SSD applies when you sell a Singapore residential property within 3 years of purchase (for properties acquired on or after 11 March 2017).

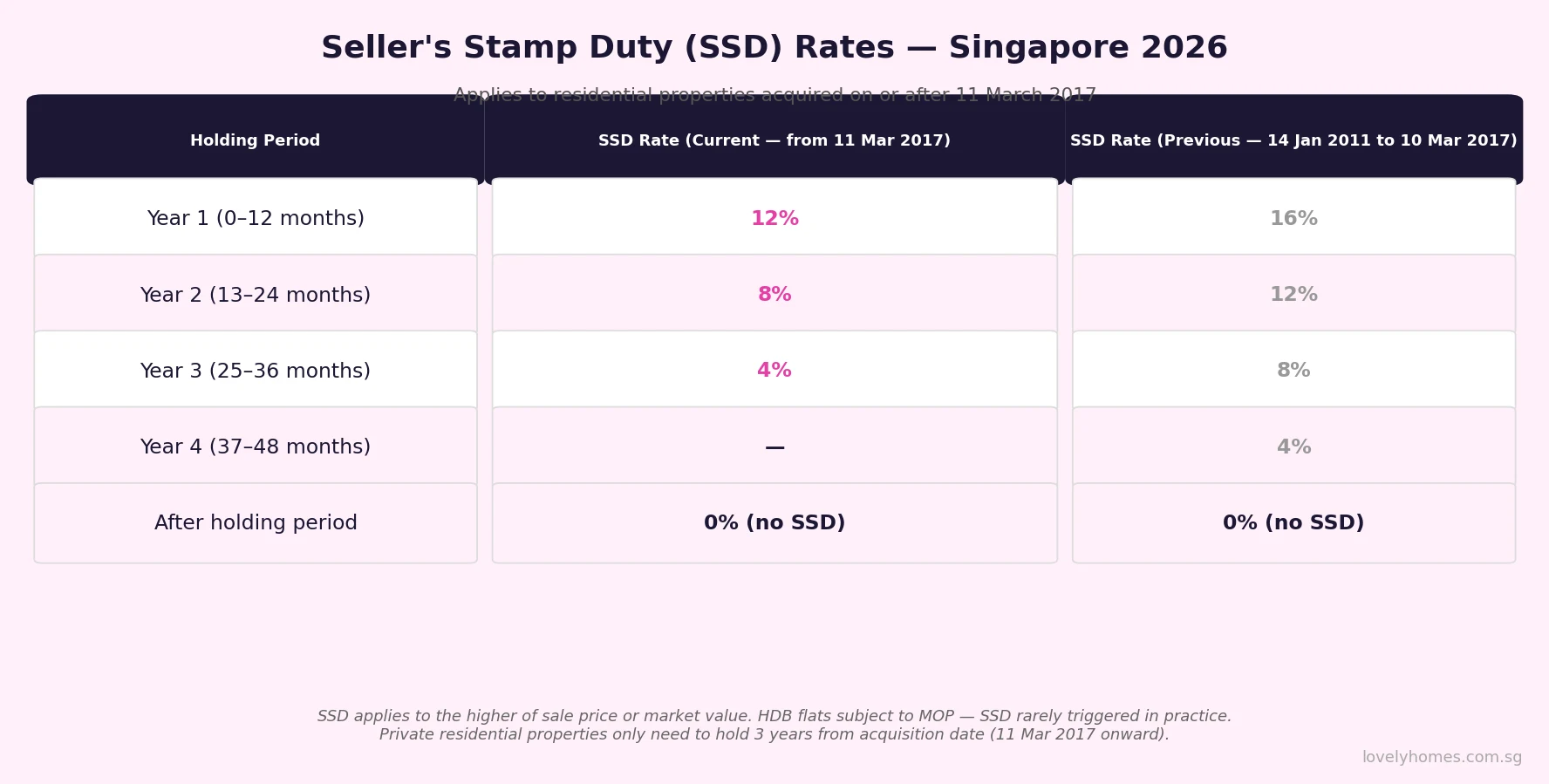

Rates: Year 1 — 12%, Year 2 — 8%, Year 3 — 4%. No SSD after the 3-year holding period.

SSD is levied on the higher of the sale price or market value — IRAS may conduct an independent valuation.

SSD applies to both private residential properties and HDB resale flats — though HDB’s 5-year MOP means SSD is rarely triggered in practice for HDB owners.

SSD must be paid within 14 days of the date of the sale contract or transfer document.

There is no remission for SSD based on citizenship or residency status — it applies equally to Singapore Citizens, PRs and foreigners selling within the holding period.

Prior regime (properties acquired 14 Jan 2011–10 Mar 2017): 4-year holding period, rates of 16% / 12% / 8% / 4%.

What Is Seller’s Stamp Duty (SSD) and Why Does It Exist?

Seller’s Stamp Duty is a tax levied by the Inland Revenue Authority of Singapore (IRAS) when a property owner sells a residential property within a specified holding period after purchase. Unlike the Additional Buyer’s Stamp Duty (ABSD) — which targets the buyer — SSD targets the seller, specifically those who sell quickly after buying. The rationale is straightforward: rapid reselling of residential property is a hallmark of speculative activity. By making short-term flipping expensive, SSD reduces the incentive to buy property purely for a quick profit rather than for genuine occupation or long-term investment.

SSD was first introduced in February 2010 as part of Singapore’s broader property market cooling framework — the same suite of tools that also includes ABSD, the Total Debt Servicing Ratio (TDSR), and Loan-to-Value (LTV) limits. For a full account of how Singapore has used these levers over the years, see our Property Cooling Measures Timeline.

SSD Rates in Singapore — Current and Historical

The rates below reflect the current SSD regime, which has applied to all residential properties acquired on or after 11 March 2017. Properties purchased before that date are subject to the rates in force at the time of acquisition.

Figure 1: SSD rates by holding year — current regime (from 11 March 2017) versus the previous 4-year regime (14 January 2011 to 10 March 2017). Source: IRAS.

Holding Period

SSD Rate — Current (from 11 Mar 2017)

SSD Rate — Previous (14 Jan 2011–10 Mar 2017)

Year 1 (0–12 months from purchase)

12%

16%

Year 2 (13–24 months)

8%

12%

Year 3 (25–36 months)

4%

8%

Year 4 (37–48 months)

—

4%

After holding period

0% (no SSD)

0% (no SSD)

The holding period is measured from the date of purchase — specifically, the date the Option to Purchase (OTP) was exercised, or the date of the Sale & Purchase Agreement if no OTP was used. For an uncompleted property (buying off-plan), IRAS calculates from the date of the S&P Agreement, not the TOP date.

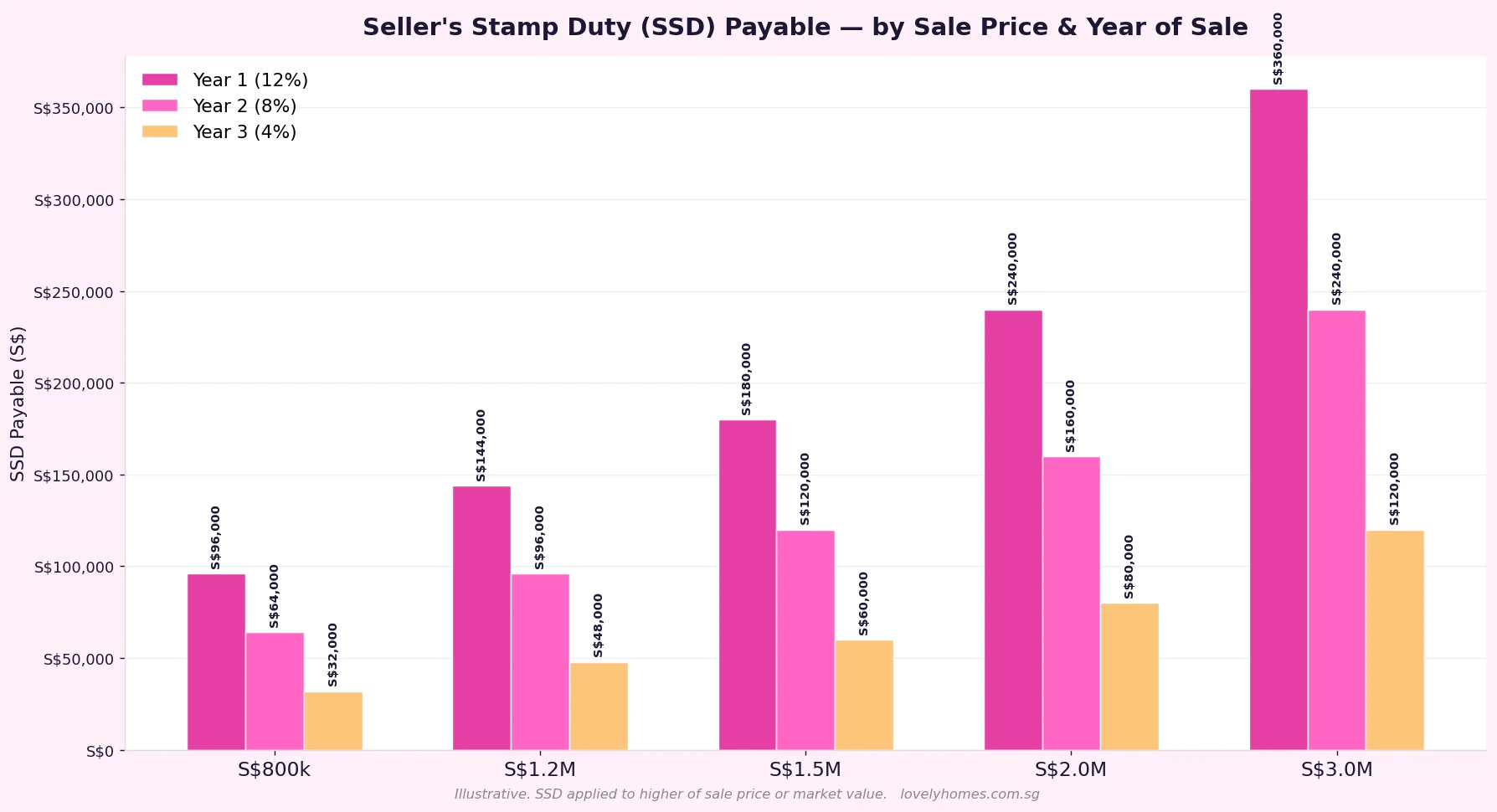

How Much SSD Will You Pay? A Worked Example

SSD is a flat rate applied to the entire sale price or market value — whichever is higher. It is not a progressive or tiered tax.

Example: Mr and Mrs Chen (Singapore Citizens) purchased a S$1.8 million District 10 resale condominium in April 2025. In November 2026 — 19 months after purchase — they receive a job relocation offer and decide to sell. The property is now valued by IRAS at S$1.95 million.

Holding period: 19 months → Year 2 — SSD rate 8%

SSD base: higher of S$1.95M (IRAS valuation) or sale price S$1.9M → S$1,950,000

SSD payable: S$1,950,000 × 8% = S$156,000

Payment due within 14 days of the date of the sale contract.

That S$156,000 would eliminate most of the capital appreciation they had hoped to realise. This is precisely the deterrent effect SSD is designed to create.

Figure 2: Seller’s Stamp Duty payable by sale price and year of sale. All figures illustrative; SSD applied to the higher of sale price or market value.

Does SSD Apply to HDB Flats?

Yes — SSD applies to both private residential properties and HDB resale flats. There is no exemption for HDB sellers. However, in practice, SSD almost never applies to HDB flat sales because of the Minimum Occupation Period (MOP).

Most HDB flats — including BTO, resale, and EC purchases — require a 5-year MOP before the flat can be sold on the open market or rented out in full. Since the current SSD holding period is only 3 years, any HDB flat owner who has completed the MOP has also automatically cleared the SSD period. The SSD and MOP rules only interact in edge cases — for example, if an HDB owner obtains a special exemption to sell before MOP completion (which is rare and requires HDB approval), SSD may still apply to the transaction.

