sale proceeds. Importantly, pledging can only be applied if the property has sufficient equity (net value after mortgage) to cover the BRS-to-FRS gap. Members should initiate the pledging application through the CPF Board’s online portal.

How does CPF usage affect my net cash proceeds when I sell my property?

CPF usage reduces your net cash-in-hand on property sale, because the refund (principal + accrued interest) comes directly out of your sale proceeds before you receive any cash. For example, if you sell a flat for S$950,000 with an outstanding loan of S$540,000 and a CPF refund obligation of S$305,500, your net cash after costs is only around S$88,500 — even though the gross sale profit appears much larger. The CPF refund is not a loss: the money goes back into your CPF OA where it earns 2.5% p.a. guaranteed and can be reused for your next property purchase. However, it means that sellers who need a large cash sum from their property sale (e.g. for a private property downpayment) must carefully model the CPF refund obligation in their upgrade financial planning.

Related Articles on LovelyHomes

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Property Buying Checklist 2026: 12 Steps from IPA to Key Collection

- Singapore Bridging Loan Guide 2026: How to Bridge the Gap Between Selling and Buying

- Singapore Property Inheritance Guide 2026: Wills, CPF Nominations and Stamp Duty

- Singapore Property Cooling Measures Timeline 2009–2026

- Singapore Prime District Property Guide 2026: D9, D10 and D11 Complete Buyer’s Guide

- Buona Vista & Holland Village Neighbourhood Guide Singapore 2026

Disclaimer: This article is produced by LovelyHomes for general informational purposes only and does not constitute financial, legal or CPF advice. All CPF withdrawal limits, accrued interest calculations, retirement sum figures and property financing examples are indicative and based on CPF Board and HDB published guidelines as at 2026. The Basic Retirement Sum (BRS), Full Retirement Sum (FRS) and Enhanced Retirement Sum (ERS) are revised annually by the CPF Board. Before making any CPF withdrawal for property purposes, readers should verify all information with the CPF Board (cpf.gov.sg), HDB (hdb.gov.sg), and the Inland Revenue Authority of Singapore (iras.gov.sg), and consult a licensed financial adviser and/or property conveyancing lawyer. CPF rules are subject to change; always rely on the official CPF Board website for authoritative guidance.

0 Comments