For private residential properties, there is no equivalent of the MOP, so SSD is the primary mechanism discouraging early resale.

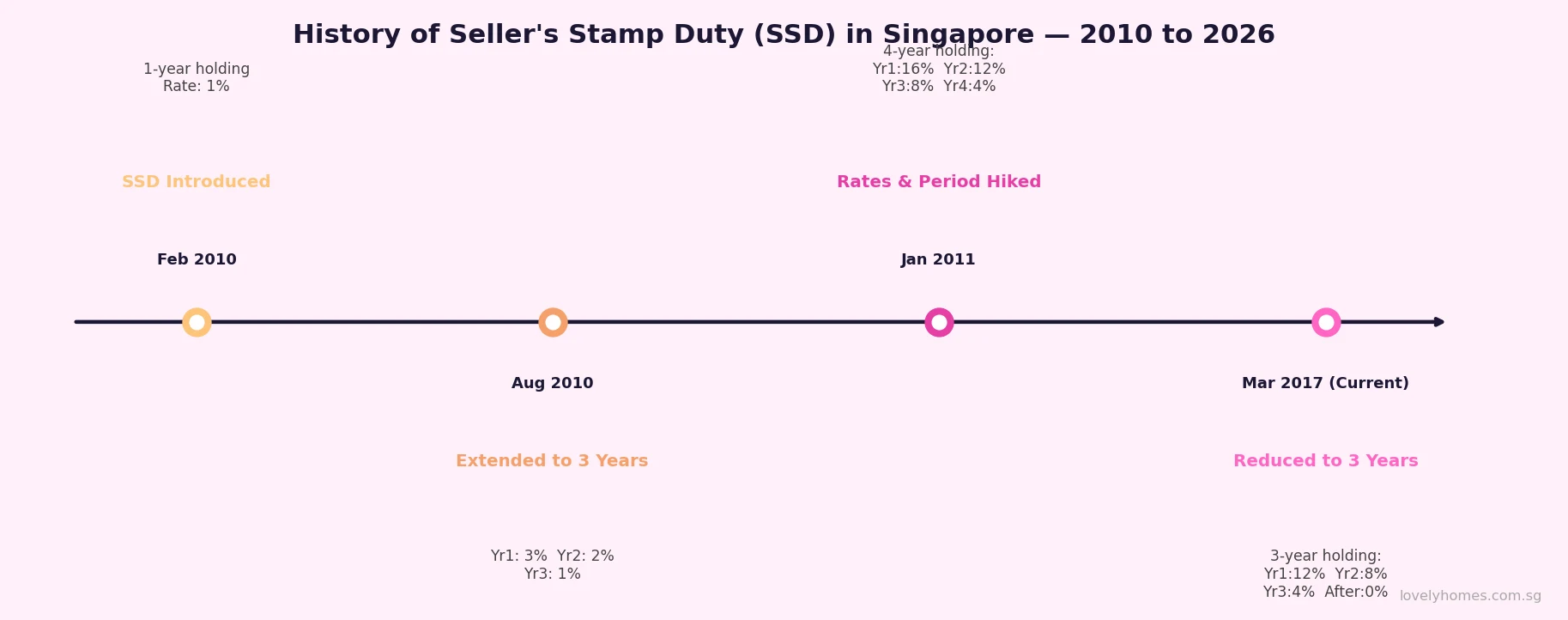

SSD and the Different Holding Period Regimes

The holding period and rates under SSD have changed three times since its introduction. The applicable regime depends on when you purchased the property, not when you sell it:

Acquired 14 January 2011–10 March 2017: 4-year holding period; rates 16% / 12% / 8% / 4%.

Acquired 30 August 2010–13 January 2011: 3-year holding period; lower rates 3% / 2% / 1%.

Acquired 20 February–29 August 2010: 1-year holding period; rate 1%.

Acquired before 20 February 2010: SSD did not exist; no SSD payable.

Figure 3: Timeline of SSD regime changes in Singapore, February 2010 to present. Source: IRAS / Ministry of Finance.

What Transactions Attract SSD?

SSD is triggered on the disposal of a residential property within the applicable holding period. This includes:

Open-market resale of a private condo, landed house, or HDB resale flat.

Transfer of a property by way of sale (including between related parties at market value).

A gift of property — where IRAS deems a market value applies, SSD may be chargeable on the transferor.

Assignment of an OTP or S&P agreement where the sub-purchaser takes over before the property is transferred.

SSD is not triggered by:

Transfer of a residential property by way of inheritance or pursuant to a court order (e.g. in divorce proceedings) — though legal advice should be taken on the specifics.

Compulsory acquisition of land by the Government under the Land Acquisition Act.

Transfer between spouses pursuant to a divorce court order (subject to conditions).

Can SSD Be Avoided or Remitted?

Unlike ABSD — which has several remission schemes for qualifying buyers — there is no standard remission scheme for SSD. Once SSD is triggered, it is generally payable in full. The only legitimate ways to avoid SSD are:

Hold for the full SSD period. The most reliable approach: simply do not sell within 3 years of purchase. Time your decision to sell around the anniversary of your OTP exercise date.

Rely on a recognised exemption. Government compulsory acquisitions and specific court-ordered transfers may not attract SSD — take specialist legal advice.

Negotiate for the buyer to absorb it. In strong markets, some sellers negotiate for the buyer to pay a higher price that effectively covers the SSD. This is a commercial negotiation rather than a legal remission.

Attempting to circumvent SSD through artificial schemes — such as inserting a related party as an intermediate buyer — is a criminal offence under the Stamp Duties Act. IRAS has the power to set aside transactions that it determines were structured to avoid stamp duty.

Selling Before the SSD Period: What to Consider

Occasionally, life events force a sale within the SSD window: a job relocation, financial hardship, divorce, or death. In such cases, SSD is generally unavoidable, but sellers should take steps to maximise their net proceeds:

Engage a conveyancing lawyer to confirm which SSD regime applies and calculate the exact sum due.

Factor SSD into your reserve price — selling for anything less than the minimum price required to cover SSD, mortgage redemption, and CPF refund (with accrued interest) will result in a cash shortfall.

If you are also buying a replacement property, account for the full chain of stamp duty costs: you may owe SSD on the sale and ABSD on the purchase.

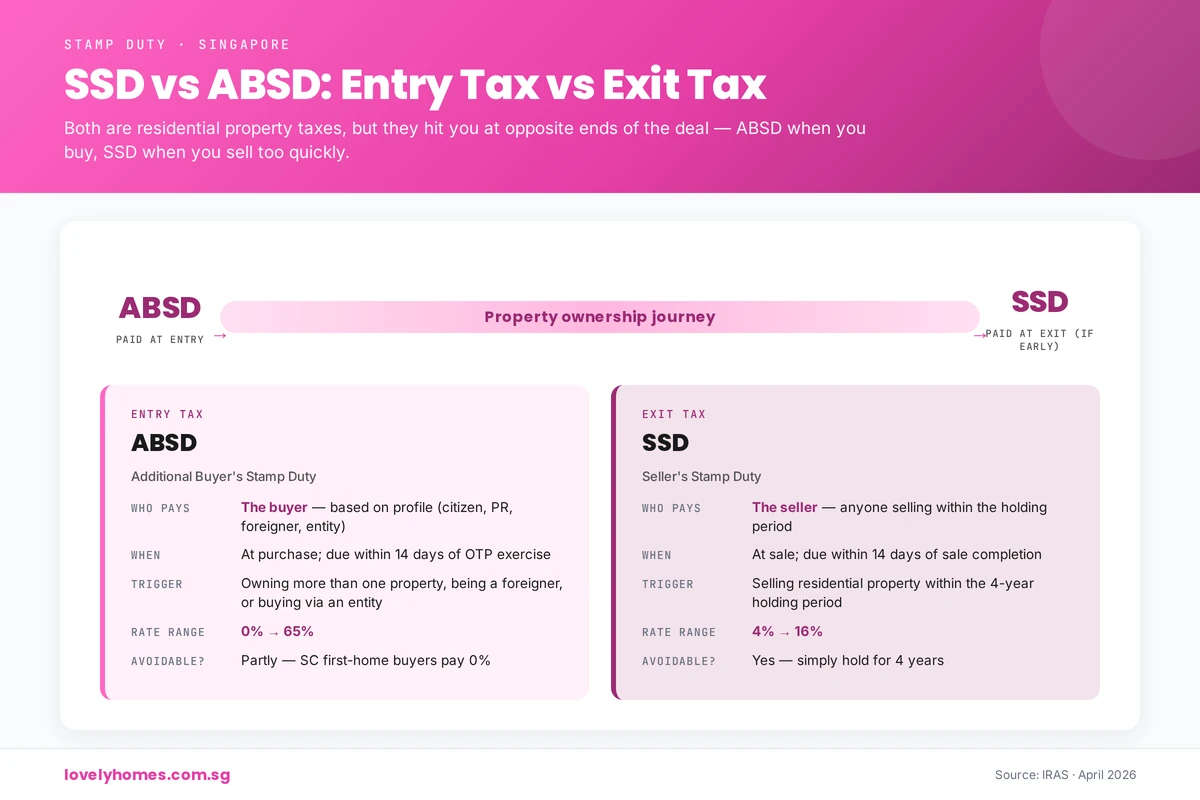

SSD vs ABSD — What Is the Difference?

Feature

SSD (Seller’s Stamp Duty)

ABSD (Additional Buyer’s Stamp Duty)

Who pays?

The seller

The buyer

When triggered?

Selling within the SSD holding period

Buying a 2nd+ residential property (or any property as foreigner/entity)

Applies equally regardless of citizenship?

Yes

No — rates vary by citizenship & property count

Current rates

12% / 8% / 4% (years 1–3)

0%–65% depending on buyer profile

Remission available?

Very limited

Yes — married couple, developer, FTA nationals

Primary purpose

Deter short-term speculation / flipping

Moderate demand from investors and foreigners

What Might Come Next for SSD?

SSD was last adjusted in March 2017, when the Government reduced the holding period from 4 years to 3 years and lowered rates, signalling greater confidence in market stability. As of May 2026, there has been no indication from the Ministry of Finance or MAS of any imminent change to the SSD framework. That said, Singapore’s cooling-measures framework has historically been responsive to price pressures — if private residential prices were to accelerate meaningfully, a tightening of SSD (or other measures) cannot be ruled out. For up-to-date guidance, monitor IRAS and the Ministry of Finance.

Frequently Asked Questions

Is SSD payable on the sale price or the market value?

SSD is calculated on the higher of the actual sale price or the market value of the property at the time of sale, as determined by IRAS. If you sell a property at a price below its market value — for example, in a family transfer — IRAS will use the market value for the SSD calculation. This prevents sellers from artificially suppressing prices to reduce their SSD bill.

Does SSD apply to commercial or industrial property?

No. SSD applies only to residential properties — private condominiums, landed houses, HDB resale flats, and executive condominiums. Commercial shophouses, office units, industrial buildings, and pure-land plots are not subject to SSD. This is one reason some investors prefer commercial or industrial assets for shorter-term investment horizons.

When must SSD be paid after signing the sale contract?

SSD must be paid within 14 days of the date of the document that triggers the duty — typically the sale contract or the transfer document. Your conveyancing lawyer will stamp the document and collect the SSD as part of the closing process. Late payment attracts penalties and interest under the Stamp Duties Act.

I inherited a property less than 3 years ago. Do I pay SSD if I sell it?

A property acquired by way of inheritance is not a purchase — it is a transmission on death. IRAS’ position is that where a property is acquired through inheritance, the SSD holding period does not apply in the same way as a purchase. However, if the estate purchased the property (rather than having long held it), the executor’s position can be complex. You should seek specific advice from a conveyancing solicitor familiar with stamp-duty rules before proceeding with any sale of an inherited property.

Can I use CPF to pay SSD?

No. Stamp duties — including SSD and ABSD — cannot be paid directly from your CPF Ordinary Account. They must be settled in cash. Before committing to a sale within the SSD window, ensure you have sufficient liquid funds to cover the SSD liability on top of all other closing costs (agent commission, legal fees, mortgage redemption penalty if any).

My property was purchased jointly with my spouse. How does SSD apply?

For jointly owned property, SSD is assessed on the entire transaction — not split between owners. Both joint tenants or tenants-in-common are jointly and severally liable for the SSD. The holding period is measured from when the property was originally acquired. If you are selling a jointly owned property and the holding period has not expired, both parties must factor in the full SSD liability when planning the sale.

Does SSD apply to the sale of a new launch (uncompleted) condo?

Yes, but the holding period starts from the date of the Sale & Purchase Agreement (the date you signed the S&P with the developer), not the TOP date. This means that if you bought an uncompleted project in 2024 and it TOPs in 2027, you may already be past the SSD window by the time you are able to sell. However, some buyers who assigned or sub-sold their S&P agreements before completion have historically triggered SSD on the assignment — IRAS treats such assignments as a disposal.

This article is for general informational purposes only and does not constitute legal, tax, or financial advice. SSD rates and rules are set by the Inland Revenue Authority of Singapore (IRAS) and are subject to change. The worked examples and figures in this article are illustrative only and do not constitute a valuation or legal opinion. Before entering into any property transaction — particularly one that may attract SSD — you should consult a licensed conveyancing solicitor, a certified financial planner, and verify the current position directly with IRAS.

Seller’s Stamp Duty (SSD) is the Singapore Government’s anti-flipping tax. If you sell a residential property within three years of buying it, you pay a percentage of the sale price — up to 12% — on top of every other selling cost. Get the holding period wrong by even a single day, and a profitable sale can flip into a six-figure loss.

This guide walks you through SSD in 2026: who pays it, how the rate ladder works, when the holding clock starts and stops, who is exempt, and the strategies sellers actually use to manage it. All rates reflect the framework in force since 11 March 2017, which remains current. For the authoritative figures, always check the IRAS Seller’s Stamp Duty page.

Quick Answer — SSD at a glance

SSD applies only to residential property sold within 3 years of acquisition.

The clock starts on the date you signed the OTP or accepted the S&P — not the day you collected the keys.

Payable within 14 days of contract for sale, on the higher of price or market value.

Most short-term sales are caught: divorce sales, job relocations, second properties — SSD applies to nearly all of them.

Industrial property has a separate (shorter) ladder; commercial property is exempt.

What Is SSD and Why Does It Exist?

SSD is a transaction tax levied on the seller of a residential property in Singapore when the property is sold within a defined holding period. It is administered by the Inland Revenue Authority of Singapore (IRAS), calculated on the higher of the sale price or the market value, and payable within 14 days of the contract for sale.

The tax was first introduced in February 2010 and progressively widened in 2011 and 2013 as part of the Government’s suite of property cooling measures. The most recent recalibration was in March 2017, which shortened the SSD holding period from four years to three and lowered the headline rate from 16% to the present 12% — a deliberate easing aimed at supporting genuine homeowners rather than speculators. The 2017 framework is still the live rule book in 2026.

The policy goal is simple: discourage speculative flipping while leaving genuine end-users untouched. By the time you have held a private condo or HDB flat for three full years, the cooling-measure case for taxing your sale is gone, and SSD falls to zero.

Seller’s Stamp Duty Singapore 2026 — the cost of selling too soon.

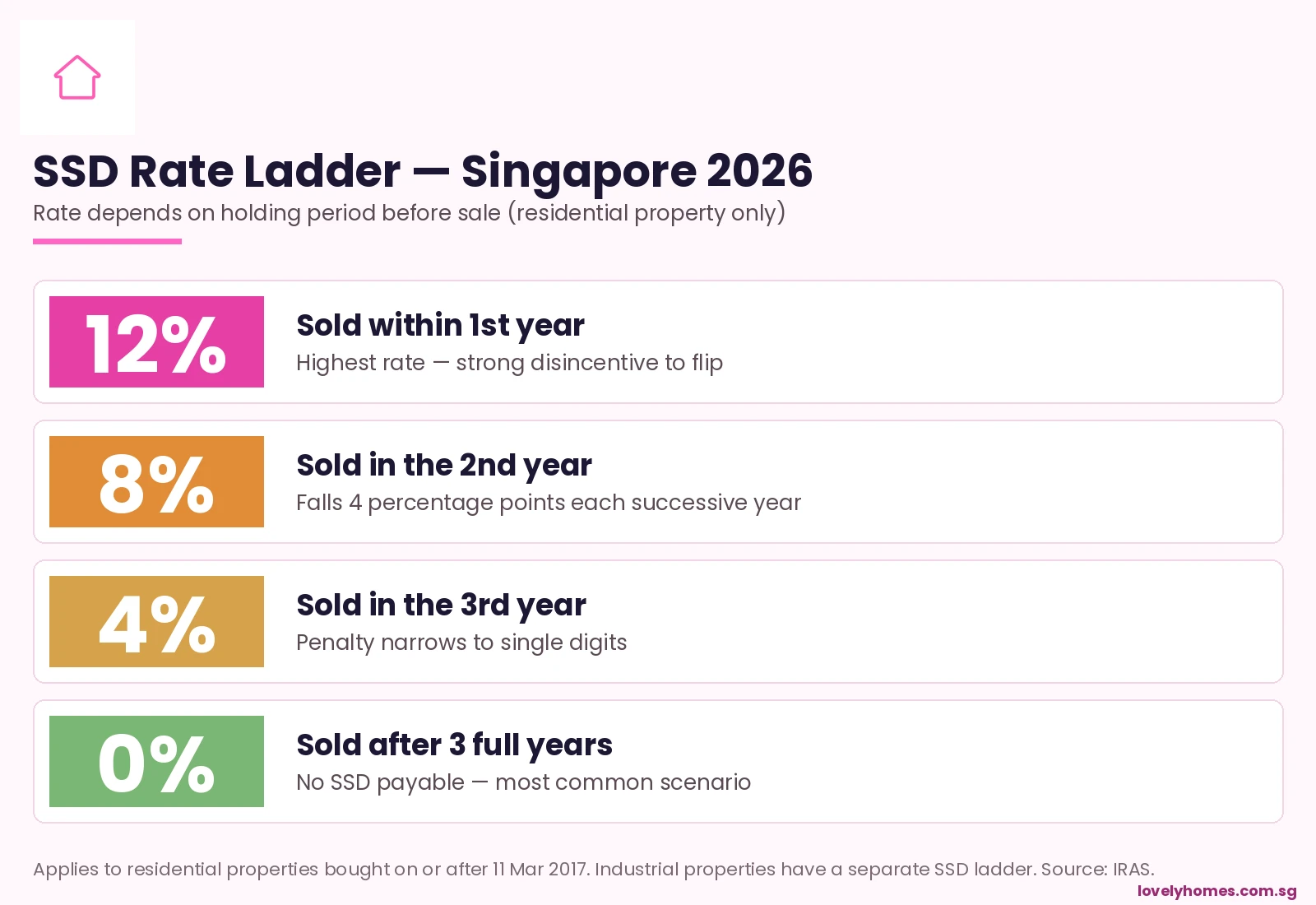

The 2026 SSD Rate Ladder

The rate you pay depends entirely on how long you held the property before signing the contract for sale. The ladder is steep at the top and falls four percentage points each subsequent year:

Figure 1: SSD rate ladder by holding period — residential property, 2026.

Holding period at sale

SSD rate

Apparent on a S$1.5M sale

Up to 1 year (within 1st year)

12%

S$180,000

More than 1 to 2 years

8%

S$120,000

More than 2 to 3 years

4%

S$60,000

More than 3 years

0%

Nil

The rate is applied to the higher of the contracted sale price or IRAS’s assessed market value — sellers cannot lower their SSD bill by deliberately under-pricing a transaction.

When Does the Holding Clock Start — and Stop?

This is where most disputes arise, because the holding period is calculated to the day. The general rule is:

Start: the date the buyer signs the Option to Purchase (OTP) or, if there is no OTP, the date of the Sale & Purchase Agreement (S&P).

End: the date the buyer signs the next OTP or S&P when reselling.

Note carefully — the keys handover (TOP for new condos, vacant possession for resale) is irrelevant to SSD. A buyer who signs an OTP on 1 March 2024 and signs the next OTP on 28 February 2027 has held for one day under three years — SSD at 4% applies. Sign on 2 March 2027 and SSD drops to zero. Conveyancers routinely time exercise dates around this calendar boundary.

For new launches under construction, the start date is the OTP exercise date, not the TOP date. This means a buyer who signed an OTP in early 2023 for a project that only TOP’d in 2026 is already past the SSD window when they collect the keys.

Who Is Exempt or Remitted?

The exemptions list is narrow. SSD remission is granted only in specific situations, including:

HDB flats — not subject to SSD because HDB has its own Minimum Occupation Period (MOP) regime, which generally bars resale within five years.

Compulsory acquisition by the State (for example, road or MRT line widening).

Bankruptcy of the owner, with proof of insolvency proceedings.

Owners required by HDB to sell on grounds of policy violation.

Inherited property — the holding period is reckoned from the original purchase by the deceased, not the date of inheritance.

Property transferred between spouses as part of a court-ordered division on divorce, in some cases.

Standard life events — relocation overseas for work, family expansion, or financial difficulty — are not grounds for SSD remission. The tax applies even if the seller is selling at a loss.

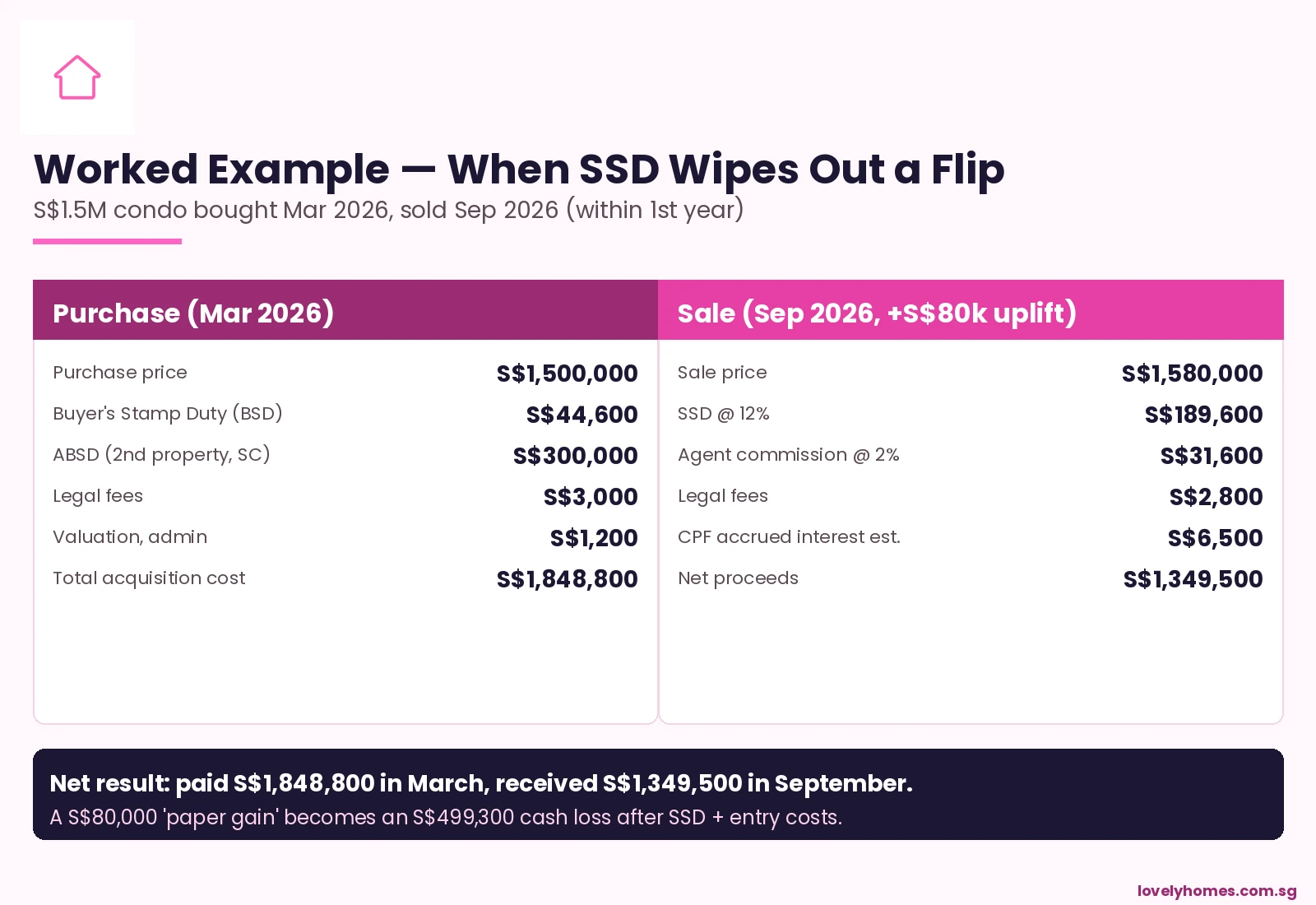

Worked Example — A S$1.5M Condo Flipped in 6 Months

Imagine a Singapore Citizen who buys a S$1.5M private condo as a second property in March 2026, then receives a job offer in Hong Kong six months later and decides to sell at S$1.58M (a S$80,000 paper gain). Here is what the maths actually looks like:

Figure 2: Worked example — an apparent S$80k gain becomes an S$499k cash loss when SSD is applied.

Acquisition costs (BSD, ABSD on the second property at 20%, legal fees) total S$348,800. The owner has paid S$1,848,800 to take possession. Six months later, the sale at S$1,580,000 attracts SSD at 12% (S$189,600), broker commission, legal fees, and CPF accrued interest. Net proceeds: S$1,349,500. Cash loss: S$499,300.

The lesson is brutal: SSD is designed to make short-term residential property sales economically unattractive even when the underlying market has moved up. For most second-property buyers, the only way to make the maths work is to stay invested for at least three years.

Strategies Sellers Actually Use

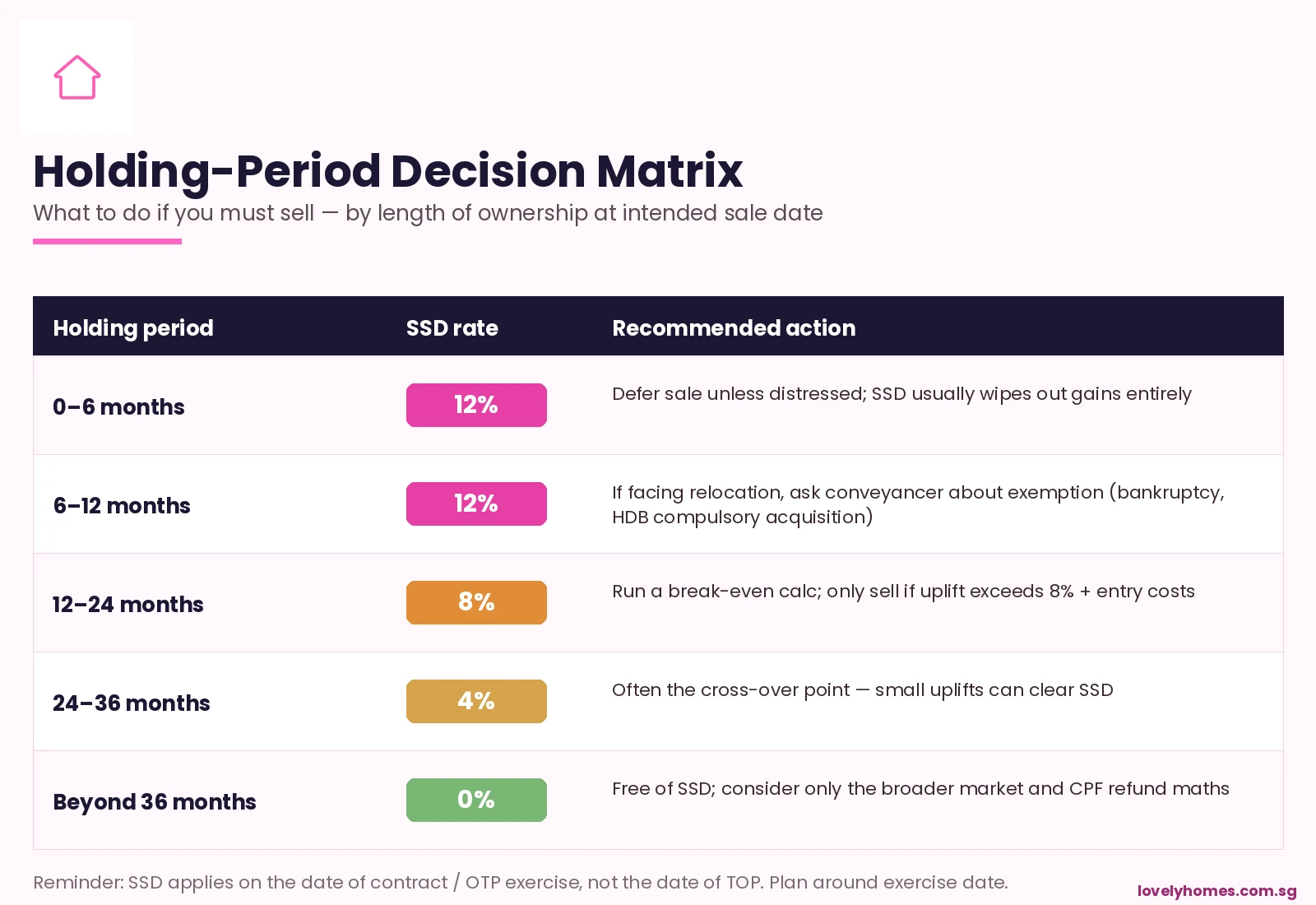

If you find yourself needing to sell within the SSD window, there are a small number of strategies practitioners commonly consider:

1. Run the holding-period calendar to the day

Conveyancers often time the OTP issue and exercise so that the sale falls just outside the next rate band. Selling on day 365 versus day 367 of the second year can mean a four-percentage-point swing on the sale price.

Figure 3: Decision matrix — what to do if you must sell, by length of ownership.

2. Rent out instead of selling

If holding-period maths do not work, leasing the unit until SSD falls to zero can preserve value. Singapore rental yields on private condos run 3.0–3.8% gross in 2026, which often covers the carrying cost of the mortgage during the wait.

3. Decoupling within marriage

Where one spouse needs to free up ABSD allowance for a future purchase, transferring a property between spouses (a Part-Disposal arrangement) may attract SSD on the transferred share. Practitioners check carefully whether the holding clock survives the transfer.

4. Swap residential for commercial

Commercial property (offices, shops) is not subject to SSD. Investors with a short horizon sometimes pivot from residential plays to commercial plays specifically to avoid the SSD window. Commercial does carry GST, however, so the trade-off is real.

SSD on HDB — Yes, Technically — But MOP Comes First

Strictly, SSD does not apply to HDB flats sold during the SSD window because the HDB Minimum Occupation Period (MOP) usually prevents resale within five years anyway. The rare exceptions — flats sold under HDB’s compulsory-sale rules, or flats where MOP has been waived by HDB — are also exempt from SSD.

For practical purposes, most HDB sellers should treat MOP as the binding constraint and ignore SSD entirely.

SSD on Industrial Property — A Different (Shorter) Ladder

SSD on industrial property uses a separate, shorter ladder introduced in January 2013: 15% within the first year, 10% in the second year, 5% in the third year, and 0% thereafter — harsher in headline terms but with the same three-year horizon. Commercial property (offices, shops, hotels) attracts no SSD at all.

What This Means for You as a Buyer in 2026

The 2026 environment makes the holding-period calculus even more important. With ABSD at 20% on the second property for Singapore Citizens and 60% for foreigners, entry costs are already punishing. Adding a 12% SSD on a quick exit means roughly one-third of an investment property’s purchase price is consumed by transaction taxes if the holding period is mismanaged.

For buyer-occupiers, the practical advice is unchanged: buy what you can hold through three full years and a typical Singapore property cycle (roughly 7 to 10 years). For investors, the calculus is whether the projected three-to-five-year capital appreciation comfortably exceeds the entry-cost stack — not just SSD but BSD, ABSD, conveyancing, agent commission, and CPF accrued interest combined.

Frequently Asked Questions

Does SSD apply if I bought before 11 March 2017?

Yes, but at the older rate ladder applicable on the date of acquisition. Properties bought between 14 January 2011 and 10 March 2017 use the four-year, 16% / 12% / 8% / 4% ladder. Properties bought between 20 February 2010 and 13 January 2011 use a three-year, 3% / 2% / 1% ladder. IRAS publishes the historical rate tables for cross-reference.

Is SSD payable on the sale of a property at a loss?

Yes. SSD is calculated on the higher of the contracted sale price or the assessed market value, regardless of whether the seller realised a profit or loss on the transaction. Loss-making short-term sales remain fully taxable.

How is SSD different from ABSD?

ABSD (Additional Buyer’s Stamp Duty) is paid by the buyer at purchase based on residency status and number of properties already owned. SSD (Seller’s Stamp Duty) is paid by the seller at sale based on how long the property was held. They are independent taxes and can both apply to the same transaction at different ends.

What if I co-own a property with my spouse and only my spouse’s share is sold (decoupling)?

SSD applies to the share being transferred, calculated on the value of that share. The holding period for the transferred share is reckoned from the original date of acquisition. Conveyancers will typically structure the transfer documentation so that SSD exposure is calculated correctly for the share at issue.

Can I deduct SSD against my income tax?

No. SSD is a transaction tax, not a deductible business expense for an individual seller. Property held by a corporate vehicle may treat SSD differently — consult a Singapore tax adviser for any company-held holding.

Does SSD apply to gifts or transfers within the family?

Generally yes, where the transfer is treated as a sale at market value. There are limited remissions for transfers between spouses incident to divorce or for inherited property where the holding period is reckoned from the deceased’s original acquisition. Always verify with IRAS directly for non-arm’s-length transfers.

When exactly is SSD due?

SSD must be paid within 14 days of the contract for sale — that is, the date the buyer exercises the OTP or signs the S&P. Late payment attracts penalty interest of 5% on the unpaid duty per annum, plus possible additional charges. The seller’s conveyancer typically pays SSD out of the sale proceeds at completion.

This article is intended as general information about Seller’s Stamp Duty in Singapore as at May 2026 and does not constitute tax, legal, or financial advice. Rates, exemptions, and procedures are set by the Inland Revenue Authority of Singapore and may be amended at any time without notice. For authoritative figures, refer to IRAS, the Housing & Development Board, the Monetary Authority of Singapore, the Urban Redevelopment Authority, and CPF Board for related procedures. For transactions of any size, engage a licensed Singapore conveyancing solicitor and, if relevant, a chartered accountant or tax practitioner before signing an OTP or S&P.

Wait-Out Period: Private property owners must wait 15 months before buying HDB resale without grant.

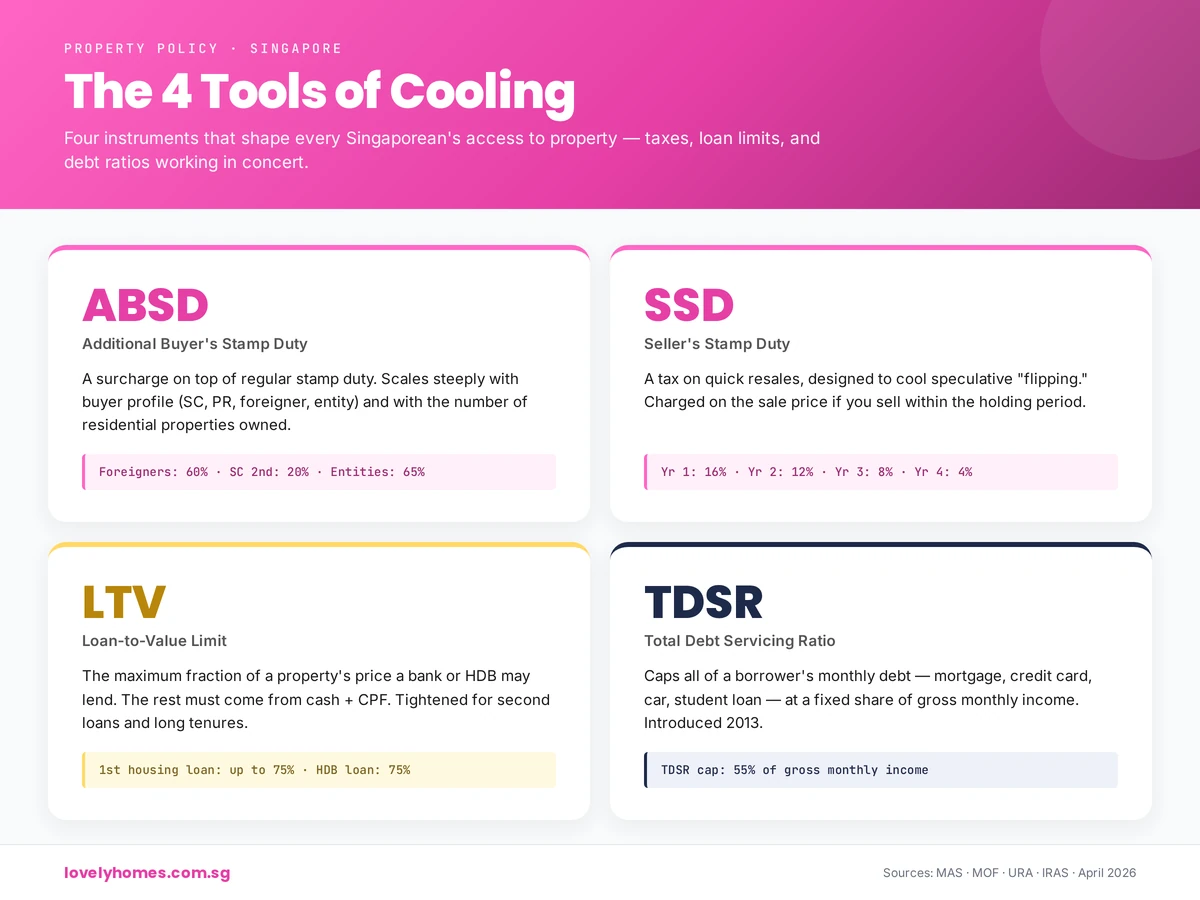

What are Singapore’s Property Cooling Measures?

Singapore’s property cooling measures are a suite of policy tools designed to moderate demand, curb speculation, and ensure housing remains affordable. They exist because rapid property price growth can outpace wage growth, lock first-time buyers out of the market, and create unsustainable bubbles. Four key agencies administer these measures: the Monetary Authority of Singapore (MAS), the Urban Redevelopment Authority (URA), the Inland Revenue Authority of Singapore (IRAS), and the Housing and Development Board (HDB). Together, they apply tools such as stamp duties, loan limits, affordability tests, and holding periods to regulate the market and protect both buyers and the broader economy.

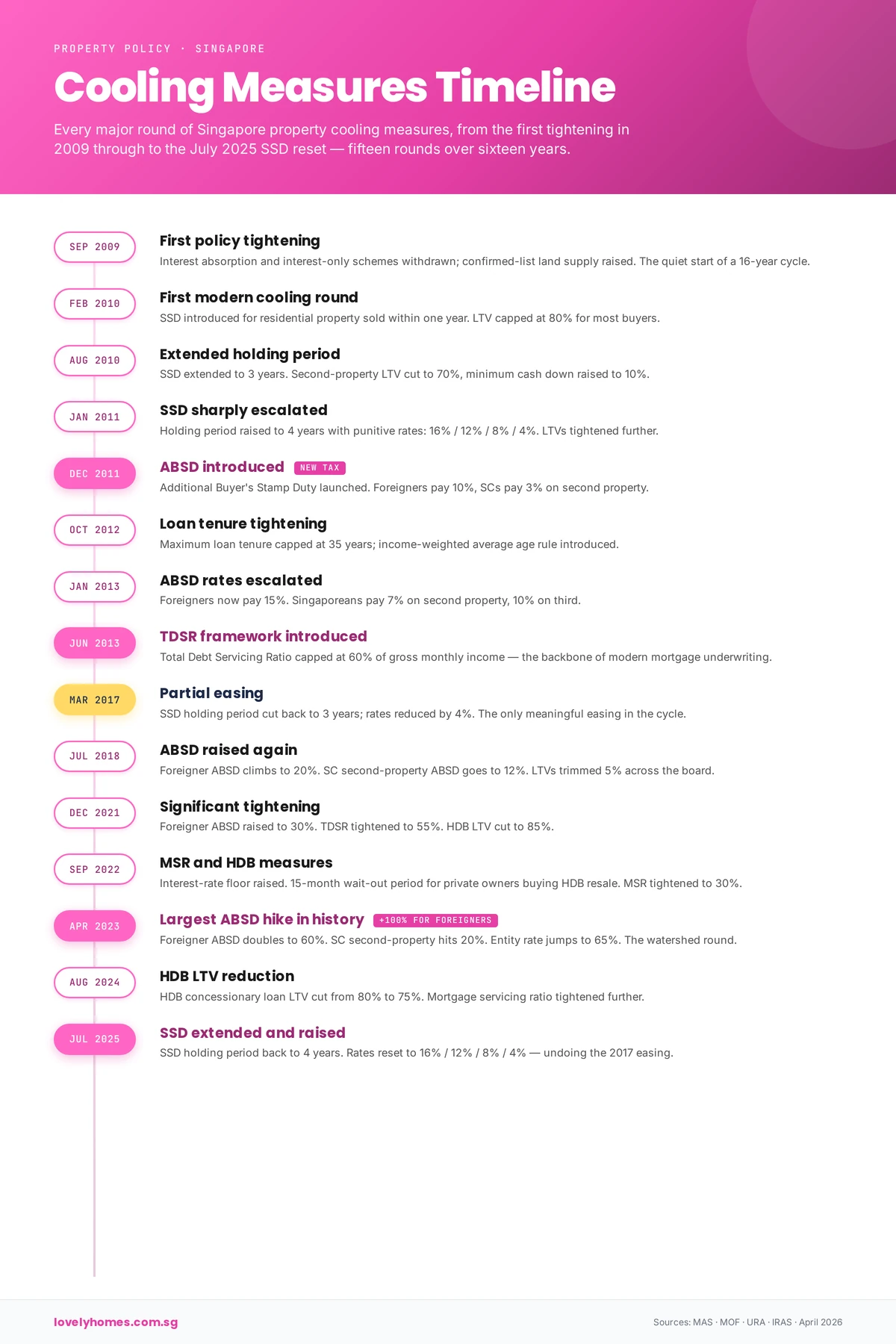

Figure 1: The 15 major rounds of Singapore property cooling measures, 2009–2026.

September 2009: The First Policy Tightening

Before the modern cooling era, the government moved to restrict lending practices. In September 2009, the Monetary Authority of Singapore (MAS) disallowed two risky loan products: the Interest Absorption Scheme (IAS) and Interest-Only Housing Loans (IOL). These products had allowed borrowers to defer principal repayment during the early years of a mortgage, increasing default risk during rate rises. By banning them, the government signalled a preference for prudent, full-amortising loans and set the stage for the more comprehensive cooling measures that would follow.

February 2010: The First Modern Cooling Round

On 20 February 2010, Singapore introduced its first comprehensive cooling package, reflecting rapid price growth and surging demand. The government introduced two major tools:

Seller’s Stamp Duty (SSD): Properties sold within one year were hit with a 3% SSD. The intent was to discourage “flipping”—rapid resale for short-term gain.

Loan-to-Value (LTV) limit: Reduced from 90% to 80%, requiring buyers to put down at least 20%. This reduced lender exposure and made buyers more cautious.

These measures reflected a key insight: when buyers can leverage heavily and exit quickly, prices can spiral. By raising the entry cost and the holding cost, the government aimed to attract only genuine buyers.

August 2010: Extended Holding Period

By mid-2010, demand remained strong. On 19 August 2010, the government extended the SSD holding period from 1 year to 3 years, raising the cost of short-term resale. For those with existing loans, the LTV limit tightened further to 70%, and cash downpayment requirements rose, particularly hurting leveraged investors.

January 2011: Sharp SSD Escalation

Recognising that the market was still overheating, the government on 8 January 2011 escalated the SSD significantly. The new structure was:

Year 1: 16%

Year 2: 12%

Year 3: 8%

Year 4: 4%

The rationale was unmistakable: hold for less than a year and lose a sixth of your sale price. LTV limits were also tightened to 60% for those with existing loans, making it much harder for property investors to string together multiple mortgages.

December 2011: ABSD Introduced

On 8 December 2011, Singapore introduced the Additional Buyer’s Stamp Duty (ABSD), its most powerful tool. ABSD was a second layer of stamp duty on top of the normal Buyer’s Stamp Duty (BSD), calibrated to buyer type:

Singapore Citizens buying a 2nd+ property: 3%

Singapore Citizens buying a 3rd+ property: 3%

Permanent Residents buying a 2nd+ property: 3%

Foreigners: 10%

Corporate entities: 10%

ABSD was revolutionary because it directly attacked investment demand, particularly from overseas. It signalled that Singapore prioritised homeownership for citizens over investment returns for outsiders.

October 2012: Loan Tenure Tightening

The Monetary Authority of Singapore further tightened lending on 19 October 2012. The maximum loan tenure was capped at 35 years, with a penalty: if LTV remained above 60% after 30 years, the LTV would be capped at 40% in year 31 onwards. This forced borrowers to repay principal faster, reducing their borrowing power and making loans less attractive.

January 2013: ABSD Escalation

On 11 January 2013, the government raised ABSD across the board:

Singapore Citizens (2nd property): 7%

Singapore Citizens (3rd+ property): 10%

Permanent Residents (2nd+ property): 10%

Foreigners: 15%

Entities: 15%

The hike reflected continued demand, particularly from foreign investors and corporate buyers. Cash downpayment requirements also rose, targeting multiple-property owners and entities.

June 2013: TDSR Framework Introduced

On 28 June 2013, the Monetary Authority of Singapore introduced the Total Debt Servicing Ratio (TDSR) framework. TDSR capped total monthly debt repayments (mortgage, car loan, credit cards, personal loans, etc.) at 60% of gross monthly income. The intention was to prevent over-leverage: even if house prices were rising, a banker couldn’t lend to someone whose entire income was going to debt service.

This was a game-changer because it wasn’t about house prices directly—it was about borrower health. It also forced banks to stress-test loans, assuming interest rates would rise, to ensure borrowers could survive a shock.

March 2017: Partial Easing

By 2016–2017, prices had stabilised and growth had slowed. On 5 March 2017, the government eased some measures:

SSD holding period reduced from 4 years to 3 years, though rates remained steep (12%/8%/4% for years 1–3).

TDSR and ABSD eased slightly for refinancing.

This signalled a shift: the government was confident the market was no longer overheating and could afford marginal relief.

July 2018: ABSD Raised Again

By mid-2018, there were signs of renewed speculative interest, particularly from foreign and corporate buyers. On 6 July 2018, the government raised ABSD sharply:

LTV limits also tightened by 5 percentage points across all categories, making down payments larger and borrowing power lower.

December 2021: Significant Tightening

After years of near-zero interest rates post-COVID, demand surged again. On 16 December 2021, the government announced a comprehensive tightening:

ABSD raised again: foreigners to 30%; entities to 35%; PR 2nd property to 20%.

TDSR tightened from 60% to 55% of gross monthly income.

Interest-rate floor for TDSR/MSR calculations raised to 3.5% for private bank loans (previously 3%).

HDB LTV limits reduced across the board.

This was a significant hardening, reflecting real concern about affordability following three years of price growth.

September 2022: MSR and HDB Measures

On 30 September 2022, the government introduced new measures targeting the HDB resale market, where first-time buyers (and upgraders) primarily shop:

Mortgage Servicing Ratio (MSR) introduced: For HDB and Executive Condominium (EC) loans, monthly mortgage payments cannot exceed 30% of gross income—stricter than TDSR’s 55%.

15-month wait-out period: Private property owners must wait 15 months after selling before buying an HDB resale flat, curbing investor demand for subsidised public housing.

Interest-rate floor for TDSR/MSR raised from 3% to 3.5% for private loans; 3% for HDB loans.

These moves directly sheltered first-time HDB buyers from investor competition.

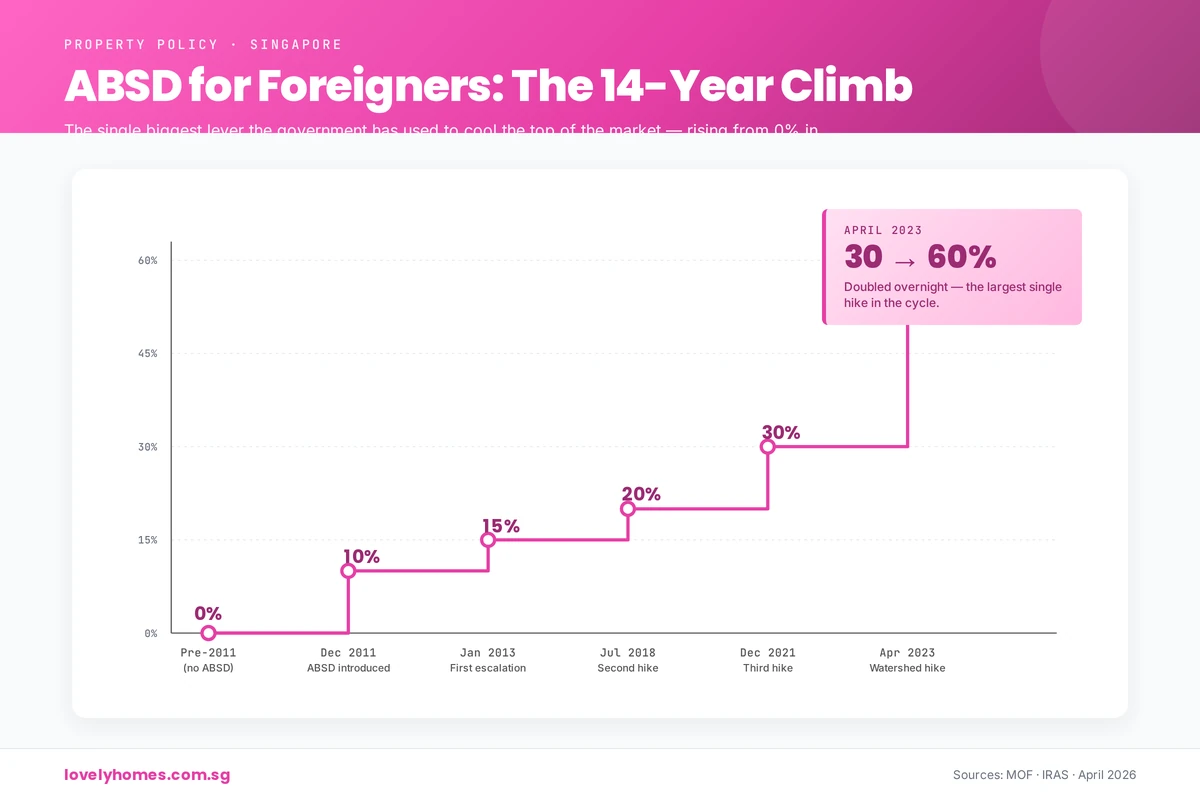

Figure 3: Foreigner ABSD climbed from 0% in 2011 to 60% in April 2023 — the largest single hike in the cycle.

April 2023: Largest ABSD Hike in History

On 27 April 2023, faced with renewed price acceleration in Q1 2023 (especially among owner-occupiers), the government announced its largest ABSD increase:

This was the most aggressive escalation since ABSD’s introduction, reflecting the government’s determination to prioritise homeownership for citizens and slow speculation. A foreign buyer purchasing a S$2 million condo now faced S$1.2 million in ABSD—an enormous barrier.

August 2024: HDB LTV Reduction

On 20 August 2024, the government reduced the Loan-to-Value (LTV) limit for HDB-granted housing loans from 80% to 75%. This meant HDB buyers now needed a 25% down payment instead of 20%, directly reducing borrowing power for this segment. Concurrently, higher CPF Housing Grants were introduced for first-time buyers to offset the impact, retaining affordability.

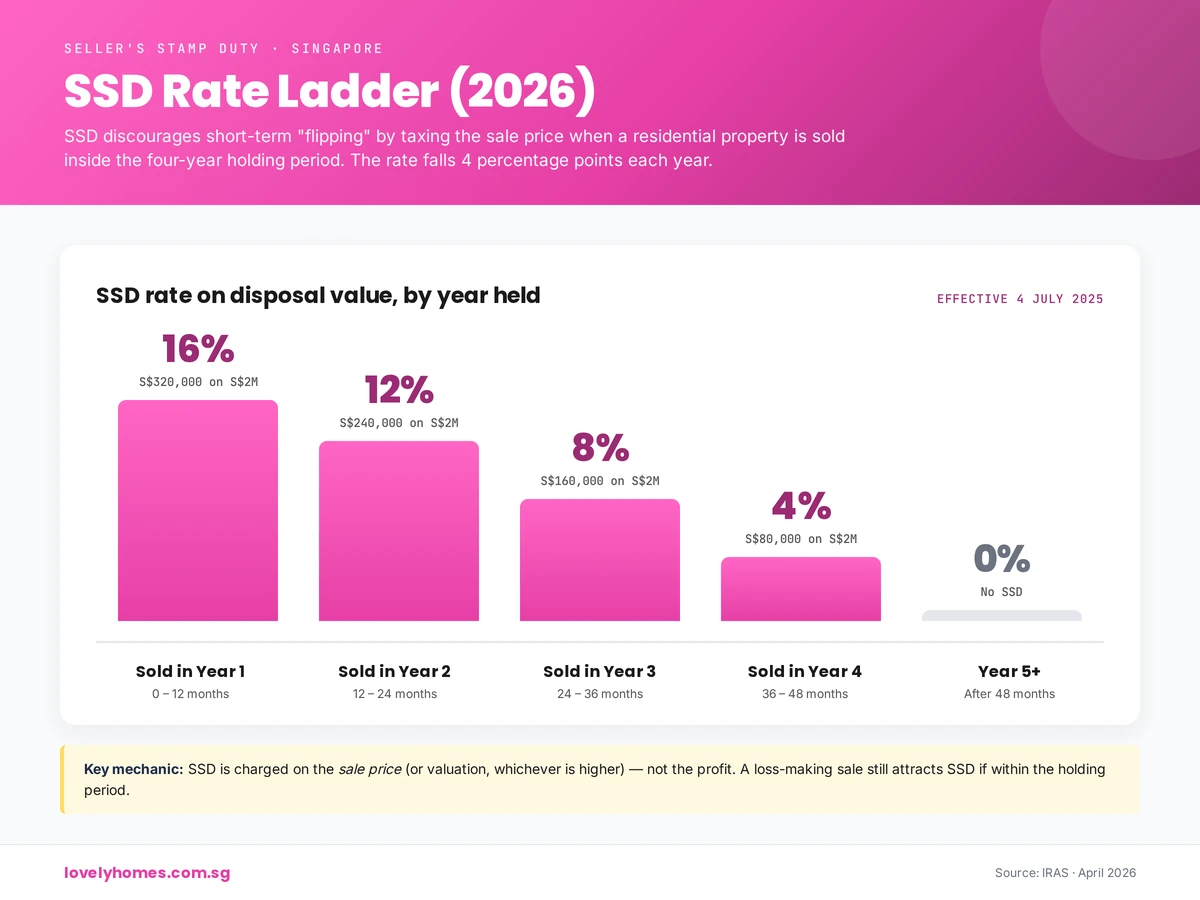

July 2025: SSD Extended and Raised

On 3 July 2025, the government responded to a spike in “flipping”—buyers purchasing uncompleted units (off-plan) and reselling before completion or soon after. The SSD holding period was extended from 3 years to 4 years, and rates were raised across the board by 4 percentage points:

Year 1: 20% (from 16%)

Year 2: 16% (from 12%)

Year 3: 12% (from 8%)

Year 4: 8% (from 4%)

This further discouraged short-term speculation while allowing long-term owners to exit penalty-free after four years.

Current Cooling Measures Framework (April 2026)

The current cooling-measures framework, established by the 27 April 2023 ABSD hike and subsequently adjusted by the 20 August 2024 HDB LTV reduction and the 4 July 2025 SSD restructure, remains in force as at April 2026. MAS, MND, URA and HDB jointly review the framework regularly and have repeatedly indicated they will recalibrate the measures — either tightening or easing — in response to market conditions.

Figure 2: The four core cooling tools — taxes (ABSD, SSD), loan limits (LTV) and debt ratios (TDSR) working in concert.

Let’s illustrate the impact with a hypothetical Singapore Citizen (SC) buying a second property valued at S$2 million:

Year

ABSD Rate

ABSD Cost (S$)

BSD + ABSD Total

2010 (Feb)

0%

S$0

~S$20,000 (BSD only)

2013 (Jan)

7%

S$140,000

~S$160,000

2018 (July)

7%

S$140,000

~S$160,000

2023 (April)

20%

S$400,000

~S$420,000

2026 (April)

20%

S$400,000

~S$420,000

Notice the leap from 2013 to 2023: the cost of buying a second home more than doubled in stamp duty alone, while the property value remained constant. This is the direct impact of cooling measures: they make property ownership more expensive, not by changing the property itself, but by raising friction and entry costs.

Why Have Cooling Measures Worked?

Singapore’s housing market has not crashed, despite aggressive cooling measures—a fact some cite as evidence of failure. But that misses the point. Cooling measures are designed to slow, not stop, price growth; to reduce speculation, not eliminate it; and to align prices with incomes, not freeze them.

Consider the evidence:

Slower growth: Private residential property annual price gains have typically stayed in the 2–5% range post-2013, compared to double-digit growth in the early 2010s. This moderation reflects a market rebalancing, where price appreciation has settled into a more sustainable trajectory aligned with economic fundamentals such as wage growth and rental yields.

Affordability preserved: First-time buyers, particularly HDB upgraders, have continued to buy; median house prices have not become so extreme relative to median incomes that the market has fractured. The price-to-income ratio in Singapore remains among the most manageable in developed Asia, allowing younger buyers to enter the market without undue hardship.

Comparison to global peers: Hong Kong, Vancouver, and Sydney have seen much steeper price-to-income ratios despite less stringent cooling measures. In Hong Kong, for example, a property may cost 20–30 times annual median household income; in Vancouver and Sydney, the ratio exceeds 12–15. Singapore’s pragmatic approach has kept the ratio at a more sustainable 8–10 times, making the market more accessible.

Investor activity moderated: The share of property transactions by investors (vs. owner-occupiers) has declined, indicating cooling measures are successfully crowding out speculative demand. This shift is crucial: when investors withdraw, price volatility typically decreases and stability improves.

Market resilience: The market has absorbed multiple rounds of tightening—seven major cooling packages since 2009—without experiencing a crash. This speaks to the underlying strength of Singapore’s economy and the government’s ability to calibrate policy precisely, neither so tight as to stifle the market nor so loose as to permit excess.

In short, cooling measures have succeeded in their core mission: managed, sustainable growth that preserves homeownership as an achievable goal for Singaporeans whilst safeguarding financial stability.

What Might Come Next?

Predicting future cooling measures is speculative, but several potential levers exist if the market overheats again. The government has shown it is willing to adjust policy swiftly when conditions warrant, and the following measures are within the realm of possibility:

Further LTV tightening: LTV could drop below 75% for HDB and 70% for private, forcing larger down payments. This would particularly affect HDB first-time buyers, though offsetting grants could mitigate the impact.

ABSD escalation on entities: Corporate and foreign entity purchases could face rates exceeding 70%, further discouraging institutional investors and offshore funds from treating Singapore residential property as an alternative asset class.

TDSR reduction: The 55% threshold could tighten to 50%, limiting borrowing power even further. This would reduce the quantum of debt banks could extend and force buyers to increase down payments or reduce property search prices.

Extended hold periods: SSD holding could extend beyond four years; MSR wait-out could lengthen beyond 15 months. A 5–7 year SSD period would effectively end short-to-medium-term flipping as an investment strategy.

Targeted HDB measures: Given HDB’s social mission, the government could ring-fence HDB buying further (e.g., longer wait-out periods for private owners, stricter owner-occupancy rules for upgrade purchases).

Differentiated ABSD by property type: Separate ABSD rates for landed (houses, land) vs. non-landed (condos, ECs) to focus cooling where prices are most extreme. Landed property prices have historically appreciated faster than condominiums, making them a natural target for stricter cooling.

Interest-rate floor adjustments: The MAS could raise the notional interest-rate floor used in TDSR/MSR calculations from the current 4% (private) to 4.5% or 5%, making loans seem more expensive during qualification, thereby reducing lending volumes.

These possibilities are illustrative, not predictions. The Government has consistently emphasised that cooling measures are reviewed against prevailing market conditions, and that any further recalibration — tightening or easing — will be driven by the data. Buyers and sellers should plan on the framework in force today and monitor MAS, URA, MND, IRAS and HDB announcements for updates.

Frequently Asked Questions

1. What’s the difference between ABSD and SSD?

ABSD (Additional Buyer’s Stamp Duty) is a tax paid by the buyer when purchasing a property (typically 2nd or 3rd+). It’s calibrated by buyer type (citizen, PR, foreigner, entity) and aims to dampen investment demand. SSD (Seller’s Stamp Duty) is a tax paid by the seller when selling within a holding period; it discourages flipping. Both reduce demand, but ABSD targets entry; SSD targets exit.

2. Are cooling measures permanent?

No. All cooling measures are policy tools, not constitutional laws. They can be eased or tightened depending on market conditions. For example, SSD was partially eased in March 2017, and TDSR has been adjusted twice (60% → 55%). The Government reviews the framework regularly against market conditions.

3. Can you appeal a cooling-measure penalty (e.g., SSD)?

No. Cooling measures are statutory levies applied uniformly. Once a property is sold within the SSD holding period, the duty is automatically calculated and due. There is no appeal mechanism, though you can seek professional tax advice if you believe your classification is incorrect. Early repayment of SSD (before expiry) is not available.

4. How do cooling measures affect HDB owners?

Cooling measures affect HDB owners primarily when upgrading (selling to buy private) or downgrading (selling private to buy HDB resale). HDB owners upgrading to private face ABSD. Private owners downgrading to HDB resale face a 15-month wait-out period and stricter MSR limits (30% vs. TDSR 55%). Cooling measures have also reduced HDB LTV to 75%, requiring larger down payments.

5. Do foreigners face the toughest measures?

Yes, unambiguously. Foreigners pay 60% ABSD (vs. 20% for SC 2nd property), and are excluded from some HDB categories altogether. The government’s policy framework explicitly prioritises owner-occupation for citizens and PRs over foreign investment. A foreigner buying a S$2M property pays S$1.2M in ABSD alone, making foreign residential investment significantly less attractive.

6. Will the government remove cooling measures if the market drops?

Possibly, but history suggests a “last in, first out” approach. When prices fell during COVID-19, cooling measures were retained (some were even tightened). The government views cooling measures as structural policy, not cyclical. However, if prices fell sharply and sustained (e.g., 15% decline year-on-year), measures like ABSD could be eased to stimulate demand. The government’s current stance (April 2026) is that stabilisation is preferable to rollback, unless emergency conditions warrant it.

This guide is for general information only and does not constitute legal, tax, or financial advice. Cooling measures are subject to change at any time by the relevant authorities (MAS, URA, IRAS, HDB). Interest rates, property values, and policy frameworks are subject to modification. Before entering into any property transaction, verify the current ABSD rates, SSD holding periods, LTV limits, TDSR/MSR thresholds, and any other applicable cooling measures with the Inland Revenue Authority of Singapore (IRAS), the Housing and Development Board (HDB), or the Monetary Authority of Singapore (MAS). Consult a licensed conveyancing lawyer and a qualified mortgage specialist or financial adviser to assess your personal circumstances and borrowing capacity. LovelyHomes.com.sg takes no responsibility for losses or liabilities arising from reliance on this article.

Seller’s Stamp Duty (SSD) is a tax payable by the seller when disposing of certain residential and industrial properties in Singapore within a specified holding period. Unlike Additional Buyer’s Stamp Duty (ABSD), which the buyer pays, SSD is borne entirely by the property seller.

Introduced in February 2010, SSD was designed as a cooling measure to deter short-term property speculation and encourage longer-term property ownership. Over the past 16 years, the rates and holding periods have changed multiple times in response to market conditions and Government policy objectives.

For sellers, understanding SSD is critical: it can significantly erode capital gains or even create a loss when selling within the holding period. Many property investors overlook SSD in their calculations and are shocked by the tax bill at completion.

Figure 1: The current four-year SSD ladder — 16%/12%/8%/4% on disposal value (IRAS, 2026).

Current SSD Rates in 2026 (Critical Update)

Quick Answer: What Are Today’s SSD Rates?

Residential properties: Depends on purchase date.

Purchased 11 March 2017 to 3 July 2025: 12% (Year 1) / 8% (Year 2) / 4% (Year 3) / 0% thereafter

Purchased on or after 4 July 2025: 16% (Year 1) / 12% (Year 2) / 8% (Year 3) / 4% (Year 4) / 0% thereafter

Industrial properties: 15% (Year 1) / 10% (Year 2) / 5% (Year 3) / 0% thereafter (unchanged since January 2013)

Commercial properties: 0% (retail shops, offices, no SSD applies)

Important: On 4 July 2025, the Government announced a significant restructure of residential SSD, effective for all properties purchased on or after that date. The holding period extended from 3 years to 4 years, and rates increased by 4 percentage points across all tiers.

Year of Disposal

Residential (Old: purchased ≤ 3 July 2025)

Residential (New: purchased ≥ 4 July 2025)

Industrial

Year 1

12%

16%

15%

Year 2

8%

12%

10%

Year 3

4%

8%

5%

Year 4

N/A

4%

N/A

Year 5+

0%

0%

0%

Figure 2: The July 2025 reset undid the 2017 easing — back to four years, up 4 percentage points per bracket.

A Brief History of SSD in Singapore

SSD rates have evolved significantly over the past 16 years, reflecting the Government’s shifting approach to cooling the property market:

February 2010: SSD introduced at 1% (Year 1) / 2% (Year 2) / 3% (Year 3) for sales within 1 year of purchase.

August 2010: SSD extended to cover sales within 3 years of purchase, maintaining the 1%/2%/3% rates.

January 2011: Rates escalated dramatically to 16% (Year 1) / 12% (Year 2) / 8% (Year 3) / 4% (Year 4) over 4 years, coinciding with the Global Financial Crisis aftermath and rising property prices.

January 2013: Industrial SSD introduced at 15%/10%/5% over 3 years, with no holding period extension thereafter.

11 March 2017: Residential SSD rates eased back to 12% (Year 1) / 8% (Year 2) / 4% (Year 3), and the holding period shortened from 4 years to 3 years. This marked a significant market cooling.

4 July 2025:Latest restructure: SSD rates for residential properties increased to 16% (Year 1) / 12% (Year 2) / 8% (Year 3) / 4% (Year 4), and the holding period extended back to 4 years. This applies to all properties purchased on or after 4 July 2025. Properties purchased before this date remain under the 12%/8%/4% regime (3-year holding period).

When Does SSD Apply? Key Conditions

SSD applies when all of the following conditions are met:

Property type: The property must be residential (private condo, terrace house, landed property) or industrial (factory, warehouse, B1/B2 zoned land). Commercial properties (retail shops, office units) are not subject to SSD.

Holding period: The property must be sold or disposed of within the holding period (3 years for pre-July 2025 purchases, 4 years for post-July 2025 purchases).

Disposal triggering event: The relevant date is when the Option to Purchase (OTP) is granted to the buyer or the Sale and Purchase Agreement (SPA) is signed, whichever is earlier. This date marks Day 1 of the holding period.

Acquisition date: The holding period starts from the date the OTP was exercised or the SPA was signed when you purchased the property (the date you acquired it).

SSD applies to most property disposals: sales to third parties, transfers to family members (unless specifically remitted), gifts, and even transfers in lieu of insolvency. The key trigger is the disposal date relative to the acquisition date.

HDB and SSD

Whilst SSD technically applies to HDB flats purchased after the legislative date (February 2010), in practice, SSD rarely applies to HDB owners because HDB imposes a Minimum Occupation Period (MOP). Most HDB flats have a 5-year MOP, meaning you cannot sell before 5 years have passed. By the time you can sell, the SSD holding period (3 or 4 years) has expired, and you owe no SSD.

However, if you own an HDB flat purchased before the SSD regime and sell early (during a defined period when some flats had shorter MOPs), SSD could theoretically apply. Consult your legal conveyancer for your specific flat’s MOP rules.

Executive Condominiums (ECs) and SSD

Executive Condominiums are subject to SSD if disposed of within the holding period after the MOP expires (typically 5 years). Once the MOP is completed and the property is decoupled from HDB rules, it is treated as a private residential property for SSD purposes.

Worked Examples: How SSD Is Calculated

Example 1: Private Condo Purchased January 2025, Sold June 2026

Scenario: You purchased a private condo on 15 January 2025 for S$1,800,000. You sold it on 20 June 2026 for S$2,000,000. At the time of sale, the property’s market value was assessed at S$1,950,000.

Analysis:

Purchase date: 15 January 2025 (before 4 July 2025 → old regime applies)

Sale date: 20 June 2026

Holding period: Approximately 17 months = Year 2

SSD rate: 8% (Year 2 rate under old regime)

Disposal value for SSD: Higher of sale price (S$2,000,000) or market value (S$1,950,000) = S$2,000,000

SSD payable: 8% × S$2,000,000 = S$160,000

Outcome: Despite a S$200,000 paper gain, you owe S$160,000 in SSD. Your actual net gain after SSD (and ignoring agent fees, legal costs, and ABSD if applicable to the buyer) would be only S$40,000—or entirely erased if other transaction costs are factored in.

Example 2: Private Condo Purchased March 2023, Sold April 2026

Scenario: You purchased a private condo on 10 March 2023 for S$1,600,000. You sold it on 5 April 2026 for S$1,750,000.

Analysis:

Purchase date: 10 March 2023 (before 4 July 2025 → old regime applies)

Sale date: 5 April 2026

Holding period: Approximately 3 years 3 months = beyond Year 3

SSD rate: 0% (holding period exceeded 3 years)

SSD payable: S$0

Outcome: You have held the property beyond the 3-year holding period, so no SSD is due. Your entire S$150,000 gain (less transaction costs and ABSD if applicable) is yours to keep.

Example 3: Industrial Property Purchased January 2025, Sold March 2026

Scenario: You purchased an industrial property (warehouse) on 20 January 2025 for S$2,000,000. You sold it on 15 March 2026 for S$2,100,000.

Analysis:

Property type: Industrial

Purchase date: 20 January 2025

Sale date: 15 March 2026

Holding period: Approximately 14 months = Year 2

SSD rate: 10% (Year 2 rate for industrial properties)

Disposal value for SSD: Higher of sale price or market value = S$2,100,000

SSD payable: 10% × S$2,100,000 = S$210,000

Outcome: Your S$100,000 paper gain is entirely wiped out by the S$210,000 SSD bill. You would need to pay S$110,000 from your own pocket to complete the sale. This illustrates why industrial property flippers face substantial tax penalties.

Example 4: New Regime – Residential Purchased July 2025, Sold November 2026

Scenario: You purchased a private condo on 10 July 2025 for S$1,500,000. You sold it on 15 November 2026 for S$1,650,000.

Analysis:

Purchase date: 10 July 2025 (on or after 4 July 2025 → new regime applies)

Sale date: 15 November 2026

Holding period: Approximately 16 months = Year 2

SSD rate: 12% (Year 2 rate under new regime)

Disposal value for SSD: S$1,650,000

SSD payable: 12% × S$1,650,000 = S$198,000

Outcome: Under the new, stricter regime, even a modest 10% appreciation is swallowed by a 12% SSD rate. The sale results in a net loss of approximately S$48,000 (before other transaction costs).

How SSD Is Calculated: Disposal Value

A critical point: SSD is calculated on the higher of the selling price or the market value of the property as at the date of sale.

If you sell below market value (e.g., to a family member at a discount, or in a distressed sale), the property’s assessed market value may still be used by IRAS to compute SSD. You cannot reduce your SSD bill by negotiating a lower sale price.

Market value is typically determined by a professional valuation, comparable sales data, or IRAS’s own assessment. If you believe IRAS’s valuation is incorrect, you can request a review, but the onus is on you to provide supporting evidence.

How to Legally Avoid or Minimise SSD

SSD is a significant liability for property sellers. Fortunately, several legitimate strategies exist:

1. Hold for the Full Period (3 or 4 Years)

The most straightforward approach: Hold your residential property for at least 3 years (if purchased before 4 July 2025) or 4 years (if purchased after) before selling. Once the holding period expires, SSD drops to 0%, and you keep your entire gain.

For industrial properties, hold for 3 years to eliminate SSD.

This strategy is ideal if you can afford to hold the property long-term. Many professional investors plan around these holding periods when structuring their portfolios.

2. Timing the OTP Carefully (Within Limits)

The key holding-period dates are:

Start date: The date you exercised the OTP or signed the SPA when you purchased the property.

End date: The date you granted the OTP to the buyer or signed the SPA when you sold the property.

If you purchased on 10 January 2025, the 3-year threshold is reached on 10 January 2028. If you can delay granting your buyer’s OTP until 10 January 2028 or later, SSD drops to 0%.

However, there are strict limits: You cannot artificially delay the OTP grant date if you have already agreed to sell. Doing so could constitute a breach of contract or fraud. The dates must reflect genuine transaction timings.

3. Properties Exempt or Remitted from SSD

Certain disposals qualify for full SSD remission or exemption:

Compulsory Acquisition (CA) by the Government: If your property is acquired under the Land Acquisition Act (e.g., for public housing, roads, or infrastructure), SSD is fully remitted.

Developer Repurchase: If a property developer repurchases a unit within a stipulated period (e.g., within 5 years of the original sale for some EC schemes), SSD may be remitted under the scheme’s terms.

Matrimonial Property Transfer: Transfers of residential property between spouses or ex-spouses as part of matrimonial or ancillary relief proceedings may qualify for remission if executed pursuant to a Court Order. However, this is a narrow exemption—consult a legal advisor.

HDB Repurchase by HDB: If HDB repurchases a flat from you (e.g., under right of first refusal schemes), SSD is typically remitted.

Bankruptcy or Insolvency: In certain insolvency situations, SSD may be remitted if the property is disposed of by a trustee or official receiver under court order.

These exemptions are narrow and require specific conditions. If you believe you qualify, consult a licensed conveyancing lawyer or contact IRAS directly for a ruling.

4. Decoupling Strategy (With Caution)

If you are married and own property as joint tenants, decoupling (transferring one spouse’s share to the other spouse) creates a new acquisition date for the transferred share. This means the holding period for that share restarts.

Example: You and your spouse bought a property jointly on 1 January 2025. On 1 July 2026, you transfer your spouse’s share to yourself. Your spouse’s share now has a new acquisition date (1 July 2026), so its holding period restarts. If you then sell the entire property on 1 January 2027, your share is subject to Year 2 SSD, but your spouse’s share (which was only held from July 2026 to January 2027 = 6 months = Year 1) would trigger Year 1 SSD on that portion.

This strategy is complex, has significant stamp duty and ABSD implications, and may not be worthwhile. Do not attempt without guidance from a tax professional and conveyancer.

5. Beware: Legitimate Avoidance vs. Tax Evasion

There is a clear legal line between legitimate tax planning and tax evasion:

Legitimate: Holding the property longer, timing transactions around the 3-year mark, claiming available exemptions.

Illegal: Falsifying transaction dates, under-declaring the sale price, splitting the sale into multiple transactions to circumvent SSD, or using straw buyers.

IRAS actively audits property transactions and has recovered substantial SSD arrears from taxpayers who attempted to evade the tax. The penalties (including interest and potential prosecution) far exceed any tax saved.

Figure 3: ABSD is charged when you buy; SSD is charged only if you sell within the holding period.

SSD vs. ABSD: What’s the Difference?

Many property sellers confuse SSD (Seller’s Stamp Duty) with ABSD (Additional Buyer’s Stamp Duty). They are separate taxes and can both apply to a single transaction:

Aspect

SSD (Seller’s Stamp Duty)

ABSD (Additional Buyer’s Stamp Duty)

Payable By

Seller

Buyer

When

At sale, if property sold within holding period (3 or 4 years)

At purchase, if buyer is foreigner, company, trust, or owns other properties

Applies To

Residential & industrial properties only

Residential properties only (no ABSD on industrial)

Purpose

Deter short-term speculation by sellers

Deter foreign ownership & multiple property purchases by buyers

Example Rate

12% (Year 1, old regime) or 16% (Year 1, new regime)

Key Point: Both SSD and ABSD can apply to a single transaction. If a Singaporean citizen (owner) sells a residential property within 3 years to a foreign buyer (or to another Singaporean who already owns 1+ properties), the seller pays SSD and the buyer pays ABSD. Each is computed on the transaction price and borne by the respective party.

Frequently Asked Questions (FAQ)

Q1: Who decides what the “disposal value” is for SSD calculation?

A: The disposal value is the higher of the actual selling price or the property’s market value as at the date of sale. If you sell at S$2M but IRAS assesses the market value at S$2.2M, SSD is computed on S$2.2M. You can appeal IRAS’s valuation, but the burden is on you to prove the value with evidence (comparables, professional appraisals). In most cases, the selling price is the disposal value, unless it is significantly below market (a rare event).

Q2: Can I use my CPF to pay SSD?

A: No. SSD is a seller’s cost and must be paid from the sale proceeds or your own funds. CPF can only be used to purchase residential property and to pay the conveyance duty (stamp duty) on the purchase itself, not on the sale or SSD. SSD is withheld from your sale proceeds at completion.

Q3: Does SSD apply if I gift my property to a family member?

A: Yes, in principle, SSD applies to gifts unless a specific remission is granted. The “disposal value” for a gift is the property’s market value (since there is no actual sale price), and SSD is computed on that value. However, if the gift is part of a matrimonial order or compulsory acquisition, remission may apply. For most family gifts without legal exemption, SSD is payable by the donor (gift-giver). Consult a lawyer before gifting property if within the holding period.

Q4: Does SSD apply if I inherited the property?

A: No, SSD does not apply to inherited properties. Inheritance is not a “disposal” triggering SSD; it is a transmission of title by operation of law upon death. Your holding period for SSD purposes starts from the date the original buyer (the deceased) purchased the property. If the deceased held it for more than 3 years before dying, there is no SSD when you (the heir) subsequently sell. If the deceased had held it less than 3 years and you sell shortly after, you may owe SSD, but the holding period is measured from the original purchase date, not your inheritance date.

Q5: Does SSD apply to HDB flats?

A: Technically, yes—SSD applies to HDB flats purchased after February 2010. However, in practice, SSD rarely triggers for HDB owners because HDB imposes a Minimum Occupation Period (typically 5 years). Once you can sell (after MOP), the SSD holding period has usually expired. If you own an older HDB flat or one with a shorter MOP and sell within the holding period, SSD would apply. Check your flat’s MOP with HDB before selling early.

Q6: Can I get SSD back if the buyer backs out?

A: SSD is paid at completion of the sale (when the sale is finalised and transferred to the buyer). If the buyer backs out before completion, the sale does not complete, and SSD is not triggered or payable. If the sale completes and you have paid SSD, but the buyer later defaults or the sale is reversed (rare), you would need to seek legal remedy or negotiate a refund directly with the buyer. IRAS does not refund SSD unless the underlying transaction is formally set aside by Court order.

Q7: How is SSD calculated on an incomplete property (Build-to-Completion, BUC)?

A: For a property sold before completion of construction (i.e., before the Completion Certificate is issued), SSD is calculated on the contract price (as stated in the SPA or OTP), not the actual completion value. The holding period is measured from the date the OTP was exercised on the original purchase. If you resale a BUC unit within the holding period, SSD is due on the resale price. This is an area where many investors get caught—ensure you understand the SSD implications before flipping an off-plan property.

Q8: What happens if I sell a property that is jointly owned with my spouse?

A: If you and your spouse own a property as joint tenants or tenants-in-common, the sale price is shared (usually 50/50 unless another ratio is agreed). SSD is calculated on the full sale price, but it is paid from the joint sale proceeds. The holding period is the same for both owners (it starts from the date the property was first acquired). No special relief applies merely because of joint ownership; both spouses are treated as single sellers of a single property. If you decouple (transfer one spouse’s share to the other), the transferred share gets a new acquisition date, which can complicate SSD calculations.

Q9: Can I defer or spread SSD payments over time?

A: No, SSD must be paid in full at the point of completion (when the sale is finalised). There is no option to spread the payment or defer it. Your conveyancer will calculate the SSD owed and ensure it is deducted from the sale proceeds before you receive your net amount. If you cannot afford the SSD, the sale cannot complete, and you remain the owner.

Q10: Are there any SSD changes coming in 2026/2027?

A: As of April 2026, no further changes to SSD have been announced. The most recent restructure took effect on 4 July 2025 (16%/12%/8%/4% over 4 years for properties purchased on or after that date). Keep monitoring IRAS’s official website and Government budget announcements for any future changes. However, do not assume changes; rely only on official announcements from IRAS and the Ministry of Finance (MOF).

This guide is provided for general informational purposes only and does not constitute legal, tax, financial, or investment advice. SSD rates, holding periods, and exemptions are subject to change at the discretion of the Government of Singapore and the Inland Revenue Authority of Singapore (IRAS).

Consult a licensed conveyancing lawyer to understand your specific SSD liability based on your property’s purchase and sale dates.

Obtain a professional valuation if you believe the market value of your property may differ significantly from the sale price.

Contact IRAS directly for clarification on any specific scenarios or exemptions that may apply to your situation.

Property laws change, and individual circumstances vary widely. LovelyHomes.com.sg and its authors assume no liability for actions taken based on this guide. Always seek independent professional advice before committing to a property transaction.